CA - Cardinal Energy: Holding For Now Keeping Some Powder Dry

Summary

- Cardinal Energy is keeping capex flat for 2023, but expects a modest boost in production from aggressive drilling in the prior year.

- WCS differentials will impact results for Q-4 along with currently lower prices.

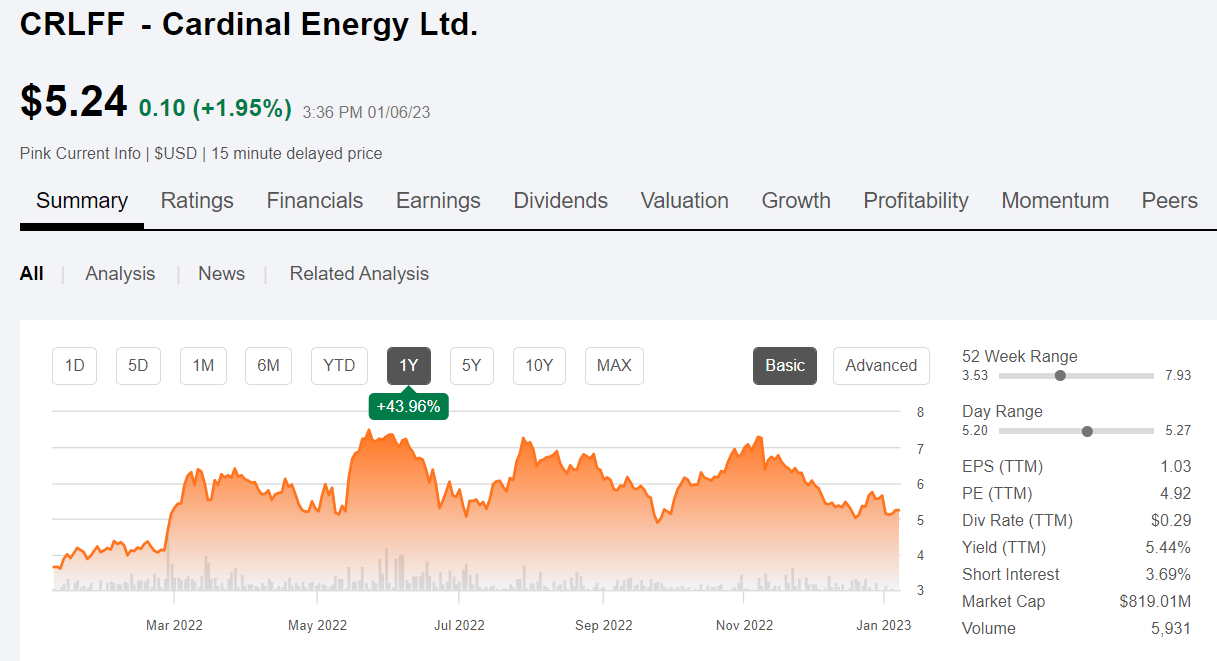

- We are holding for now, but a dip below $5.00 per share would get us off the couch.

- We think better days are ahead and investors with a moderate risk tolerance should put Cardinal on their watch list.

Note: this article appeared in largely its present form in the Daily Drilling Report on January, 7th.

Introduction

Cardinal Energy, (CRLFF) is a company we've wanted to own... someday. It hasn't hit the price target we established for it in our last article, some nine months ago. As so often is the case, I will ask you to refer to that older article for deep-dive information, so we can focus on the current and long term investibility of the stock. Generally, we will be patient as in the near term the stock may struggle a bit from present levels. Here's why.

{kind=link}

The company has made some optimistic assumptions regarding the WSC spread from WTI, ($18 vs $27.4 ) that may impair results for Q-4, 2022. We shouldn't have long to find out and are going to hold-fire at the present.

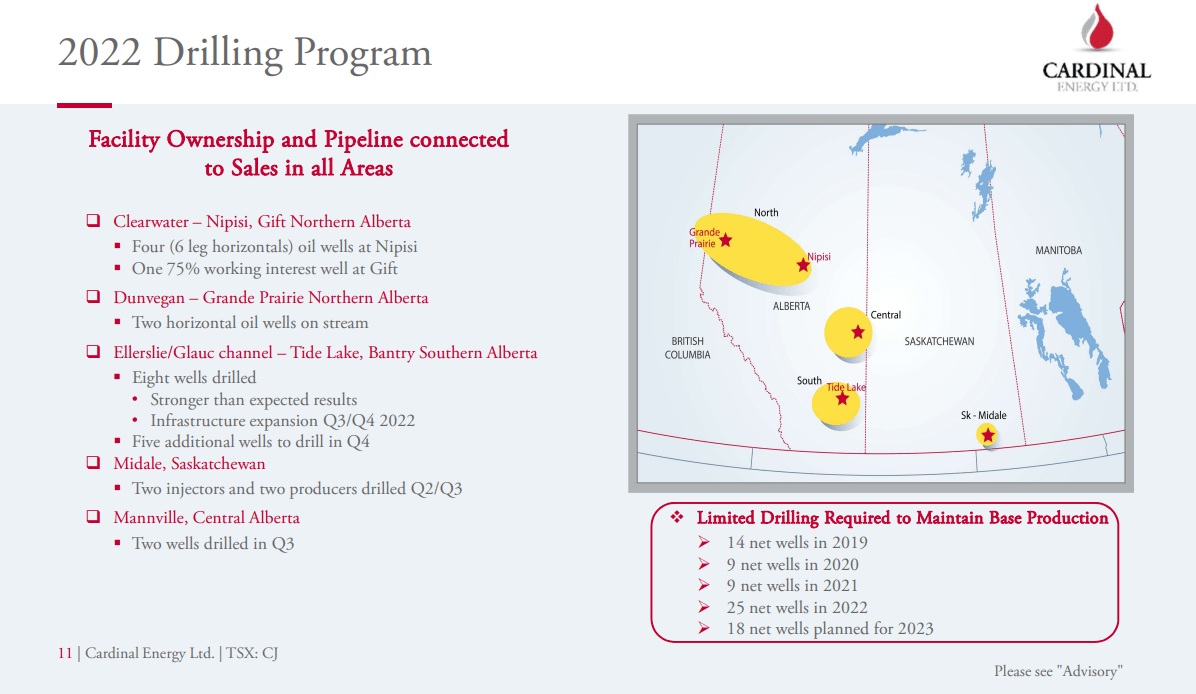

That said, longer term, the company's low decline, light-to-heavy oil water and CO2 floods-~10% annually, provide a steady source of reliable and low cost production. This enables the company to slow drilling when costs are high as shown in the slide below, and still maintain output. 2023 is a pretty good setup for CRLFF, as we think oil is about through consolidating and higher WTI prices are ahead.

{kind=link}

Cardinal Energy had a debt target for Q-4 of $50 mm, which represents an 80% decline YoY. Once LT debt is reduced to zero , the company has an aggressive shareholder return package that will kick in and should be exceedingly lucrative in coming years. In 2022 and planned for 2023 returns thus far have taken the stock buyback route to avoid a new tax on buybacks in Canada in 2024. After that these returns should go toward beefing up the currently, very modest $0.24 CAD annual dividend.

Water and CO2 flooding

We've covered "flooding-style" production a good bit in the past, but a refresher for those who are new is in order. Of all the ways you can coax oil out of the ground, water floods, sometimes called EOR, are among the lowest cost long term. Water floods drive oil toward producing wells. The water cut is separated at the surface for reinjection, and the oil kept in tanks for pickup or piped to a sales point.

CO2 is generally the last resort at "squeegeeing" a little more out of a particular interval, but the carbon sequestration gambit adds some new punch to this "tertiary" phase of EOR-Enhanced Oil Recovery, development. The gas is miscible in the oil and helps to charge it up and thin the oil as it is injected. In the formation the CO2 reacts with minerals in connate brines to form carbonate precipitates or scales, and is permanently stored geologically in this fashion. Permanent in geological terms is a bit of an oxymoron, but it gets bandied about by those with a certain chartreuse -ish stripe in a happy way, so we'll use it as well. Sadly, Canada exempts EOR sequestration from the nice carbon credit package they implemented a while back. Darn the luck!

{kind=link}

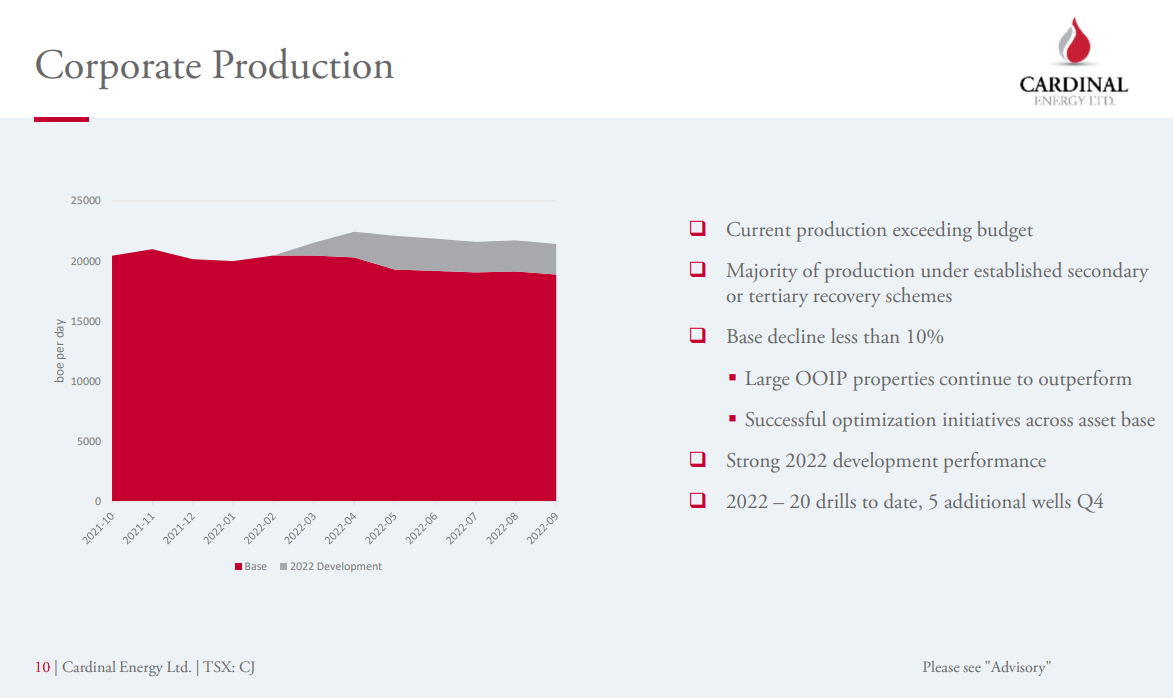

Last year, across its portfolio, Cardinal brought in 25 new wells on a capex budget of ~$97 mm, about $43 mm of which is D&C-Drilling and Completion cost. That works out to just about $1.73 mm a pop, which is recovered in just about 6-8 months on-line.

It was enough to completely offset their base decline and grow overall production by several percent. From what I can see in their guidance, capex and growth plans remain about the same for 2023.

{kind=link}

Here are management's comments to that effect:

For 2023, we will continue with a prudent financial plan that will allow the Company to show a 3% year over year average production growth on a $97 million capital budget. Our budget is based on an oil price of US$80 WTI and our sensitivity to a US$1 change in WTI is approximately $7 million in adjusted funds flow. ( Source )

The beauty of all of this is it's pretty low tech and relies on decades old infrastructure. About the only topside capex needed are pumps-stainless or inert material, CO2 is horribly corrosive, and a supply line for the gas. Easy peasy.

Q-3, 2022-USD

In Q-3, 2022 Cardinal had revenues of $102mm, down from Q-2 as expected. Cash flow fell to $71 mm and netbacks fell to $34-ish. Obviously, lower WTI prices and higher WCS discounts were taking their toll. Let's not dwell on the past, what can we expect in Q-4?

Guidance for Q-4

In Q-3 revenues were off 25% from Q-2 which, with realized prices near $110 per BOE, was certainly atypical. I think revenues for Q-4 will probably come in just below Q-1's, say, $95 mm-ish, taking an average of $85 per barrel for WTI for each period, and putting the netback in the low-$30's. Quite a step down, but those WSC differentials are killers. Hence my call to wait at least into the sub-$5's before staging into Cardinal. The CME forward curve doesn't hold out a lot of hope for the WCS spread narrowing anytime soon, suggesting the current situation is structural-meaning pipeline capacity related.

That should be the worst of it for 2023, if as we expect crude prices begin to move higher. ( Source )

Your takeaway

I like low cost/low decline companies like Cardinal. They aren't flashy but are set up to produce reliable revenues year after year, without taking on a lot of debt. With their balance sheet drudgework behind them, 2024 looks like it holds good prospects for enhanced dividends. The company's commentary regarding debt reduction and shareholder returns plans:

With current forecasts of oil prices to exceed US$80 WTI in 2023, we currently expect to have significant free cash flows in excess of our base budget and dividend outlay plans. The excess free cash flow will first be applied to reducing our net debt to zero. With current higher interest rates the cost to borrow is close to the dividend yield. After our debt is fully repaid, funds previously used for interest can be repurposed. Our second priority after our debt is eliminated will be to increase returns to shareholders in 2023 via dividends and purchases under our NCIB. With the recent federal government announcement of a tax on share buybacks in 2024 we expect companies will be motivated to increase buyback activities in 2023. ( Source )

Cardinal is trading at 3.5X forward EV/EBITDA, so it is already investable; we're just hoping for a little better price. The price per flowing barrel is $39K and not really expensive compared to some players, particularly shale companies with much higher well costs.

If oil bottomed out in Q-4, 2022 as a I suspect will be the case, we are in pretty good shape for a return to $100 oil as we have posited on numerous occasions, and still maintain that it is the easiest path from here. In that light, Cardinal is unhedged and has full exposure to higher prices should they come.

The professional analyst cadre is suggesting we overweight Cardinal at current prices, with 4 of 7 rating it as a hold. Price targets range from ~$8.00 USD to ~$10 USD, suggesting a reasonable upside at current prices. I think those may be a little aggressive given the back and forth in oil right now. I don't think I'd be interested in this one until a dip below $5.00 USD.

Patience is a virtue when stalking prey... and oil companies.

For further details see:

Cardinal Energy: Holding For Now, Keeping Some Powder Dry