CVNA - Carvana: Kicking The Can Down The Road

2023-12-09 23:54:22 ET

Summary

- Carvana has reduced its inventory and entered into a debt exchange agreement to lower its debt and interest expenses.

- After 2 years of PIK interest, the company could find itself in a similar situation in a few years, trying to stave off bankruptcy.

- Carvana will need to prove it can increase cash flow and grow at the same time.

In March , I wrote that bankruptcy was still a very real possibility for Carvana ( CVNA ). The stock has skyrocketed since then, so let’s check in on the name and its most recent earnings that were reported last month .

Company Profile

As a quick refresher, CVNA is an online used car dealer through which consumers can buy, sell, or trade-in used cars. Buyers typically have cars they buy cars delivered to them, although they also can pick them up from one of CVNA’s car vending machines. Customers can also sell or trade-in their vehicles online by just answering a few questions and CVNA will pick up the vehicle. CVNA has a network of inspection and reconditioning centers that it uses to bring vehicles up to its standards before re-selling.

Q3 Results

When looking at CVNA, one of the first things to look at is its balance sheet. The company ended Q3 with $5.9 billion in debt and $544 million in cash and equivalents. The company has significantly reduced its inventory over the past year, taking it from $2.57 billion a year ago to $1.08 billion. A year ago, it had $7.4 billion in debt and $316 million in cash and equivalents.

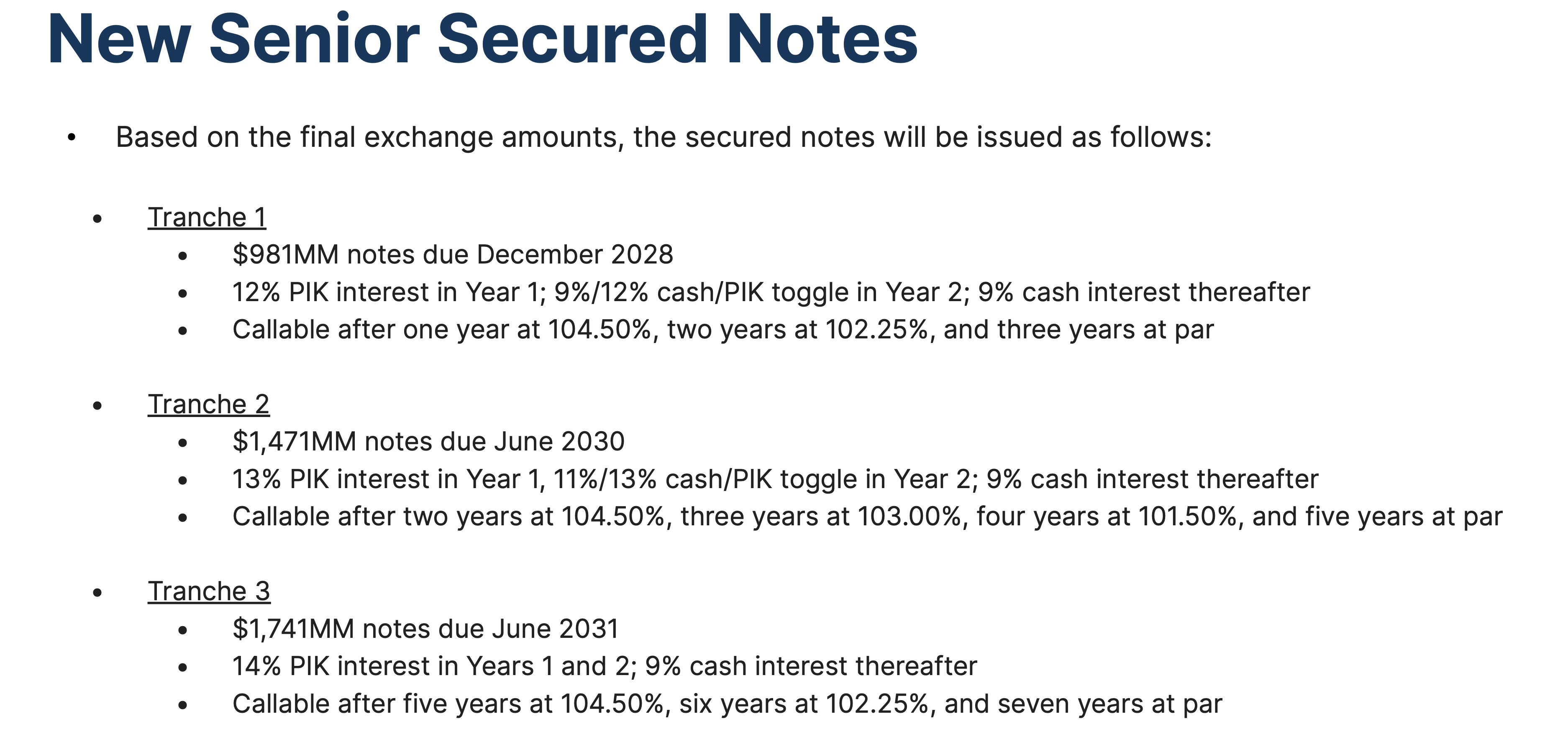

In September, the company entered into a debt exchange agreement, exchanging $5.52 billion in senior unsecured notes due between 2025-2030 for new senior secured notes due between 2028-2031. The exchange lowered its total principal by -$1.33 billion to $4.19 billion.

The new notes with have PIK interest (pay in kind) in the first year and potentially in year two for two of the three tranches, and then all three will have cash interest in year three and thereafter. They are secured by substantially all of Carvana and ADESA's assets. After the deal, the CVNA also had $205 million of senior unsecured notes remaining as well.

{kind=link}

CVNA generated $599 million in operating cash flow in Q3 and $1.04 billion through the first nine months of the year. FCF year to date is $1.03 billion. Much of this has come from the inventory reduction the company has seen.

Looking at CVNA’s Q3 operational results, revenue declined -18% to $2.77 billion. Retail units sold, meanwhile, fell -21% to 80,987 units.

Total gross profit per unit ((GPU)) was $5,952, an increase of 70%. Adjusted GPU was $6,396, up 65%. Gross profit rose 34% to $482 million.

Retail GPU jumped from $1,131 a year ago to $2,692. Wholesale GPU climbed to $618 from $448, while wholesale market GPU rose from $127 to $271. Other GPU - which includes financing, extended warranties, gap insurance, etc. – was $2,642 versus $1,921 a year ago. It saw a $400 benefit from selling and holding a higher-than-normalized volume of loans. Over 16% of its other revenue and gross profit come from related parties.

CVNA said it has reduced transport and reconditioning costs by $900 per unit over the 12 months, and by $600 per unit over the last two quarters. It said it has also made $400 per unit in operating efficiency gains the past two quarters as well.

On its Q3 earnings call , CFO Mark Jenkins said:

“So I think we start focusing on reconditioning. In-sourcing was probably the single biggest driver. So basically taking services that had previously been provided by third parties in the inspection and reconditioning centers and taking them in-house and doing them ourselves. And that obviously saves costs and allow us to have better control of the process. So I think that's been a big win. In addition, I think we've gotten better at standardizing processes, making sure we're properly normalized at our staffing levels. We made some big gains in proprietary inspection and reconditioning center software, including fully in-sourcing our inventory management system. ... We've also made gains automating parts procurement. It used to be a highly manual process. and more variable process than it is today. And so I think we've made big wins there in the proprietary software development department. So those are a few of the places where we've made real gains in reconditioning. I would note that we do see opportunities for further gains in those areas that I just pointed to in recon. We don't think we're done. We do see opportunities for further gains in reconditioning cost per unit. Moving to inbound transport. I think a couple of sources of gains there are getting better at logistics network utilization as well as having lower inbound miles. And so both of those things, I think, have also led to declines in inbound transport costs.”

Adjusted EBITDA came in at $148 million versus -$186 million a year ago. The number included a benefit of $40 million from selling and holding a higher-than-normalized volume of loans.

Looking ahead, the company is looking for a sequential decline in retail units sold. It is expecting positive adjusted EBITDA in Q4, as well as adjusted GPU to be above $5,000.

It said for 2024, it is looking to drive significant total GPU and adjusted EBITDA.

The quarter itself in isolation was good for CVNA, as it greatly improved its GPU, generated strong free cash flow, and was EBITDA positive. However, the company has had to ditch growth to do this, with revenue and units sold down considerably.

Meanwhile, the debt exchange will lower its debt and buys it some time not having to pay interest. However, the PIK feature will only add to its principal and eventually lead back to some pretty high debt payments while encumbering all its assets. With its inventory at some pretty lean levels, the company also likely won't see the same type of cash flow it has seen this year in 2024.

Valuation And Bankruptcy Risk

Based on 2023 EBITDA projections of $344.9 million, CVNA trades at a 26x multiple. Based on 2024 EBITDA estimates of $392.2 million and 2025 EBITDA of $599.7 million it trades at 23x and 15x multiples, respectively. The EV has not been adjusted for the debt exchange.

CVNA is expected to see revenue fall -19.5% this year, before growing 5.7% next year and 15.4% in 2025.

Now that CVNA has significantly reduced its inventory and is PIKing its debt the next two years, eliminating most of its interest expense, the company should generate cash similar to its EBITDA. However, if it PIKs it debt the next two years, it will be back to having $5.4 billion in long-term debt and nearly $500 million in interest expense in 2026. If the company can get to 2026 consensus estimates of $800 million in EBITDA, it would have about 6-7x leverage. At the same time it would be generating about $300 million in operating cash flow with $5.4 billion in debt, with its creditors now owning bonds secured by all its assets and it essentially being unable to issue more secured bonds due to covenants. That's a less than ideal situation and would see the company once again facing questions regarding bankruptcy.

Conclusion

CVNA has been able to kick the can down the road for the next few years, but how it gets into a situation to do much more than service its debt in a few years is very much still in doubt. The company has the next two years to grow and become more consistently free cash flow positive, or it will end up back in the same situation it was earlier. Thus far, the company has only really shown that it can grow or be cash flow positive, but not meaningfully both at the same time. To accelerate growth it would likely need to increase inventory, which would cut into cash.

At the end of the day, CVNA likely will end up either bankrupt in several years or will be a zombie company that exists mostly to pay off its debts. Either way there does not appear to be much left on the bone for equity holders down the line. As such, the stock remains a “Sell,” with bankruptcy a possibility over the next 3-5 years. In between then, though, expect a stock that makes some pretty large moves both to the upside and downside.

For further details see:

Carvana: Kicking The Can Down The Road