CA - Canada Goose: Undervalued Luxury

2023-10-13 16:29:32 ET

Summary

- Luxury conglomerates are struggling with demand overhang as consumers pulled forward purchases into the pandemic period.

- Canada Goose stock has declined nearly 30% this year, presenting a great opportunity for long-term investors.

- The company's fundamentals, including high gross margins, direct channel sales, product expansion, and global market potential, support a bullish outlook.

- The company's ~13x P/E is overdue for a rebound, especially with expectations for double-digit growth and EPS/EBIT expansion this year.

It's been splashed across the news: luxury conglomerates like LVMH are struggling with a demand overhang, as consumers pulled forward purchases into the pandemic period when they were feeling more flush and are now dealing with more constrained budgets. As macroeconomic malaise continues around the world, driven in part by high interest rates, retail and consumer stocks continue to drop.

Canada Goose ( GOOS ) has seen its share of pain this year as well, with the stock receding nearly 30% this year to land at $13. Amid this carnage, I think there's a great opportunity for long-term oriented investors to step in.

The line chart above looks like a falling knife, but when stacking up Canada Goose's fundamentals against this decline, I see tremendous opportunity here. Though my bullish position on Canada Goose has not worked out great so far, I remain bullish and continue to believe a rebound here is long overdue.

The long-term thesis for Canada Goose

As a reminder for investors who are newer to this stock, here is my updated bull case for Canada Goose:

- $1,000+ parkas have given Canada Goose a rich gross margin profile: Canada Goose's high-60s gross margin puts the company more akin to a tech stock than a consumer products manufacturer. Canada Goose's incredible brand moat has also allowed the company to increase prices to offset inflationary pressures, actually even leading it to expand its gross margin profile.

- Shift into direct channel sales will stabilize revenue profile and improve margins: As the company rationalizes its fleet of reseller relationships, more and more revenue is being attributed to Canada Goose's direct channel at full price. This is both a tailwind to gross margins and will have a stabilizing impact on revenue trends (as less of Canada Goose's revenue will be subject to the timing of when channel partners load up on inventory).

- Product category expansion: With ambitions beyond just being a parka brand, Canada Goose has made significant strides in expanding into other categories, most notably footwear. The company also has a lineup of accessories like scarves and gloves, as well as a full kids selection.

- Huge untapped global luxury market: At the moment, Canada Goose is very popular in its home markets of the U.S. and Canada. It's expanding aggressively into Mainland China, which is the world's biggest consumer of luxury goods; and it's still largely new in Europe. The opportunities for global expansion here are unparalleled.

The outlook for FY24 calls for immense profit growth

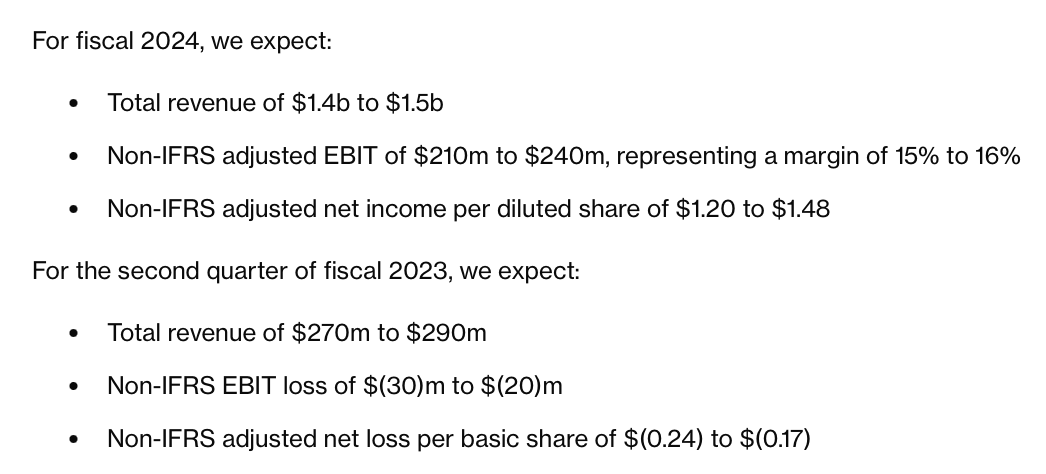

Canada Goose's outlook for fiscal 2024, which is the year for Canada Goose ending next April, calls for substantial growth in spite of an expectation of declines in wholesale revenue (driven both by existing channel partners being more cautious on loading up inventory, as well as an expected shrinkage of the company's wholesale door count).

Take a look at the outlook below:

Canada Goose FY24 outlook (Canada Goose Q1 earnings release)

{kind=link}

The company's expectation of C$1.4-$1.5 billion in revenue represents top-line growth of 15-23% y/y.

Note that this outlook contemplates both an expected -6% y/y decline in wholesale revenue and a -6% y/y shrinkage in "door count" of reseller partners. In turn, the company expects DTC to grow to a "mid to high 70s" percentage of overall revenue.

This will be a substantial boon to margins. The company's expected adjusted EBIT of C$210-$240 million, or a 15-16% EBIT margin, is much richer than 175.1 million in EBIT in FY23 at a 14.4% margin.

While many investors are worried about Canada Goose's brand visibility as its reseller network shrinks, I don't think it's a completely negative thing when a high-end luxury brand centralizes its sales and exercises more control over merchandising and pricing. As long as the expected wholesale shrinkage is not expected to materially harm growth (which expectations of double-digit revenue growth this year are clearly saying is not true), my concern here is minimal. In my view, an expensive product like Canada Goose is a highly intentional purchase - people don't tend to walk into a store, run into a coat and decide to buy it. Reducing the number of partners carrying Canada Goose inventory increases the share of these intentional buyers purchasing directly from Canada Goose, at full price for the company without trade discounts.

Recent trends

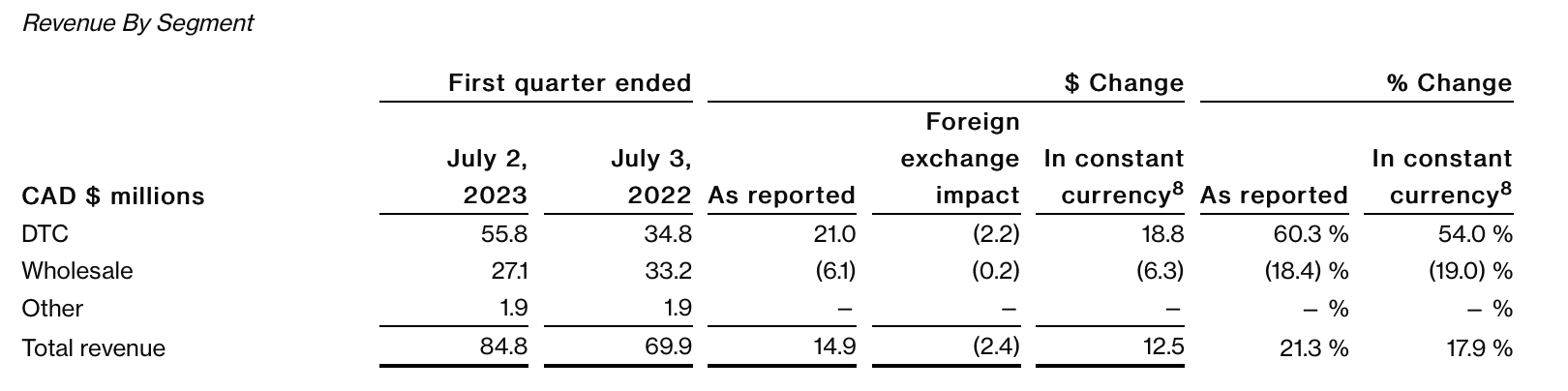

Canada Goose has results out for the first quarter ending in June, but as a reminder, the June quarter is a seasonal low for the company. Canada Goose expects Q1 to be just 5% of full-year revenue, with Q2 contributing 20%, Q3 50%, and Q4 25%.

Nevertheless, since Q1 consisted primarily of direct-channel trends, we can parse through some of the key themes that will dominate this year.

Canada Goose channel trends (Canada Goose Q1 earnings release)

{kind=link}

First, as shown above, DTC revenue grew 54% y/y on a constant-currency basis, while wholesale revenue declined 19% y/y. DTC represented 66% of overall Q1 revenue, as the company marches toward a high-70s target for the balance of the year.

{kind=link}

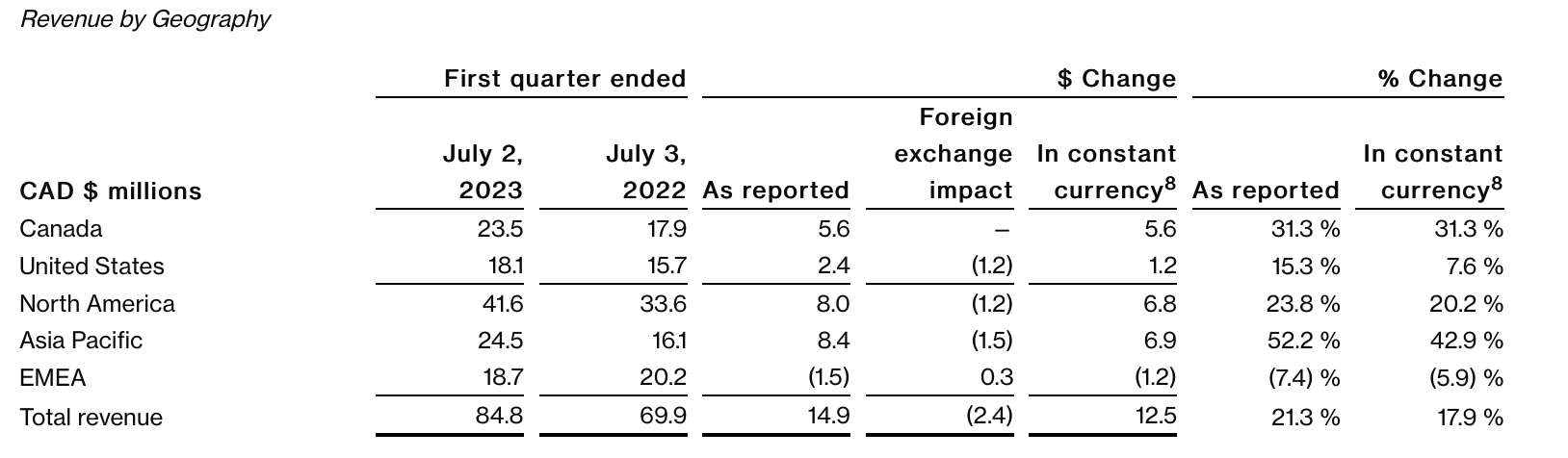

Also interesting is the fact that on a geographical basis, Europe saw broad weakness with a -6% y/y constant currency decline (consistent with LVMH's woes), but Asia Pacific grew 43% y/y, demonstrating strong growth in China.

The company also notes that non-heavyweight categories helped boost direct channel sales in Q1. Per CFO Jonathan Sinclair's remarks on the Q1 earnings call:

We saw a higher proportion of new and existing consumers entering our non-heavyweight down categories and demonstrating significantly higher interest in apparel. We also gained traction with women in the US, which is one of our top markets for this segment. Share of revenue increased within the country's mix compared to the same period last year with our rain, every day and lightweight down pieces resonating with women. Our progress in Q1 further strengthens our belief in our long-term US retail expansion strategy, while also continuing to grow DTC comps as we continue to navigate the uncertain economic environment."

Valuation and key takeaways

At current share prices of $13, Canada Goose trades at just a 13.4x P/E against Wall Street's $0.97 consensus EPS expectations for this year (Canada Goose's C$1.20-$1.48 in EPS guidance for this year translates to a $0.88-$1.08 range in dollars, using today's spot rate of C$1.37 to the dollar).

Considering an expanding margin profile, double-digit growth, and many tailwinds for further growth (non-parka product expansion, China) - I'd say there are plenty of reasons to be optimistic. Stay long here.

For further details see:

Canada Goose: Undervalued Luxury