CA - Canadian Natural Resources: The 3-Way Booty Split

Summary

- Canadian Natural Resources has been one of the best dividend growth stories in Canada.

- The company had committed to a 100% free cash flow return policy when net debt reached $8.0 billion.

- We look at Q4-2022 results and the decision to ramp to start the 100% return policy right away.

Note: All amounts discussed are in Canadian Dollars.

When we last covered Canadian Natural Resources Limited ( CNQ ), we highlighted its stellar record for dividend growth, but suggested there were better plays out there for your money.

CNQ is the king if you think that the commodity bull market is just getting started. It also remains one of the few companies that can prove bullish price prognostications wrong by continuing to deliver big production increases. At present, we do not own the stock, as we think there are better relative values there. But this high-class performance is finally getting recognition, and we are now just three years away from the official dividend aristocracy.

Source: 22 Years Of Dividend Growth At 22% A Year

The stock has gone a tad lower and the lower commodity prices since that article have certainly contributed to its underperformance vs the S&P 500 ( SPY ).

Seeking Alpha

CNQ has been in the middle of the pack as far as the oils sands group is concerned. It has kept pace with Suncor Energy Inc. ( SU ), while lagging Meg Energy Corp ( MEG:CA ) and outperforming both Cenovus Energy Inc. ( CVE ) and Imperial Oil Ltd. ( IMO ).

The company released its Q4-2022 results today and had a notable surprise for shareholders.

Q4-2022

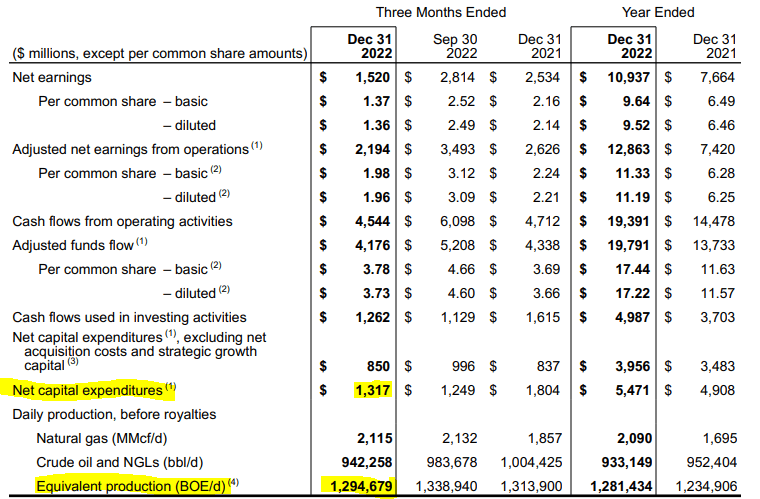

CNQ finished off 2022 with a solid quarter. Combined production of oil and natural gas came in slightly below most estimates which were near 1.3 billion barrels of oil equivalent per day and net capital expenditures were a bit above the expected $1.2 billion mark.

{kind=link}

These weaknesses were more than offset by pricing of natural gas which handily came to the rescue and operating cash flow was an extremely healthy $4.54 billion. The biggest metric, i.e. free cash flow, was at $2.5 billion in the fourth quarter. CNQ calculates this after both the dividend and the baseline capex. The company allocated about $750 million of this $2.5 billion to share buybacks and the rest to debt reduction. Net debt was reduced is the fourth quarter by $1.9 billion and during the entire year it was decreased by $3.4 billion.

2023 & Change In Policy

Despite a relatively heavy shareholder return policy, the company had previously committed to do even more in the years ahead. The next target was originally set at a net debt of $8.0 billion, after which, all free cash flow after base dividends and capex would be returned to shareholders. This would be either in the form of special dividends, share buybacks, or a combination of the two. Depending on your optimism or pessimism for commodity prices this target was slated to occur between very early Q1-2024 or very late Q2-2024. In fact part of the relative delay here had been due to CNQ raising its base dividend and the collapse in natural gas prices. Nonetheless, investors could get all the free cash flow allocated back to them relatively soon. With the Q4-2022 press release, CNQ raised the ante.

After reviewing our strong financial position and sustainable cash flow profile, particularly when you compare our debt levels to the size, diversity, and long life low decline nature of our high value reserves, the Board of Directors has enhanced our free cash flow allocation policy to accelerate incremental shareholder returns to 100% of free cash flow when the Company's net debt reaches $10 billion, changed from the previous $8 billion net debt level. These changes reflect the substantial debt reduction over the last two years of approximately $10.7 billion, the increase in our production and reserve base and that our fixed outstanding bonds of approximately $11.4 billion are similar to the $10 billion net debt level in the free cash flow allocation policy. Additionally, with fully committed undrawn bank credit facilities of approximately $5.5 billion, we ensure strong liquidity. Once the Company's net debt reaches $10 billion, the enhanced free cash allocation policy will be adjusted to define free cash flow as adjusted funds flow less dividends, less total capital expenditures in the year

Source: CNQ Q4-2022 Press Release

The company's same press release said that net debt was at $10.5 billion at the end of Q4-2022. Adjusting for the base dividends ( which was raised by 6% ), capex and the share buybacks conducted in Q1-2023, the company should be at or below those levels already.

That leads us to the question as to what we can actually expect from the company in 2023. CNQ will be investing for some growth in 2023. This is based on their 2023 budgetary guidance.

Our 2023 budget is disciplined, targeted at approximately $5.2 billion, consisting of approximately $4.2 billion in base capital and approximately $1.0 billion in strategic growth capital. In 2023, we target to deliver strong year over year production growth of approximately 56,000 BOE/d, or 4%, over 2022 targeted levels, based on the midpoint of our 2023 production guidance range of approximately 1,330,000 BOE/d to 1,374,000 BOE/d. Our strategic growth capital targets to deliver additional production and capacity growth in years after 2023.

Source: CNQ Budget Press Release

We think capex numbers will likely come in a bit higher than this and production a bit lower. This comes from our bias toward stronger pricing power for oil services company and a weak natural gas outlook getting the company to lower production in that area. Our forecast further calls for about $14.0 billion in cash flow in 2023. Subtracting out the capex and the base dividend, we get to about $4.5-5.0 billion left. With 1.1 billion shares outstanding, you could see special dividends of an additional $4.0 per share in 2023.

The company also could choose to buy back shares instead and repurchase about 6% of its float during 2023. Realistically, we think it will split the booty three ways. Expect the base dividend to keep being bumped up and reaching at least $1.00 per quarter in 2023. Expect at least $2.0 billion more of buybacks, over and above what has been disclosed as being conducted year to date. Expect at least $1.50 of special dividends.

Verdict

CNQ took a strong commitment of shareholder returns and pushed it up further. Most other Canadian oil and gas plays are doing something similar although the timelines and percentages are a bit different. Here's SU talking about 75% of free cash flow:

Our quarterly dividend is now the highest in the coming history after the most recent increase of 11% to $0.52 per share. And as Kris said, we continue to strengthen the balance sheet and reduced net debt during the year by $3.2 billion, excluding FX impacts on US dollar culminated debt.

As previously noted, we intend to increase excess funds to buybacks to 75% by the end of Q1. And subsequent to the fourth quarter, the Board approved a renewal of the company's share repurchase program for up to 10% of Suncor's issued and outstanding common shares as of February 3, 2022. And this program is planned to begin on February 17, 2023.

Source: Suncor Q4-2022 Conference Call Transcript

Cenovus Energy Inc. ( CVE ) is working toward a similar goal and Meg Energy has an almost identical path toward rewarding shareholders. Which of these should you own? We think the decision comes down to two factors. The first being valuation and there CNQ continues to trade at big premium to the three. Whether you see free cash flow yield or EV to EBITDA, you're paying for the premium company. Nothing wrong with that, but you should be aware of the cost. The second part is your outlook on natural gas. The other oilsands plays are all oil or almost all oil. CNQ has a pretty substantial chunk coming from natural gas. If you're bullish on natural gas and its future, then CNQ can still outperform, despite the current higher multiple. At current strip that 25%-30% of production is making nothing or virtually nothing on a full cycle basis. So there's upside and you can come out ahead. For our money, we major positions in MEG and SU and minor positions in CVE and IMO. We don't own any CNQ and rate it as neutral/hold.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Canadian Natural Resources: The 3-Way Booty Split