CA - Cardinal Energy: Low Financial Leverage And An Excellent Dividend Yield

2023-04-21 07:53:02 ET

Summary

- Cardinal Energy is a small Canadian oil producer with a large percentage of production coming from liquids.

- The stock has a reasonable valuation, very little financial leverage, and a high dividend yield.

- I consider it a good stock to buy or add to on dips, provided one does not view lower oil prices as a likely scenario.

Investment Thesis

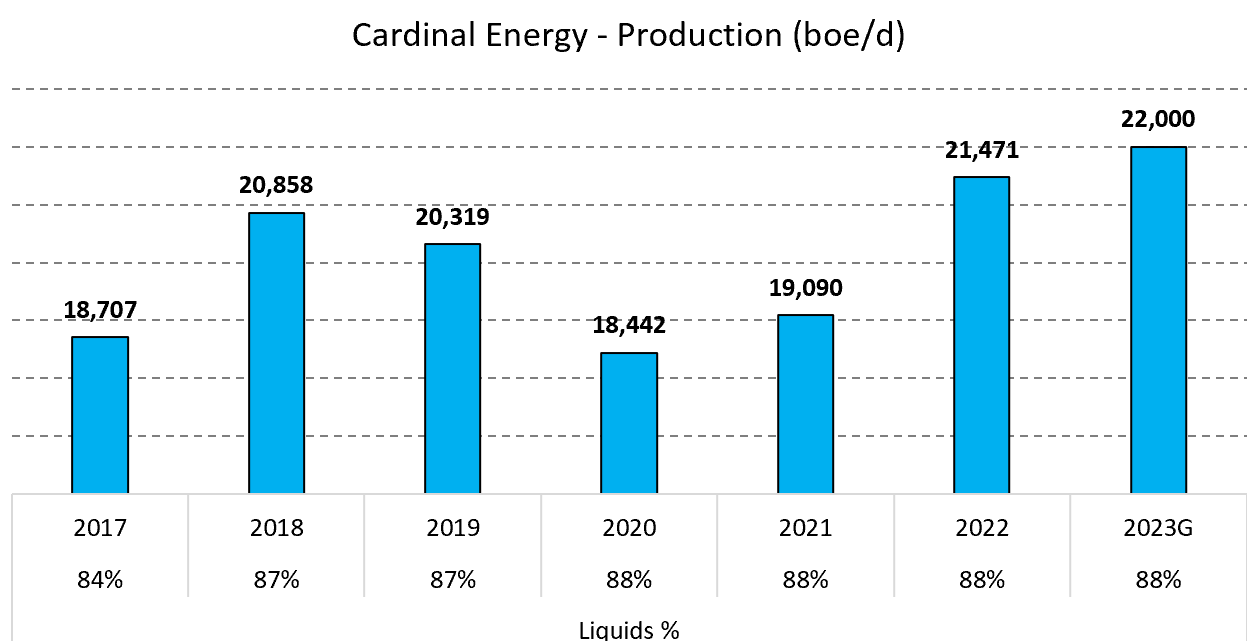

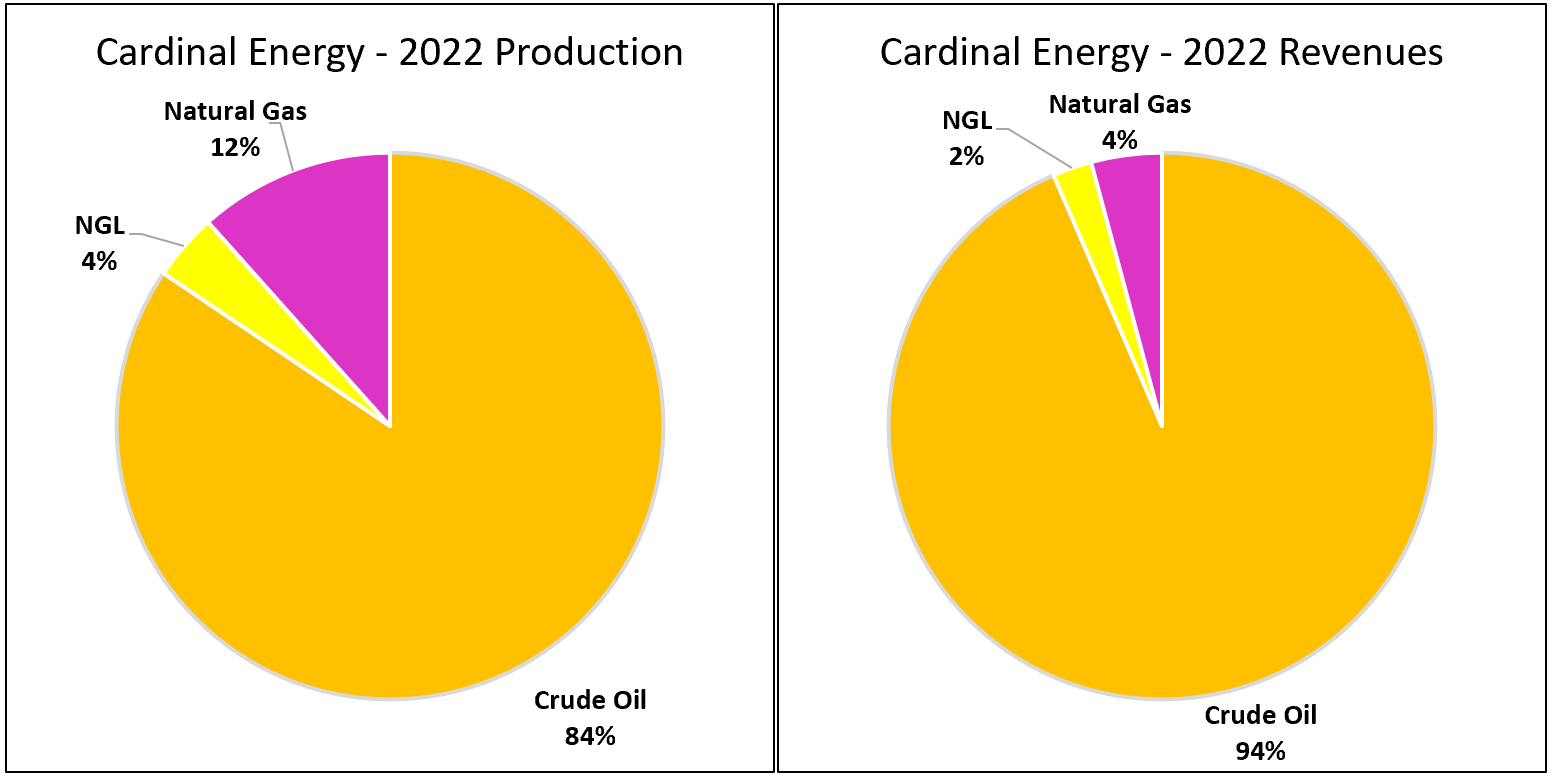

Cardinal Energy ( CRLFF ) is an almost debt-free small Canadian oil producer with a very high dividend yield. The company has had a relatively stable production volume over the last few years, where the vast majority of production and revenues come from liquids.

Figure 1 - Source: Quarterly Reports & Corporate Presentation Figure 2 - Source: Cardinal Q4-22 MDA

{kind=link}

{kind=link}

The company has a reasonable valuation, very little debt, a high percentage of production and revenues coming from liquids. These are welcomed characteristics in a higher interest rate environment when natural gas is rather depressed.

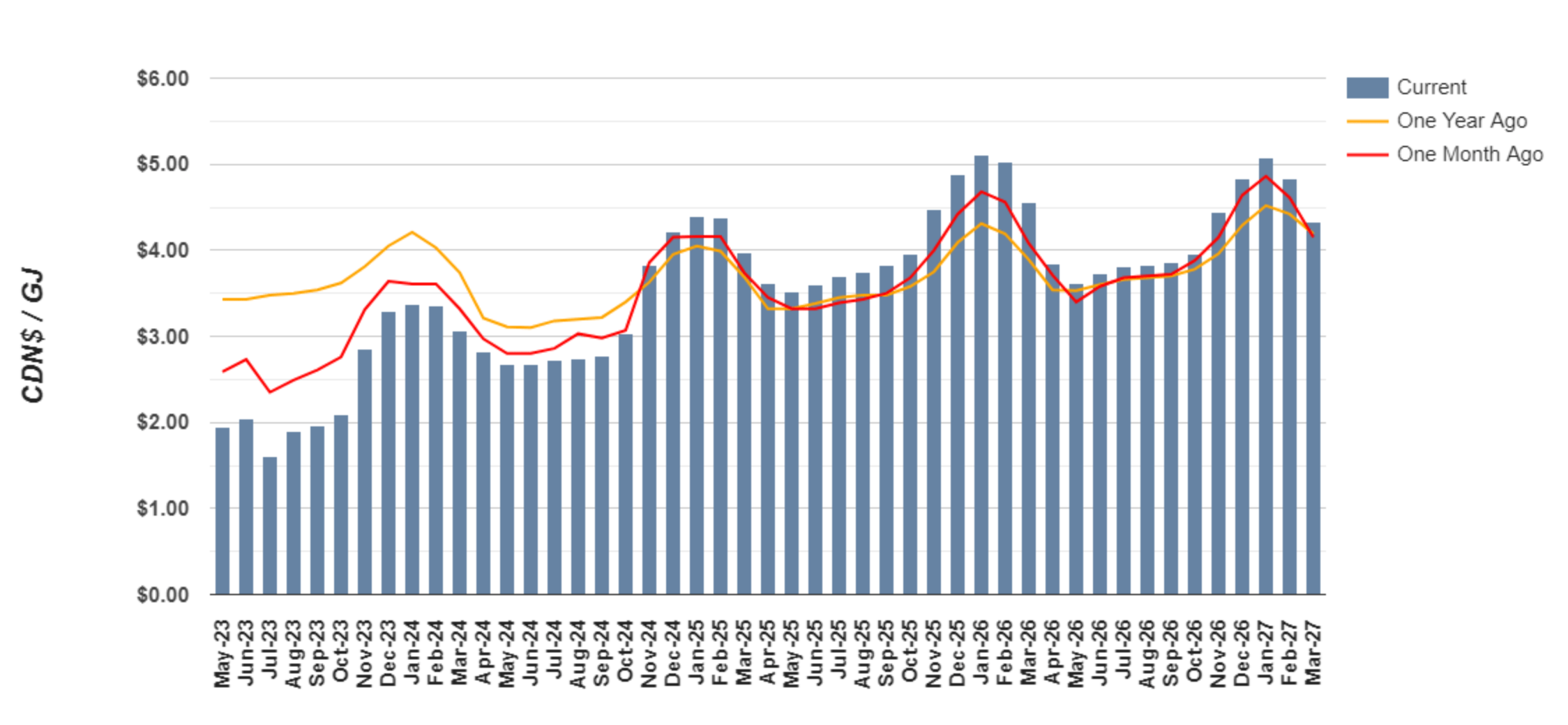

Futures are now indicating Canadian natural gas prices to recover above C$3/GJ in December of this year first, even if that can change relatively quickly. The impact of the lower natural gas prices is only of marginal importance to Cardinal, given the higher percentage of production coming from crude oil.

Figure 3 - Source: gasalberta.com

{kind=link}

Liquidity, Leverage, And Valuation

One clear benefit of Cardinal Energy compared to many other oil producers is that the company has very little financial leverage. Cardinal still relies on debt to fund its operations and the working capital is marginally negative, but the bank debt is only at C$31M as of Q4-22. That is a very minimal amount of debt for a company which is guiding for C$270M in adjusted funds flow in 2023.

{kind=link}

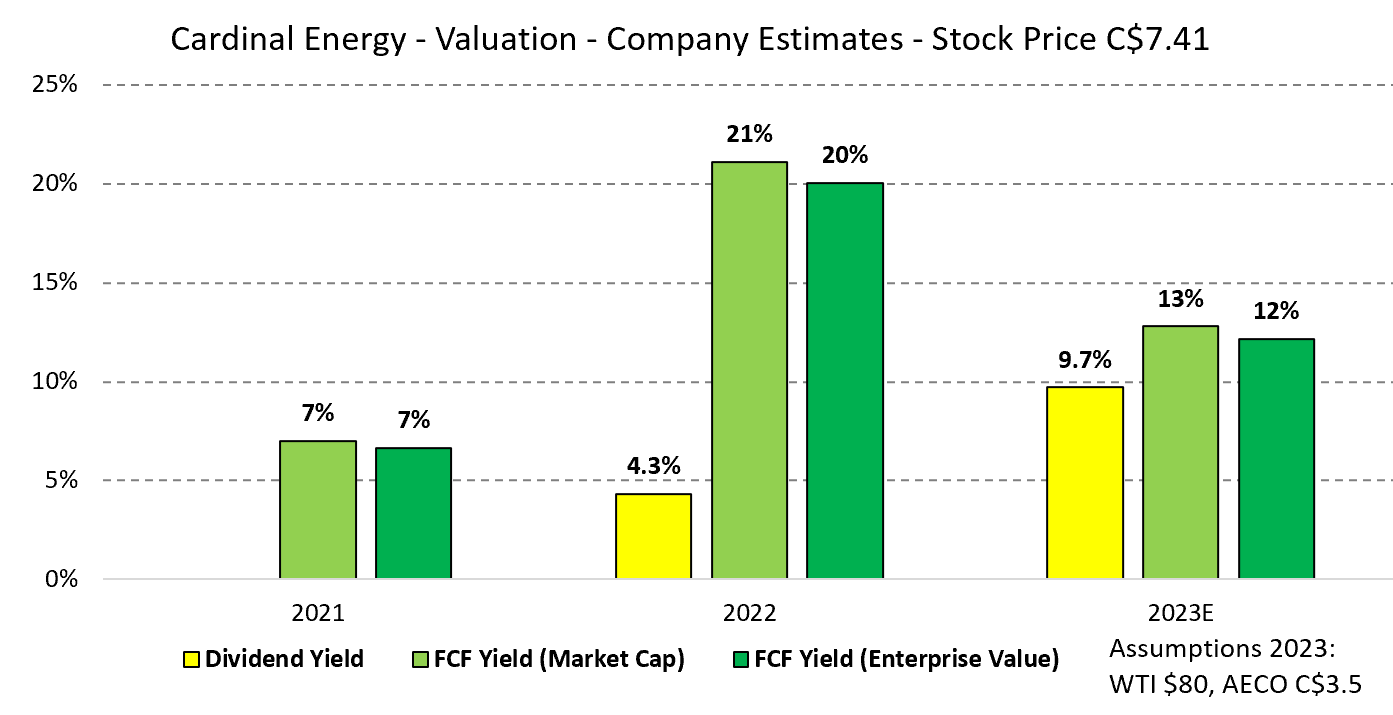

In the chart below, you can see that the company is offering a 12-13% free cash flow yield for 2023, using a WTI price of $80/bbl. However, given the slight differences to the assumptions used for those estimates, we are probably more looking at a free cash flow yield in the 10-12% range for 2023 today.

{kind=link}

The dividend yield that Cardinal offers is excellent at 9.7%, but that is the vast majority of free cash flow with the current oil price. So, if we saw the price of WTI drop down below $70/bbl for more than a brief period, I do think the company will need to reevaluate the dividend level, which could cause the stock to sell off more than peers.

Costs

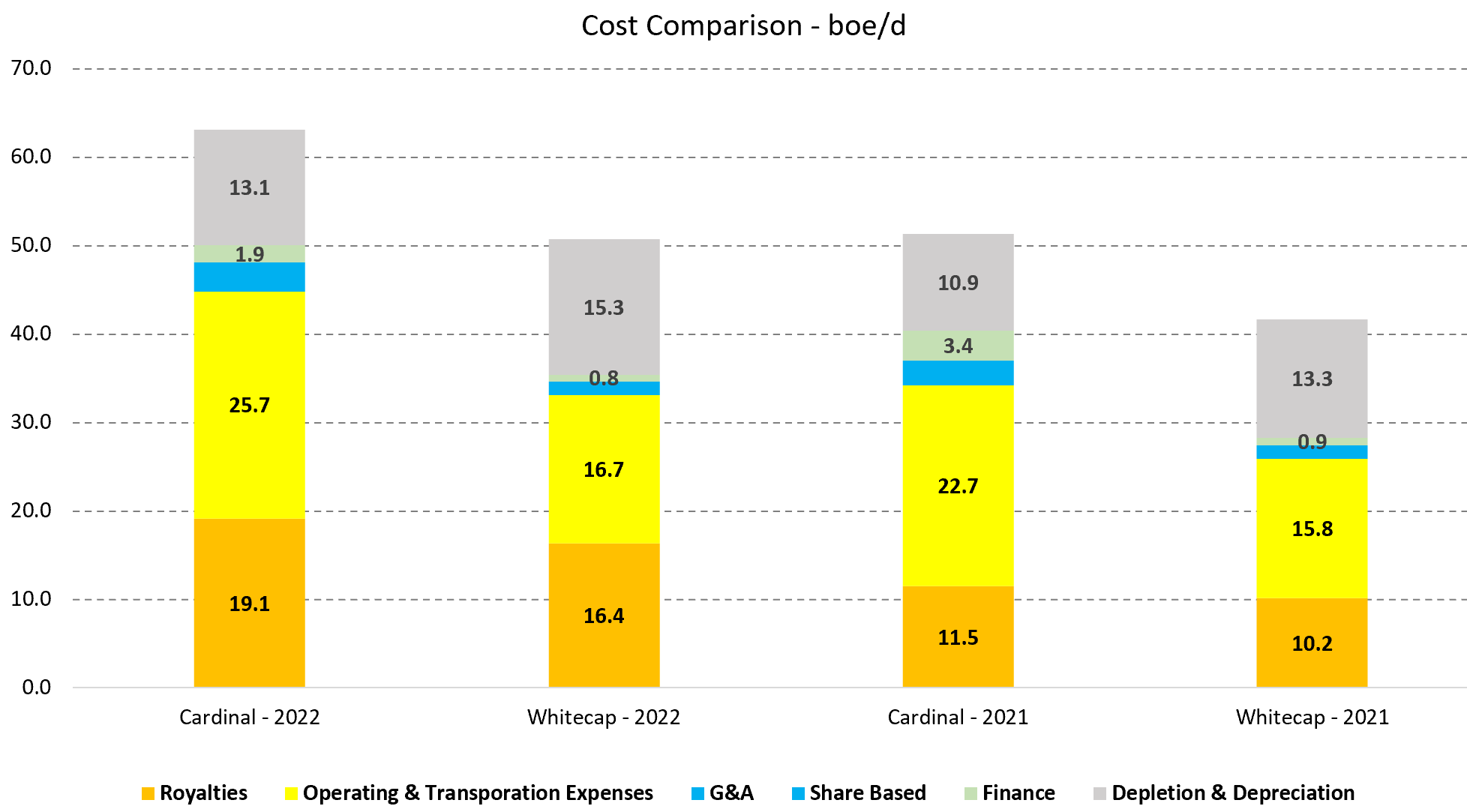

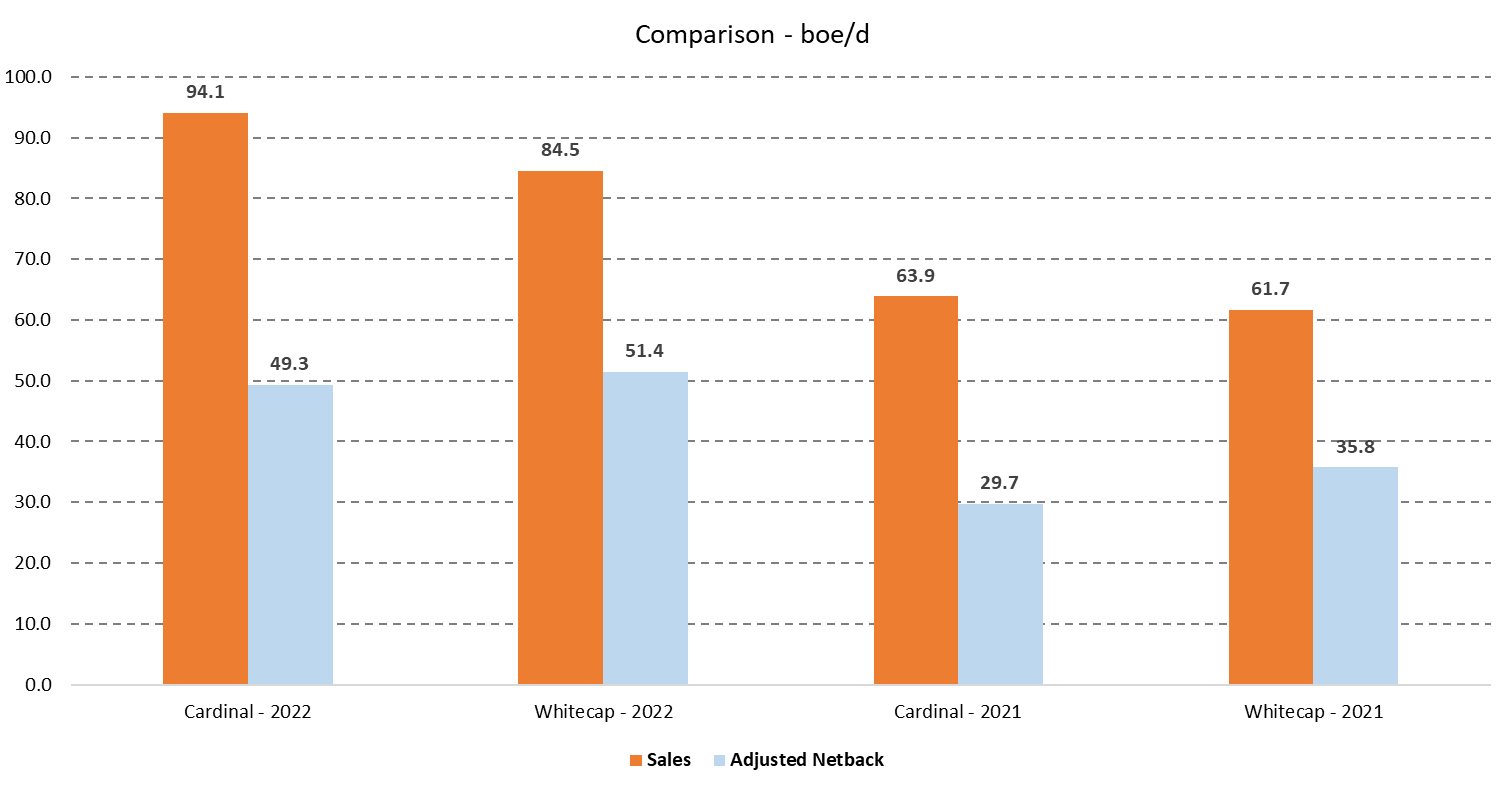

In the chart below, you can see how the costs in barrels of oil equivalent per day of Cardinal compares to Whitecap ( SPGYF ) over the last two years. Whitecap is a much larger Canadian oil producer, but I compared Cardinal to Whitecap to illustrate how it compares to a relatively low-cost operator.

Figure 6 - Source: Quarterly Reports

{kind=link}

The biggest difference between the companies is operating & transportation expenses, where Cardinal is significantly higher. However, that is partly offset by achieving a higher sales price, at least in 2022, due to a higher liquids percentage.

Another aspect to consider is that Cardinal's lower financial leverage will in 2023 improve the company's costs on a relative basis due to higher interest rates. I do think the overall profitability for Cardinal is good compared to the industry at current or higher oil prices, but I also think it is fair to say that the breakeven is higher for a company like Cardinal Energy.

Figure 7 - Source: Quarterly Reports

{kind=link}

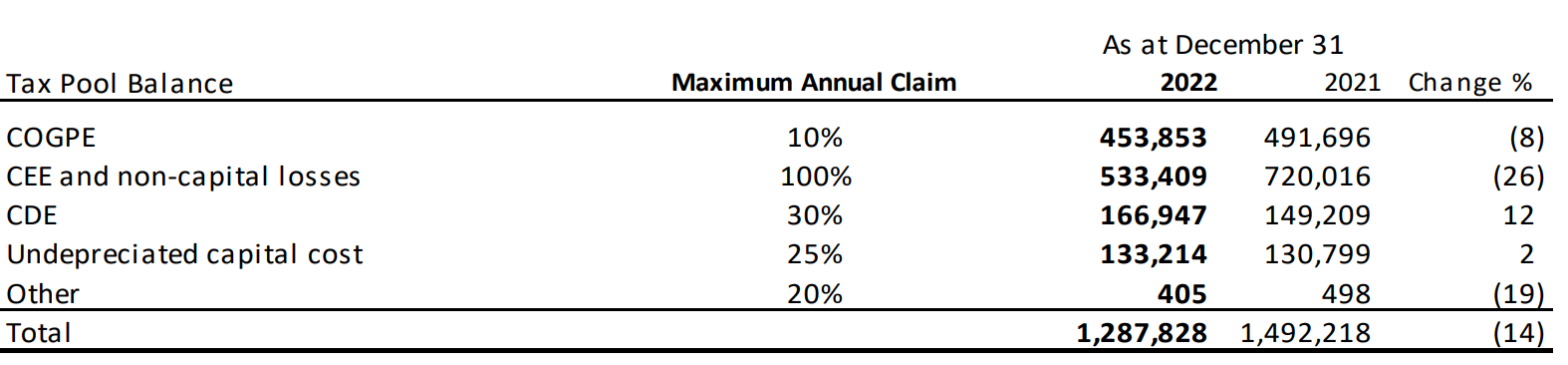

Apart from a good netback level, Cardinal also has a very substantial tax pool of C$1.3B, which means the company is not projecting to pay income taxes until 2026 and beyond.

Figure 8 - Source: Cardinal Energy Q4-22 MDA

{kind=link}

Conclusion

Cardinal Energy is a relatively cheap Canadian oil producer, with some quality characteristics that I like to see in my holdings. The company has a high shareholder distribution, low financial leverage, and a high liquids percentage.

The stock is presently trading with a dividend yield of 9.7%, with monthly distributions, which is no doubt attractive. However, that dividend will not be covered down to a WTI price of $50-60/bbl as for some of the industry peers. That is something every investor should be aware of.

Overall, I like Cardinal Energy, which primarily offers unhedged production, and I would consider adding it to my portfolio if we saw a slight dip from the current level.

For further details see:

Cardinal Energy: Low Financial Leverage And An Excellent Dividend Yield