CVNA - Carvana: Like Duct Tape On A Fuse

2023-07-20 09:11:40 ET

Summary

- Carvana shares rose by 40.2% on July 19th after it announced better-than-expected Q2 2023 results and a significant debt restructuring initiative. However, its future remains uncertain due to high debt levels and weak profitability.

- Carvana's restructuring initiative will reduce overall debt by roughly $1.2 billion and reduce interest expense in the near term. However, its debt will remain high and interest expense will increase after 2 years.

- Despite a decline in revenue, Carvana exceeded analysts' expectations in Q2 2023 due to cost cutting, but this may not be enough for long-term stability.

It's incredibly rare for shares of a company to shoot up double digits in the course of a single day. Such moves are practically always reserved for big news items that have a meaningful and long-lasting impact on the firm in question and its investors. Such an occurrence happened on July 19th, when shares of Carvana ( CVNA ) skyrocketed, closing up 40.2%. In addition to announcing financial results that exceeded expectations for the second quarter of the company's 2023 fiscal year, management also announced a rather significant restructuring initiative that will meaningfully reduce interest expense in the near term and will temporarily reduce overall debt. Both of these developments are incredibly positive. But unfortunately for investors, they don't necessarily translate into the company becoming a good investment prospect. Given how pricey the stock is and how uncertain its future still looks, I believe that a more bearish stance would be appropriate from this point on.

A short story

I would like to tell you a little story. When I was about 12 years old, I had a family member who was dating a car mechanic. This family member had an issue with her car and it got to the point where the car wouldn't run. Her boyfriend at the time thought he could save her some money by looking at it himself. Given that he was a professional car mechanic, my family felt as though this was a wise decision. Sure enough, he got the car running. But it was only a day or two before it broke down again.

This time, she took it to a repair shop. And apparently, he had, for whatever reason, placed duct tape around a fuse to keep the car running. That’s not how you fix a car. In some ways, the story I'm going to tell you about Carvana parallels that. Right now, there's something broken about the company. There are certain improvements being made, but the big development that sent shares soaring higher is, I believe, akin to placing that duct tape on the fuse that my family member experienced so many years ago.

Tackling the big news first

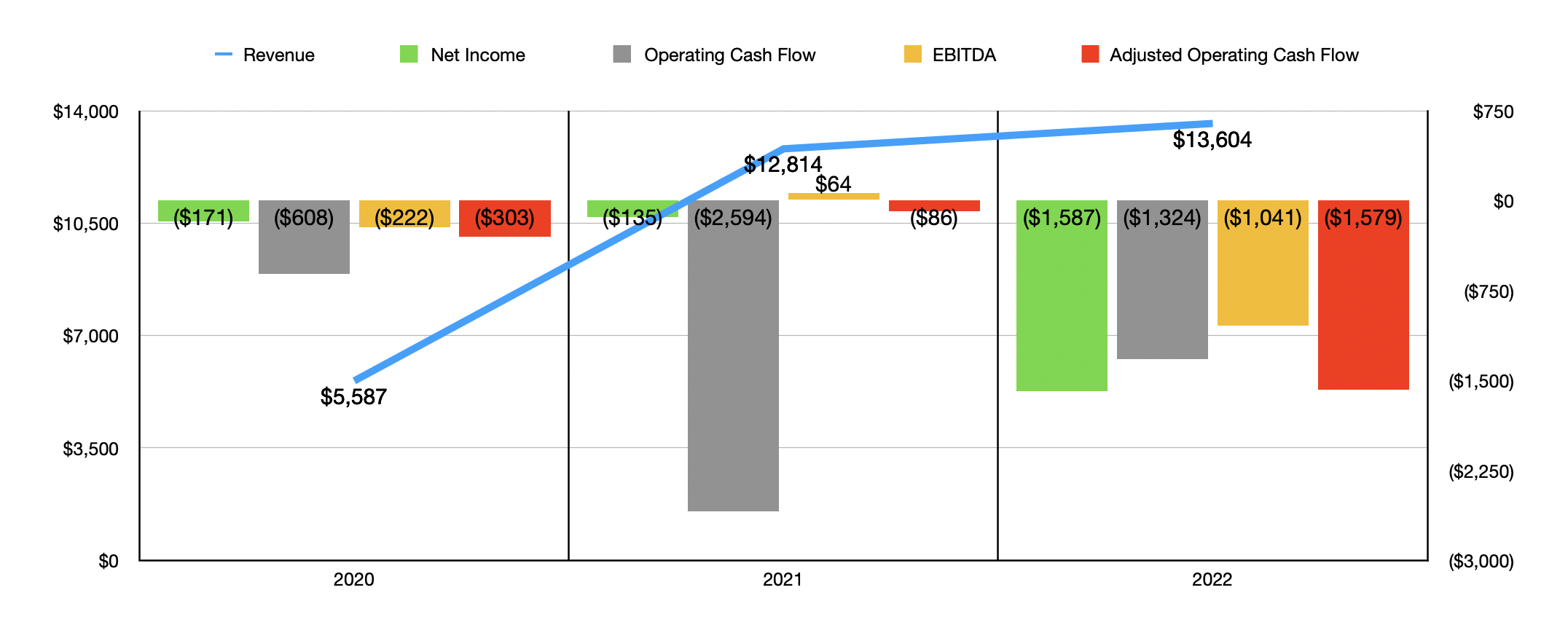

In writing this article, I debated on whether to focus on the earnings picture first or on the really big news item centered around debt. At the end of the day, I opted for the latter so as to not leave you in a state of suspense. But before I get there, it would be helpful to discuss briefly exactly what Carvana is and what it does. For those who don't know the company, it operates as an ecommerce platform that enables individuals and organizations to buy and sell used cars. The company has truly grown over the past few years . In 2020, for instance, revenue totaled only $5.59 billion. By 2022, sales had expanded to $13.60 billion.

{kind=link}

Obviously, some of this growth can be attributed to organic expansion. But a good part of it can also be chalked up to acquisition activities. In May of 2022, for instance, the company acquired the physical auction business of ADESA U.S. Auction, LLC from KAR Auction Services, now known as OPENLANE ( KAR ). In a deal valued at $2.2 billion. That purchase included 56 auction sites and 6.5 million square feet of real estate spread across over 4,000 acres of land.

Pretty much no matter how you stack it, Carvana is a sizable player in the automotive retail space. Since it's launched in 2013 and through the end of last year, the company transacted around 1.4 million vehicles through its websites, generating combined revenue of $39.3 billion. It has grown to operate on a truly national scale, with its in-house distribution network accessible to over 81% of the population of the US.

This all sounds very exciting, but the company has some problems. Even though revenue has grown nicely, bottom line results have always been problematic. In the past three completed fiscal years, the company generated cumulative net losses of $1.89 billion. The largest chunk of this, about $1.59 billion in all, occurred in 2022. Cash flow data has been even more challenging. Operating cash flow over the past three years was negative in the amount of $4.53 billion, while adjusted operating cash flow was negative by $1.97 billion. Even EBITDA, which is a metric that is quite easy to manipulate, has struggled to common positive. In two of the past three years, it ended up negative, with the reading in 2022 totaling negative $1.04 billion.

Another issue for the company relates to the tremendous amount of debt on the firm's books. In order to grow, especially by means of acquisition, the firm has had to take on large amounts of financing. Net debt as of the end of the second quarter of 2023 came in at $7.23 billion. You can imagine what kind of impact this would have on the company. Obviously, most of its debt is fixed. But some of it is variable, so rising interest rates are painful for it. In 2022 alone, the business paid out $486 million in interest.

{kind=link}

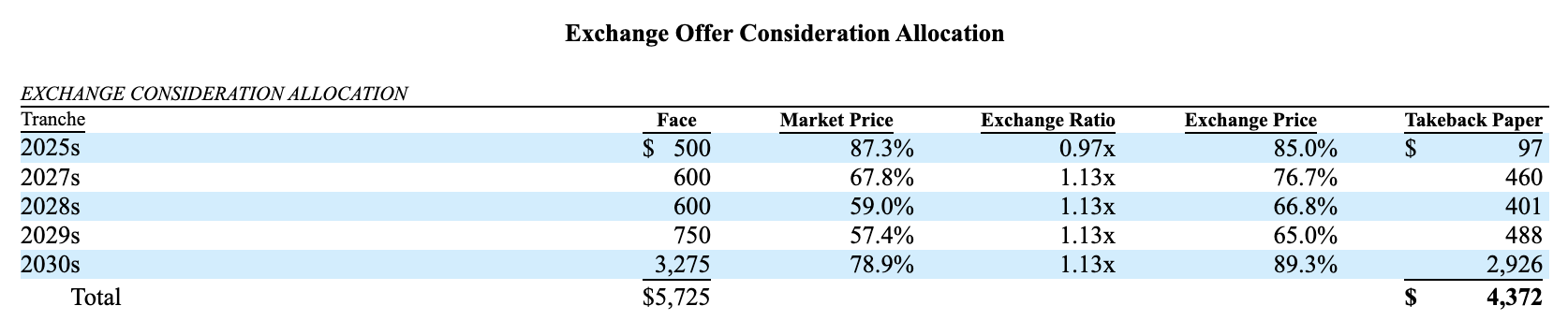

It's this debt picture and the profit issues that led the company to try to find a solution for its ills. On July 19th, management announced that the firm reached a restructuring agreement with its creditors whereby it would swap out some of its existing debt for some other debt that has longer dated maturities and in a way that will reduce overall debt by roughly $1.2 billion. The specifics of the exchange can be seen in the table above and the table below. The short version is that the company intends to conduct a tender offer for some of the debt that it has coming due in 2025. That debt will ultimately be paid down in part with $320 million of cash. Even though the company has cash and cash equivalents, including restricted cash, of $677 million on its books, the cash used for this will likely come from a $350 million equity raise that is part of the restructuring initiative.

{kind=link}

In addition to extending out the maturity of over 83% of its unsecured note debts to 2028 and beyond, Carvana has agreed to some interesting terms. The first tranche of debt that the company is issuing will be in the amount of $1 billion. During the first year, the debt will pay interest in a manner that's referred to as PIK, or paid-in-kind. What this means is that, instead of paying out cash, it will issue additional debt that it will have to pay interest on in the future. The rate for this debt will be 12% per annum. During the second year, the company can either continue with the 12% PIK rate or it can toggle this and pay 9% in cash. Starting in the third year, it has no choice. At that point, it must pay in cash at 9% per annum for the duration of the existence of the debt.

The second tranche, $1.5 billion in all, carries the same kind of terms. Instead of being senior secured and due in 2028, however, it will be senior secured but second lien and will be due in 2030. For the first two years, the company must pay interest at a rate of 13% PIK, with 11% per annum in the form of cash as an option in the second year alone. From year three and on, the firm must pay 9% per annum in cash. And lastly, the third tranche covers $1.876 billion. This debt will come due in 2031 and will require the company to pay 14% per annum PIK for the first two years, after which the firm will have to pay 9% per annum until the debt matures.

Let's start with the good news on this. In addition to pushing out the maturity of the debt that the company has, this maneuver will allow the company to significantly reduce how much interest it is paying in the near-term. For the next two years, management is forecasting a total reduction in interest expense of $430 million. Unfortunately, that's where the good news ends. If the company does pay all of the interest expense optional and required as PIK debt, the amount of additional debt that it would take on because of the PIK nature of it well actually, according to my estimates, render the $1.2 billion of debt reduction meaningless. This is because additional debt of about $1.23 billion will ultimately accrue from these payments. On top of this, annual interest expense paid in the form of cash after the two-year window ends will be about $36 million higher than what it would be under the existing arrangement.

So in the near term, this strategy gives the company some breathing room. But two years out from now, its debt should be about as large as it is now and interest expense would be even higher each year. The deal is better than nothing. But it's not something that is going to save the company on its own. It is important to note that there is another development on this front. On the same day, management also announced an ATM (At-the-Market) offering program whereby it can, from time to time, issue up to $1 billion worth of additional stock or 35 million shares, whichever applies first. Using the 35 million share scenario, and ignoring the $350 million worth of stock the company is going to be issuing, this would imply dilution for shareholders of 24.8%.

Great earnings results

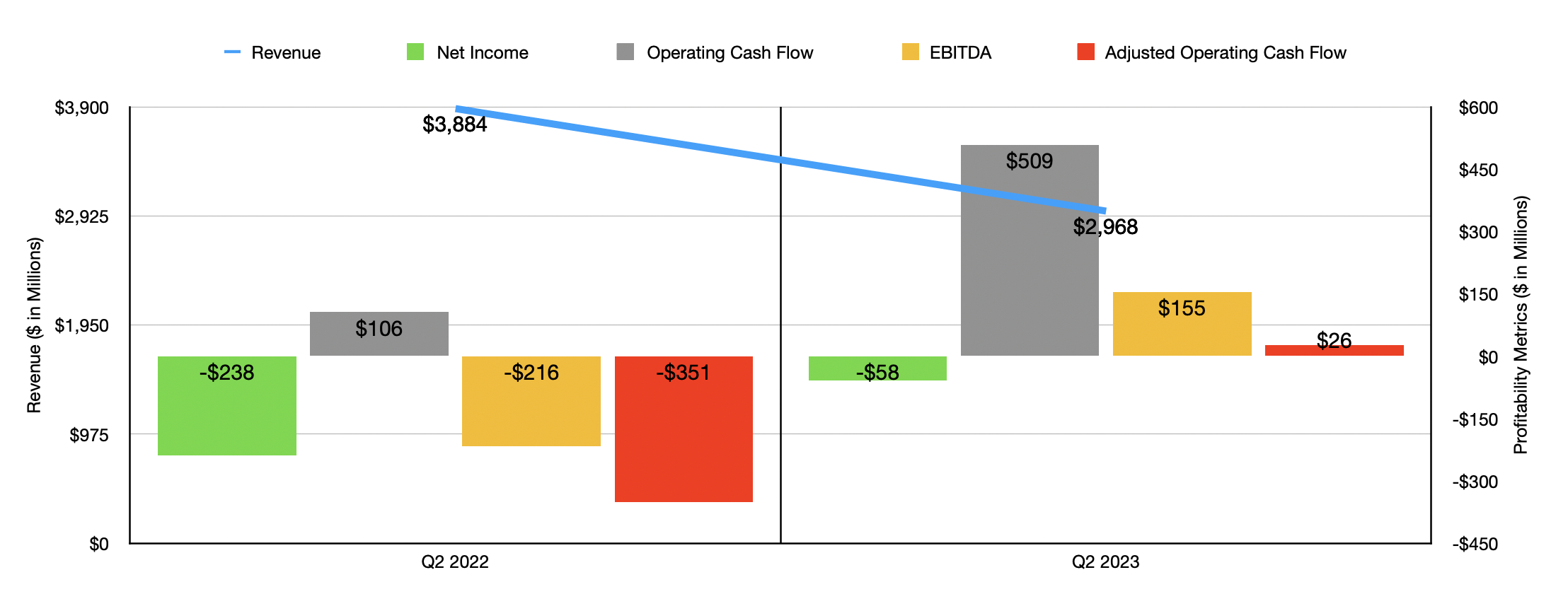

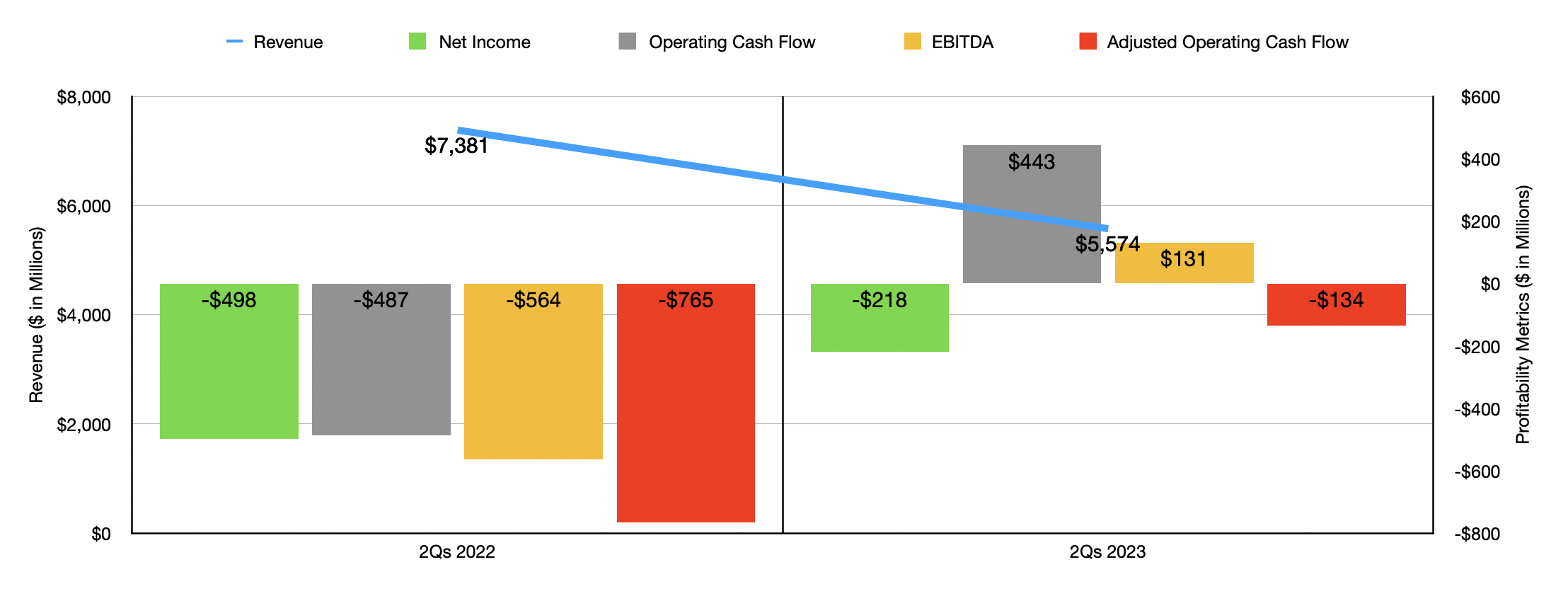

In addition to this significant development, management also announced some interesting results for the second quarter of the company's 2023 fiscal year. As analysts expected, revenue for the business tanked, falling from $3.88 billion in the second quarter of 2022 to $2.97 billion the same time this year. Even though this looks painful, investors saw the news as bullish because revenue actually exceeded analysts’ expectations by an impressive $360 million. The drop in revenue for the company was driven by a meaningful decline in the number of vehicles sold. Retail units sold dropped from 117,564 to 76,530. That drop, management said, Largely because of broader economic factors like continued high interest rates and inflationary pressures that make buying such a pricey asset prohibitive. Management also decided to focus their efforts more on becoming profitable and less on growth, leading to lower advertising levels and a reduction in inventory.

{kind=link}

The company also saw a decline in the number of wholesale vehicle units from 55,299 to 46,453. The same economic and business factors that I mentioned when it came to retail units applied here as well. However, unlike with the retail side of the equation, which saw the average price per unit climb only 1.7%, the wholesale side reported an increase in revenue per unit of 10.7%. What was really impressive for the company during this time was the profitability per vehicle sold. The most significant improvement came from retail vehicles sold. Because of lower acquisition, reconditioning, and inbound transportation costs, the company saw an increase in retail vehicle gross profit per unit of $1,535 year-over-year. Overall gross profit per unit totaled $6,520 during the quarter compared to the $3,368 reported one year earlier. However, it's important to note that about $900 per unit of this was in the form of one-time items that should not occur in the future.

Even more significant for the company during this time was a reduction in selling, general, and administrative costs. This category of expenses fell from $721 million to $452 million. According to management, the improvement the company saw on this front was largely attributable to cost cutting initiatives the company implemented last year. These initiatives involved reducing employee head count, integrating acquired real estate from the aforementioned acquisition, reducing the company's corporate footprint, and making changes to advertising spending, amongst other things. Management also said that some of the decline was driven by a reduction in the number of retail units sold. And that makes a lot of sense as well.

{kind=link}

To these bottom line improvements, the company went from generating a net loss per share of $2.35 in the second quarter of 2022 to generating a net loss of $0.55. That translates to an improvement in the company's bottom line from a loss of $238 million to a more modest loss of $58 million. For context, analysts were expecting the company to post a loss of $1.01 per share for the quarter. Other profitability metrics also followed suit. Operating cash flow skyrocketed from $106 million to $509 million. If we adjust for changes in working capital, it went from negative $351 million to $26 million. And finally, EBITDA went from negative $216 million to $155 million.

When it comes to the future, there's a lot of uncertainty. However, management has provided some guidance when it comes to the third quarter. They currently anticipate non-GAAP gross profit per unit of $5,000 or more. This would actually represent a decline most likely compared to the $7,030 reported for the second quarter. But even with this weakness, management believes that EBITDA will be positive and that the firm will be put on a more solid track toward achieving positive free cash flow.

Takeaway

When it comes to just the quarterly results provided by management, Carvana did a solid job. I would even say that it was perhaps exceptional. Even though revenue fell, management exceeded expectations. Cost cutting initiatives are coming through. You might be surprised, then, that I have taken such a bearish stance on the company. Frankly, while I appreciate the breathing room that its debt restructuring has afforded it, all that does is kick the can down the road. Overall debt remains incredibly high and even at the company can achieve positive EBITDA on an annual basis, there is no strong evidence that the company is going to be able to generate enough positive cash flow in the next year or two to justify the $10.55 billion market cap of the company and the $16.17 billion enterprise value. So even though the company is making some amazing improvements, I think that the stock looks very expensive and investors would likely be wise to look elsewhere for opportunities, especially at a time when sales in the automotive retail space are weakening.

For further details see:

Carvana: Like Duct Tape On A Fuse