CA - Canadian Apartment Properties REIT: Rethinking The MHC Strategy

2023-05-01 11:17:35 ET

Summary

- CAPREIT's MHC portfolio has underperformed the larger multi-family residential portfolio.

- The REIT's residential portfolio is poised for substantial growth in rents as leases turnover. The MHC segment is not anticipated to participate fully in these potential rental rate increases.

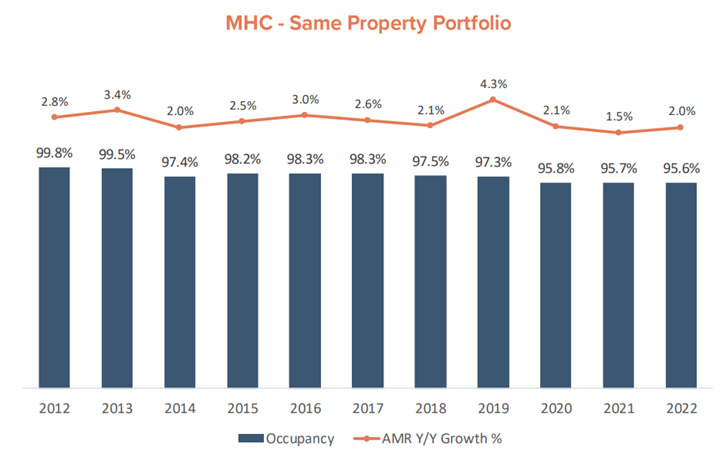

- CAPREIT’s core residential portfolio has current occupancy rates of 98.9%, the MHC portfolio has lagged at 95.6% as of 2022.

Author's Note: All currency reported in Canadian Dollars unless otherwise stated.

Canadian Apartment Properties Real Estate Investment Trust ( CAR.UN:CA ) ( CDPYF ) or "CAPREIT" is Canada's premier multi-family residential REIT. The REIT owns a large portfolio of residential properties in Canada and the Netherlands as well as a portfolio of manufactured housing community ("MHC") sites. Despite these MHC site assets being Wall Street darlings, this MHC portfolio has underperformed the larger residential portfolio and looks set to continue to.

For a closer look at CAPREIT core business and operations, please see my previous coverage here and here.

| CAPREIT Scorecard By Property Type |

| Residential Portfolio |

| MHC Portfolio |

| Occupancy |

| 98.9% |

| 95.6% |

| 2022 NOI Growth |

| 7.8% |

| (1.6%) |

| NOI Margin |

| 64.5% |

| 56.5% |

| 2022 Net YoY AMR* Growth |

| 5.2% |

| 2.8% |

*Average monthly rent

MHC Portfolio - Trailing Returns

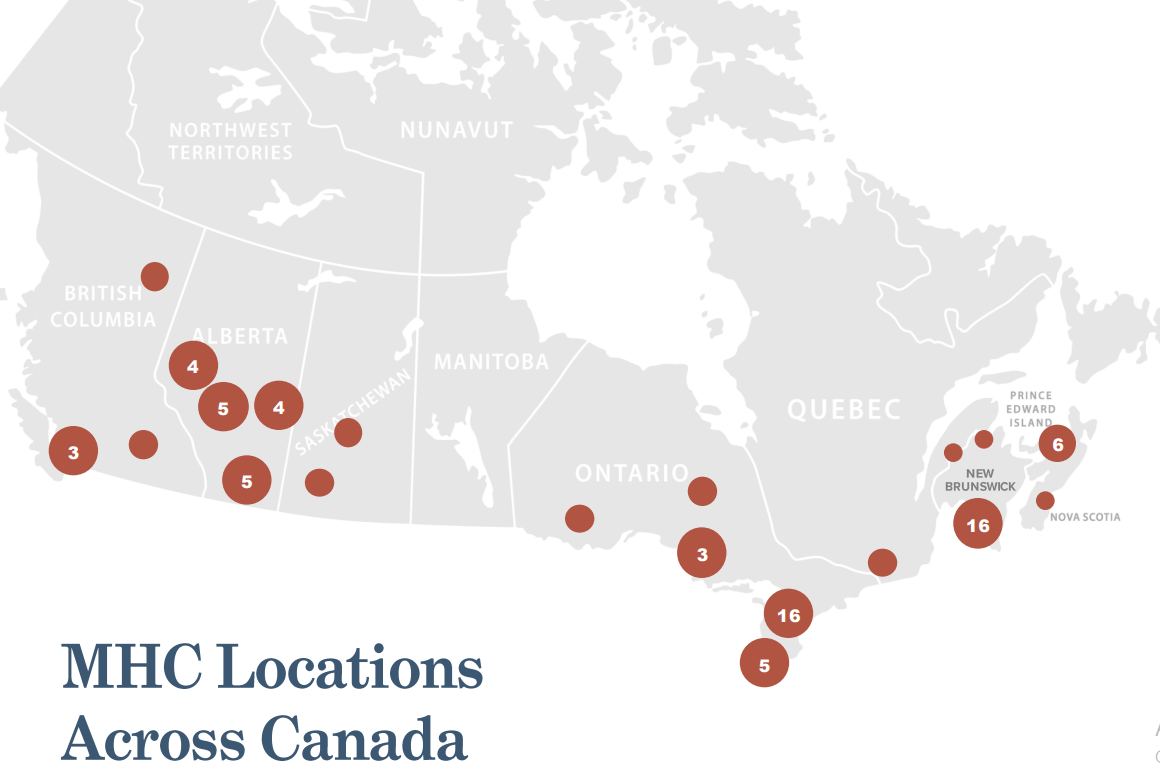

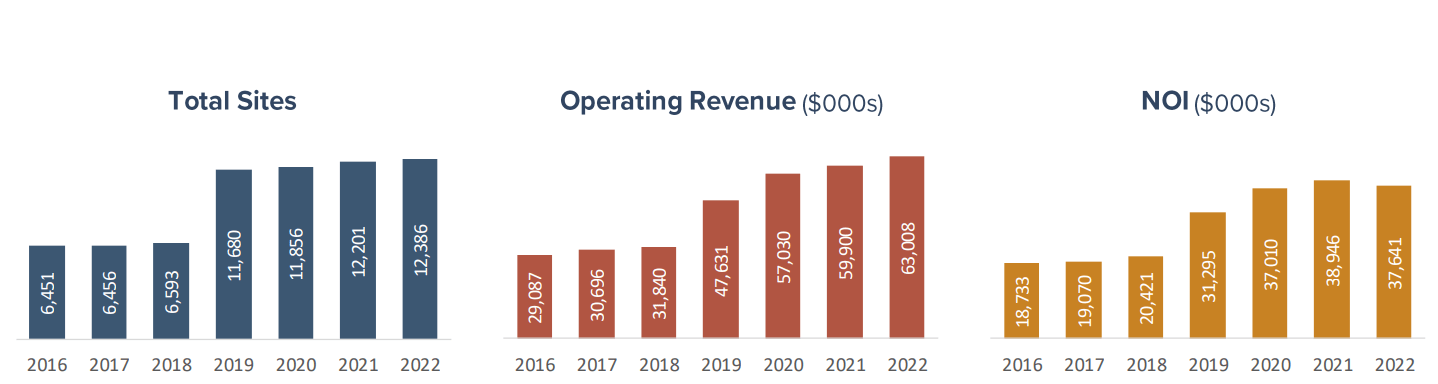

With 12,386 MHC sites across 77 communities, CAPREIT is the second-largest owner of MHCs in Canada. CAPREIT collects pad fees for these sites and provides supporting infrastructure to tenants. The average occupied rent for these sites was $425 monthly in 2022 with 95.6% occupancy. Tenants own their homes, while CAPREIT owns the land.

CAPREIT MHC Portfolio (CAPREIT)

{kind=link}

Modern manufactured homes are not trailers. Instead of trailer hitches and wheels; these are prefabricated, energy-efficient, modular housing units, built on assembly lines. Once delivered, to a community site, manufactured homes ranging in size from 500-1,800 square feet are set on concrete blocks and connected to utilities. A typical manufactured home will range in price from $120,000 to $350,000 for deluxe models. In Canada, there are more than 190,000 households living in manufactured homes, the majority of owners are 55 years or older. With relatively low purchase and monthly costs, MHCs are an attractive affordable housing alternative for more than 20 million North Americans.

These land lease sites tend to be located in or near major urban centers and are characterized by low operating costs and steady occupancy. In recent years, many asset management firms have looked to manufactured home communities for superior returns. Some of the largest investment services firms, including the Blackstone Inc. ( BX ), Apollo Global Management ( APO ), Brookfield Asset Management ( BAM ), Stockbridge Capital Group, and the Carlyle Group Inc. ( CG ) began buying MHCs in the early 2010s. Asset management firms are attracted to MHCs for their location, their limited supply and their low operating costs. MHC sites are often 1960s-1970s era properties built on large tracts of valuable land in urban and suburban areas, making them attractive for future densification or divestment plays.

Manufactured or mobile homes are not actually that mobile, with moving costs estimated at $5-10K per unit. This makes for lower turnover in MHC sites and stable occupancy. MHC communities are often seen as more affordable alternatives to renting apartments or home ownership. As this housing option exists at the lower end of the cost spectrum, there are fewer alternatives down market for consumers. As a result, owners of these assets have significant pricing power. The ability to increase pad fees at higher rates than other segments of the real estate market has resulted in the broad financialization of MHCs in recent years and has made these properties a favorite for asset managers.

MHC Segment Underperformance

In 2022, MHC NOI accounted for 5.5% of CAPREIT's total NOI, down from 5.9% in 2021. Year over year, NOI in the MHC segment shrunk by 1.6%, while the core residential portfolio grew by 7.8%. Not only did NOI fall during this period, NOI margins shrunk almost 6% from 62.4% to 56.5%. CAPREIT noted that approximately 5% of this NOI margin impact was attributable to the $815K in septic tank maintenance. This compression is against a wider backdrop of margin expansion of 70bp in the residential suite segment.

CAPREIT MHC Performance (CAPREIT)

{kind=link}

This margin compression within the MHC business is the result of a string of issues with infrastructure at multiple sites, including septic tank replacement costs. Not only have capital costs increased to deal with tank replacements, the operating costs have spiked as CAPREIT has had to arrange septic service by trucks on some sites. On the company's recent earnings call , Management addressed analyst's questions about the poorly performing MHC segment:

Julian Schonfeldt, Chief Investment Officer

So we've been looking -- we've been working with the ministry and with some of our vendors to mitigate or lower the hauling costs as much as possible. And on my end, to the extent that I can do it effectively, I'm going to look to dispose at appropriate values, some of the worst spenders. This is certainly tough assets to get liquidity on, but it's something we're exploring and making sure that we do at prudent price levels.

Stephen Co, Chief Financial Officer

I mean I would also just add on that front that the high grading of the CAPREIT portfolio is moving into our image sector as well. We love this sector, but we're taking, with the help of our asset management team, a much closer look at returns. We love the tradition [is] to love the sector. Now we're looking to love the returns. So, more realignment in total return will help drive the high grading of the MH[C] portfolio as well.

For 2022, the MHC portfolio accounted for 10% of non-discretionary capital deployment, while the segment only accounts for 5-6% of NOI. At almost double the capital maintenance cost on an NOI basis, the quality of the MHC portfolio as it relates to deferred maintenance liabilities comes into question. This question of quality is reflected in occupancy rates as well that have declined independently of property acquisition timelines.

CAPREIT MHC Occupancy (CAPREIT)

{kind=link}

While CAPREIT's core residential portfolio has current occupancy rates of 98.9%, the MHC portfolio has lagged at 95.6% as of 2022. In addition to the 3.3% spread in occupancy rates between the two segments, they have been trending in opposite directions. As new housing formations have been slowed by higher interest rates and high residential occupancy during the pandemic, one would expect the MHC portfolio to be a strong beneficiary of the demand for affordable housing options in Canada's large centers.

CAPREIT's execution of its MHC portfolio has been disappointing in the past few quarters. The company remains committed to this strategy, and I anticipate that CAPREIT will be able to unlock value from these properties in the future. While the MHC segment only accounts for 5% of the company's asset base, it has been the recipient of $337M in investment to scale up the portfolio since 2017. This compares to approximately $1.16B invested in new building development over the same period. As of Q4 2022, the fair value estimate for these MHC properties is $713M with a cap rate of 5.94%, well above the portfolio average of 3.93%. As CAPREIT systemically recycles assets in its portfolio with a focus on disposing of older properties in favor of newer apartments, it may consider trimming some of its MHC sites with aging infrastructure as well.

Rental Increases

In Q3/22, residential rents across CAPREIT's portfolio grew 14% on the 5% of properties turning. In the fourth quarter, rent on new leases grew a staggering 24% on 3.4% of the portfolio turning. Residential property rent has grown approximately 6% annually on average over the long term and up to 10% over the past year. This far exceeds the long-term average monthly rent increases in the MHC portfolio, which have averaged just 2.57% over the last decade. The core residential segment is poised to benefit tremendously as additional turnover will release the pent-up rental increases to be unlocked during release. The MHC portfolio is unlikely to participate in the opportunity to increase rent in the same fashion as MHC sites have lower turnover due to the higher switching and moving costs of occupants.

CAPREIT Lease Turnovers (RBC Global Markets)

Retuning Capital

In 2022, CAPREIT aggressively pursued its NCIB, having acquired 5.2M units at an average price of $45.44/unit for a total of $238M. This capital has been harvested through dispositions of older apartment buildings. In March 2023, CAPREIT renewed an NCIB to purchase up to 16,901,348 units, representing approximately 10% of public float. At the end of Q4 2022, CAPREIT had approximately $381 million of liquidity, representing cash and cash equivalents on hand and available liquidity.

Recent divestments including the January 2023 sale of a 50% non-managing interest in three assets in Ottawa for $136.25M has added to that cash balance. CAPREIT noted that the cash proceeds are " intended for redeployment into accretive new-build opportunities in attractive markets and CAPREIT's value-enhancing NCIB program."

On the most recent earnings call, Julian Schonfeldt, Chief Investment Officer, spoke to CAPREIT's priority to allocate capital to its NCIB program:

By selling noncore assets at or above NAV and repurchasing units at a major discount to NAV, we are arbitraging the significant spread and realizing immediate value for our unitholders. To date, CAPREIT has invested over $245 million in our NCIB program with the purchase of 5.4 million units at an attractive average price of approximately $45 per unit, which is well below our $58.1 year-end net asset value per unit. We will continue to stand by CAPREIT's strong fundamentals and invest in our own portfolio of increasing quality as long as it is prudent and economical to do so.

The aggressive nature of this NCIB program signals that the company sees units as undervalued. While the discount to NAV has compressed in recent months, units are trading at approximately 20X 2023 FFO and are still trading below NAV of $53.00. If the REIT is successful in disposing of some of its highest-spending MHC sites, it may have additional opportunities to exercise its NCIB with the proceeds.

Investor Takeaways

CAPREIT's real value right now is in its pent-up residential unit leases that have not turned over since the pandemic. Same property turnover has generated strong increases in rent. With lower turnover, lower margins and lower occupancy, CAPREIT's MHC has not participated to the same extent in this opportunity for same-property NOI growth. While the MHC segment has potential and is attractive for its low capital requirements, in the current rental environment, CAPREIT is better off unlocking value by optimizing its residential portfolio and investing in development in my view.

For further details see:

Canadian Apartment Properties REIT: Rethinking The MHC Strategy