CVNA - Carvana: Don't Be Fooled By The Recent Profit Forecast

2023-06-20 12:08:43 ET

Summary

- Carvana's stock price surged by over 50% after a press release and presentation at the William Blair Annual Growth Stock Conference, but the forecasted 20% boost in gross profit is likely a one-time event due to a timing issue in loan sales.

- Despite impressive growth, Carvana has never been profitable, accumulating total losses of over $2.2 billion and carrying a debt of over $8 billion with negative shareholder's equity.

- The company's debt trades at prices well below nominal value, indicating a risk of bankruptcy, and it is unlikely that Carvana can generate enough cash to redeem $500 million of bonds due in 2025.

On the morning of June 8 th , before the market opened, Carvana ( CVNA ) issued a press release and an 8-K form summarising a presentation that they would be giving later that day at the William Blair Annual Growth Stock Conference.

The market reacted by driving the stock price up by more than 50% , options volumes were up 400% with calls trading twice as many options as puts.

The press release and presentation materials were positive for the company, but the forecast 20% boost in gross profit is likely a one-time event resulting from a timing issue in the sale of loans. It is unlikely to be repeatable.

Carvana came onto the scene in 2014, disrupting the used car industry by introducing online buying and selling. Their trademark “innovation” is a multi-story vending machine for used cars, allowing a buyer to pick up a car at his/her own convenience without even meeting a salesman. It is really a marketing gimmick, it would be simpler and much less expensive to have the cars at ground level and put the keys in a lockbox.

Between 2014 and 2022 the company grew at a 170% rate to become one of the largest used car dealers in the USA. However, the growth came at a price. Profitability was nowhere to be seen. The company was generating growth but losing money on every sale. During its eight-year existence, Carvana has never had a profitable year and has accumulated total losses of over $2.2 billion dollars.

Cash flow has always been negative, but Carvana was able to cover its losses and fund its growth by issuing debt and raising capital on the stock market. That is not a sustainable business.

This is the key slide from Carvana’s presentation.

{kind=link}

Let’s take a closer look:

The first line item, “retail units- no change from the initial outlook”. The initial outlook was an expected sequential decline in units sold compared to Q1, which itself was a 25% decline from Q1, 2022.

We can get an estimate of the decline by looking at the forecast adjusted EBITDA. In Q1,2023, that number was -$24 million, the forecast for Q2 is positive $50 million, an improvement of $74 million.

The forecast gross profit per unit goes to “above $6,000”, compared to $4,750 for Q1. S.G &A is forecast to be similar to Q1, so the improvement in gross profit should flow into EBITDA, all other things being equal.

$74 million improvement in EBITDA and a $1,250 per unit improvement in GPU (non-GAAP) equates to sales of about 75,000 retail units, a decline of 5% from Q1 and 36% from Q2 of 2022.

However, it was not the decline in units sold that grabbed the headlines , it was the 20% increase in forecast GPU.

Carvana includes in its GPU calculation, profits from three sources:

- Retail profits

- Wholesale profits

- Other profits - including sales of GAP insurance, commissions from insurance sales, and gains on the sale of loans. Most of the profits in this category are gains on the sale of loans.

Carvana’s standard practice is to lump all those profits together and divide the sum by the number of retail units sold, to arrive at the gross profit per unit.

Moving excess inventory to wholesalers and selling loans to finance companies is a fundamental part of the retail business, so Carvana argues that those profits are legitimately included in retail profit per unit.

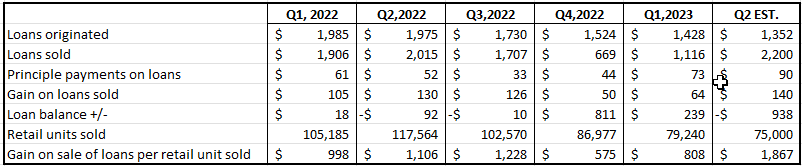

However, there is a timing issue. The loans are not necessarily sold in the quarter in which they are originated. A loan for a car that is sold in Q1 for example, may be sold to a finance company in Q2 or later. This did not affect Carvana’s GPU to any degree until Q4 of last year because the value of loans originated in any period did not differ very much from the value of loans sold. But in the latter half of 2022, Carvana was not able to sell enough loans to cover the loans that originated during the quarter, it was left carrying those loans on its books at the end of Q4 and it also sold fewer loans than it originated in Q1.

According to the 8-k form and the presentation, Carvana has sold most of those outstanding loans this quarter. The table below shows the origination and sale of loans for the past 5 quarters and an estimate for Q2:

Summary of loans originated and sold (From Carvana's financial statements)

{kind=link}

The gains on those loans will be booked as profit in Q2, though the sales originated in Q4,2022 and Q1,2023. The 20% improvement in gross profit per unit is not a fundamental improvement in the business, it is a one-time boost resulting from the timing of loan sales.

The $50+ million adjusted EBITDA also includes the one-time boost from the catch-up sale of loans, otherwise, EBITDA would remain negative. Even with the one-time boost, adding back the adjustments (share-based compensation $15 million), depreciation ($93 million) and interest ($156 million), leaves Carvana with a net loss exceeding $200 million for the quarter.

Despite the rosy picture outlined in Carvana’s latest press release, the facts remain:

- Carvana has never made money in its eight-year existence.

- The business is shrinking, not growing.

- The business does not generate enough cash to pay the interest on the massive debt incurred during its growth phase.

- Total debt exceeds $8 billion, and shareholder’s equity is negative.

- Carvana’s debt trades at prices well below nominal value. For example, the 2028 notes trade at around 50 cents on the dollar and the 2030 bonds have a 36% yield, indicating that bondholders see a risk of bankruptcy.

- $500 million of bonds come due in 2025, and it is unlikely that Carvana’s ongoing business can generate enough cash to redeem those bonds.

Given the company’s precarious debt position and its lack of cash flow, I fail to understand the appeal of buying or holding CVNA at the price at which it has been recently trading.

For further details see:

Carvana: Don't Be Fooled By The Recent Profit Forecast