CA - Canadian Apartment Properties: Exposure To Growing Markets Keeps The Stock Expensive

2023-05-26 10:30:32 ET

Summary

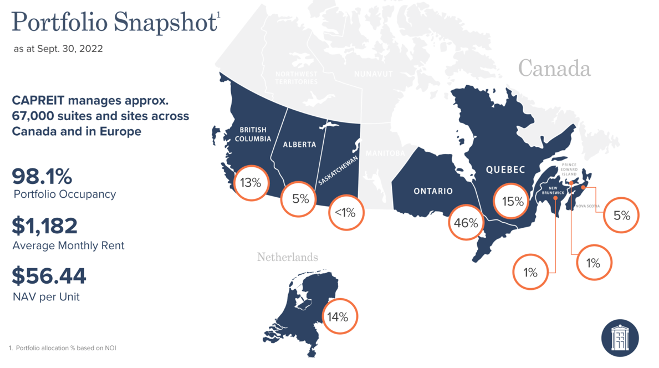

- The REIT owns 86% of properties in Canada and 14% in the Netherlands.

- Both of these are good markets which have seen some of the fastest growth, but also have record low levels of new supply.

- As much as I’d like to invest in these markets, the market is not giving me a chance as the stock remains expensive.

The first Canadian apartment REIT I covered was Killam Apartment REIT ( KMP.UN:CA ). In that article I discussed the Canadian Real Estate market in detail so I encourage you to check it out. To recap quickly, the market North of the border has seen much higher growth than the US, especially when on an inflation-adjusted basis. Not only that, but the increase in prices has actually been the highest in Canada out of all G7 countries at around 400% since 1975 (followed by the UK at around 350% and the US at just 150%). That’s meaningful growth, but again, it doesn’t necessarily mean that it has to reverse any time soon.

To better understand why prices have quadrupled over the past 50 years (inflation-adjusted), we have to understand a couple of things about the Canadian market. Firstly, it has a growing population due to very aggressive immigration policies that the government has had for a while. With an influx of people, it’s obvious that more housing will be needed or else prices will get out of control. And this is where the problem lies, there haven’t been enough apartments, because the supply has been low. It’s really that simple. This is why I actually like investing in Canadian real estate and especially apartments despite much higher price increases. With a low supply and increasing construction costs which are being fueled by inflation, it’s quite unlikely that developers will reduce their prices. In fact, I expect the opposite. Of course, older second hand properties could see a temporary decline if for example unemployment spikes up because so far we have seen no indication of that happening. To conclude that prices must come down simply because they grew a lot would be foolish in my view. This is why I want to cover another Canadian based apartment REIT today – Canadian Apartment Properties ( CAR.UN:CA , [[CDPYF]]).

The company has 86% of their properties located in Canada, with Ontario being the highest weighted province at 46%. Of the total of nearly 70,000 units, 14% are located in the Netherlands which happens to be where I currently live and study. This is why I can tell you from personal experience, that the market is hot here. Vacancies are near zero, it’s still nearly impossible to find an apartment to rent without engaging in a price war with other interested renters and the lease terms are very one sided in favor of the landlord (deposits of 3 month’s worth of rent with 3 month’s of rent paid upfront are not uncommon). So yes, I like their geographical presence a lot and expect the portfolio to do well.

{kind=link}

An important point to touch on is rent regulation. This is not something that happens in the Netherlands, but is the norm in Canada. This is a slight risk factor in a high inflation environment because the REIT can only raise rents so far and usually regulated rents lag market level rents. For 2023 for example, landlords are only allowed to raise rents by 2-2.5% depending on the province. Regardless, the REIT has been able to maintain a solid level of occupancy above 98% and given the housing shortage, I really don’t see this changing any time soon. Going forward, with limited same store NOI growth due to regulation in Canada, the REIT is dependable on new acquisitions for growth. Luckily, the REIT has been doing just that. Their FFO is expected to grow by 3-5% for the next 3 years and should reach $1.87 per share by 2025.

A monthly dividend of $0.1208 per share translates to a forward yield of just under 3%. Frankly that’s relatively low, compared to its US peers, that are closer to the 4% mark. Still, if you’re seeking exposure to Canadian Real Estate, you’ll probably not find much better yield with a similar risk profile. Though not the highest, the dividend is covered by a payout ratio of 80%.

That brings me to valuation and I have to say, the REIT is not cheap. It trades at 21x FFO which is in line with its historical average since the Financial Crisis and actually above the average since it began – though that’s to be expected with real estate prices appreciating so much. In either case, it’s hard to see the stock as undervalued here and with a dividend yield of just 3%, I don’t see much potential here beyond a standard 8% return. Although I really like their geographical exposure, I rate CAR.UN as a HOLD because I don’t see it as undervalued.

For further details see:

Canadian Apartment Properties: Exposure To Growing Markets Keeps The Stock Expensive