CA - Capital Power Offers A 7% Dividend Yield Growing By 6% Per Year

2023-11-02 10:30:00 ET

Summary

- Capital Power, a power producer with assets in Canada and the USA, remains an attractive investment despite the declining appeal of the utilities sector.

- The company reported a strong AFFO performance in the third quarter, meeting expectations and remaining on track towards its full-year targets.

- The dividend sustainability is not up for debate, in my view, with the increased dividend well covered by the company's AFFO and a low payout ratio.

Introduction

Utilities were a sought-after asset class in the past decade as the reliable cash flows and attractive dividend yields caused some income-seekers to focus on this sector to boost their dividend income. Unfortunately, that also means that now the interest rates are moving in the opposite direction, the sector is losing its appeal. But that doesn't mean all utilities are suddenly 'bad' and I have become increasingly interested in Capital Power ( CPX:CA ) (CPXWF), an Alberta-based power producer with assets in Canada and the USA. The company recently hiked its dividend and thanks to relatively strong power prices, the payout ratio remains firmly below 50% of the AFFO despite offering a 7% dividend yield. I am a buyer at these levels although I do expect the company's EBITDA and AFFO to decrease in the next few years on the back of the normalization of power prices.

A strong AFFO performance in the third quarter

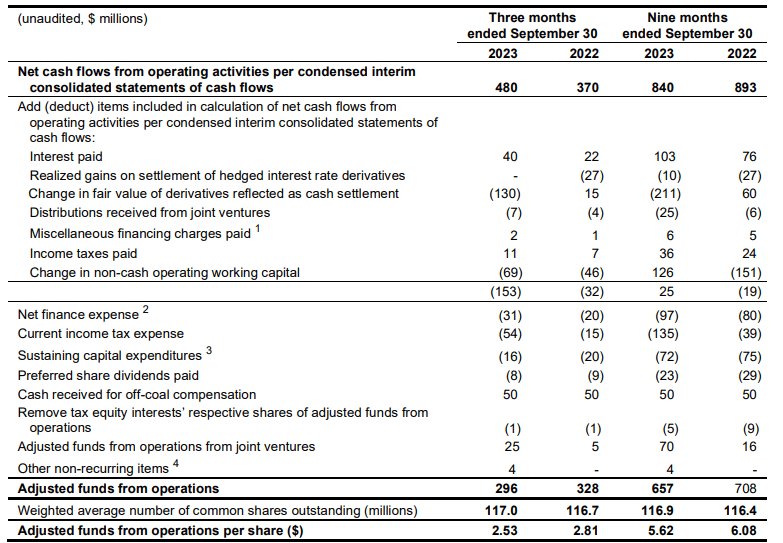

After seeing the relatively strong guidance provided by the company subsequent to its H1 results, I was definitely looking forward to seeing Capital Power's results for the third quarter. As a reminder, the company generated an AFFO of C$361M in the first semester but guided for a full-year AFFO of C$805-865M which indicated it needed in excess of C$440M in AFFO in the second semester to meet the lower end of that guidance.

And Capital Power delivered. Although its AFFO result in the third quarter was lower than in the same quarter of last year, it definitely provided a boost to the 9M 2023 results. As you can see below, the company reported a total adjusted funds flow from operations of C$296M . And while that indeed is about 10% lower than the C$328M it generated in the third quarter of 2022, it for sure keeps the company on track towards its full-year targets.

{kind=link}

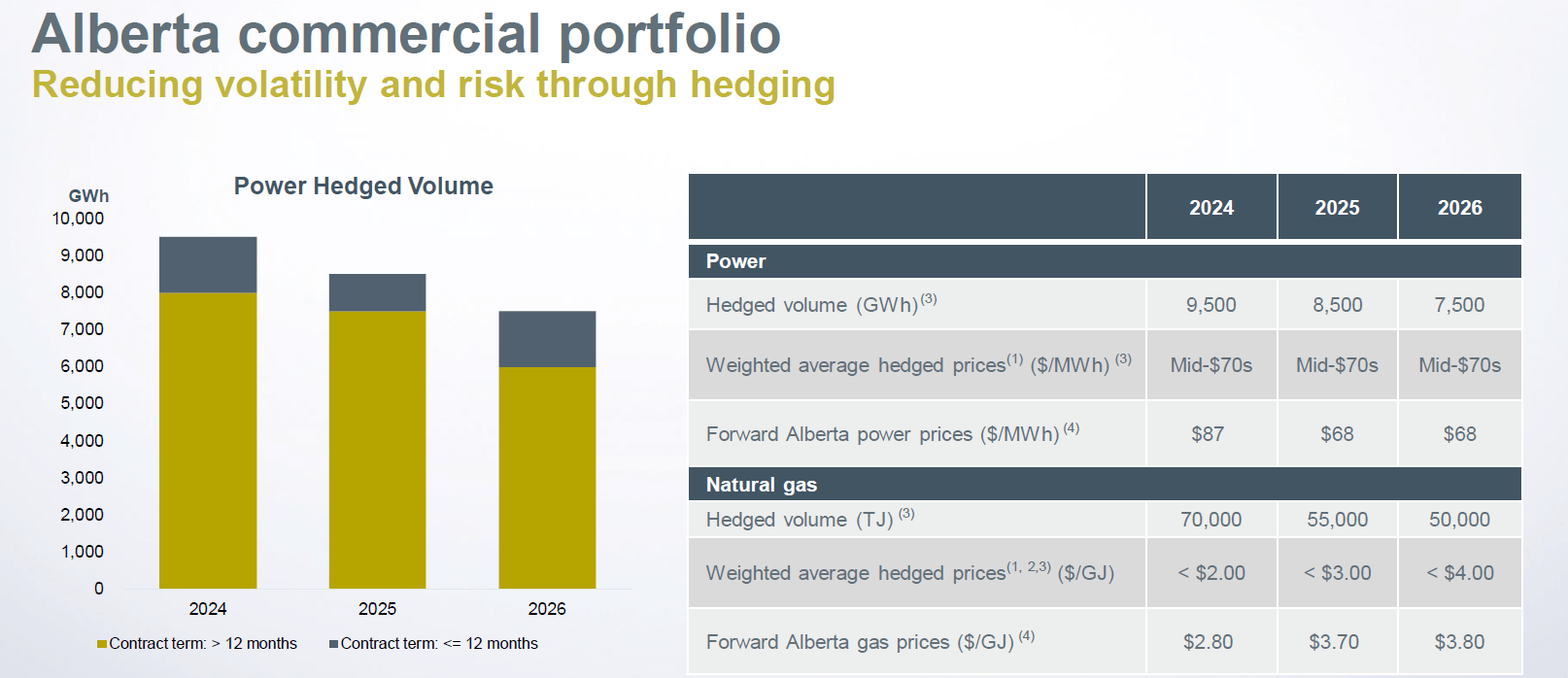

With an AFFO of C$2.53 per share, the company did meet the expectations and don't let the relatively weak performance compared to Q3 2022 pull the wool over your eyes. Electricity prices were pretty high last year and have come off those highs. Although Capital Power has hedged a portion of its energy production, its average realized price is obviously a bit lower than in the same quarter last year. This trend of lower realized prices will likely continue into the next few years as electricity prices normalize and existing hedges at higher prices will roll off. As you can see below, the company has hedged a portion of its anticipated electricity production in Alberta at prices in the mid-C$70 range. While that will work against Capital Power in 2024 as the forward curve indicates market prices are slightly higher, the smart hedging policy results in Capital Power having hedged a substantial portion of its Alberta output for 2025 and 2026 at prices above the current forward prices.

{kind=link}

And just to give you an idea of how important the hedge book is; the total power production in Alberta will likely be 15,000-16,000 GWh which means that about half of the anticipated power production in 2025 and 2026 has been hedged at higher prices.

That being said, the average realized electricity price in those years will be lower than the 2023 and likely the 2024 prices. So we should expect the company's EBITDA (and AFFO) to show a gradual decline as power prices normalize. The company can mitigate the impact of lower prices simply by expanding its operations and producing more power.

And Capital Power is doing just that. In October, the company announced it signed an agreement to acquire a 50.15% stake in the Frederickson 1 Generating Station from Atlantic Power & Utilities. This plant is a 265 MW natural gas fired combined cycle plant in Washington State. The company is paying C$137M for the acquisition while it expects to generate about C$21M in annual EBITDA in the 2024-2029 period based on the current tolling agreements for the facility. This acquisition also makes sense for Capital Power because it owns some land directly adjacent to the power plant and the company may decide to expand operations by building battery capacity.

Why the dividend sustainability is not up for debate

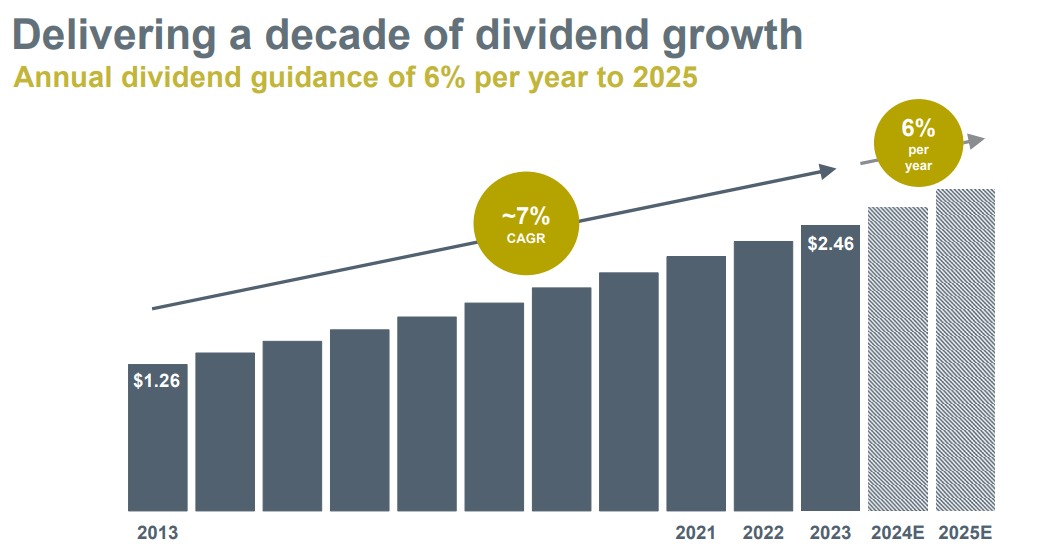

Utilities are liked by the market for their sometimes generous dividend policies and Capital Power is no exception. The company recently hiked its quarterly dividend payment to C$0.615 per share . The annualized dividend of C$2.46 represents a dividend yield of 6.9% based on the current share price.

With about 117 million shares outstanding, the increased dividend will cost the company about 288M CAD per year and given this year's guidance to generate north of C$800M in AFFO, it goes without saying the dividend is very well covered.

But as mentioned earlier in this article, as electricity prices normalize we should expect the EBITDA and AFFO to decrease. But that still shouldn't jeopardize the dividend payments given the payout ratio of just 36% based on the lower end of this year's full year guidance. Even if (read: when) the AFFO decreases, I don't expect the payout ratio to exceed 50%.

{kind=link}

The low payout ratio also means the company's guidance to continue to increase its dividend by 6% per year is credible in my view. This implies a dividend of C$2.76 per share for FY 2025 for a dividend yield of almost 7.8% based on the current share price.

Investment thesis

While I understand the nervousness on the markets when it comes to utilities, not all utilities were created equal. Capital Power will likely generate close to C$7/share in AFFO this year (using the lower end of its guidance, as the company confirmed on its conference call it is tracking to a result below the midpoint of the guidance ) which doesn't only mean the dividend is well covered, but also means the company's growth plans are handsomely covered as well.

I have a small long position in Capital Power and plan to add to this position. I realize the EBITDA and AFFO will likely decrease from the 2022 and 2023 levels but even if the EBITDA decreased from almost C$1.5B in 2023 to C$1.25B in a few years from now, the net debt of C$3.4B is low enough to keep the debt metrics under control. This year's debt ratio will be less than 2.5 times EBITDA and even if the EBITDA falls by in excess of 15%, the debt ratio will remain limited to less than 3%. Interest expenses will increase as the era of low interest rates appears to be over but I believe even a 200 bp increase in the cost of debt across the spectrum would be very manageable for the company.

For further details see:

Capital Power Offers A 7% Dividend Yield Growing By 6% Per Year