CA - Capital Power: 6.2% Yielder Reaches Attractive Entry Point

2023-12-10 18:00:00 ET

Summary

- Capital Power Corporation is a Canadian independent power producer with interests in renewable and traditional power assets.

- The company's high cash flow yields and strong hedges make it a good investment opportunity, despite not receiving premium valuations.

- The stock is trading at a low multiple of AFFO and has a very probability for 10% annual returns, with the possibility of compounding returns reaching 20% if valuation expands.

Note: All amounts discussed are in Canadian Dollars

There are some companies that will never ever get a premium valuation. That tends to frustrate the value investors as making money seems hard. But even in this space, the ones that can use their own high cash flow yields to grow their revenues, can make successful investments. You just need to realize that premium valuation is not coming your way and hence your entries have to be extremely well timed. You have to adjust your multiples based on the company's history rather than benchmarking against the wrong comparatives. We show you one example today.

The Company

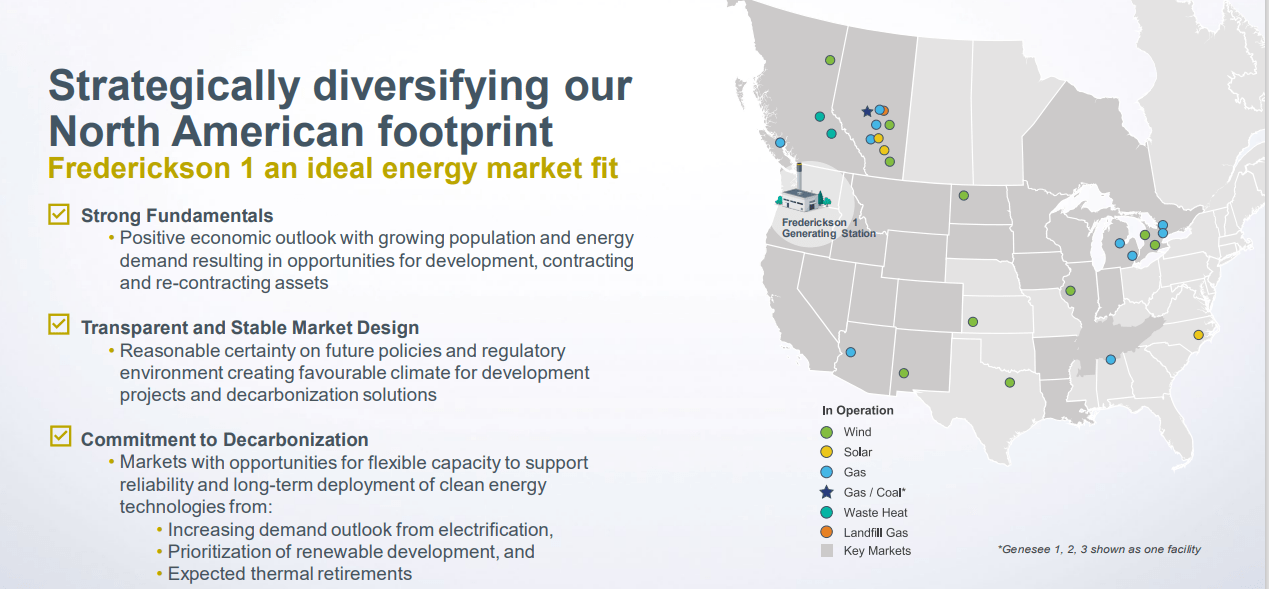

Capital Power Corporation ( CPX:CA ) ( CPX.R:CA ) is one of Canada's largest independent power producers. It has interests in approximately 7,500 MW of generation capacity in Canada and the U.S. It has kept expanding and diversifying over the years and the latest set of assets is shown below.

{kind=link}

You can note above that the company has assets in renewables as well the traditional gas and gasp, coal, powered assets. If you need to know at this point, yes, there is a "net zero 2050" strategy in place but it is a slow inch towards that and some years can take a step back.

{kind=link}

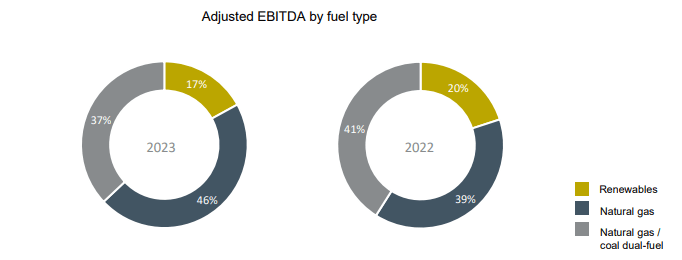

The most recent results shown below attest to the high margins being generated off this power assets.

{kind=link}

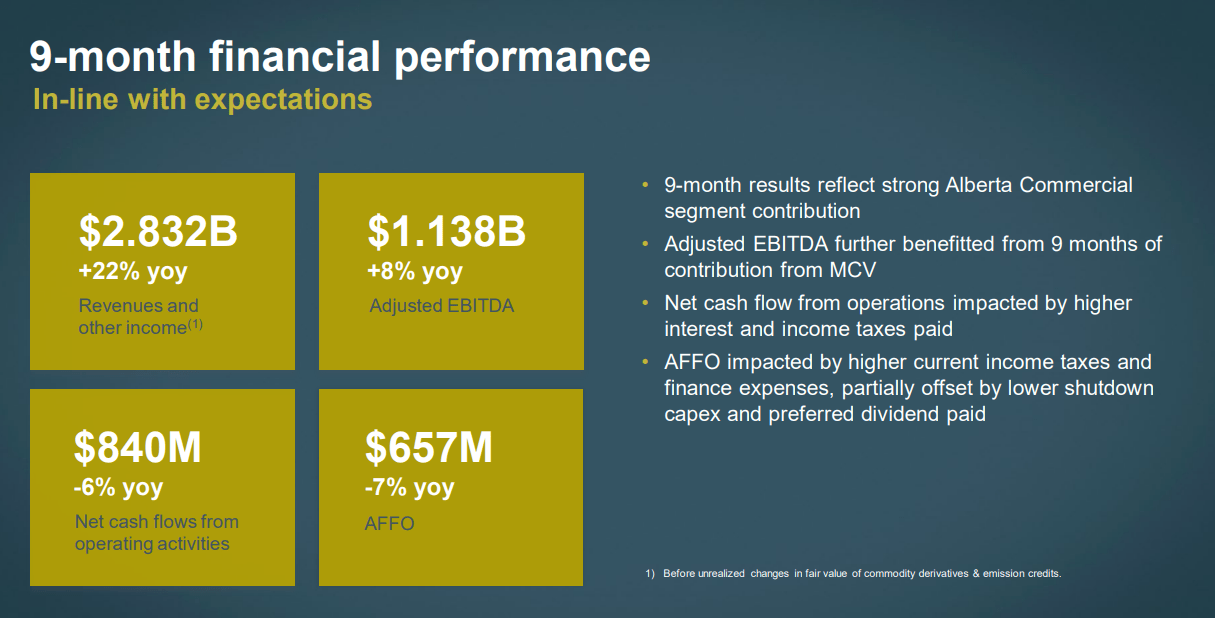

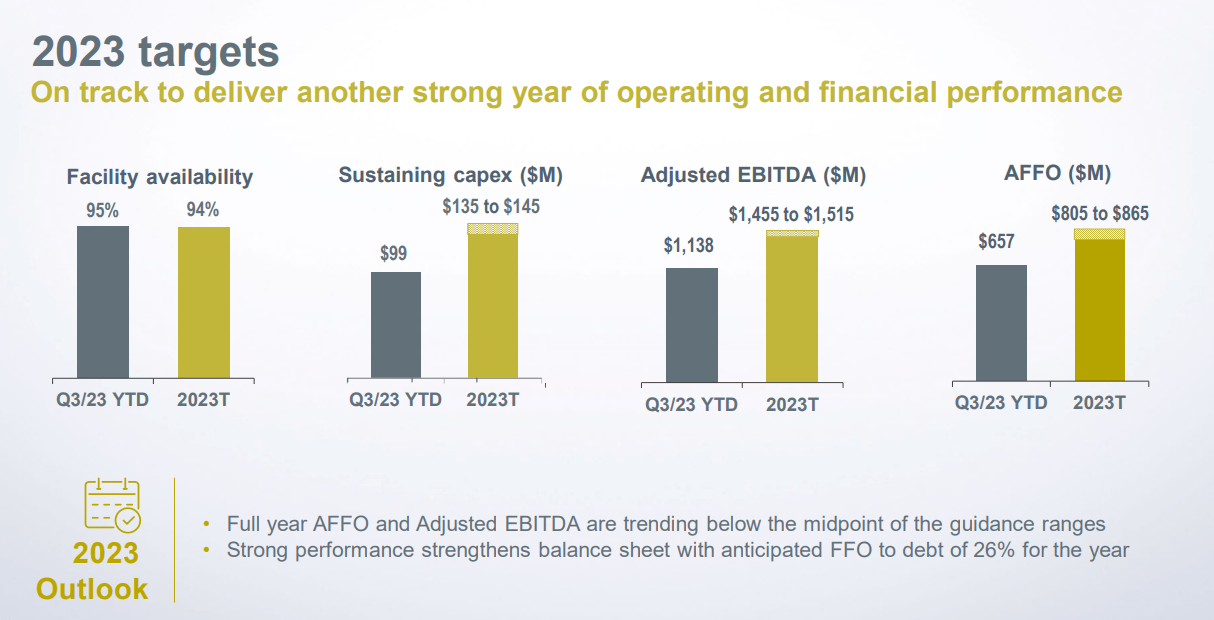

The company's guidance was slightly softer than expected but the overall numbers will still make 2023 the best year by far.

{kind=link}

For 2023, the adjusted funds from operations (FFO minus sustaining capex) will come in near $830 million or close to $7.00 per share. This puts it at close to 5X AFFO.

Some investors mistakenly include these companies alongside utilities and that is just plain wrong. These companies like TransAlta Corporation ( TAC ) and Vistra Corp ( VST ) are never ever going to get the multiples of regulated utilities, not even close. Power generation unfortunately is not a sexy industry and while one might think that these assets should always be in demand, the market tends to value these at ridiculous low numbers.

For comparison here are NextEra Energy Inc. ( NEE ), Duke Energy Corp ( DUK ) and Fortis Inc. ( FTS ). They average more than double the EV to EBITDA multiple and generally more than triple the equivalent P/E ratios.

Why We Still Think This Is A Point To Buy

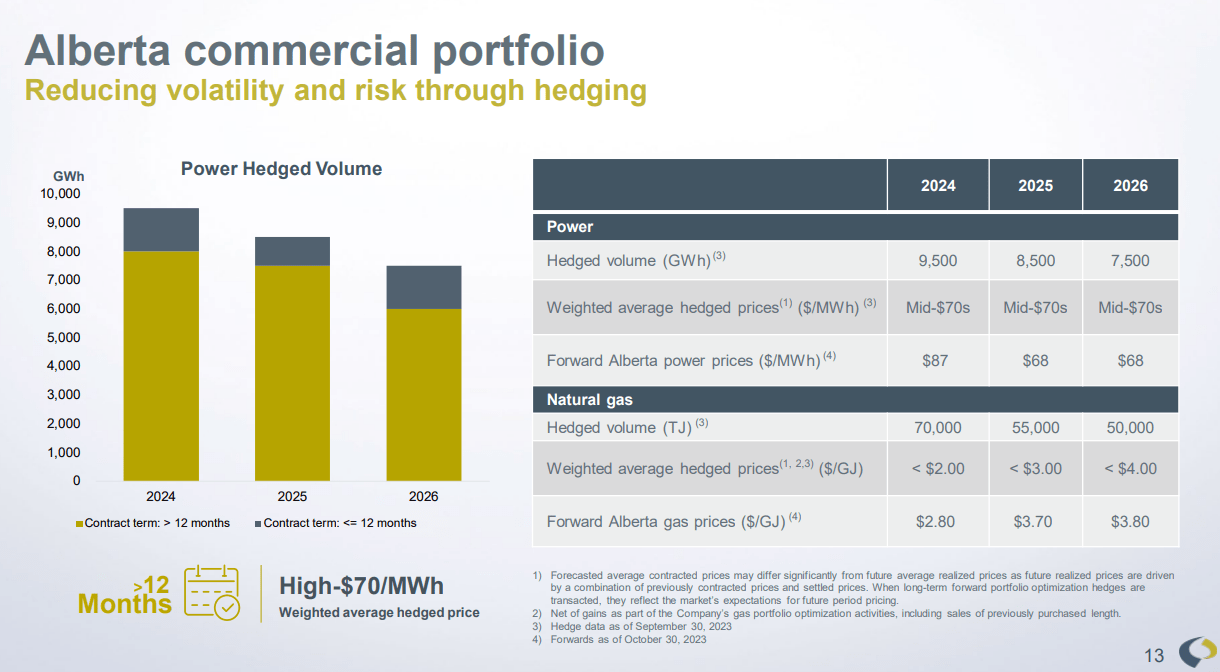

The immediate softer outlook aside, the company is still poised for solid performance. Capital Power has big hedges in place, locking in power prices for a majority of its generation in Alberta.

{kind=link}

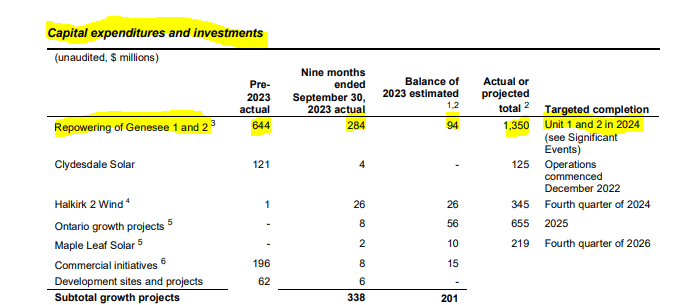

The cool part here is that forward prices are sill very strong with $87 expected for 2024 (the company has locked in mid-$70s). The company has locked in great spreads by locking in Natural Gas (which it consumes) at extremely low rates. So we are looking at AFFO coming in hot for 2024 (at least $6.50 would be our estimate) and then we settle into the low $5's down the line if power prices normalize as the forward strip prices suggest. The stock is hence trading at close to 6-7X AFFO multiples. The company has been spending a lot of money repowering its Genesee 1 and 2 power units in Alberta. These are coal powered plants but this work is close to completion.

{kind=link}

Capex (non sustaining) should be moderating into the back half of 2024-2025 and Capital Power will comfortably cover the dividends from the residual cash flow. In fact, one can easily expect a 6% growth in dividends on top of the generous yield, in our opinion.

Capital Power will reinvest its remaining AFFO into new assets and that is what "powers" the growth. Considering that the dividend will be consuming less than 50% of trough AFFO, we see no issues with this. Of course that brings us to the most important question as to why now is a time to buy. There is some significant degree of volatility in the company's AFFO and EBITDA and it is hard to make a case just based on them. But a price to sales number tends to be a better indicator for this company.

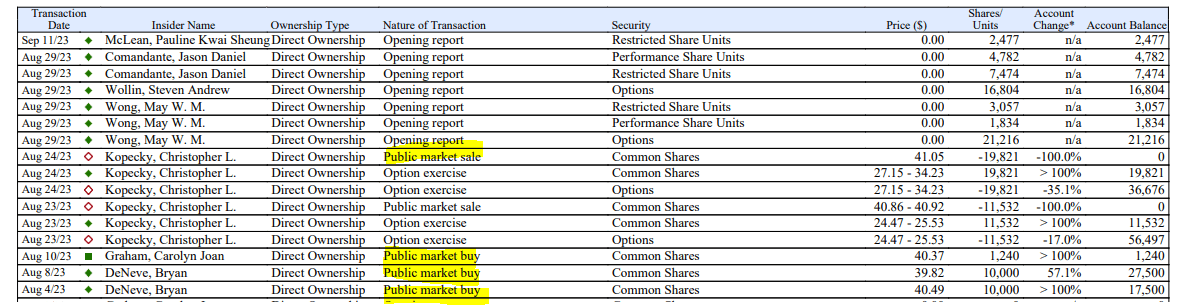

The company has always looked cheap by AFFO and EV to EBITDA multiples, but it is pretty rare to get this down to a 1.1X sales figure. Even this multiple is a bit understated. as the company's cash flow this year has reduced its debt to FFO levels down to an extremely low level. So from here on out we can expect 10% returns annually pretty comfortably. This requires no great level of imagination. The dividend itself is 6%. The trough AFFO (even ignoring the extremely strong years of 2023 and 2024) will be around $3.00 higher than the dividend. If you assume that just half of this amount adds on to the stock price every year, you get about $4.00 of total returns on your $38.00 stock price and your 10% returns are in. Insider activity has also been modestly positive here and that adds faith in the outlook.

{kind=link}

Risks

Power generation is volatile. This applies even to Capital Power with its investment grade balance sheet (VST is junk rated and TAC only has DBRS supporting the IG rating). Alberta continues to shuffle the deck on what it expects from power plants and this remains a wild card into 2024-2025. We don't think this will play a major role, if the forward curves materialize. If the power prices drop as the strip suggests, things will be fine. If we have a spike higher, well we might see some meddling by the government. But the two should offset each other. While some may think this is an overhang, the last time Alberta stepped in to interfere marked the bottom for TAC and Capital Power in 2015-2016.

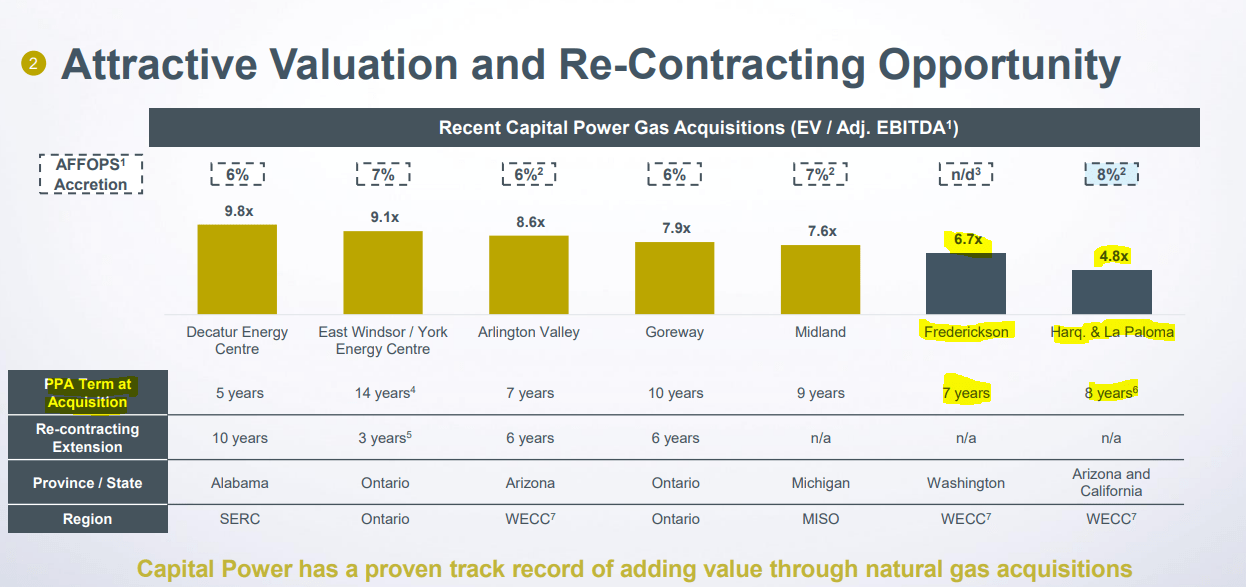

The bigger issue here is the company's purchase of new assets . There are two important lessons from that acquisition. First being that natural gas power assets, even with a nice PPA term, are still being sold rather cheaply.

{kind=link}

This also argues back for CPX to be valued cheaply.

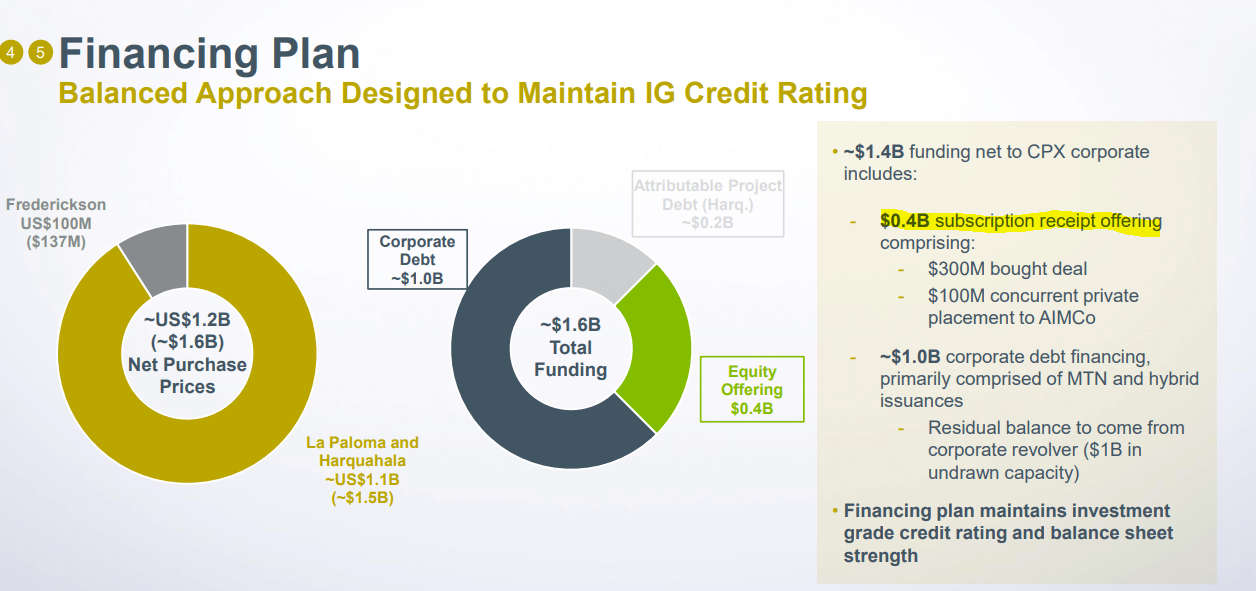

The second lesson here is that if the company is ready to issue stock at this low valuation (they just did in November), don't expect the market to push it higher.

{kind=link}

While the debt portion looks large, keep in mind that the 2023 cash flow had reduced corporate debt quite a lot, so overall this part does not bother us.

Verdict

We like it here and think that the NPV here comfortably exceeds the present day price. Again, we are not reliant on valuation expanding to get 10% returns, but if we manage to sell this out in the next 7 years at a 2.0X revenues multiple, total compounding returns could easily reach 20% annualized. One final note here is that we did not buy the common shares. We bought the Capital Power Corporation subscription receipts, (CPX.R:CA ) which were trading at a 55 cent discount. These are the receipts issued to purchase the recently announced acquisition and will convert into common down the line. There is an extremely low probability that these will be returned to you in cash of $36.45 , if the purchase does not go through. You do receive the dividends which the common shares get until then.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Capital Power: 6.2% Yielder Reaches Attractive Entry Point