CA - Carrols Restaurant Group: Financial Turnaround Just Getting Started

2023-03-16 05:39:54 ET

Summary

- TAST reported its Q4 earnings which beat expectations.

- Shares have rallied in recent months based on an improving financial outlook while we see more upside ahead.

- Firming margins and a strengthening balance sheet should be positive tailwinds for the stock.

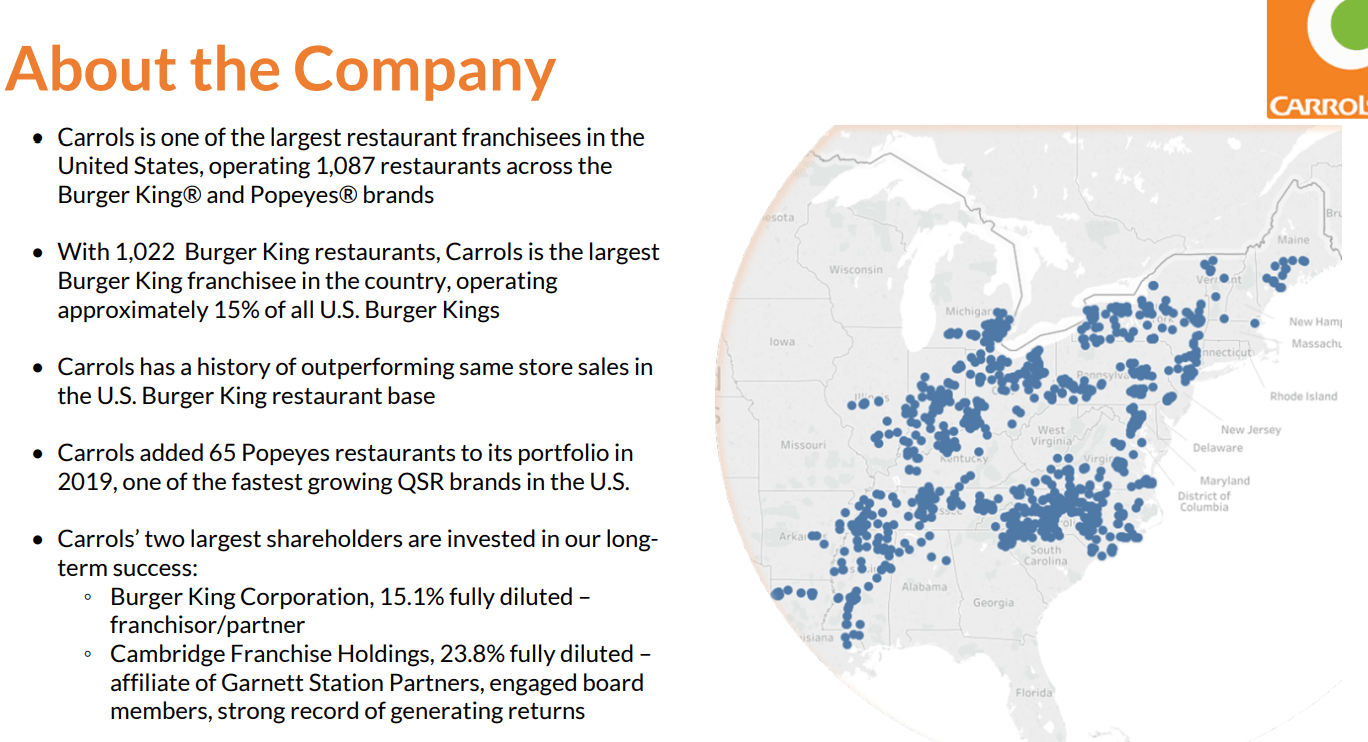

Carrols Restaurant Group, Inc. ( TAST ) operates more than 1,000 "Burger King" restaurants in the U.S. as one of the largest independent franchisees along with a smaller number of "Popeyes" locations. This is a stock we previously covered , highlighting improving conditions compared to significant disruptions going back to the depths of the pandemic.

The update here takes a look at the latest quarterly report defined by solid restaurant-level trends and firming margins, reaffirming a bullish case for the stock. Despite the challenges in recent years, our view is that TAST is well-positioned to emerge stronger with a positive long-term outlook and path to stronger profitability.

TAST Earnings Recap

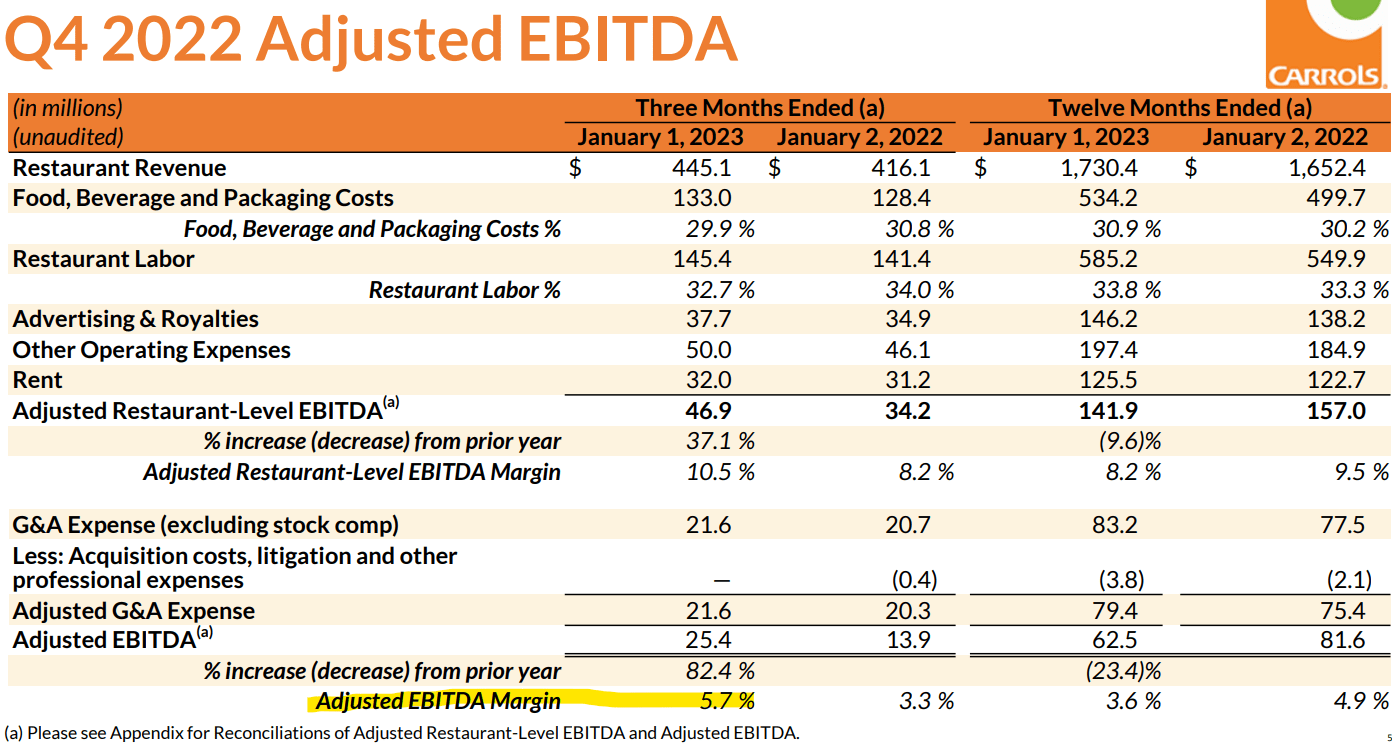

TAST reported a Q4 non-GAAP EPS loss of -$0.05, although this narrowed from a -$0.15 result in the period last year, and was also $0.16 ahead of estimates. Restaurant revenue at $445.1 million climbed by 7% y/y and was also above expectations.

The story has been the solid comparable restaurant sales , up 6.2% for the Burger King locations and 9.2% for Popeyes. During the quarter, expenses related to food, beverage, and packaging costs, along with restaurant labor, have declined as a percentage of revenue.

Management explains that the adjusted EBITDA margin at 5.7% this quarter, up from 3.3% in the period last year, is based on not only easing commodity input inflation but also greater flexibility in the workforce. For context, there was a period in late 2021 when fast-food restaurants were dealing with employee shortages in an exceptionally tight labor market. Those dynamics have passed.

{kind=link}

If we take that Q4 adjusted EBITDA figure of $25.4 million, the annualized level at $100 million starts to look a lot better than the full-year fiscal 2022 result of just $62.5 million. The implication here is for a narrowing leverage ratio which has been the main knock on the stock going back to the extra debt the company took on during the pandemic.

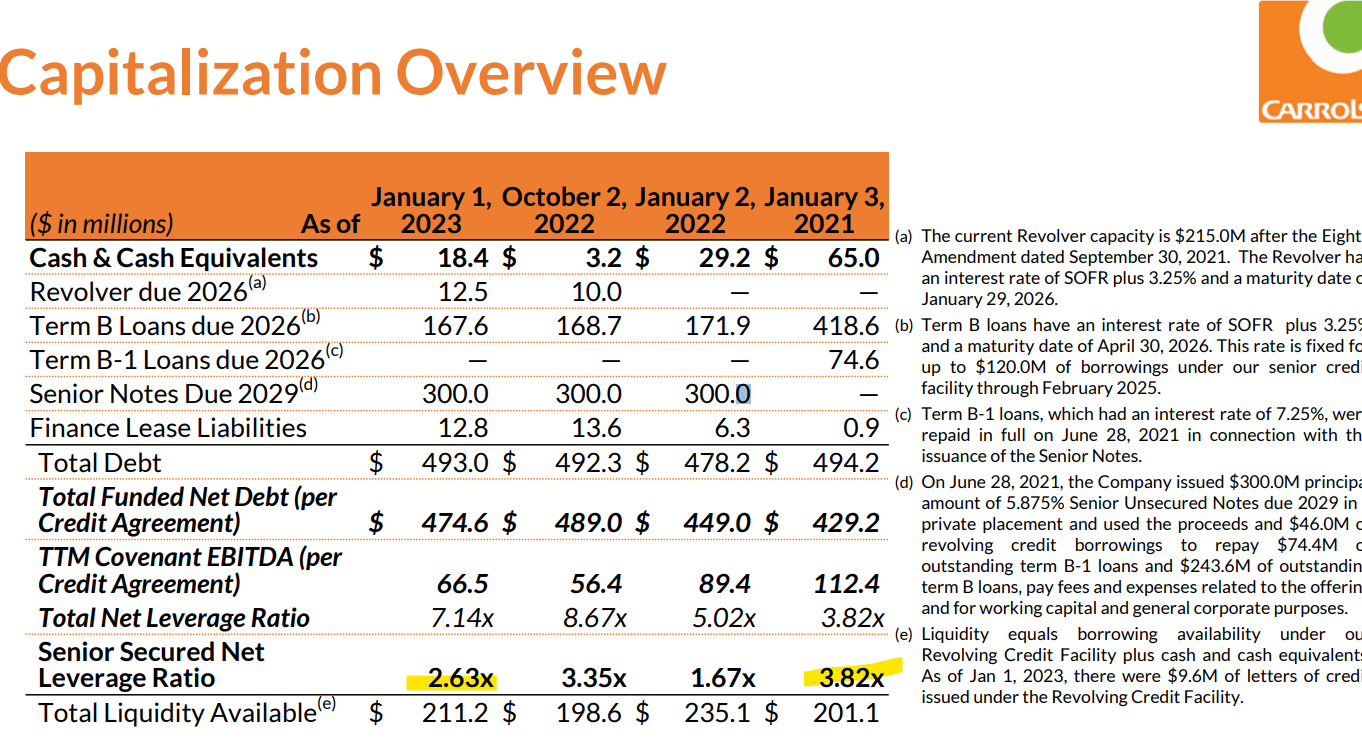

Carrols Restaurant Group ended the quarter with $18.4 million in cash, up from $3.2 million the prior quarter. The senior secured net leverage rate improved to 2.6x from 3.4x in the quarter prior and as high as 3.8x at the end of 2020. In many ways, this ongoing deleveraging that can accelerate through 2023 is one of the strong bullish tailwinds for the stock.

While management is not providing financial guidance targets, comments in the press release projected some optimism suggesting a continuation of the latest trends over the next several quarters.

As we look into 2023, we are excited by the trends we are seeing, both on the top-line and with input costs, and believe we are on track to deliver continued gradual margin improvement over time...

Overall, we believe that the operational improvements we continue to make, combined with the potential positive impacts from Burger King's multi-faceted plan to strengthen the brand, put us in a strong position heading into 2023."

{kind=link}

TAST Price Forecast

The first point here is that TAST with a market cap of $120 million or approximately $600 million enterprise value remains an otherwise speculative small-cap, particularly considering it's not currently profitable. We're taking a bullish outlook on the stock, but just recognize that ongoing volatility is to be expected.

The good news here is that the operation appears to be turning a corner, with the attraction here is that the business is connected to the Burger King and Popeyes brands, meaning it enjoys a broad level of customer loyalty and market recognition as an advantage to the franchise model.

On this point, the parent company of "Burger King Corporation" and "Popeyes" as subsidiaries of Restaurant Brands International ( QSR ) is among TAST's largest shareholders meaning the long-term success of the business is in line with the strategic views of the larger group.

Notably, the company notes that Carrols' operated locations have historically outperformed the broader restaurant base as part of the appeal of the stock. We'd also say that the financial leverage we noted above can make the equity side particularly attractive to the upside as part of the reasoning to invest in TAST over QSR.

{kind=link}

From there, what we like about TAST is the idea that in the current market environment, fast-food restaurants should be a relatively resilient segment of the consumer discretionary sector as consumers will always need to eat. An affordable meal at Burger King or Popeyes would be down the list of spending categories consumers cut even in a recession compared to luxury goods, travel, and leisure for example.

To the upside, a scenario where economic conditions outperform would be positive for even strong comparable restaurant sales and allow profitability to climb even further. Overall, we sense that TAST is simply undervalued as its turnaround is more based on company-specific factors.

We'll note that among several publicly traded restaurant stocks, TAST at an EV to forward EBITDA multiple of 6.6x is well below an average closer to 10x for a group that includes QSR, Brinker International Inc. ( EAT ), Cheesecake Factory Inc. ( CAKE ), Jack in the Box ( JACK ), The Wendy's Co. ( WEN ), and BurgerFi International Inc ( BFI ). Keep in mind that these names each have varying business models, but we believe there is room for TAST to converge higher with the group.

TAST Stock Price Forecast

We rate TAST as a buy with a new price target of $3.00 representing an 8x EV to forward EBITDA multiple on the current consensus EBITDA estimate of $90 million for the full year 2023. This is a level the stock traded at in early Q1 2022, which could be on the table as shares build momentum.

We want to see another strong series of quarterly reports, confirming the strengthening margins and the balance sheet position. On the other hand, weaker-than-expected results including softer comparable restaurant sales would likely force a reassessment of the outlook as the risk to watch.

{kind=link}

For further details see:

Carrols Restaurant Group: Financial Turnaround Just Getting Started