CVNA - Carvana Continued Its Bear-Busting Journey

2023-06-08 22:16:30 ET

Summary

- Carvana's stock has seen an overall increase of 170% since our initial coverage on May 1, 2023.

- CVNA stock surged due to improved profitability.

- Concerns about Carvana's profitability are addressed by focusing on operating metrics rather than financials, as the company is still in the early stages of growth.

- Our DCF model values Carvana at $51 per share, making it a strong buy recommendation.

Recap

Carvana Co. (CVNA) made an exciting announcement about its updated outlook. The news sent the stock soaring, with a premarket surge of 28% and an overall increase of 170% since our coverage of the company in "Carvana: 2023 Barbarians At The Gate" on May 1. This remarkable growth prompted our readers to ask some important questions and led us to reevaluate our target price for CVNA stock.

Why did the stock go up so much? What is our target price?

Many wondered why the stock had experienced such a significant surge. Used car prices are still high, well above the levels seen during the pandemic.

{kind=link}

Some people initially thought that high prices and expensive loans would discourage consumers from buying used cars, which could have negatively impacted Carvana's performance. However, there was a crucial aspect that many overlooked—the fact that Carvana operates as a dealership rather than a manufacturer.

Dealerships rely on the discrepancy between the purchase and sale prices of cars to generate profits. Although price levels can impact the number of cars sold, liquidity plays a crucial role in determining success.

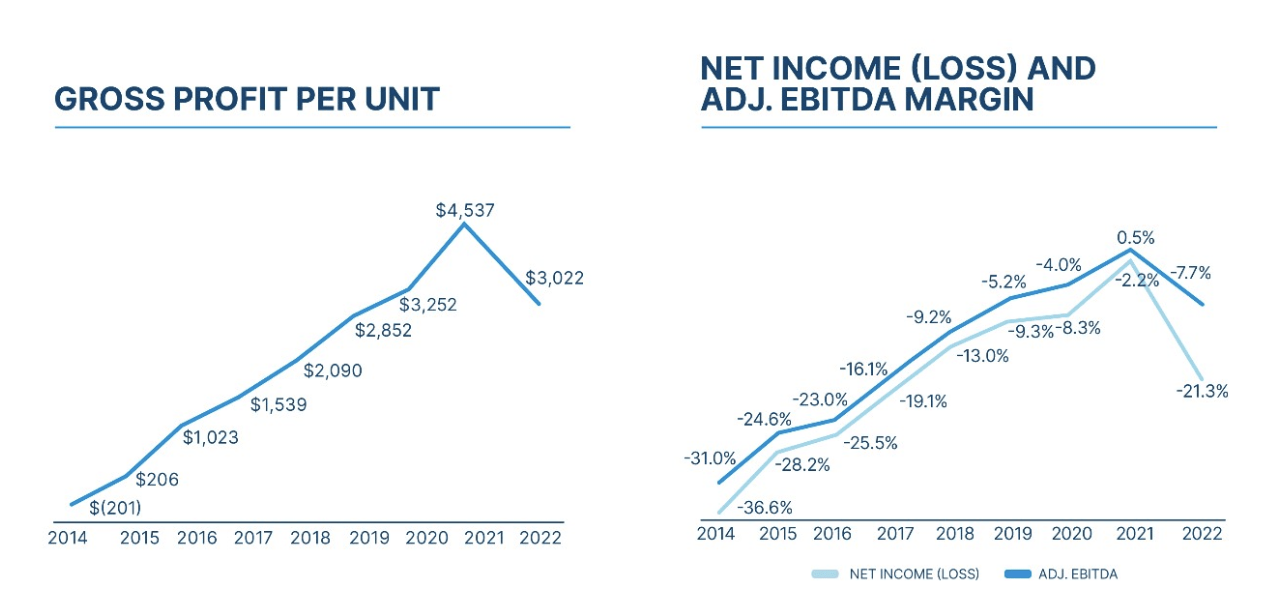

In a previous article, " The Power Of ADESA: How Carvana's Acquisition Is Game-Changing ," we explored how Carvana's acquisition of the second-largest car auction, ADESA, could significantly improve their profitability. This strategic move has opened up new avenues for Carvana to streamline their operations and enhance their financial performance. Carvana recently achieved a historic milestone by reaching a gross profit of $6,000 per unit. This showcases their proficiency in enhancing profits by effectively managing inventory and the robustness of their online marketplace platform.

In addition, we believe that along with improved profitability in the wholesale sector, the profitability of its loans can contribute significantly to its GPU. In Q1 2023, Carvana experienced a 12.5% increase in other gross profit per unit, primarily driven by loan profits, reaching $2,032. This figure is significantly higher than its retail and wholesale gross profits per unit of $1,388 and $883, respectively. When compared to CarMax Inc. (NYSE: KMX ), it becomes evident that Carvana's business model differs greatly. CarMax's financing income constitutes only 1/5 of its gross profits, whereas Carvana relies much more on loans for profitability than vehicle sales. This difference stems from Carvana's pure online presence, which creates a cost advantage in variable costs. We previously discussed this disparity in our 2019 article titled "Carvana's Secret Auto Loan And Low Variable Cost Business Model" .

While we had previously employed a DCF model in the 2019 article, we will update below based on management's updated outlook.

Carvana will never be profitable since it couldn't generate profits at its prime in 2021

There have been concerns that Carvana will never achieve profitability, as it failed to generate profits during the prime time of the used car market in 2021. We often use the term "building castles in the air" to describe this investment mindset, which can sometimes be misleading when conclusions are drawn based on flawed assumptions. One key question to consider is whether 2021 was truly the optimal time for Carvana's success or if there is a more opportune period.

In this regard, we draw inspiration from Elon Musk's concept of "First Principles Thinking." This problem-solving methodology involves breaking down complex problems into fundamental truths or principles and building solutions from those foundational elements.

When analyzing investments, it is essential for investors to evaluate companies through fundamental analysis. In the case of Carvana, investors should consider how many cars the company needs to sell to break even before making a judgment call based on its financials.

Over the past few years, Carvana has consistently improved its operating leverage.

GPU and margin (CVNA)

{kind=link}

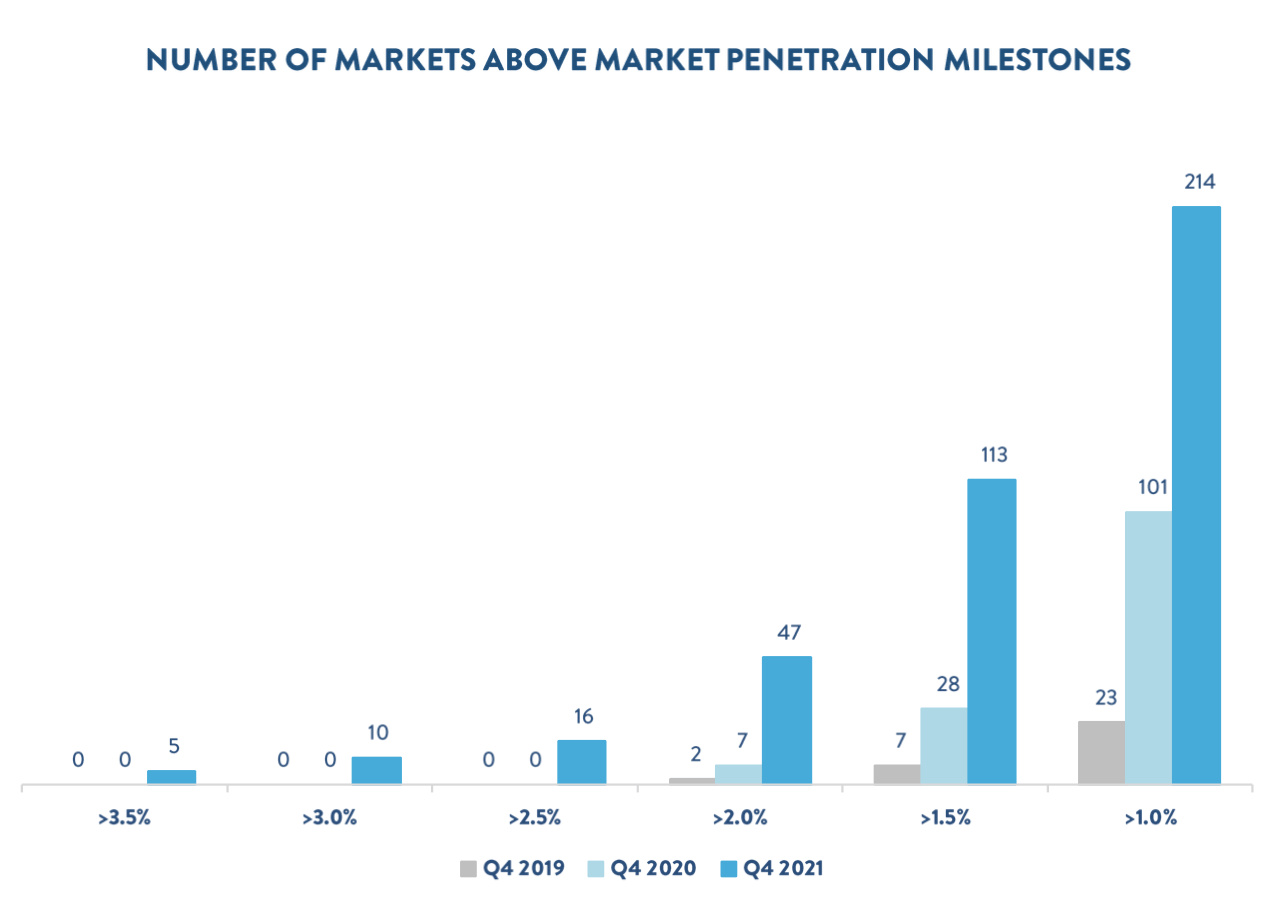

However, as of 2021, the company only held a 1% market share in the U.S., expanding state by state and gradually improving profitability within each state. Cohort data provided by the company, cited from our original analysis, showed a reduction in advertising expenses from $3,749 per unit in newer cohorts to as low as $440 per unit in older cohorts. This suggests that the older and newer cohorts exhibit distinct profitability profiles and that Carvana is still in the early stages of its growth, with 2021 marking just the beginning.

Advertising expense by cohort (CVNA)

Notably, the company demonstrated improved penetration consistently before the Federal Reserve began raising interest rates in 2022. Its 2013-2020 cohorts experienced a 52% growth in retail units sold, with its oldest cohort in Atlanta achieving a 51% increase and reaching a market penetration of 3.53%, a new record for the company.

Market penetration (CVNA)

{kind=link}

For a company that showcases significant growth potential, we always advise investors to exercise caution when making buy or sell recommendations solely based on financials. At this stage, the company's elevated expenses do not provide significant insights about the company.

So, what should investors focus on? We believe operating metrics hold greater importance than financials. Operating metrics provide insights into the company's customer metrics and offer a deeper understanding of its operations. Financials, on the other hand, evaluate the company's operating performance. It's akin to wanting your children to focus on improving their learning methods or approaches rather than solely focusing on their results. Results (financials) become more crucial for growth companies at matured stage or for mature companies.

Carvana's Outlook and Valuation

Carvana recently provided an updated outlook that showcased their optimistic expectations.

- Carvana expects to achieve an adjusted EBITDA of over $50 million in the Q2 of 2023.

- Non-GAAP total GPU of above $6,000.

- Carvana has sold or securitized approximately $2 billion in loans quarter-to-date.

- Carvana's CEO, Ernie Garcia, expressed confidence in the company's strategy, stating that their focus on profitability has led to savings, efficiencies, and faster-than-expected progress.

These positive developments in EBITDA and GPU are not surprising to us. In our previous article, we noticed early signs of an improved GPU based on the earnings reports of Carvana's peers, CarMax and AutoNation (AN). AutoNation specifically mentioned the potential tailwind in the used car industry due to supply constraints caused by the COVID-19 situation in 2020.

We also looked at the unsold financing receivable on the balance sheet, which, in our opinion, is only a matter of timing and will result in a significant increase in cash flow once resolved.

The CEO's emphasis on profitability aligns with our own perspective on the company, as we also believe that focusing on profitability rather than solely chasing growth is essential for long-term success at this stage.

Regarding our valuation approach, we find it appropriate to utilize a DCF model based on the management's projections. The improvements in Carvana's financials and operating metrics have enhanced management's credibility and provided investors with greater confidence.

We used the following assumptions.

- TAM 40 million used car unit sale

- Market share:1%->5% in 10 years (CAGR 16%)

- WACC: 12%

- Free cash flow margin: ->4% in 10 years

- Terminal growth rate: 3%

- Net debt:7969 million (Q1 2023 data)

- Shares outstanding: 106 million (Q1 2023 data)

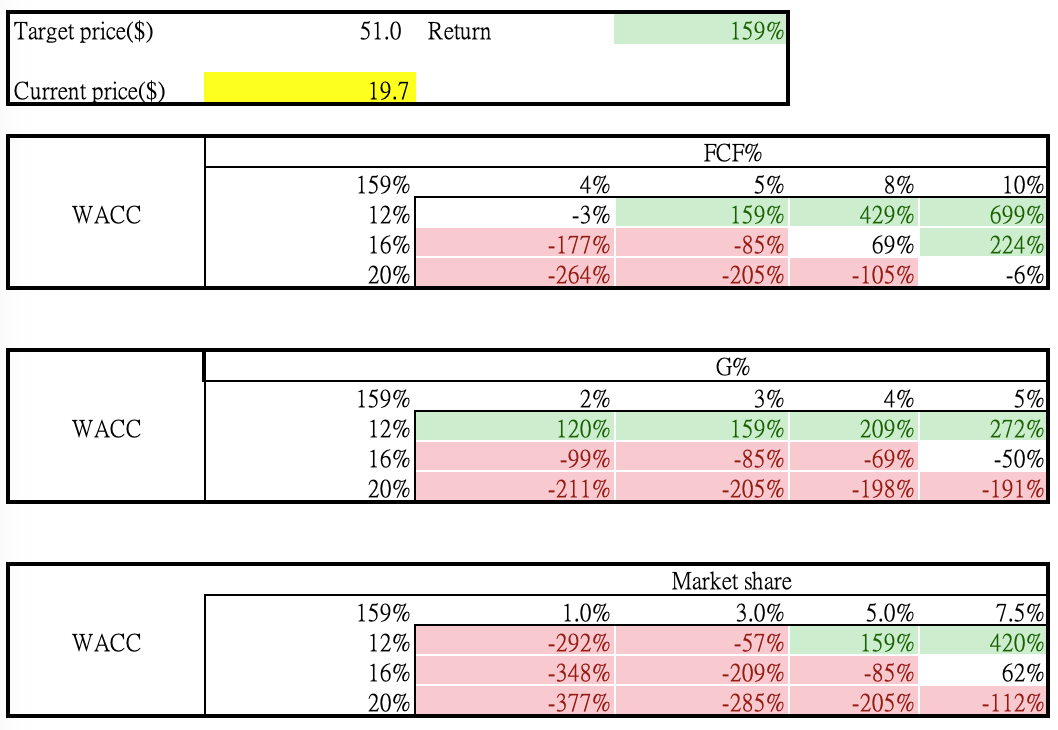

Through the DCF model, we arrived at a $5.4 billion equity value ($51 per share), which is ~159% above the current price.

Based on the sensitivity test below, the stock is likely overvalued if the company fails to improve its free cash flow margin to above 4%, its WACC increases above 15%, or its long-term market share is below 3%.

Sensitivity analysis (LEL Investment)

{kind=link}

However, it's important to note that our model does not include revenue or profit projections from Carvana's wholesale business, despite the significant improvements in revenue growth and profits since the acquisition of ADESA. As a result, our model may be slightly conservative.

Conclusion

We believe it is still early in the game for Carvana, but we caution that this stock may not be suitable for everyone. If you are seeking stable income, Carvana should definitely be considered for your portfolio. Considering the improved risk-reward profile and the stock's positive trajectory in GPU, we anticipate a potential repricing of the stock in the near future. Therefore, we rate CVNA stock as a "strong buy."

For further details see:

Carvana Continued Its Bear-Busting Journey