CA - Canadian Western Bank: A Deep Discount Play That Pays A Safe 5.2% Dividend

2023-07-09 11:11:14 ET

Summary

- Canadian Western Bank is a riskier investment than its larger peers due to its smaller size and regional focus, leading to a larger discount and lower price-to-earnings multiple.

- CWB's loan portfolio is primarily diversified across British Columbia, Alberta, and Ontario, with a significant portion in Alberta, making it vulnerable to fluctuations in natural resources prices.

- Despite the risks, CWB stock trades at a deeper discount than larger banks and offers a safe dividend yield of 5.2%, potentially making it a strategic medium- to long-term value trade.

Canadian Western Bank (CBWBF) (CWB:CA) receives less recognition than the Big Six Canadian Banks, including National Bank of Canada (NTIOF) (NA:CA) that I just covered here . Additionally, CWB is smaller and categorized as a regional bank. It is obviously a riskier investment than the bigger players and therefore trades at a larger discount and lower price-to-earnings (P/E) multiple.

How Canadian Western Bank is Riskier Than Its Bigger Peers

Greater Volatility Might Lead to Greater Reward

The graphs below compare the price action and total returns of Canadian Western Bank stock and BMO Equal Weight Banks Index ETF (ZEB:CA), which has a roughly equal weighting of the Big Six Canadian Bank stocks. As illustrated, CWB was a poor buy-and-hold investment.

That said, zooming in, the one-year charts below indicate that it has greater volatility and therefore could potentially work as a strategic trade for higher returns potential. After all, one textbook definition of risk is volatility, and greater risk could potentially lead to greater rewards. However, investors need to be careful and strategic about their entry and exit points.

(The company reports in Canadian dollars, so the figures in this article are in C$ unless otherwise noted.)

Riskier Loan Portfolio

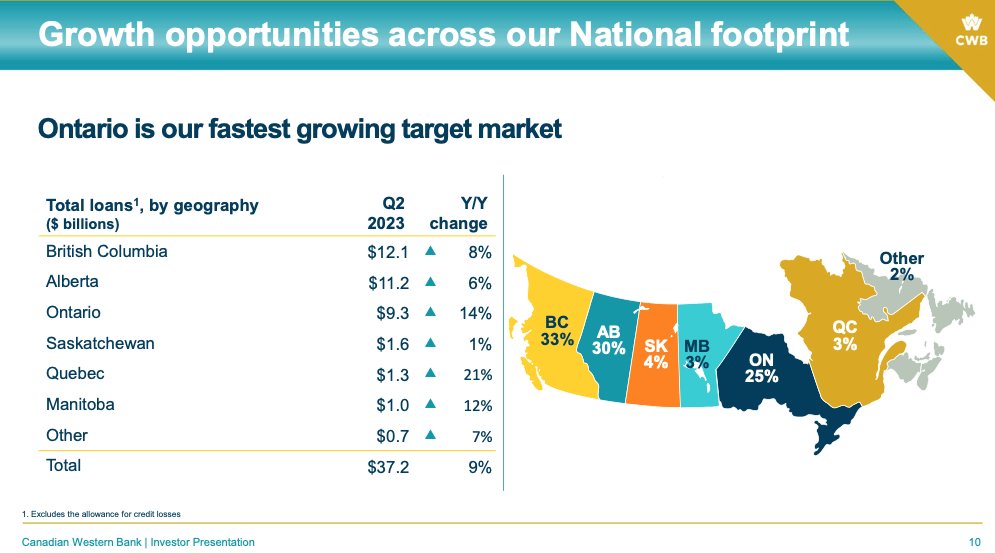

The Canadian bank's loan portfolio are primarily diversified across British Columbia, Alberta, and Ontario, which together make up approximately 88% of its loan portfolio.

Although in Q2 FY2023, the bank highlighted the solid growth it has been experiencing in Ontario, investors should be cognizant that it has a good portion (30%) of its loans in Alberta, whose economy can go through boom or bust depending on highly cyclical natural resources prices like oil and natural gas prices.

CWB Q2 FY2023 Investor Presentation

{kind=link}

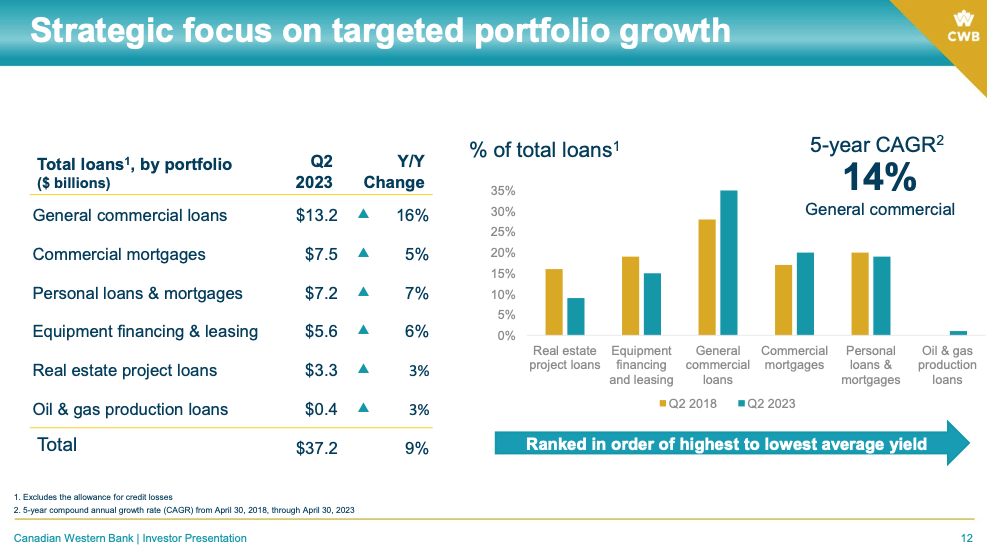

Moreover, although the bank has little exposure to oil & gas production loans (~1% of the loans portfolio), which may be viewed as a riskier type of loan, the bank also has about 56% of its loans portfolio in general commercial loans (~35% of the loans portfolio) and commercial mortgages (20%), which are also generally riskier than personal loans.

CWB Q2 FY2023 Investor Presentation

{kind=link}

We believe this kind of loans portfolio mix creates a more volatile stock and plays a factor in the bank stock trading at a lower valuation to its bigger peers.

Valuation

The bank's near- to medium-term earnings could be stalled to a growth rate of about 2% due to a potential recession and higher provisions for credit losses. In this BNN Bloomberg article last month, it noted economists expecting a recession in Canada in 2023 or 2024.

{kind=link}

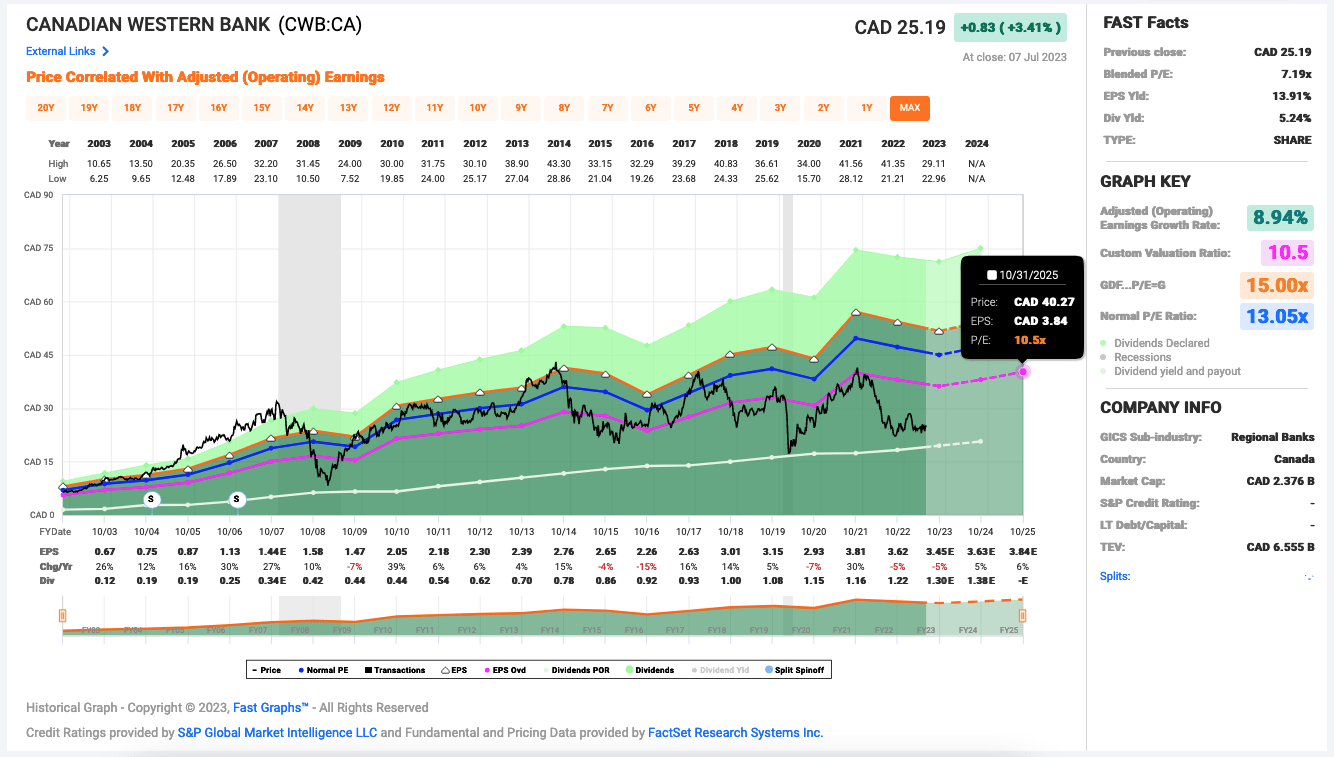

The bank stock's price-to-earnings chart shown above suggests a near-term target of about $30.82 based on EPS decline of about 5% in fiscal 2023 and 5% growth in fiscal 2024 and a conservative target P/E ratio of 8.5. This suggests the stock trades at a discount of about 8% at $25.19 at writing. The medium-term target would be $40 for a target P/E of 10.5.

{kind=link}

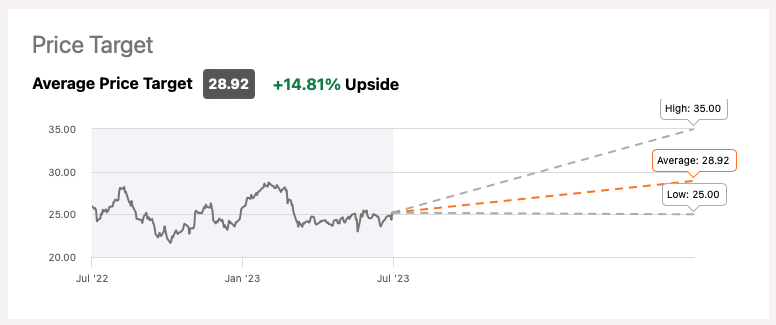

Wall St. analysts are more conservative, believing the stock is slightly discounted by close to 13% from the average price target of $28.92 per share, which also suggests a near-term upside potential of almost 15%.

CWB also trades at a discount of almost 28% from its recent book value of $34.90. Based on its historical price-to-book valuation displayed in the graph above, we believe investors should have a chance to take profit at a minimum the book value, which suggests upside potential of almost 39%.

{kind=link}

Recent Results and 2023 Outlook

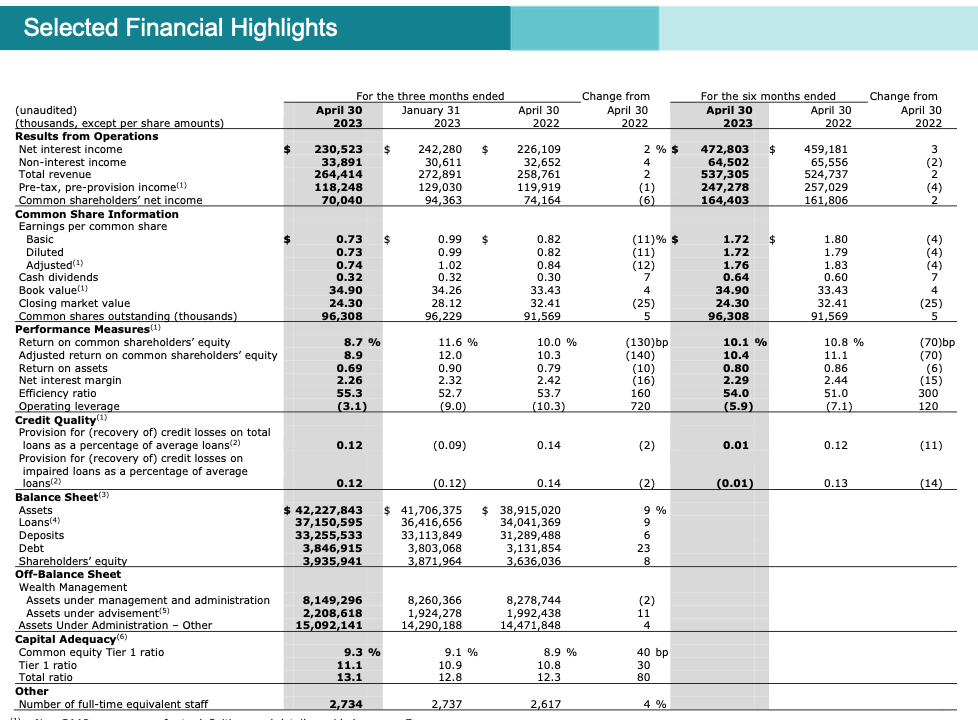

Canadian Western Bank reported its fiscal Q2 2023 results on May 26. In the first half of the fiscal year, revenue climbed 2% to $537.3 million -- net interest income climbed 3% to $472.8 million but non-interest income fell 2% to $64.5 million. Non-interest expense rose 8% to $295.6 million. Diluted and adjusted EPS both fell 4% year over year to $1.72 and $1.76, respectively.

Management provided fiscal 2023 outlook as follows: adjusted EPS of about $3.50-3.60 and adjusted return on equity ("ROE") of 10-11%.

Dividend

Based on the midpoint adjusted EPS estimate of $3.55, its payout ratio is estimated to be about 37% this year. CWB stock offers a safe dividend yield of 5.2%.

Again, because it's a riskier stock, we believe it's natural that CWB currently has a lower payout ratio than the Big Six Canadian banks, whose payout ratios typically range 40%-50%.

CWB has a solid dividend growth track record. According to the Canadian Dividend All-Star List maintained by Dividend Growth Investing & Retirement, the bank has paid an increasing dividend every year since 1992. Specifically, its 3-, 5-, 10-, and 15-year dividend growth rates are 4.1%, 5.7%, 6.8%, and 8.6%, respectively.

The bank maintains profitability and is able to increase its earnings over time through economic cycles. It last reported retained earnings of $2,419 million, which could act as a strong buffer for its dividend.

Investor Takeaway

Canadian Western Bank trades at a deeper discount than its larger peers at about 7.2 times adjusted earnings. Additionally, it offers a dividend yield of 5.2%, which is safe dividend income. With the looming clouds of a recession, its growth will be dampened, and the stock will remain depressed.

A reversion to a target P/E of 10.5 by the end of fiscal 2025 could drive outsized total returns of about 24.6% per year. Even if it took five years to get there, the stock will still return 15% per year, which would be pretty good since a good portion of the returns come quarterly in the form of dividends.

We think CWB could work as a strategic medium- to long-term value trade. Therefore, we rate it as a "Buy" for riskier accounts. If you're looking for quality bank stocks with higher certainty, you should look elsewhere.

For further details see:

Canadian Western Bank: A Deep Discount Play That Pays A Safe 5.2% Dividend