CVNA - Carvana: Catching A Falling Knife Might Get You Cut

2023-04-27 12:03:23 ET

Summary

- Growing losses even in period of high used car sale prices are a sign of long term unsustainability.

- Corporate governance alone should be a red flag for prospective investors.

- Aggressive accounting practices are not a good sign for general reliance on company figures.

- Cash problems, high debt and growing interest rates might be the straws that broke the camel's back.

Carvana ( CVNA ) has been suffering tremendously in the past years, trading now at roughly $8 per share - about 97.75% below the August 2021 highs. With high debt and rising interest rates, falling margins and non-existent profits, and overall negative market sentiment, I would run away from this stock as fast as possible. If you're a current shareholder of Carvana would suggest realizing your losses and reallocating what's left to other investments.

Promising Mission

In theory, Carvana has a very interesting business model - buying a selling used cars online without any of the time-consuming interactions of a typical in-person transaction with a dealer or a private seller is very appealing. Furthermore, most people that saw either in person or online the car "vending machines" are inevitably drawn in with curiosity.

According Carvana , their mission is to change the used vehicle market by providing a completely online car buying experience, streamlining the process and eliminating the need for a dealership. They also emphasize the honesty and transparency with their 7-day money-back guarantee returns and allegedly outstanding customer service. To be fair, they did manage to revolutionize a very old and painful process, with customers being able to buy and sell cars in under 10 minutes, get easy access to financing and many other perks.

With this online-heavy mission, many investors and analysts have been long-time supporters of the stock, even calling it the Amazon ( AMZN ) of cars. For instance, Morgan Stanley's Adam Jones has issued price targets as high as $430 dollars on the basis of a growing market share of online retail. However, even Morgan Stanley had to recognize the difficulties the company is facing and changed its predictions to a base case range between 1$ and 40$, a bull case of $70 and a bear case of $0.10.

With the used cars market being highly fragmented and prone to disruption, it's no surprise that new entrants claiming all kinds of innovations would have gained a lot of attention and funding. Every year, about 40 million used cars are sold across the US, for an estimated value of $1 trillion . Of this huge market, 50% of transactions are private and most of the rest is done through dealerships. For the moment, the online sales account for barely 2% of the market. As also Carvana mentions in their annual report, the market is very fragmented, with a large number of independent car dealers with mostly offline presence.

The Harsh Reality

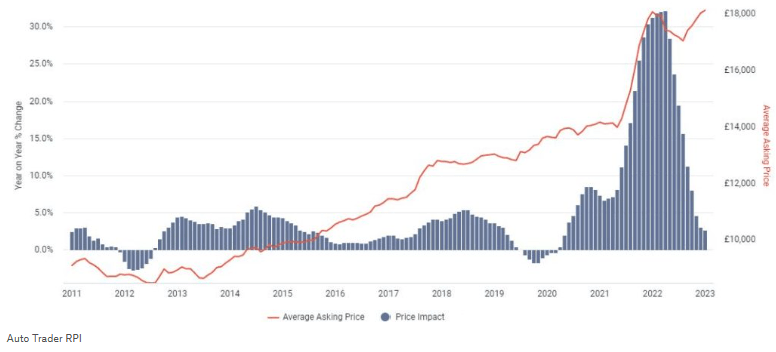

If everything is so good, why is Carvana struggling so much? Although its IPO was only in 2017, the company has been operating since 2012 and has yet to turn a profit. If we consider Carvana as another tech unicorn this could even be fine for many investors. However, I don't believe that Carvana's business can return the crazy economy-of-scale dynamics as some internet-based start-ups do. In fact, the more the company grows the more inventory, auto inspectors, "vending machines" etc. it will need - capping their potential profitability. Therefore, I don't see this as a business that will be able to gain any considerable moat in the future. Carvana wasn't able to turn a profit or even have a positive free cash flow at the peak of the covid restrictions when the hype around their business was at its highest. Even during the past 3 years when the price of used cars rose dramatically, Carvana still didn't achieve positive earnings.

Used Car Average Asking Price and Price Impact (MotorFinanceOnline)

{kind=link}

Corporate Governance

I try to invest only in companies in which I feel trust towards the executives and founders. In this article the author, Joseph Widley, describes in great detail the history of Carvana and that of its founders, uncovering some details that would probably make me stay away from such an investment event if it was the most profitable in out there. I'll summarize the main points I find relevant in Widley's article and also add some other information I gathered from other sources.

- Ernest Garcia II, major shareholder of Carvana who controls almost 84% of the voting rights, and father of one of the founders (Ernest Garcia III) pleaded guilty to a felony fraud charge in 1990 and spent three years on probation for arranging a complex real estate purchase. Although people can definitively make mistakes and are allowed to recover from them, for me this requires a more detailed assessment.

- A Delaware judge declined to dismiss a lawsuit from shareholders regarding the roughly $600 million sale of shares through a non-public direct offering to raise capital, after management allegedly assessed that Carvana didn't need further capital to survive the pandemic. According to the lawsuit proceedings, after the stock price had fallen from $110/share on February 21, 2020 to less than $30/share on March 20, Garcia III bought $25 million worth of stock at $45/share on March 30, 2020 through the direct non-public offering. After the short-swing trading period expired, the plaintiffs claim, Garcia II sold Carvana shares for a total of $478.4 million. The summary of the court proceedings (linked at the beginning of this bullet point and again here) continues to describe how the court has found that two of the six directors had deep personal and professional ties to a third director, Garcia III, which made their judgement not objective. It is important to note that the lawsuit is ongoing and that declining to dismiss doesn't entail guiltiness. However, for me this is a further point that makes me not weary about a possible investment.

- Carvana has a few car vending machines around the country and, as Widley points out, the states with the highest number of physical locations are those with higher-than-average delinquency rates for car loan payments. In these states, namely Texas and Florida, consumers also tend to have high reliance on car loans to make their purchases. This could be seen in two opposite ways depending on one's interpretation. On one side, Carvana might be trying to push easy-to-obtain auto loans that it will later securitize and sell to investors, disregarding the ability of its clients to pay back the loan. On the other side, Carvana is being strategic in its location placement by placing its vending machines where there is a higher chance of consumers making a purchase.

Corporate governance dynamics are open to interpretation and how much to care about them depends widely on individual investor preference. For my investment criteria, the trust I can have in management places a relatively significant role, but each person can make their own judgment.

The Accounting Side

If the corporate governance wasn't enough to make me reluctant, reading through the annual report I came across some accounting practices which in some cases I find odd. In particular, I'll go through the way the company sells its loans to take them off their books and their methods to calculate gross profits .

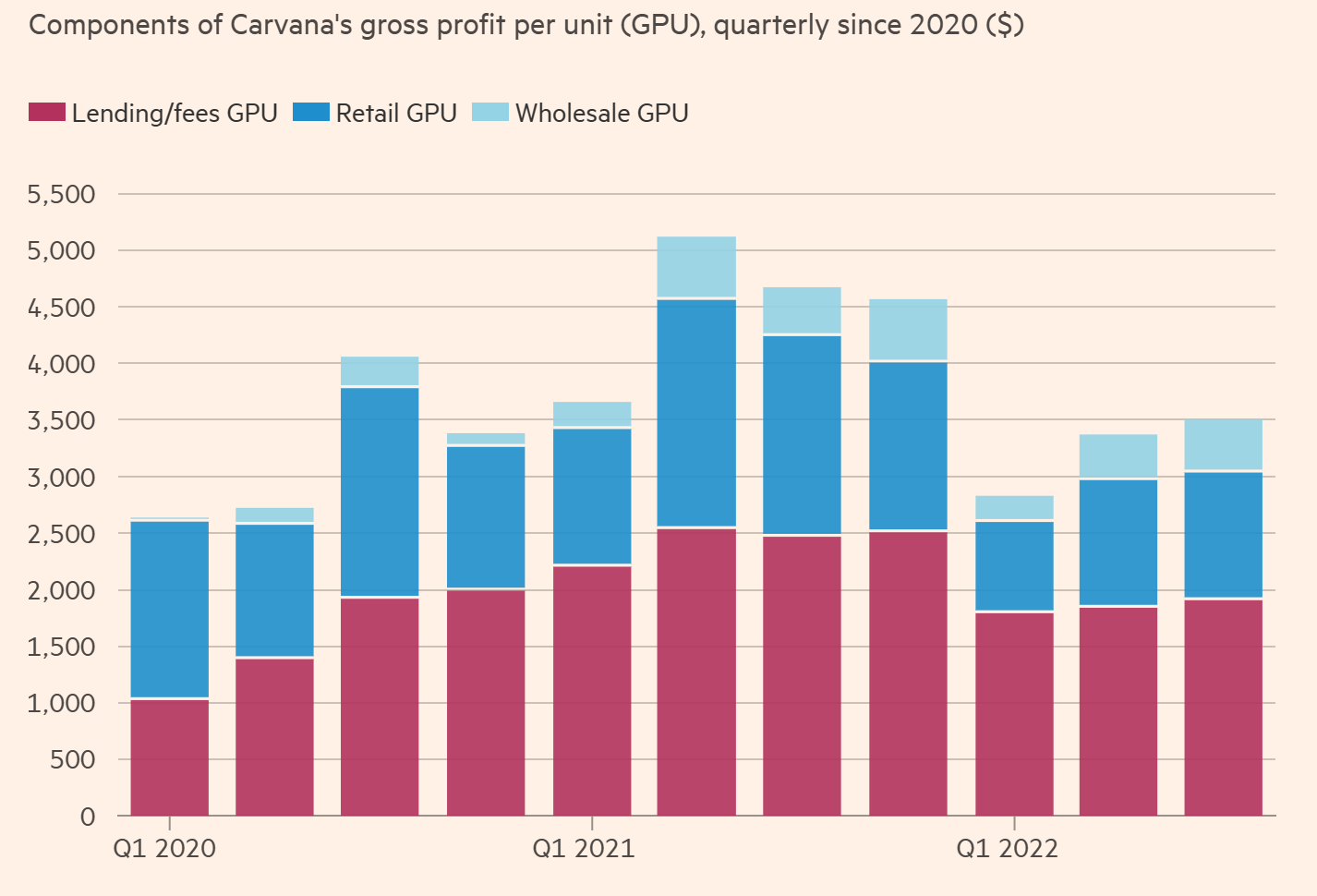

The financing revenue

In my opinion, Carvana is more of a financing company that uses used car sales to promote its business and get borrowers in the door. Looking at the graph below we can see that for the past two year at least half of Carvana's gross profits came from the financing side. Standalone, this fact is nothing surprising and arguably relatively common in the auto sale industry, both new and used. However, Carvana doesn't keep the loans but rather securitizes them and sells them to investors.

{kind=link}

In this 2021 article , Robert Freedman points out some key points that might be troublesome for this strategy, especially now with rising interest rates. While this strategy allows the company to immediately account for the revenues and gross profits, much needed as one of their few financial selling points, it also forces them to give up future profits and higher lifetime revenues. The author also points out how this strategy will make earning more volatile as they would be even more correlated to the interest rates.

Furthermore, I believe that with a possible recession in the making and higher interest rates investors might be less likely to buy this packaged loans. With consumer prices rising together with interest rates, risk of consumers not making payments might rise and therefore make investors more selective on how much they are willing to pay for these securities.

Furthermore, this model is sustainable only as long as investors are willing to pay a premium for the company's securitized loans. Finally, this adds an additional level of volatility to the company's earnings since they depend a lot from the financing side, which in turn depends a lot on interest rates and economic activity.

Gross profit growth?

Gross Profit per Unit Calculation (Carvana Annual Report 2022)

{kind=link}

According to the extract above from Carvana's 2022 Annual Report, the company uses some particular accounting rules to calculate the gross profit per unit. In fact, it uses the total gross profit for a given period divided the retail units sold. To be clearer: the gross profit generated from retail sales plus wholesale plus financing activities plus commissions plus gross profit from other ancillary products is divided by only the retail units . This seems a quite odd way of accounting for gross profit per unit, which makes me question the overall reliability of other metrics presented by the company.

Final struggles

All of what I've written above started to lose a bit of meaning when I read that Carvana is also struggling to raise more cash to support its very unprofitable business . To give a further idea of how much the company is struggling its 10.25% bond due 2030 is trading at 53 cents on the dollar.

Carvana is attempting to restructure its $9 billion debt and if the company manages to find willing investors, would reduce the bond debt by 1.3$ billion and it annual cash interest payments by about $100 million. However, it is still to be seen if there is any interest buyer. The alternative could be to raise cash through equity, which would also not be ideal given the historically low prices.

Risks in my rating

While I don't see any future for Carvana, the company might still be able to convince investors and debtholders that it has a promising future, if only they trust it a bit more. If an investor were to buy some stock now at these very low prices, the downside would be limited while the upside potentially very positive. The car retailer might be able to restructure the debt, and make the necessary changes to make the company a profitable business. I personally wouldn't assign much likelihood to such an event.

Conclusion

Sometimes stocks are unfairly punished by the market and this unlocks precious opportunities for value investors, other times the companies in questions are just not good investments. I believe that Carvana is the latter and that investors should avoid any involvement. In addition to what I talk about in this article, there is plenty of information more specific to the valuation itself about the company that only strengthens my argument. Historically, environments with higher interest rates tend to "clean" the market from unsustainable businesses as cash starts to get more expensive, I think that Carvana's time has come. The only thing we can do is avoid catching the falling knife.

For further details see:

Carvana: Catching A Falling Knife Might Get You Cut