CVNA - Carvana: Risk Factors Remain

2024-01-14 08:27:03 ET

Summary

- Carvana shares are experiencing a sharp resurgence, aided by increased risk-taking attitude in the markets and anticipation of rate cuts.

- Investors are focused on Carvana's ability to increase unit sales and achieve economies of scale to boost profitability.

- Softening used-car sales and potential price competition may eat into Carvana's recent momentum and profitability.

- It's best to retreat to the sidelines until the company can prove a return to its growth trajectory.

After briefly dipping into penalty box territory last year, shares of Carvana Co. ( CVNA ) are experiencing a sharp resurgence - no doubt also helped by the increased risk-taking attitude in the markets as investors look forward to a multitude of rate cuts this year.

So far in 2024, shares of Carvana have slipped nearly 20% and given up a portion of December's rally - but the stock has multiplied by ~6x over the trailing twelve months. Needless to say, this has been a very volatile trade - the question now for investors is, does Carvana still have room to shine further in 2024?

All eyes on Carvana are focused on two factors: one, the company's ability to increase unit sales in a difficult macro environment (the company still claims it has 99% of its addressable market left to go), as well as its ability to achieve economies of scale and boost its profitability.

These watch list items form the core tenet of the company's three-step plan to recovery. As written in the company's recent Q3 shareholder letter , this plan is as follows:

1. Drive the business to positive Adjusted EBITDA.

2. Drive the business to significant Adjusted EBITDA per unit (also referred to as significant positive unit economics).

3. After completing Steps 1 and 2, return to growth."

I last wrote a neutral article on Carvana in October, when the stock was trading closer to $27 per share. Since then, the stock has nearly doubled on a confluence of both stronger-than-expected progress toward financial targets in Q3, plus the general enthusiasm for tech and risk stocks in the last quarter of 2023. In light of all the new information on Carvana plus its higher share price, I still remain neutral on this name, as I view the stock to be a relatively balanced bag of positives and negatives.

Let's go through the reasons next.

Encouraging signals: GPU is on the rise, driven both by pricing plus operational improvements

For investors who are newer to Carvana, one of its most closely-watched metrics is GPU or gross profit per unit - a measure of how much Carvana is making from each car sale. We'll footnote here that many investors have issues with this metric, as Carvana includes profits from selling its book of car loans in this figure, and so the actual gross profit per vehicle may be lower than suggested - but we'll counter that profits on financing deals are a common monetization strategy all the way from local dealers to the large auto manufacturers, so I think it's valid to count this as part of Carvana's profit base.

{kind=link}

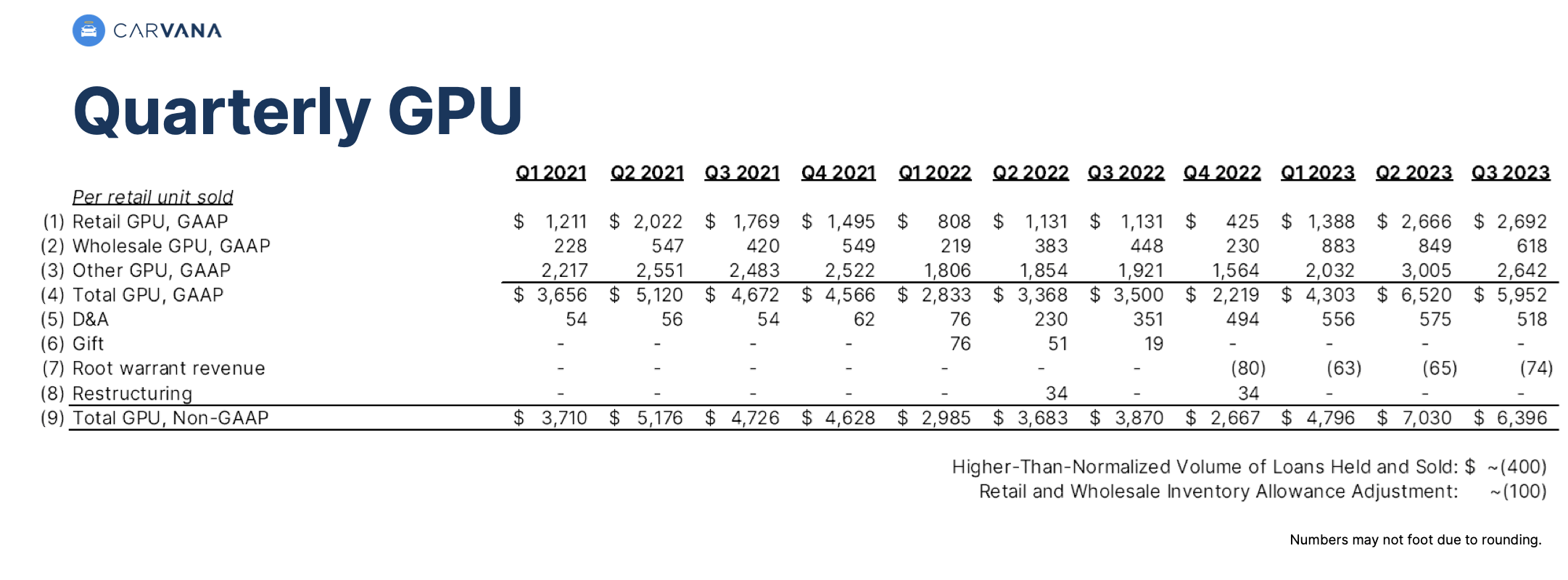

GPU has been trending sharply upward ever since the pandemic. Q3 pro forma GPU of $6,396 was up 74% y/y . Now, the company noted that there was roughly $500 of one-time benefit in this figure, both from a favorable inventory adjustment plus a timing shift of loan sales that disproportionately benefited Q3 this year and disadvantaged Q3 last year. Even adjusting for this, GPU would have been up 61% y/y.

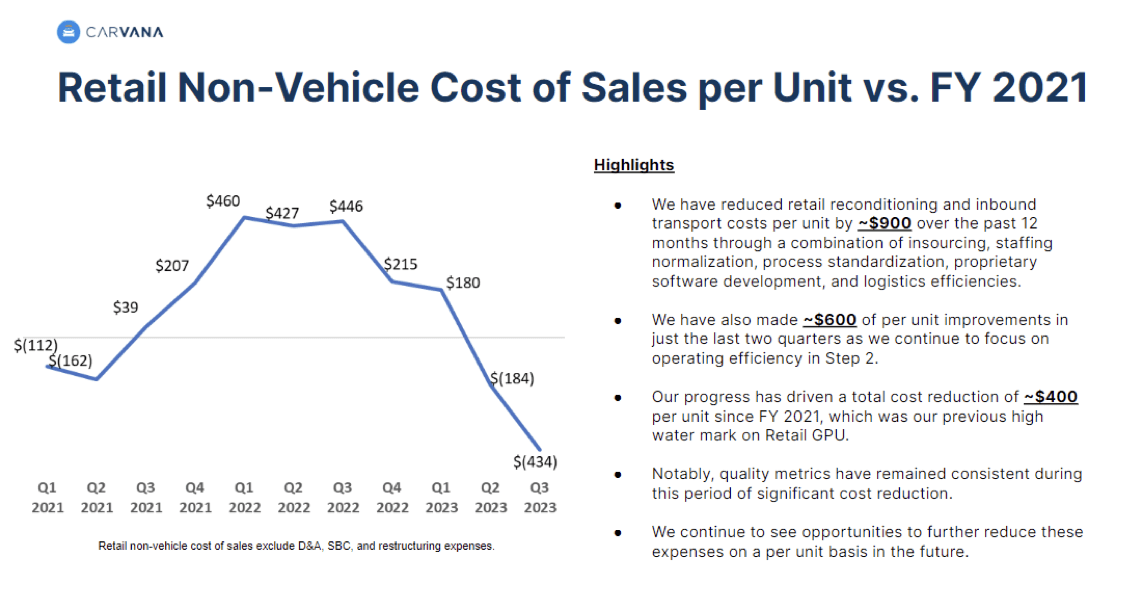

Higher pricing for used cars - which surged ever since the pandemic created supply chain bottlenecks - has helped Carvana increase its spread on sales. On top of this, the company has made a number of operational improvements detailed in the slide below. Namely, the company has improved both reconditioning and transportation costs - both heavy lifts in the company's sales operations procedure - which has led to a $434/unit improvement in costs since 2021.

{kind=link}

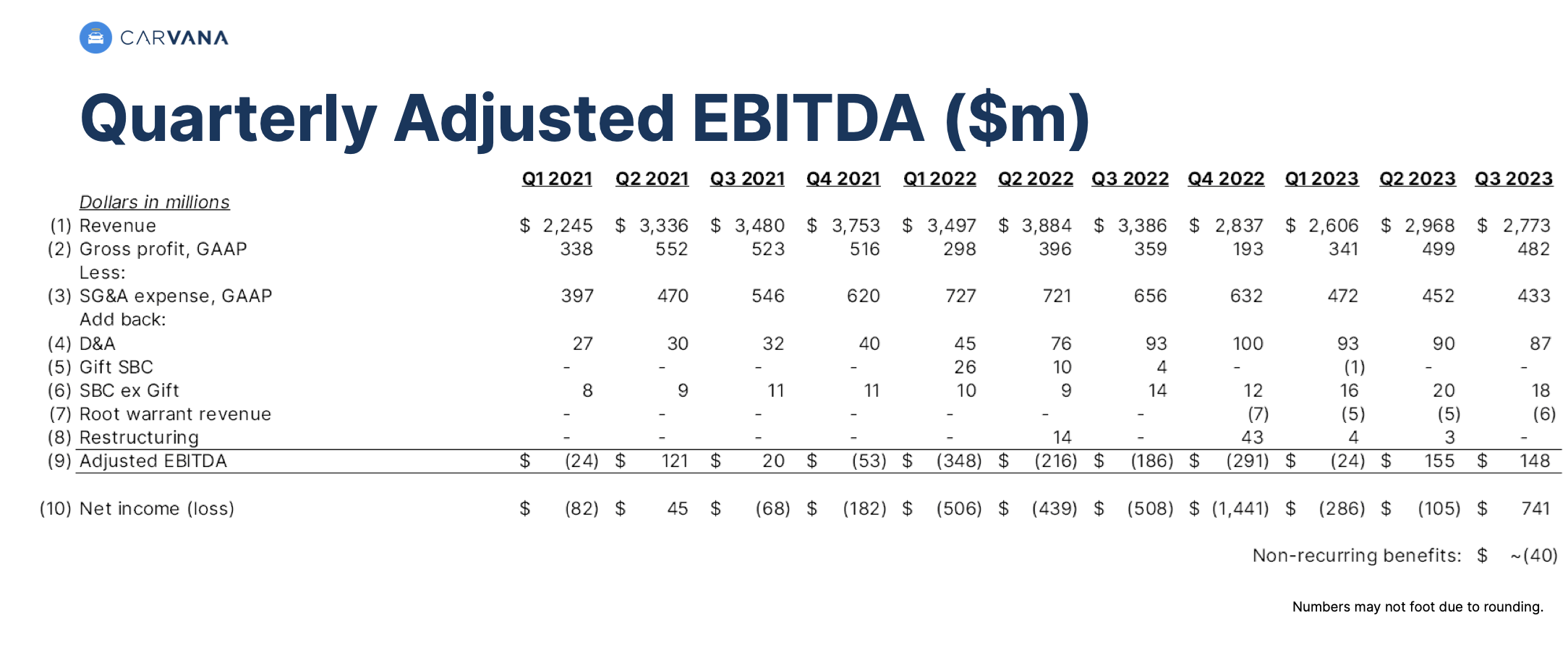

This increased operating leverage, meanwhile, has helped Carvana achieve positive adjusted EBITDA for each of the past two quarters - recall that pre-pandemic, investors blasted Carvana for its sharp losses in spite of huge growth rates:

{kind=link}

But can the company grow again?

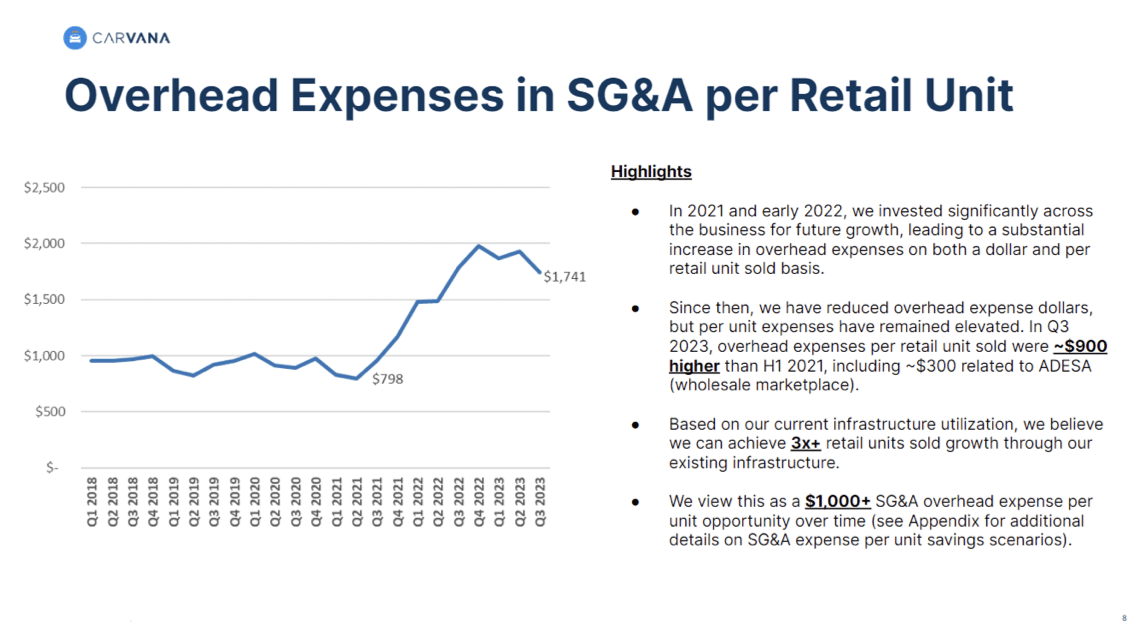

This being said, nobody can argue with the fact that Carvana is a business that relies on economies of scale. During the pandemic demand boost, Carvana invested dramatically into operations and particularly vehicle reconditioning capacity to support a much higher level of sales.

As shown in the chart below, the company believes it can support 3x its retail unit volume with its current installed infrastructure. The unfortunate news here is that Carvana has excess operational capacity which is increasing its per-unit overhead and overall profitability.

{kind=link}

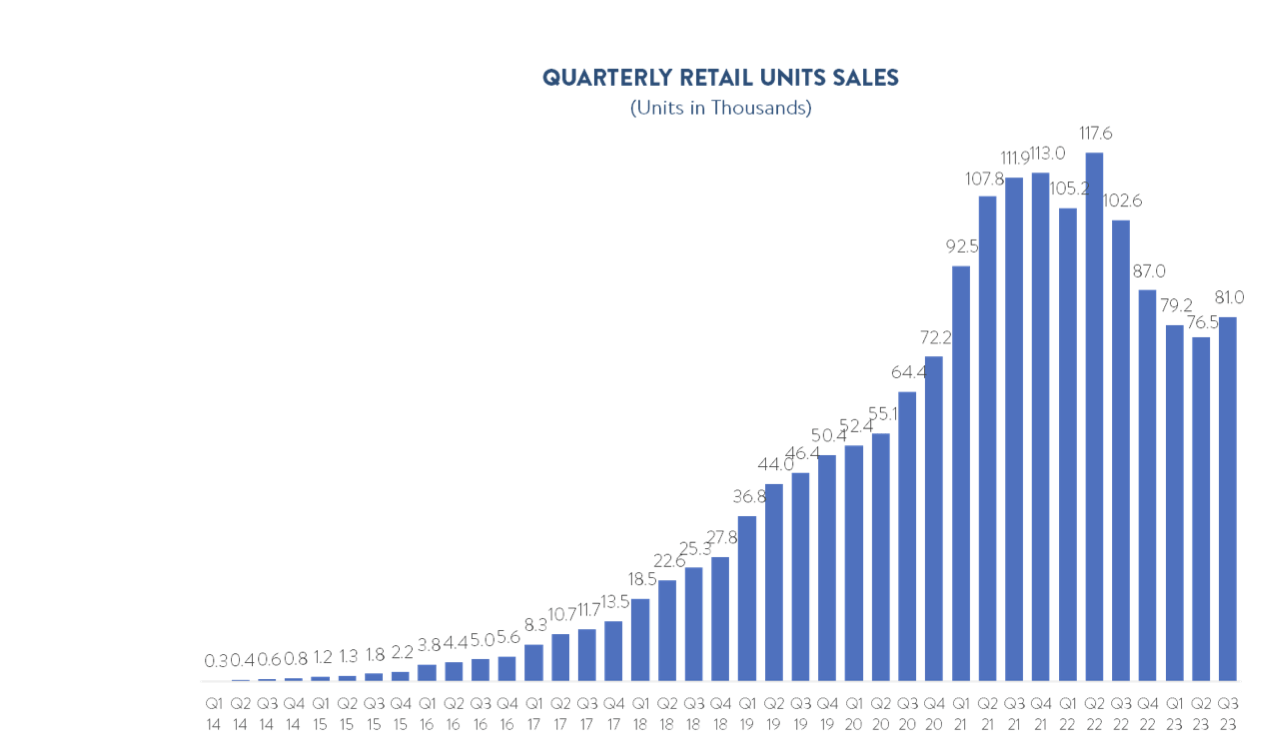

Making matters worse: Carvana planned for higher capacity at a time that sales were surging, not foreseeing the pull-forward of demand that is causing unit volumes to drop now. As shown in the chart below, retail unit volumes are struggling to keep up with pandemic-era levels:

{kind=link}

This is in spite of prices flattening. Kelley Blue Book recently reported that wholesale used vehicle prices fell -7% y/y in 2023 , which is leading to lower consumer sticker prices at dealer lots. I can envision a scenario in which Carvana will start competing on price to draw customers away from traditional dealers - which may threaten its recent GPU gains.

Management is also seeing industry softness and isn't holding its breath for a return to growth anytime soon. For the fourth quarter, CEO Ernie Garcia noted as follows on the Q3 earnings call :

In the fourth quarter, we expect to continue making fundamental gains through various projects that comprise Step 2. We also expect volumes to reduce relative to Q3 due to normal seasonality and potential industry softening observed over the last four weeks. Despite this, we continue to operate in our target unit range for Step 2. The sum of these dynamics leads us to expect to produce another great quarter, but as in past Q4s, we expect lower industry-wide volume, coupled with higher industry-wide depreciation rates to cause lower adjusted EBITDA than we have achieved in the past two quarters."

With a seemingly shrinking market, and consumers appearing to soften on car purchases, it's not difficult to see Carvana giving back some of its recent profit gains.

Key takeaways

The road ahead is still not clear for Carvana, and given the sharp surge in the stock over the past quarter, it's more than appropriate to exercise some caution here. I'd prefer to remain on the sidelines until we see more fundamental clarity.

For further details see:

Carvana: Risk Factors Remain