CA - Cardinal Energy: Large Q3 Increase In Funds Flow Due To Energy Prices Rebound

2023-11-07 09:00:25 ET

Summary

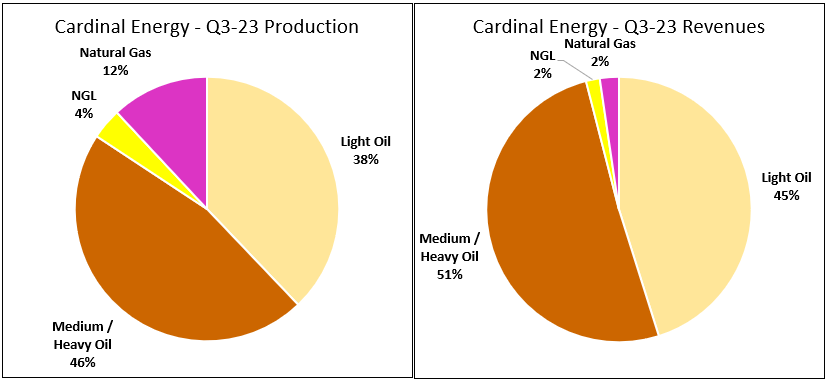

- Cardinal Energy Ltd. is a Canadian oil producer primarily focused on liquids production, spread between light and medium/heavy oil.

- The netback increased substantially in Q3, due to a higher sales price and relatively flat expenses.

- The valuation remains attractive for Cardinal Energy, which is now looking to grow production significantly in 2025-2026.

Investment Thesis

Cardinal Energy Ltd. (CRLFF)(CJ:CA) is a smaller Canadian oil producer, with most of its production and revenues coming from light and medium/heavy oil. I have covered the company a few times earlier this year and those articles can be found here .

Figure 1 - Source: Cardinal Energy Q3-23 MDA

{kind=link}

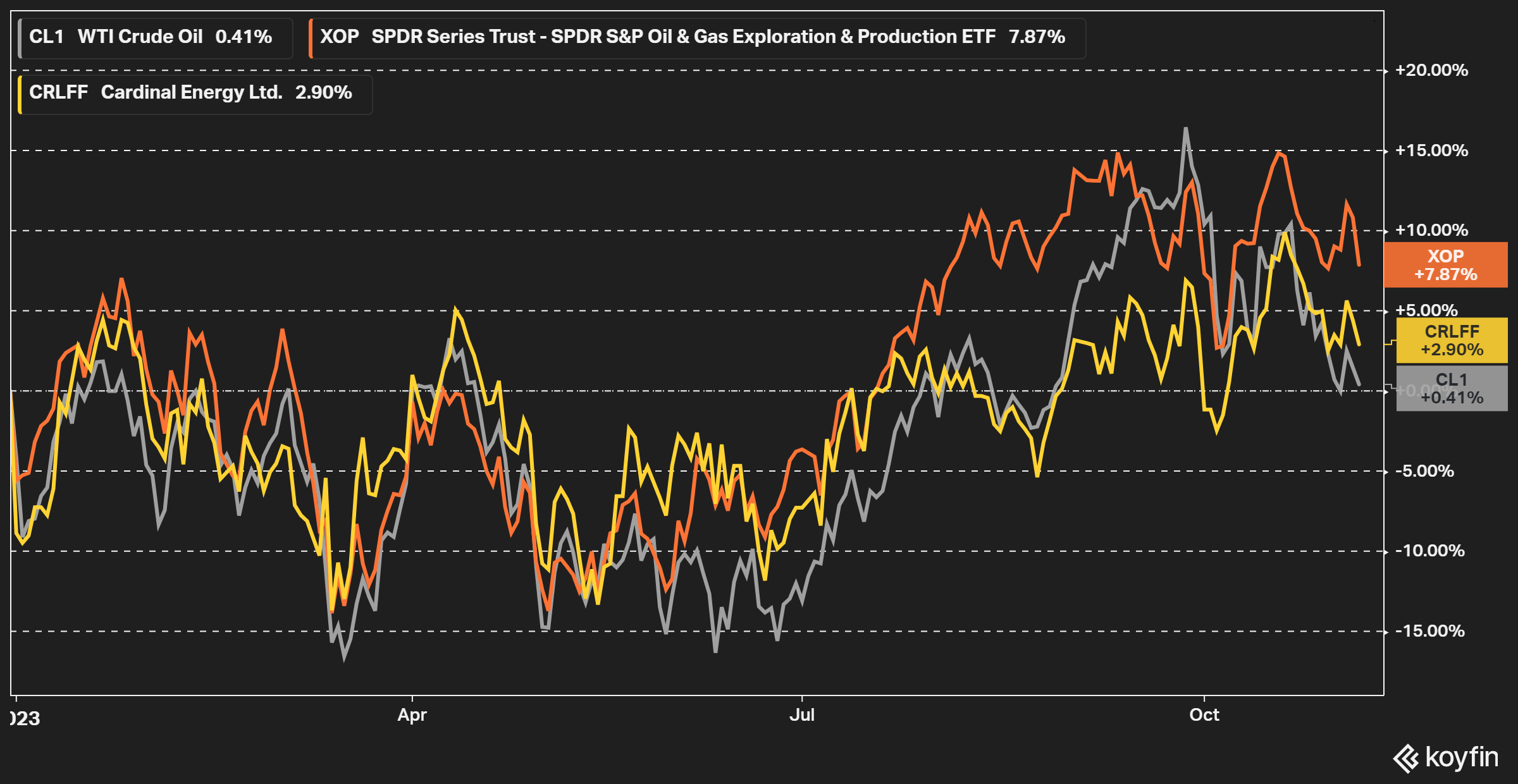

The performance of Cardinal Energy has lagged slightly YTD, which is a little bit surprising when we consider the high percentage of production coming from oil together with high shareholder distributions. The company has very few commodity hedges as well, so if we see even more upside in energy prices, that will benefit Cardinal Energy more than many of its peers.

{kind=link}

There was a shorter period during Q2 with slightly lower production, due to the wildfires in Canada, but the company has maintained the annual production guidance of 22,000. With that said, the annual production is now more likely to end up somewhere in the 21,500-22,000 boe/d range.

Cardinal Energy reported its Q3 result yesterday after the close, so this article will be focused on that result, and include my general views on the company.

Q3 23 Result

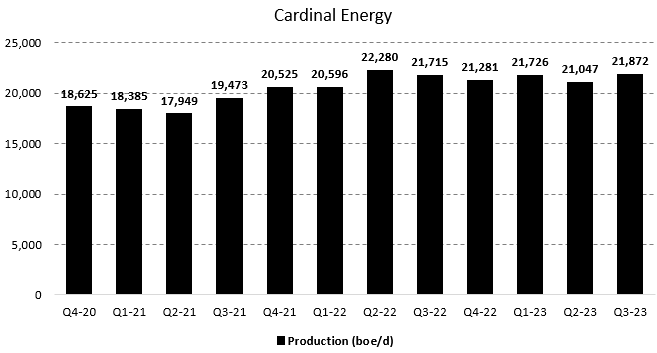

Production in Q3 came in at 21,872 boe/d, which was above the production in the earlier quarters this year, and roughly in line with the annual guidance. The exit production in 2023 is now looking to be around 22,500 boe/d, so another small bump in production is expected in Q4 compared to Q3.

Figure 3 - Source: Cardinal Energy Quarterly Reports

{kind=link}

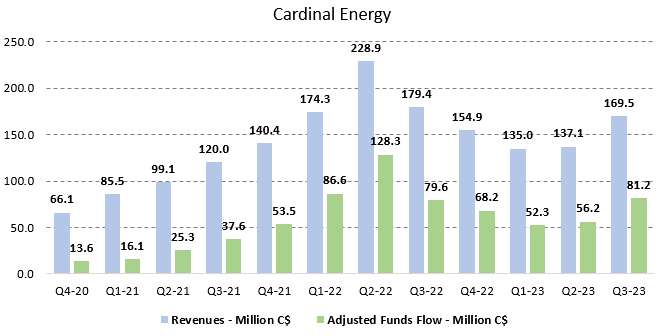

Adjusted funds flow in Q3 was C$81.2M, which was a 45% increase compared to Q2 (C$56.2M). The increase was in part due to the higher production volume, but primarily higher energy prices.

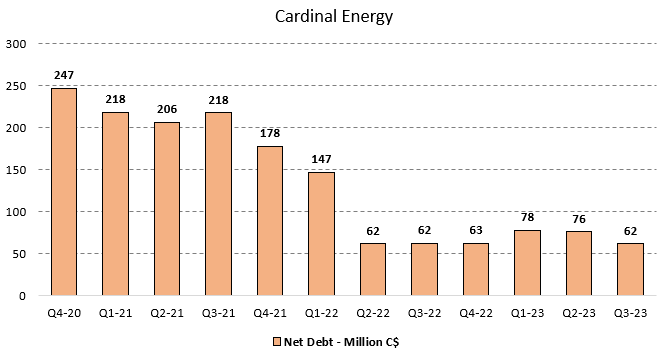

Figure 4 - Source: Cardinal Energy Quarterly Reports

{kind=link}

Due to the strong funds flow, we saw the already low net debt figure decrease further during Q3. The low debt figure offers the company more optionality with regard to capital allocation compared to some peers, which have deleveraged much less.

Cardinal Energy has a sizable dividend paid each month, which comes to a dividend yield of 9.9% using the latest share price. That equals an amount of C$114M annually. Following the end of the quarter, in early October, the company also announced a small C$25M acquisition , which is the main reason we are expected to see a slight increase in production during Q4.

Figure 5 - Source: Cardinal Energy Quarterly Reports

{kind=link}

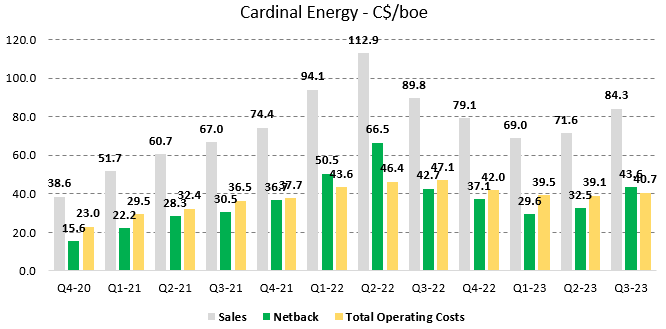

In Q3, Cardinal Energy saw a C$12.7/boe increase in the quarter-over-quarter sales price, which came in at C$84.3/boe, while total operating costs only increased marginally. This caused the netback to increase by C$11.0/boe quarter-over-quarter to C$43.6/boe, which is of course a very encouraging change.

Figure 6 - Source: Cardinal Energy Quarterly Reports

{kind=link}

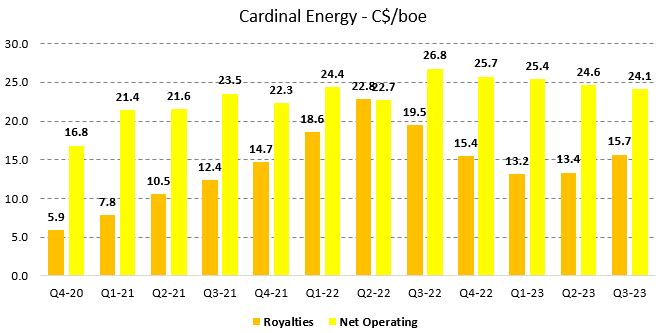

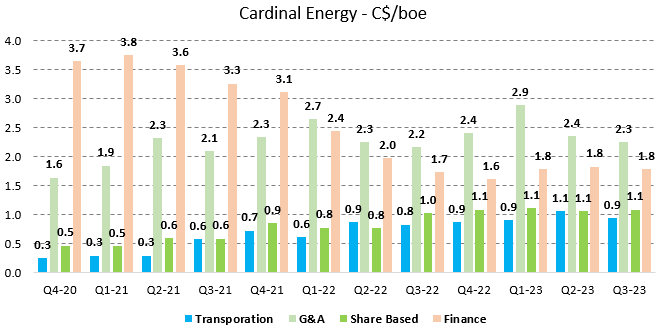

Most expenses were otherwise roughly flat quarter-over-quarter, with the exception of royalties, which naturally increased due to a higher sales price. We have seen net operating cost decline slightly in each quarter during the last year, which is also a very positive trend.

Figure 7 - Source: Cardinal Energy Quarterly Reports Figure 8 - Source: Cardinal Energy Quarterly Reports

{kind=link}

{kind=link}

Conclusion

Cardinal Energy is an unhedged oil producer, with its production split between light and medium/heavy oil. There are no hedges apart from a few WCS-WTI basis swaps.

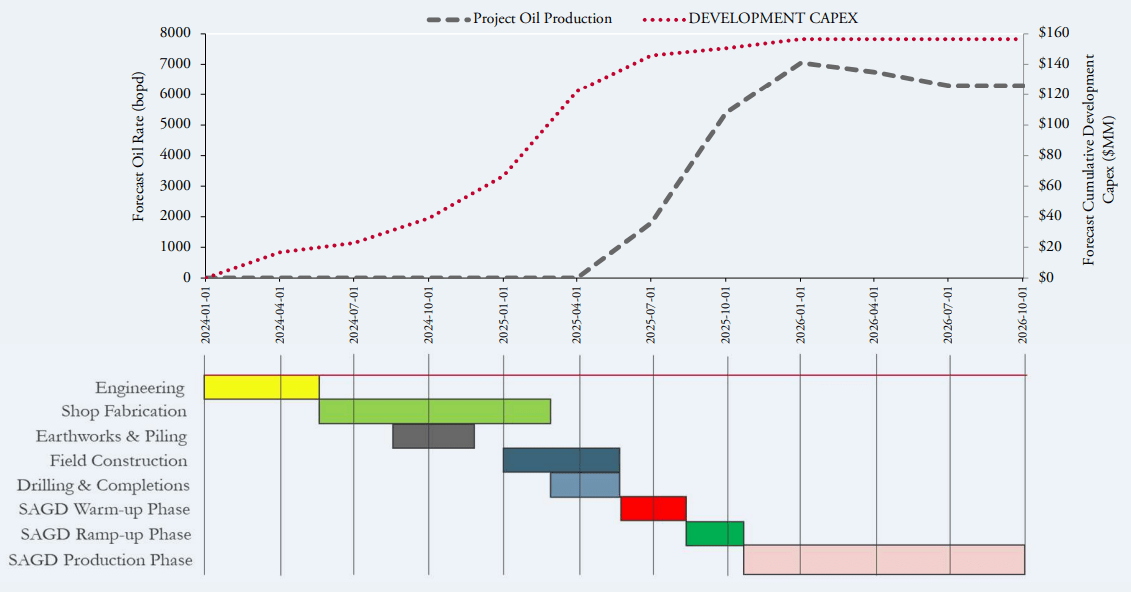

The company did in conjunction with the Q3 23 result release its capital budget for 2024, where the big announcement was the Reford Thermal Project. This growth project has an estimated capital cost of C$155M over the next few years, where C$69M is in 2024.

The project is estimated to grow production of the company by 6,000 boe/d, which equates to a 27% increase on the 2024 guidance of 22,500 boe/d, and lower operating costs. However, production from the project is expected to start in mid-2025 first. Based on the estimates, this is a very cost-efficient way to grow production and boost cash flow in the medium term, but it remains to be seen how it is received by the market.

Figure 9 - Source: Cardinal Energy Corporate Presentation

{kind=link}

Without the Reford Thermal Project, Cardinal Energy is estimated to have a free cash flow yield, of around 15% for 2024 with a WTI price of $80/bbl. Including the growth project in the calculation, the free cash flow drops down just below 10%, which is marginally below the monthly dividend.

However, given how deleveraged Cardinal Energy is at this point, I wouldn't worry too much about the growth spending eating into the dividends. What the project will most likely do is stop further deleveraging, which wasn't needed at this debt level, and delay any buybacks some investors might have been looking forward to.

For anyone critical about the lack of buybacks going forward, I would point out that the reason to do buybacks is to use a low-risk option to grow production, earnings, and cash flow per share. Now, the Reford Thermal Project naturally carries more risk than buybacks, but it will grow production by 27% and lower costs. Using that C$155M for buybacks instead, would at the current stock price decrease the share count by less than 15%. So, Cardinal Energy can be off on the estimates by quite a lot, and the project would still be more accretive compared to buybacks.

I continue to like Cardinal Energy, which might not have the lowest operating costs in the industry, but the high realized sales price and netback in Q3 illustrate that the company is thriving in this environment.

For further details see:

Cardinal Energy: Large Q3 Increase In Funds Flow Due To Energy Prices Rebound