CVNA - Carvana's Financial Struggle: A Debt-Fueled Quagmire

2023-06-09 11:28:50 ET

Summary

- Carvana's shares are recovering after a compelling Q2 presentation, but the company still faces serious financial issues, including burning cash and approaching debt maturities.

- The company has a three-step plan to achieve positive adjusted EBITDA, improve operating margins, and return to growth, but profitability remains uncertain.

- Carvana operates in a $200 billion dealership market with potential for technological disruption, but its high debt and unprofitability make it a risky investment.

Following a compelling presentation of second-quarter results, Carvana's shares are recovering. The company assures investors that 2023 won't be as gloomy as 2022, and amid the general uptrend in the markets these weeks, this stock seems to be convincing shareholders again.

However, my forecast for CVNA remains extremely pessimistic, and the company's fundamentals continue to be the primary reason. The core business is burning cash, debt maturities are approaching, and refinancing efforts are not proving successful. Meanwhile, monetary policy continues to pose a problem for unprofitable companies, a category which Carvana will be a part of for at least the next five years.

Removing the enthusiasm for short-term news, Carvana remains a company that has prioritized growth in the past, now finding itself with serious capital and financial problems to manage.

Strategy and Outlook

Currently, the company defines its short-to-medium-term strategy in three steps:

- Achieving positive adjusted EBITDA, which management expects to reach already in Q2, 2023;

- Striving to achieve a positive operating margin for each car sold;

- Returning to focus on growth once the second objective is completed.

Even granting Carvana another 4–5 years, the company is almost certain not to become profitable, let alone generate positive Free Cash Flow ((FCF)). Thus, the two truly important metrics about the profitability of the business will almost certainly remain in negative territory.

The company is already in the process of lowering operating costs, having planned to finish 2023 with $1 billion less in SG&A expenses. Unlike other tech companies that have managed to break even or become profitable in 2022-23 following this kind of cost restructuring, Carvana will continue to operate at a loss indefinitely.

Strengths and Opportunities

If Carvana could make its operations profitable—which is a big "if"—it would be in an interesting position. The dealership market in the United States generates nearly $200 billion in revenue annually , and it's a fragmented market where technology has had a minimal impact over the decades.

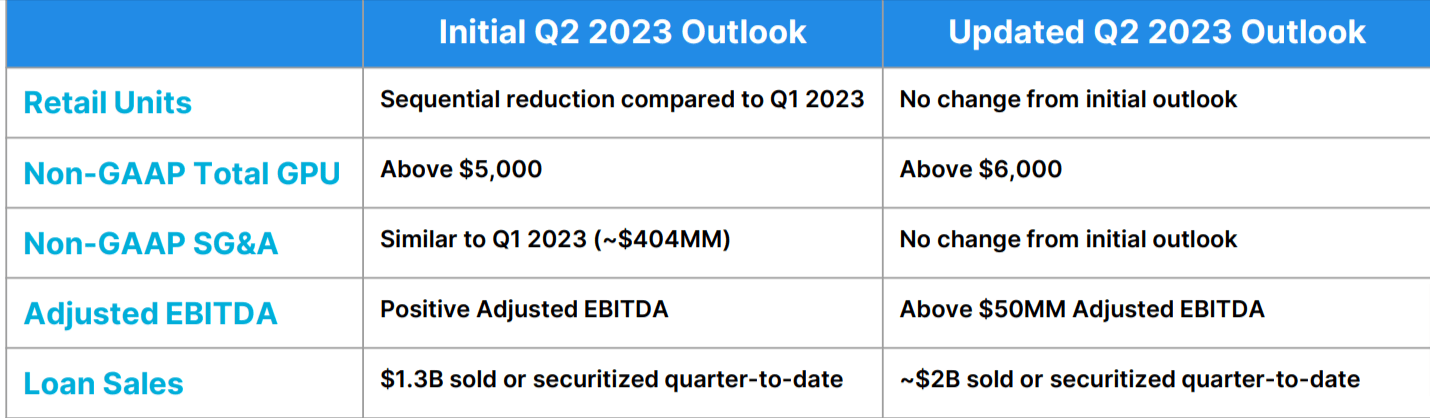

The company has also improved its forecasts for Q2 2023, assuring investors that 2022 was a challenging year and things will "return to normal" this year. Now management expects:

- Sales should slightly decline compared to Q2 2022, as the company already suggested in its previous forecast;

- Non-GAAP Total GPU should increase from last year's $5,000 to $6,000 in Q2, 2023. This metric measures Carvana's gross profit net of amortization, depreciation, share-based compensation, and excluding the impact on the balance sheet due to Root warrants;

- From the forecast of a slightly positive adjusted EBITDA, they are moving to a forecast of positive adjusted EBITDA over $50 million.

Carvana's updates for the results expected in Q2 2023 (Company Presentation at William Blair 43rd Annual Growth Stock Conference)

{kind=link}

It thus seems things are going better than expected and better than last year, mainly due to cost-cutting measures. However, it's tough to say whether this improvement will be sufficient to save Carvana.

Weaknesses and Threats

The key problem for Carvana is being unprofitable without a clear plan to become so. The CFO does a great job presenting non-GAAP measures that can reassure investors, but the uncomfortable questions remain on the table: can this business genuinely become profitable, or is it a loser at its core? Will this indeed be the future of car dealerships?

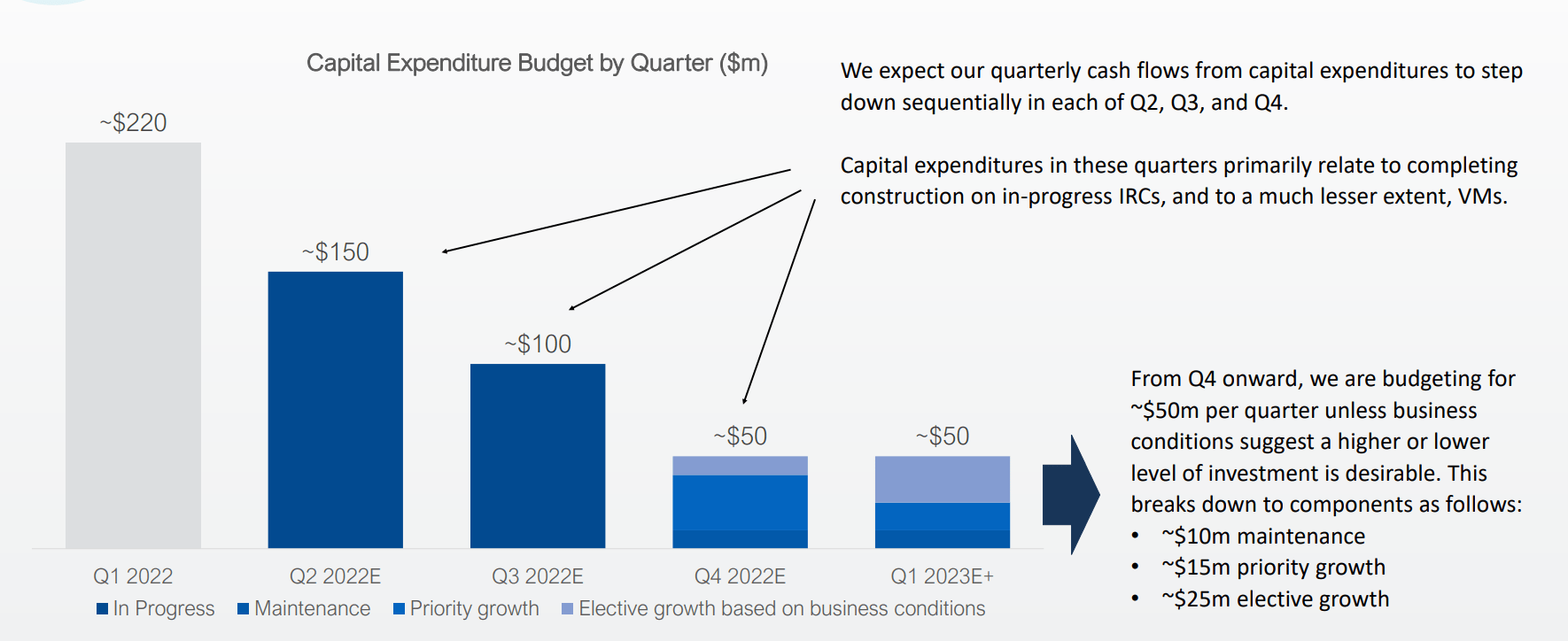

To enhance its balance sheet metrics, Carvana last May acquired ADESA, a used car auction house. In the meantime, the capital expenditure has been trimmed down from $220 million in Q1 2022 to $100 million in Q3 2022, and further down to $50 million in Q1 2023. Carvana has already stated that investments in new infrastructure will remain static at this first quarter's figure until favorable market conditions arise. This is the result of two forces acting together: the inability to generate scale economies that would justify additional capex investments, and the need to conserve liquidity reserves to avoid bankruptcy in the coming years.

Carvana's quarterly CapEx budget (Investor Deck Presentation - "Update on Carvana Operating Plan" (Pub. Aug 2022))

{kind=link}

The bankruptcy risk is more concrete than many investors may perceive, especially since Carvana is trying hard to postpone the payment of some obligations due in 2024. The company had to withdraw its offer to bondholders in early June, failing to reach the minimum threshold of $500 million. This is despite the company being in active dialogue with bondholders for months, offering increasingly attractive terms to those willing to exchange their existing bonds for new ones with longer maturities. Offers have even included 9% cash yields and 12% for payment-in-kind.

Bondholders lack confidence that Carvana can actually meet bond payments. At the same time, banks are facing their most uncertain year in over a decade, and accessing credit has become decidedly more difficult for a company that burns cash at Carvana's rate. Even shareholders' patience is running thin: despite the recent rally following the announcement of improved forecasts for the next quarter, the stock remains down 80% from its pre-pandemic high and down 93% from its post-pandemic peak.

Financials

Examining the balance sheet numbers brings anyone riding high on optimism back down to earth. Between lack of profits and looming debt maturities, Carvana can only hope that the American economy continues to show remarkable resilience and that interest rates start to decrease early next year. Even then, it is not a given that the company can turn its fortunes around.

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| Revenue |

| 13,604.00 |

| 12,814.00 |

| 5,587.00 |

| 3,940.00 |

| Operating income |

| -1,490.00 |

| -104.00 |

| -332.00 |

| -280.00 |

| Net income |

| -1,590.00 |

| -135.00 |

| -171.00 |

| -114.00 |

| Diluted EPS |

| -15.74 |

| -1.63 |

| -2.63 |

| -2.45 |

| Book value per share |

| -4.89 |

| 3.40 |

| 5.07 |

| 1.94 |

| Free Cash Flow |

| -1850 |

| -3,370.00 |

| -1,010.00 |

| -1,030.00 |

| Total Debt |

| 8,900.00 |

| 5,800.00 |

| 1,890.00 |

| 1,630.00 |

| Debt/Asset ratio |

| 1.02 |

| 0.83 |

| 0.62 |

| 0.79 |

Source of the data: TradingView

These results have been achieved:

- During the best-ever period for the job market in the U.S.

- Except for the last year, during an expansionist monetary policy period and low-interest rates.

- During a boom in the automotive market, with many consumers changing their cars for electric or low-emission vehicles.

Nobody knows for sure if there will be a soft landing during this period of high central rates, or if we will start seeing a slowdown in the job market at some point. What remains clear is that Carvana, even with years of experience in one of the best macroeconomic environments ever, still hasn't found a clear path to profitability.

Final thoughts

There are too many uncertainties currently weighing on Carvana shares. It is extremely difficult to justify a valuation of over $4 billion for a company that was willing to offer a 9% return on $1 billion of its own bonds and yet failed to reach even the minimum fundraising goal. Finding funding sources has become very complicated and, with the situation teetering between banks and commercial real estate, even the Fed has already warned that credit conditions will become even more challenging in the coming months.

The company has a very high volume of debt which, in the best-case scenario, will be refinanced at such high rates as to make reaching positive net income by the end of the decade highly unlikely. Other possible paths are bankruptcy or a disproportionate dilution of shares.

From a theoretical perspective, Carvana operates in an already established sector and merely acts as an intermediary between buyers and sellers. The idea is to make this intermediation more efficient than in the past, and in principle, the way the company aims to do this works. However, management has chosen to ride the growth-at-any-cost wave that dominated Silicon Valley until last year. In the pursuit of higher revenues, Carvana went too far with losses and debt: as a result, it is now a company with short-medium term liquidity problems and a business that will generate losses for the foreseeable future.

In a world that offers a risk-free rate close to 4%, amid the fundamental-based recovery of many other companies after the declines of 2022, I see no reason to risk one's capital on Carvana shares.

For further details see:

Carvana's Financial Struggle: A Debt-Fueled Quagmire