UNP - Canadian National Railway: Better To Wait For The Next Train

2023-12-19 05:44:20 ET

Summary

- CNR is the most competitively-advantaged railroad.

- An attractive footprint, unique access to some ports and fluidity advantage are few examples of its strength.

- Current valuations are not attractive enough to be a buyer.

Company overview

Founded in 1919, Canadian National Railway ( CNI )( CNR:CA ) operates one of the smallest rail networks in North America. Its three-coast Y-shaped network is 18,600 route miles long and spans Canada from east to west and down through the U.S. Midwest up to the US gulf coast. Railroads own the rail tracks (including the land on both side of the track) and operates their rail networks, locomotives, and rail cars. While some passenger railroads may use their network, railroads deal only with freight transport.

Industry overview

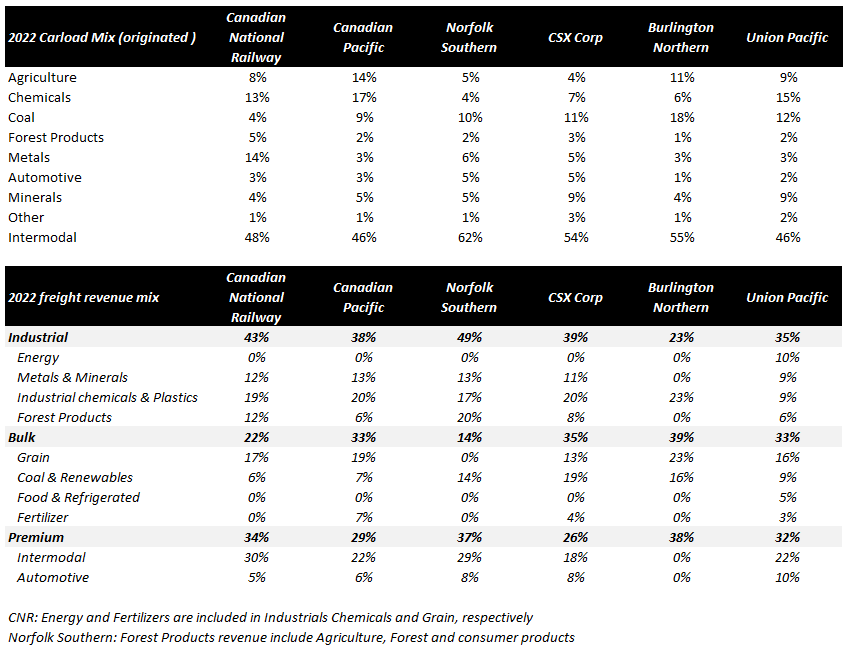

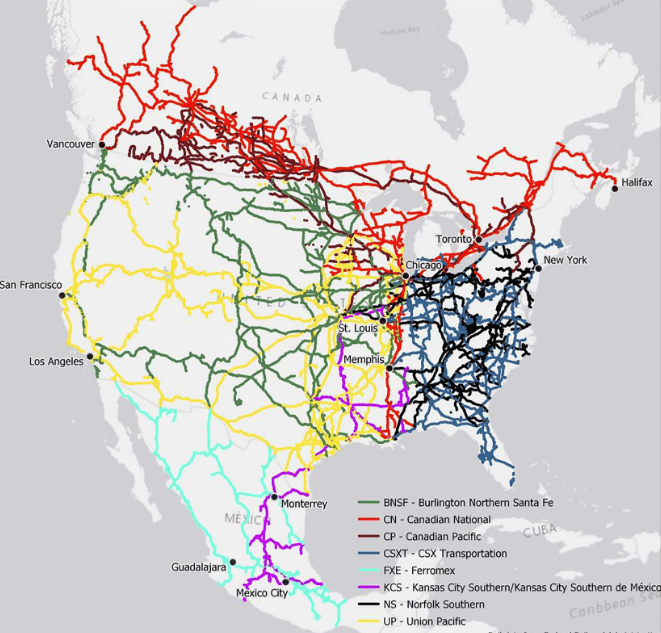

In short, the industry is highly consolidated with six class 1 railroads operating in regional duopoly. Canadian National Railway and Canadian Pacific ( CP ) cover the Canada from coast to coast and down through the Midwest to the Gulf of Mexico (and even Mexico in the case of CP), CSX ( CSX ) and Norfolk Southern ( NSC ) operate east of the Mississippi River covering one-third of the US while Union Pacific ( UNP ) and Burlington Northern Santa Fe (owned by Berkshire Hathaway) operate on the western part of the river and cover two-third of the US.

{kind=link}

While rail transportation is less flexible and has longer delivery times, it is the most preferred options for moving heavy, bulky, low-value goods over long lengths of haul. This preference is the result of being the lowest cost transportation alternative given rail transportation is more fuel-efficient and has larger freight capacity than trucks. Besides, railroads enjoy strong pricing power as highlighted by an increase in rates twice larger than the inflation over the period 2004/2019. This pricing power comes from the lack of transportation alternatives for many customers. A full comprehensive review of the industry is available here .

Our preference for Canadian railroads and CNR in particular

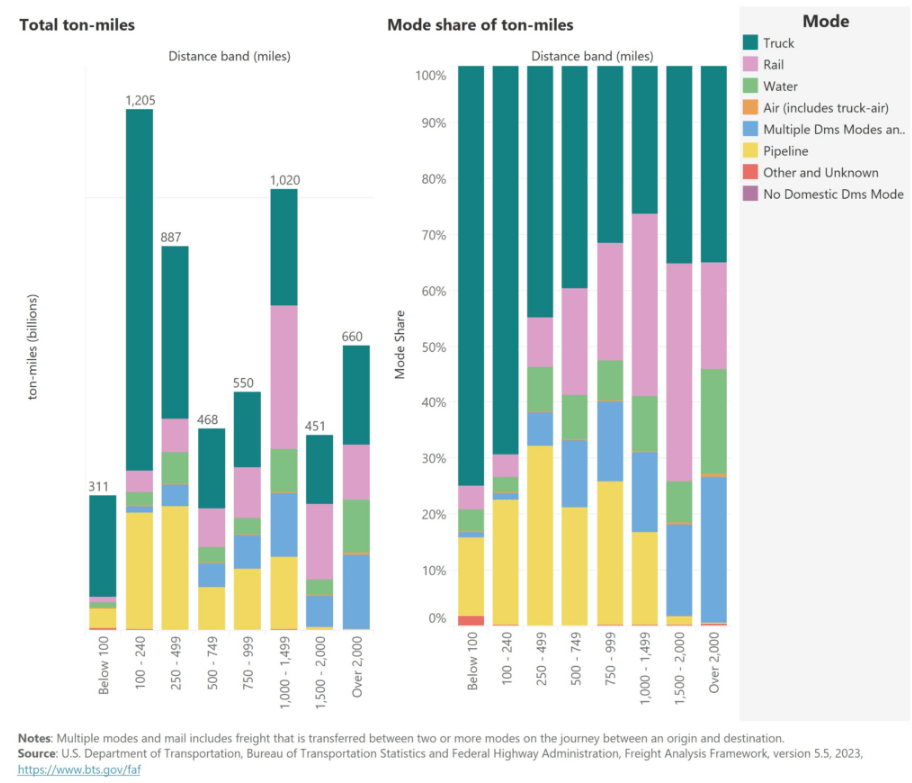

Unlike US railroads, both Canadian railroads posted positive volume growth and it should keep outgrowing US peers, in our view. Indeed, the Canadian government and the private sector did invest significantly in port infrastructure to increase capacity.

(Source: CNR presentation) (Source: CNR presentation)

{kind=link}

{kind=link}

In addition, CNR has the lowest exposure to the structurally challenged coal category, which face volume decline as it is replaced by cheap natural gas as a power generation fuel source.

(Source: Company annual reports and Author)

{kind=link}

Finally, Canadian railroads are most likely better positioned against regulatory risk. Their US operations are close to the Mississippi River, giving customers the option to ship by barge, thus reducing the level of customer captivity and eventual pricing abuses.

Canadian National Railway is the most competitively-advantaged railroads

CNR has most likely the most attractive rail network of the industry. Firstly, it has a three coast-access, connecting both coasts in Canada and the US Gulf Coast. Canada has a lot of natural resources such as grain, oil, potash (fertilizers), copper, lumber… that are suitable for rail transportation. In addition, the long lengths of haul, the harsh weather conditions, and the low-density areas spanning a large portion of Canada make rails the most appropriate transportation method.

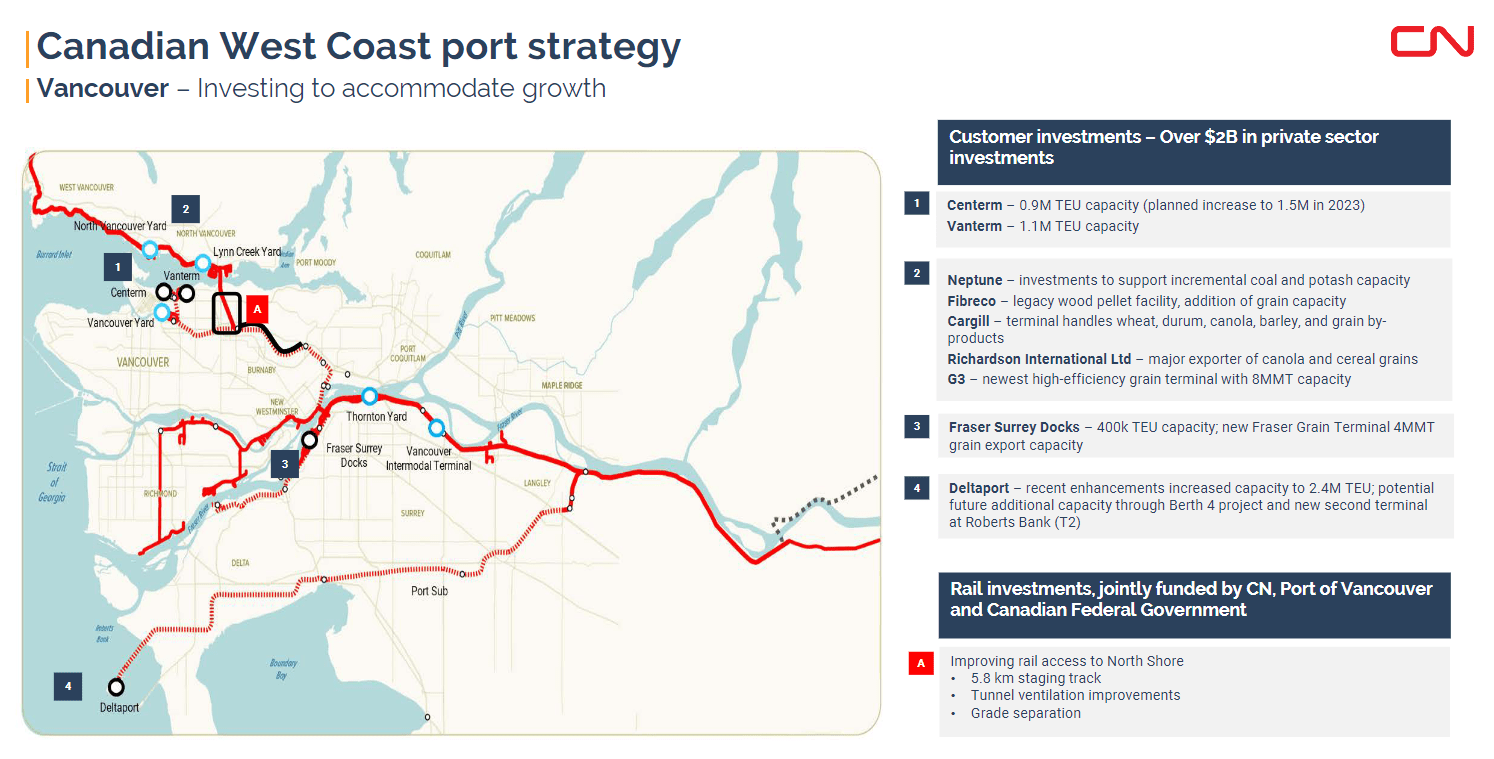

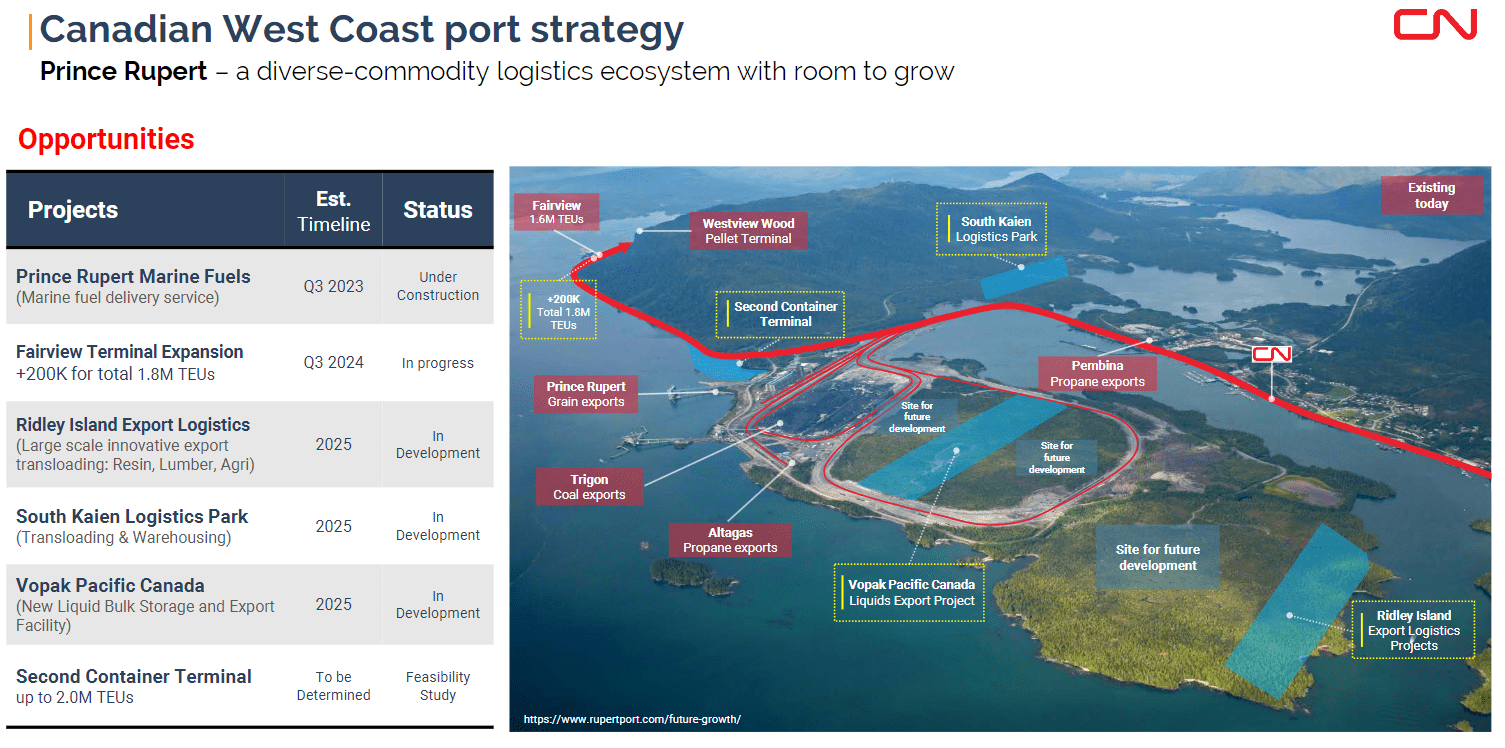

CNR has also a unique access to the Prince Rupert and Halifax ports, which is a key competitive edge versus its direct competitor, Canadian Pacific Kansas City. It is also an advantage versus US peers because western Canadian ports (Prince Rupert and Vancouver) have gained market share over US west coasts ports due to significant infrastructure investments, lower port fees and faster transit time to US Midwest destinations for cargoes coming from Asia (more direct route than US western ports).

Finally, CNR benefits from fluidity advantage around Chicago. Chicago connects the eastern, western, and Canadian railroads, making the city the most important freight hub in the US, with~ 25% of all freight trains and 50% of all intermodal trains in the U.S passing through the city. As a result, railroads must face the complicated and slow process to co-ordinate rail car movements and change crew and locomotives. CNR owns a railroad that skirts the city, giving the options to interchange with other railways at Chicago or to bypass the city and its congestion issues to keep going south.

{kind=link}

A strong operating performance

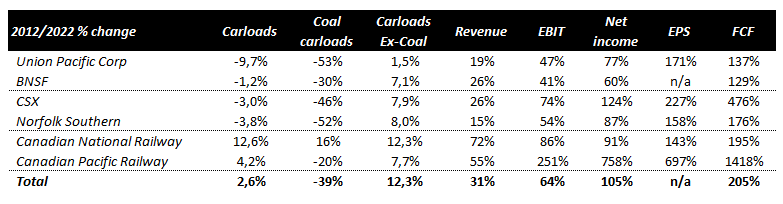

Over the last ten years, Canadian railroads stand out with positive volume grow (all US peers faced declining volume) and much stronger revenue growth than US peers. It is the result from a lower exposure to coal (a category in structural decline due to the transition from coal to natural gas-sourced electricity production) and market share gains from Canadian ports.

(Source: Company annual reports and Author)

{kind=link}

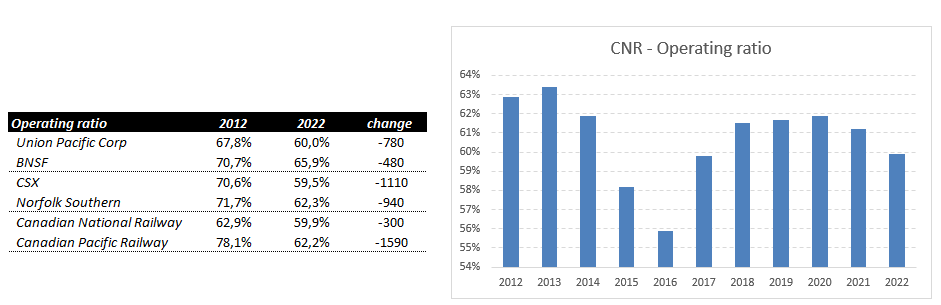

From 2003 to 2009, under the leadership of Hunter Harrison, CNR pioneered the implementation of PSR (precision scheduled railroading) and improved significantly its profitability as highlighted by the decline in the operating ratio from 76.8% in 2003 to 63.6% in 2010 (all other class 1 railroads were above 70% at that time). Peers started implementing PSR principles over the last ten years and have caught up with CNR's profitability, even though CNR has still one of the best operating ratios of the industry. As a result, efficiency gains were much lower than peers during the last ten years, translating into a much slower EPS growth versus other railroads (Revenue and EPS grew 4.6% and 7.7% CAGR between 2012 and 2022, respectively).

(Source: Company annual reports and Author)

{kind=link}

Valuation

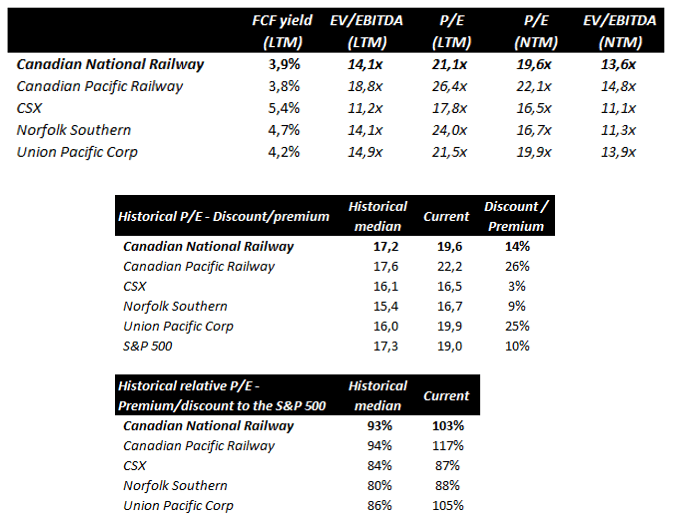

CNR is currently trading at a FCF yield of 3.9%, a P/E of 19.6x and EV/EBITDA of 13.6x. From a relative perspective, CNR does not seem undervalued. It trades at a premium to eastern railroads, which have a more complex network and shorter lengths of haul, and in-line with Union Pacific. Canadian Pacific is trading on higher valuation multiples because of its recent acquisition of Kansas City Southern.

(Source: Bloomberg and Author)

{kind=link}

From an historical perspective, it trades to a 14% premium to its median P/E of the last 10 years, which is lowest than Canadian Pacific and Union Pacific and higher than Norfolk Southern and CSX. CNR is also trading roughly in-line with the S&P 500 (a 3% premium) while it used to trade at a 7% discount over the last 10 years.

Conclusion

Canadian National Railway has a wide moat with one of the longest durability profiles. Its rail network is one the most attractive as it benefits from an attractive footprint, unique access to some ports and fluidity advantage around the most important US hub. Therefore, we consider CNR has the highest-quality railway. Nevertheless, like all class I operators, it faces limited reinvestment growth opportunities (cannot build new tracks) and the existing business will not soar either, which limits the growth in company's intrinsic value. As a result, we prefer to wait for a better entry point, when valuations will be much more favourable (a P/E closer to17x seem more appropriate).

Risks

An economic slowdown can have an impact on the quantity of goods and commodities that railroads transport.

Adverse winter conditions can materially hamper efficiency by blocking tracks, necessitating shorter trains throughout certain times of the year and increase delivery times.

CNR carries chemicals and oil, which may lead to significant liabilities in case of hazardous material spills.

Negative regulation change could impact railroads. Pricing cap and/or forced switching (reciprocal switching) could be implemented by the regulators. In addition, more stringent regulation could also pressure railroads' profitability. For instance, in 2008, a new regulation forced railroads to purchase and install positive train control systems.

For further details see:

Canadian National Railway: Better To Wait For The Next Train