CA - Canadian Utilities: Time To Go To 'Buy' (Rating Upgrade)

2023-12-04 16:04:47 ET

Summary

- Canadian Utilities offers an attractive yield of nearly 6% and is trading below its typical multiple after a double-digit drop in share price.

- The company's focus on expansion in LATAM, NA, and Australia is expected to drive overall growth.

- CU's clean fuels strategy, including the ATCO Heartland Hydrogen Hub project, aligns with government priorities and enhances its position in clean energy.

Dear readers/followers,

It's been about 9 months since I offered my initial opinion on Canadian Utilities ( CU:CA ) ( CDUAF ). I went "HOLD" given that I saw the company as not "attractive enough" for what it offered in the context of the current market environment. I believe it's now time to change this rating, but barely. The last few months have clearly impacted how much we should be paying for attractive yield, even the near-6% yield this Canadian multi-utility offers.

However, after a double-digit drop in share price, and following the company now trading below its typical multiple, I don't believe you'd be wrong in considering this company somewhat differently.

You can view if you're interested, my previous thesis on this company in this article.

Now we'll see exactly what sort of upside we can consider to be likely for the company going into 2024, and if it's enough to interest you in a world where 7-8% yielding preferred stocks are the rule rather than the exception.

All amounts in this article are in Canadian dollars unless otherwise noted.

Updating on Canadian Utilities - an ATCO business

As with my last piece, I don't focus on ATCO, I focus on CU, even if CU is a part of ATCO. 5,000 employees manage $22B in worldwide production, distribution, and infrastructure assets, including a very appealing mix of natgas, hydro, power, infrastructure gas lines, power lines, and "clean energy".

The company's strategy mimics the strategy of almost any utility you can think of: Leverage its expertise in its operational areas, invest in the infrastructure and assets, optimize and harden, where necessary, its portfolio, and in turn drive cash flows and earnings.

CU has a certain focus on expansion and this focus is on LATAM, NA, and interestingly enough, Australia, in order to drive the company's overall growth. The latest set of results we have at this time is the 3Q. Thankfully enough, like most utilities I cover, they are very boring, meaning results don't really fluctuate that much, and operations are relatively practicable.

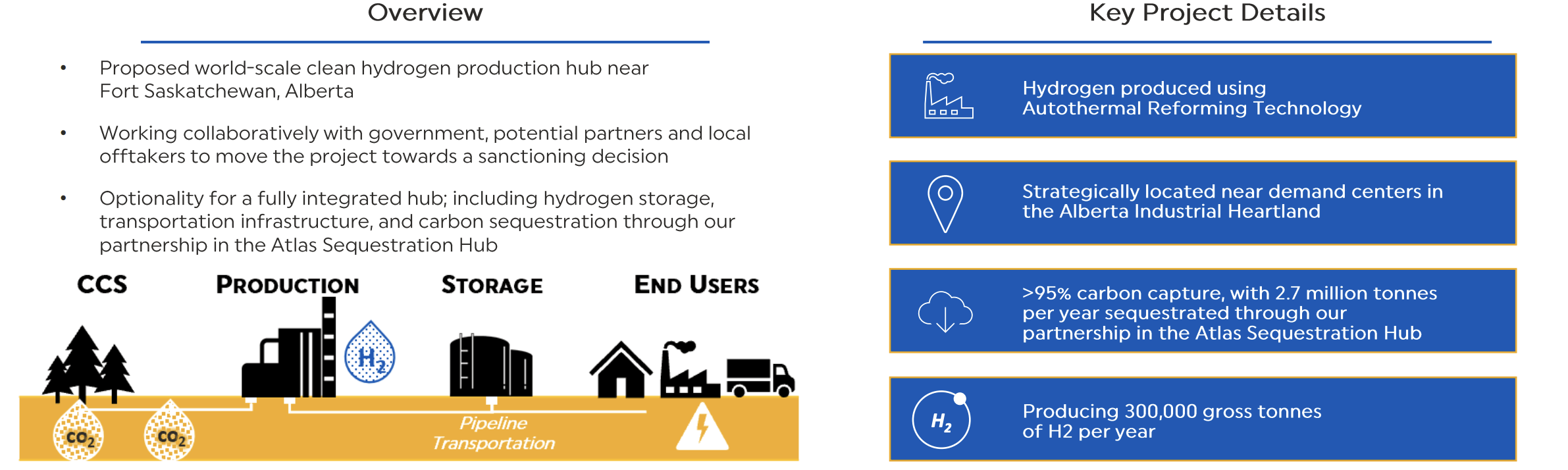

It's worth taking a second following 3Q to focus on the company's clean fuels strategy - because the company's ATCO Heartland Hydrogen Hub project is moving forward.

{kind=link}

This project is entirely in line with government priorities in Canada, offering avenues to long-term competitiveness and enhancing the company's position in clean energy.

Also, as I mentioned, the company has a wide array of solar projects, one of which achieved full commercial operation in 3Q, adding 27 Gross MW to the company at 49% ownership - and 2 more with 49% and 100% ownership respectively coming online in 4Q23. After that, it's more solar and wind projects, with others both solar and wind being in the mid-stage, and 4 more solar opportunities in early-stage development. As a result of the difficulties in returns for many wind power projects which have become apparent in 2Q and 3Q (just look at the reports Orsted is giving), solar seems a safer bet here given what I view to be far more simple operational specifics for the technology.

There are some regulatory highlights worth mentioning for the company as of 3Q. First off, a decision was made regarding Alberta Electric and Gas distribution, specifying the introduction of an X factor premium, capital provisions, Earnings share mechanisms, and an efficiency carry-over mechanism. Secondly, and more importantly, the generic cost of capital decision for 2024, which saw the relevant regulator/the commission introduce a 9% base approval as the starting point for ROE determination, adjusted for utility spread and bond yields with a continued 37% equity thickness.

The results for the company meanwhile, were so-so. The rebasing of Alberta distribution utilities saw lower earnings - but this was neither an unexpected trend nor an unexpected set of news, and also compared to a very strong YoY performance, which is at least part of the reason why this seems "negative".

I expect the new earnings sharing mechanism to deliver opportunities for outperformance from this company, and while the full 2024E RoE is not known yet, the company describes a likely RoE range of 9-9.2%, and this is up from the current 8.5%, meaning an improvement.

The company is meanwhile seeing strong growth in gas distribution in Australia. This is due to new connections, volume, new tariff rates and pure system volumes. However, inflation is still strong in Australia, which hampers the addition this can give to the company's earnings.

Expect some renewable lag from this and from other companies in the same sector due to the recent decision to pause approvals for new renewable projects until February of next year - while it doesn't impact projects under construction, it does impact the company's pipeline.

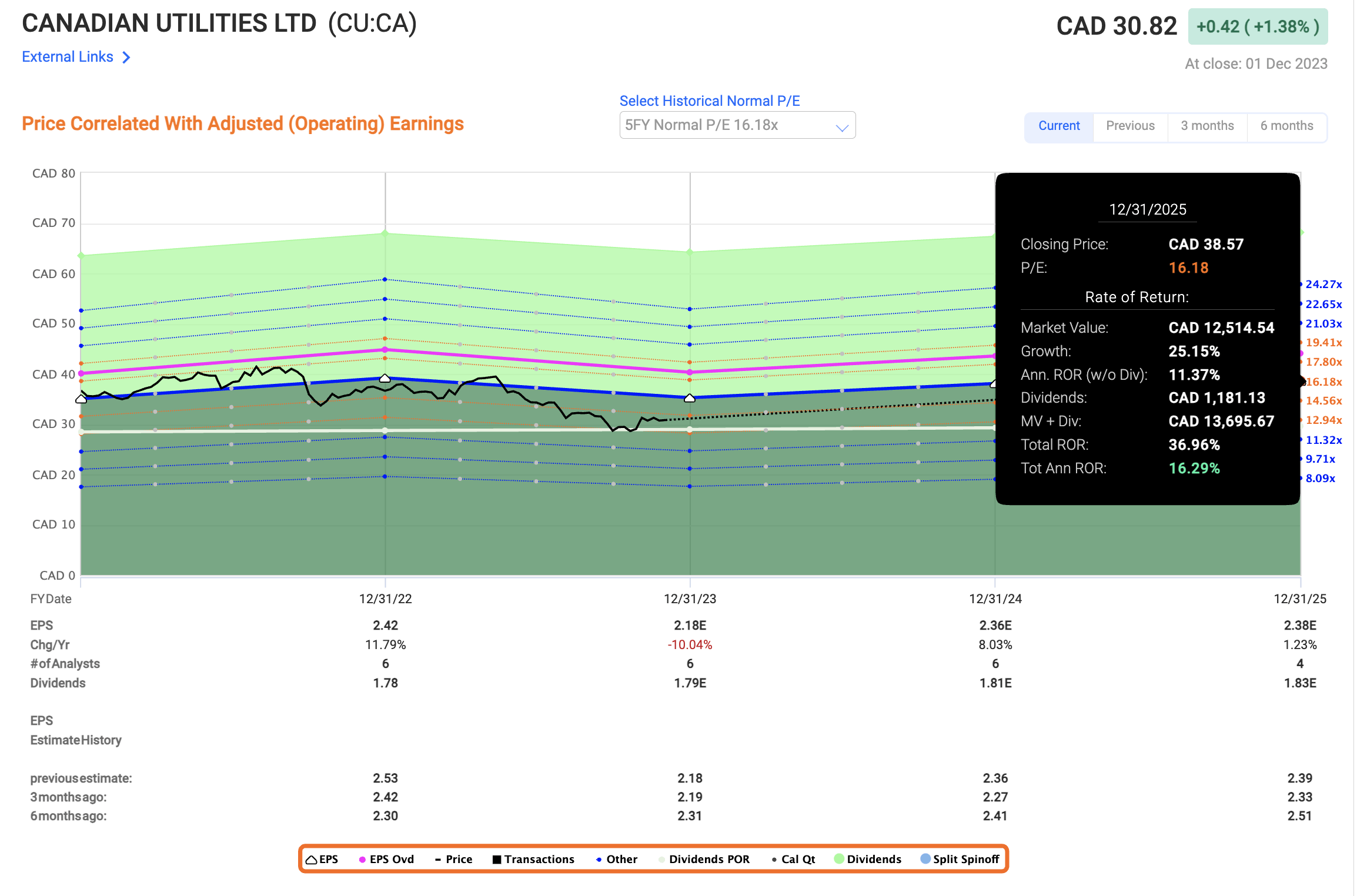

Overall, earnings for CU are expected to decline about double digits, 10% this year on an adjusted operating earnings basis, but this is, to remind you again, to very good YoY results. Also, 2024 is set to more or less normalize this and see the company's earning back to above $2.35/share here.

The company offers a relatively good visibility as you'd expect from a utility, but it's LATAM/AUS profile does mean somewhat more volatility, translating to a not-100% margin-of-error adjusted accuracy, but 83% with a 17% miss rate (Source: FactSet). Not perfect, but good enough for what is offered.

Over time and historically, CU has been a good investment. If you invested back in 2003 and held on, you could have made over 350% RoR, around 8% annually. If you applied certain valuation rules and sold when the company reached insane levels, which it has, you could have made 14% per year - 20% if you bought at extreme undervaluation after the GFC. The company has both the operational stability and the history to make it what I believe to be a solid utility investment.

I did not "time" this article properly to its trough - but that's okay because in the longer term, the company is still at a point, where at any time in the last 15 years, you'd have made a profit by investing.

That's a very good valuation starting point and a good time to change my rating for CU.

Risk & Upside

The risks to CU are not operational, as I view them, but value-related. In order for this to be an attractive investment, you need to accept that you're paying a 14x P/E for a business that's generating a 5.82% yield with an upside to a normalized P/E at around 16%. This is not a bad return in the least. But the thing is, there are utilities available that still, despite this attractiveness, offer comparable or even better upsides to you. The company may underperform in the next few quarters, improving its upside here, but I still have difficulties seeing that it offers a better upside than my current largest utility investment Enel (ENLAY), which I view as an investment with upside potential of almost 30% per year.

That's the main risk I see here.

The upside meanwhile, to this company, is obviously good returns from a safe set of operations backed by ATCO. That 16% annual rate of return? I think that one's pretty "safe" as far as such returns go. Anything can happen, but unlike when the company was 15% more expensive than now, this is a good upside.

Valuation

As mentioned above, valuation is the linchpin here. The company currently trades at a not-uninteresting level from a historical perspective. Why? Because typically, this company warrants 16x P/E - even 16.1x on a 20-year basis. So this slight premium is what I would view as "well-established".

Because the company trades at 14x P/E, and because a 4-5% forecasted upside on average is pretty good, there is a case to be made for the following conservative upside here, resulting in that aforementioned 16% annualized RoR.

{kind=link}

Typically, with this being a Canadian stock, you also have fewer risks in terms of withholding taxes, FX, and other issues compared to my Italian investment in Enel, depending on your specific investment locale, of course.

But I still want to make it very clear, that while I am bumping my target to the company here to a "BUY", and I'm sticking to my overall price target of $33 CAD, I'm also saying that Enel is a vastly more profitable investment, at least from where I stand.

To compare, the company trades at 10x P/E with an upside to a P/E 14x with an estimated growth rate at similar levels of 5%, but with a yield of over 6% (that's set to increase based on the rent company 3Q23), and an upside to the 2025E 14.5x P/E level of 29.1% annually.

However, for some of you wanting diversification into Canadian investments and into the TSX market, CU is a fair choice at this level - and that is why I am bumping my stance to "BUY" here.

CU is followed by 7 analysts - and it appears to me that these analysts are not convinced by the company's price, despite their targets. None of these analysts have the company worth less than $33/share, with targets ranging from $33 to $38.5, and an average of $35.3 Despite these targets which should imply a 15% upside, only 2 out of 7 are at "BUY" or equivalent here, with most holding the company at a "HOLD" stance at this time. I've covered the lack of conviction to many analysts before - so I'll just say that my targets are usually very indicative of whether I consider the company buyable or not.

In this case, I do consider the company to be a clear "BUY" - but I also would say that there are companies in the same sector, if you look globally, that offer similar or better upsides.

Here is my updated thesis for CU.

Thesis

- Canadian Utilities is a foundationally solid business, but one that has been encountering growth and margin issues for the past few years. Its high yield and established rate base make it safe, but I don't see much growth potential in the business. Due to a relatively non-discounted valuation, I cap the realistic upside at 8-10% per year.

- This is now enough of an appeal for me. Even if I consider there being more attractive potentials than this specific company, I would call this a "BUY" here and go positive on the business for the first time.

- My PT for CU is a conservative $33/share.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I now go to a "BUY" due to the company being attractive enough to "BUY" here.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Canadian Utilities: Time To Go To 'Buy' (Rating Upgrade)