CARS - Cars.com: Still Strong Trends But Upside Is Limited

2023-08-02 12:10:38 ET

Summary

- The company continues to show growth in revenue and improvement in the operating margin.

- The company's shares are not cheaply priced according to multiples, while I do not see additional growth catalysts.

- Cars.com shares have risen 65% YTD and hit the price target I wrote about in my previous article, so my recommendation is hold.

Introduction

Shares of Cars.com ( CARS ) have risen 65% YTD. Since my last publication , where I recommended buying the company's shares, quotes have risen by 47%, while the S&P 500 index has shown growth by 15%. Despite the solid operating and financial performance, I believe that now is not the best time to go long.

Investment thesis

For now, I'm keeping a hold recommendation for the company's stock because: First, the current stock price is close to my $24/share target price I wrote about in my previous article. Secondly, quotes rose strongly at the beginning of the year and significantly outpaced the growth of the index, while I do not see additional growth drivers/catalysts in the following quarters. Thirdly, in my personal opinion, in accordance with the multiples, the company is not valued cheaply, the shares are traded at a premium both to the sector median and to their own historical values.

Company overview

Cars.com operates and maintains an online platform that helps sellers and buyers buy and sell used cars. The company was founded in 1998 and operates in the US market.

My expectations

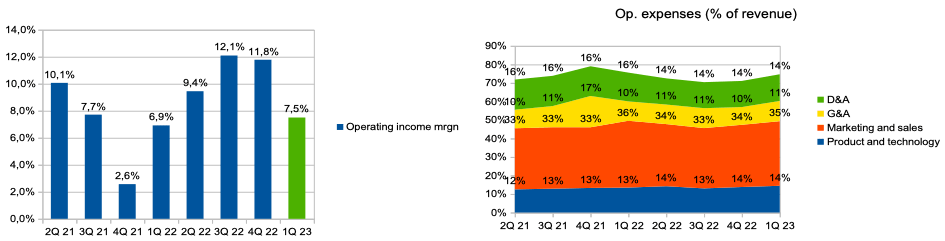

On the one hand, I like the strong and stable operating performance of the company. According to the results of Q1 2023 , platform traffic increased by 11% YoY, and the number of unique visitors increased by 7% YoY, while ARPD (Monthly Average Revenue Per Dealer) increased by 4% YoY, as a result, the company's revenue increased by 6% YoY for the 1st quarter of 2023. Operating margin increased from 6.9% in 1Q 2022 to 7.5% in 1Q 2023 due to a reduction in spending (% of revenue) on marketing and D&A. You can see the details in the charts below.

{kind=link}

However, at the moment, taking into account the current level of valuation and the dynamics of the quotes at the beginning of the year, I do not see additional catalysts/drivers for the growth of shares, thanks to which the quotes could outperform the S&P 500 index.

Firstly, I don't expect we can see a quick rebound in used car sales in quantitative terms in the coming quarters because, in my personal opinion, even if we see inflation slow down in the second half of 2023, consumer spending will bounce back, delayed because consumers continue to face higher spending on food, rent and interest payments. In addition, the recovery of sales in quantitative terms may be affected by the level of inventories among dealers, which, in accordance with statements by companies, is at a relatively low level. In addition, the company reaffirmed, but did not raise, its 2023 revenue guidance, which suggests 3%-6% growth.

Secondly, I expect operating margins to improve slightly in the coming quarters due to effective marketing spend and organic traffic growth on the platform that management spoke about during the Earnings Call following the release of Q1 2023 results , however, I don't think that this can serve as a catalyst for the growth of shares, because, in my personal opinion, the relatively low growth rates of the business will not allow economies of scale to be realized. In addition, I believe that as used car sales recover, we may see increased competition and, consequently, an increase in marketing spending in the coming quarters.

Risks

Revenue: low inventory levels among dealers could lead to lower sales volumes and, consequently, lower revenue growth rates for the company. In addition, the decline in real consumer incomes and high inflation may have a negative impact on consumer spending in the discretionary segment, which may also have a negative impact on business growth rates.

Margin: rising marketing spending due to increased competition in the sector and declining economies of scale could put pressure on business operating margins.

Valuation

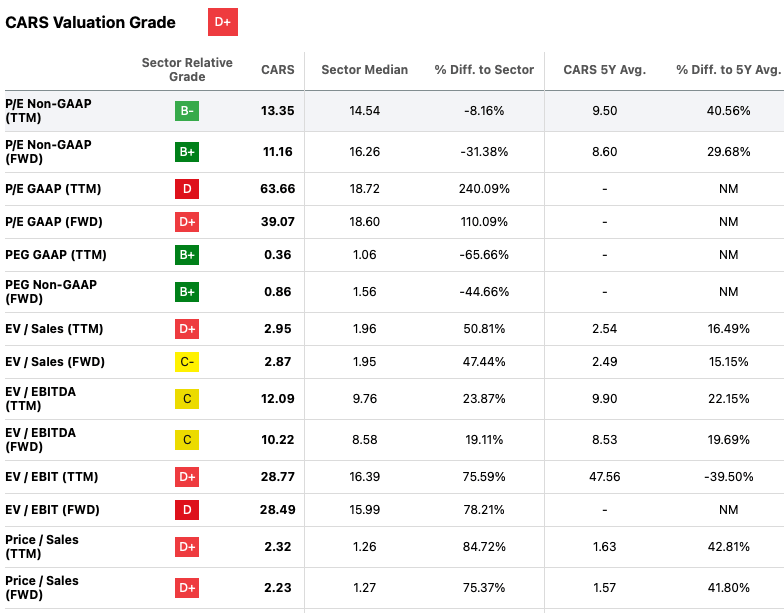

Cars.com's valuation grade is D+. Despite the fact that the P/E ('FWD') the company is trading at is 11.2x, it's still discounted to the sector, under the multiples of EV/EBITDA ('FWD') and P/S ('FWD') the company trades at 12.1x and 2.2x, which are higher than the sector median by 24% and 75% respectively. On the one hand, in my personal opinion, the company deserves a certain premium due to its stable and relatively high operating margins and business scale, however, the current premium to both the sector median and the 5-year average makes me change my view on the company's shares.

{kind=link}

Conclusion

On the one hand, I like the fact that the company continues to demonstrate both business growth in monetary terms and an increase in operating margin, so I avoid the Sell recommendation, however, on the other hand, at the moment I do not see growth drivers that could drive the stock up at current multiples valuation, so I'm sticking with the hold recommendation for the company's stock.

For further details see:

Cars.com: Still Strong Trends But Upside Is Limited