CVNA - Carvana: Mini 2021 All Over Again

2023-12-06 03:07:13 ET

Summary

- Carvana stock has surged 660% YTD but chasing the stock is risky for average investors.

- Industry challenges, including high used car prices and competition from stronger players like Amazon, pose risks.

- Carvana's mounting debt, dilution of shares, and technical setup indicate potential problems for the company.

Carvana Co. ( CVNA ) stock is up a mind-boggling 660% YTD, primarily on the back of better than expected Q2 earnings and constant fears/hope of a short-squeeze. The short-squeeze argument does have some merits as nearly 38% of the float has been shorted according to Seeking Alpha data. But, chasing the stock here is likely to end up harming the average investor (or trader). I am presenting 5 reasons here to sway the average investor or trader from this stock. Let us get into the details.

{kind=link}

Industry Challenges

While Carvana recently reported a slight headline beat in its Q3, the reported net income of $49 million loses its shine when you factor in the interest expense (covered below). In addition, while used car prices have fallen a bit recently, they are still trading quite close to their peak than their trough. Used cars are still trading at 30% higher than their historical normal and I am not getting a rosy picture in my mind about Carvana's operations when prices do return to normal.

{kind=link}

Let's not forget competitive threats from existing or new, stronger players. For example, I believe Amazon.com ( AMZN ) is a threat for anyone and everyone with their distribution system and general ecosystem strength. Hence, it was not surprising when news broke out that Amazon had partnered with Hyundai Motor Company ( OTCPK:HYMTF ) to sell cars online.

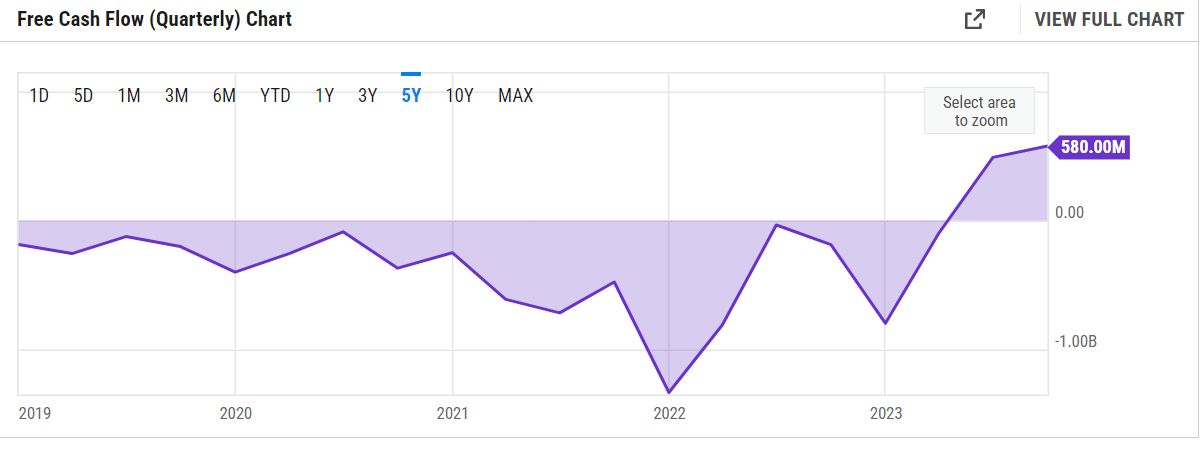

Free (of) Cash Flow

It may surprise you to hear now in hindsight that Carvana was not Free Cash Flow [FCF] positive even at the height of stock optimism in 2021. Sure, I get that they offer loans and hence FCF may not be a good metric here like it is not for Banks but Carvana's operating income is not a picture of consistency either with only the last two quarters showing positive operating income. And let's not forget that operating income excludes taxes and interest expense and adding those to the equation make things worse for Carvana. But let's forget about taxes and focus just on interest expense on debt below.

{kind=link}

{kind=link}

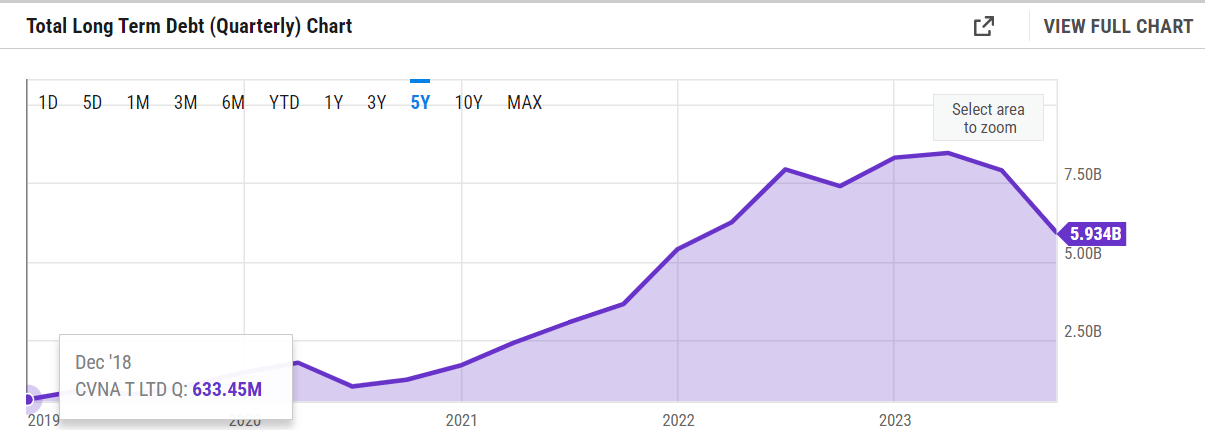

Mounting Debt

Carvana's long-term debt has grown nearly 10 folds in the last five years, reaching nearly $6 billion at the end of the most recent quarter. Clearly, this is not a recipe for success in the current high-interest rate environment as the company is consistently shelling out more than $150 million/quarter towards interest expense on debt. This number (interest expense on debt) has grown five folds since March 2021.

Another way to understand the enormity of the debt situation is by looking at the company's market capitalization. With a market cap of $7 billion, Carvana carries a debt load that is 85% as big as its overall worth.

{kind=link}

{kind=link}

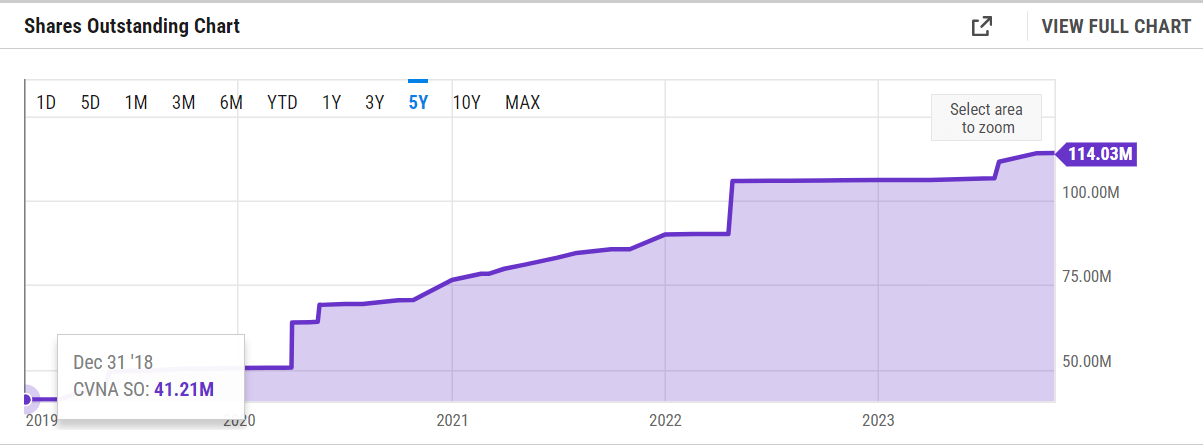

Diluting Away

When companies run into difficulties generating cash on their own and are already leveraged enough, the next logical avenue is the market or new investors. Carvana's total shares outstanding has almost tripled in the last 5 years, reaching a high of 114 million shares at the end of the most recent quarter. I expect further dilution as the company is likely to struggle given the macro and fundamental challenges explained above.

{kind=link}

Technical Setup

The recent strength shown by the stock has pushed its Relative Strength Index [RSI] close to the overbought level of 70. Interestingly, despite that, the stock is trading about 10% below its 100-Day moving average. I am more intrigued by the fact that the 200-Day moving average is more than 20% below the current market price and that suggests the stock has ways to fall before getting long term support should it fail to clear the 100-Day average.

CVNA Moving Avgs (barchart.com) CVNA RSI (barchart.com)

Conclusion

One of my favorite adages about the market goes something like " The market can stay irrational longer than one can stay solvent ". Buying Carvana here in the hope of a short-squeeze is madness. Shorting the stock based on fundamentals may actually be insanity. The prudent thing to do is to stay away if you have no position and to sell if you hold it. Sure, you may be down quite a bit if you got caught up in the 2021 buying frenzy but at least you are 6 folds better now than at the beginning of the year. I firmly believe this company is unlikely to exist in its current form five years from now. Dealing with such stocks is not investing and not even trading. It is speculating. Do not speculate.

For further details see:

Carvana: Mini 2021 All Over Again