CVNA - Carvana's Problems Don't Have A Near-Term Fix

2023-04-24 10:17:52 ET

Summary

- Shares of Carvana have lost 90% of their value over the past year as sales growth plummeted and profitability sank.

- The company is battling declining affordability for used cars, driven by inflation as well as rising interest rates.

- Carvana is saddled with over $8 billion of debt that it will struggle to repay.

- With limited cash left on its books and a long path toward profitability ahead, Carvana's problems don't have an easy cure.

Times are tough, but especially so for Carvana ( CVNA ), the flashy car e-commerce dealer that was one of the hottest stocks on Wall Street during the pandemic. Known for its glassy "car vending machines", Carvana's dealer-free business model was touted during the pandemic as traditional car dealerships struggled from less foot traffic, but now, the company is facing issues that threaten to jolt it toward bankruptcy.

Down nearly 90% over the past year, shares of Carvana have wiped out nearly $10 billion in market value:

Despite how tempting it is to try and catch a falling knife here, I'd resist the temptation to do so. Carvana has two main issues that are going to be very difficult to surmount:

- Car sales are declining, crimped by affordability. It didn't take very long for a constrained car environment in 2021/2022 (which saw cars go off the lot faster than expected, and dealers to charge more than MSRP) to invert, and now car sellers are stuck with a load of unsold inventory. The more promotional environment, of course, will hurt Carvana's already-pressured gross profit per unit.

- Heavy debt load and no clear path to profitability. Carvana's debt pile now is worth multiples of its equity, and with giant holes in free cash flow amid surging interest rates, it's unclear how Carvana intends to get out from under.

Needless to say, I'm bearish here - though I think Carvana has been putting up a valiant fight on a number of fronts. The company is attempting to restructure its long-term debt , in an attempt to extend maturity. It's also making deep cuts in corporate overhead and advertising to speed up the process toward breakeven. Unfortunately, I don't think Carvana's problems have a near term fix.

Steer clear here - Carvana will continue to see extreme pain throughout 2023.

Already struggling to match pandemic-era volumes, the macro recession is hurting Carvana even more

Even absent a recession, Carvana was already on the downturn in the waning days of the pandemic. COVID, it seems, pulled-forward a lot of demand for large expensive purchases including cars (as well as other bulky household goods), but now we are seeing that pull-forward unwind.

{kind=link}

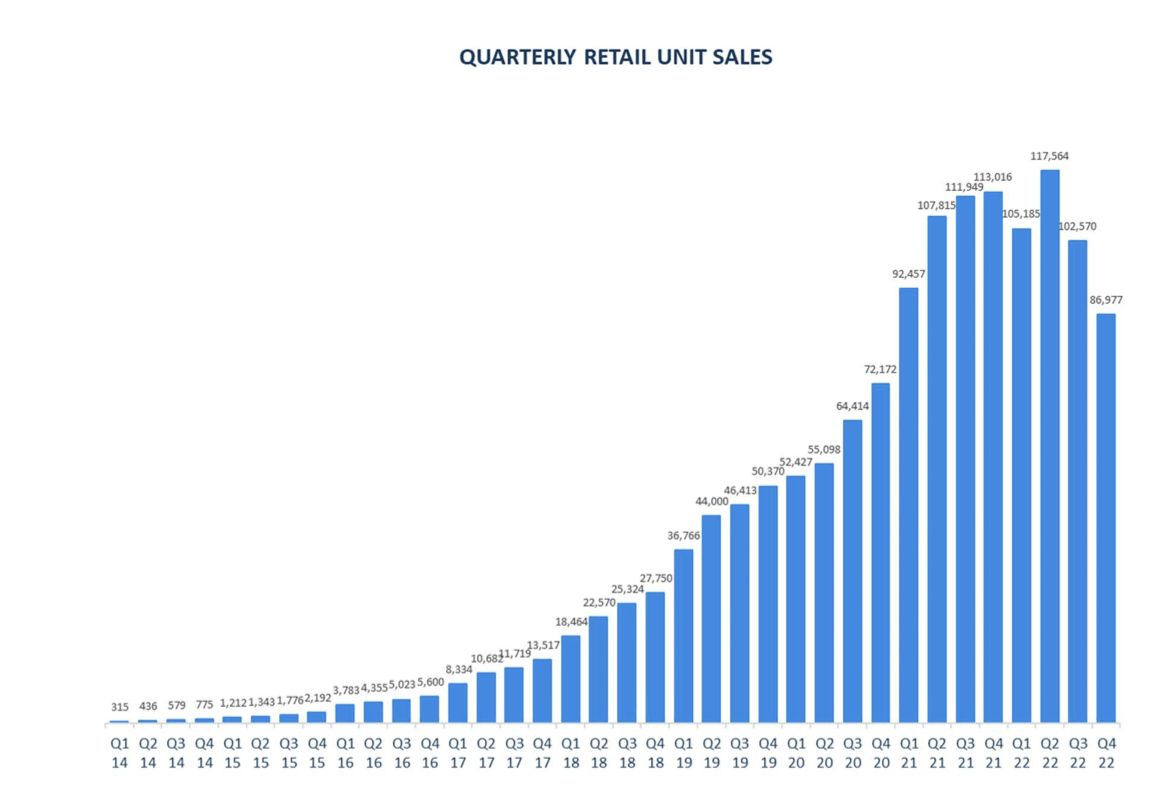

The chart above showcases Carvana's unit sales by quarter. As can be seen above, the company had been growing steadily every quarter until the third quarter of 2021. Sales then reached a temporary peak at 118k in the second quarter of 2022, before beginning a precipitous decline.

Management notes that it believes Carvana's unit sales will stabilize at the levels seen in the second half of 2022, and the company is sharply cutting marketing spend in order to prioritize profitability in the near term.

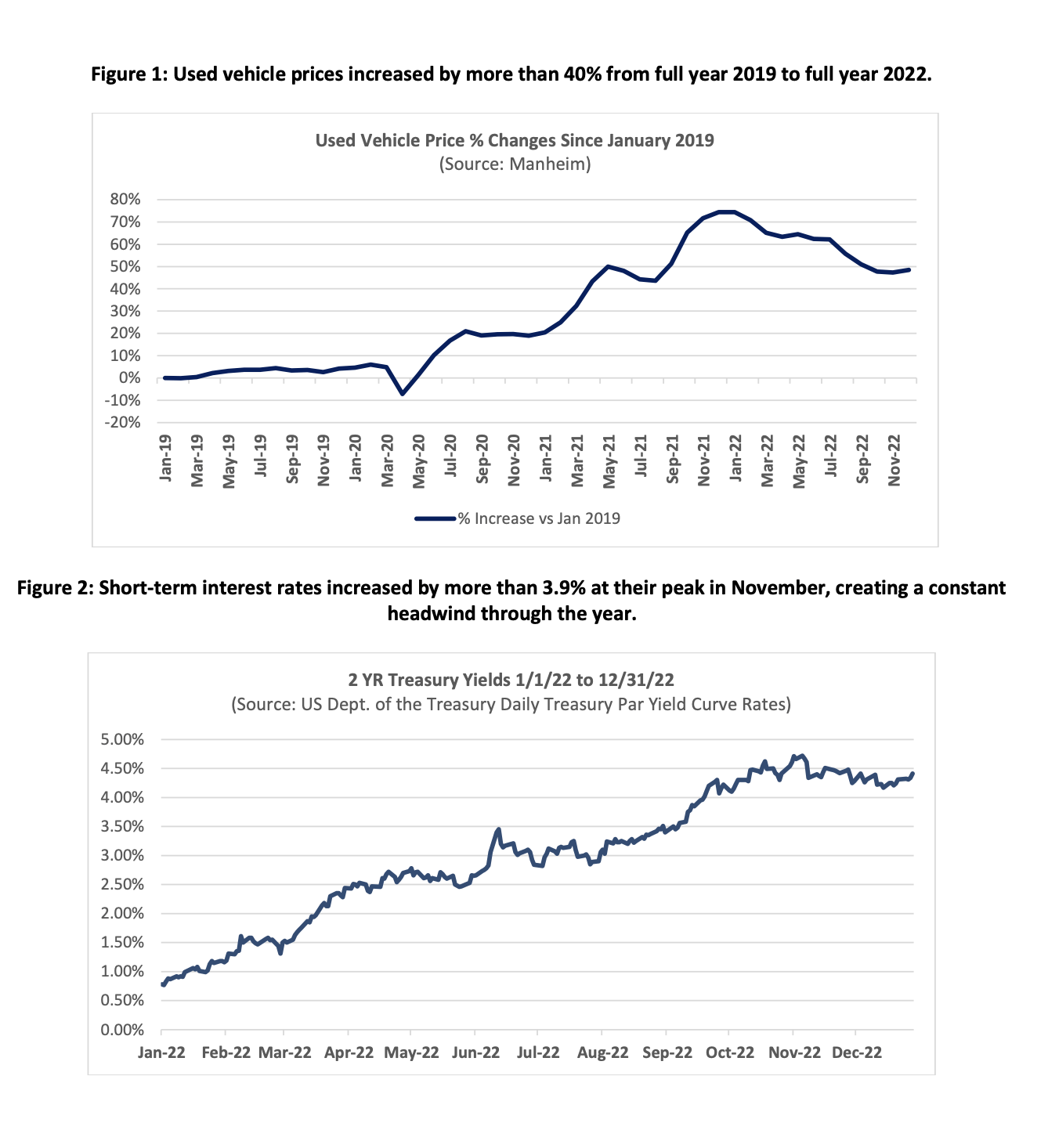

Macro conditions aren't helping here. The set of charts below, taken from Carvana's Q4 shareholder letter, showcase two factors that essentially denote "stagflation" in the used-car market. Used car prices have remained persistently high, while interest rates have continued to soar - so seeing as many car buyers finance their purchases through an auto loan, it's not difficult to understand why used car sales have plummeted.

Used car prices and interest rates (Carvana Q4 shareholder letter)

{kind=link}

Note as well that Carvana is losing market share. The company's retail unit sales declined -23% y/y in the fourth quarter, while management reported that the used-car industry saw only a -6% y/y decline in the fourth quarter. This suggests that as the brick-and-mortar retail world has resurfaced, traditional car brokerages are regaining share (and some of these competitors may be in a better position to discount inventory to attract sales than Carvana, which is pinched on profitability).

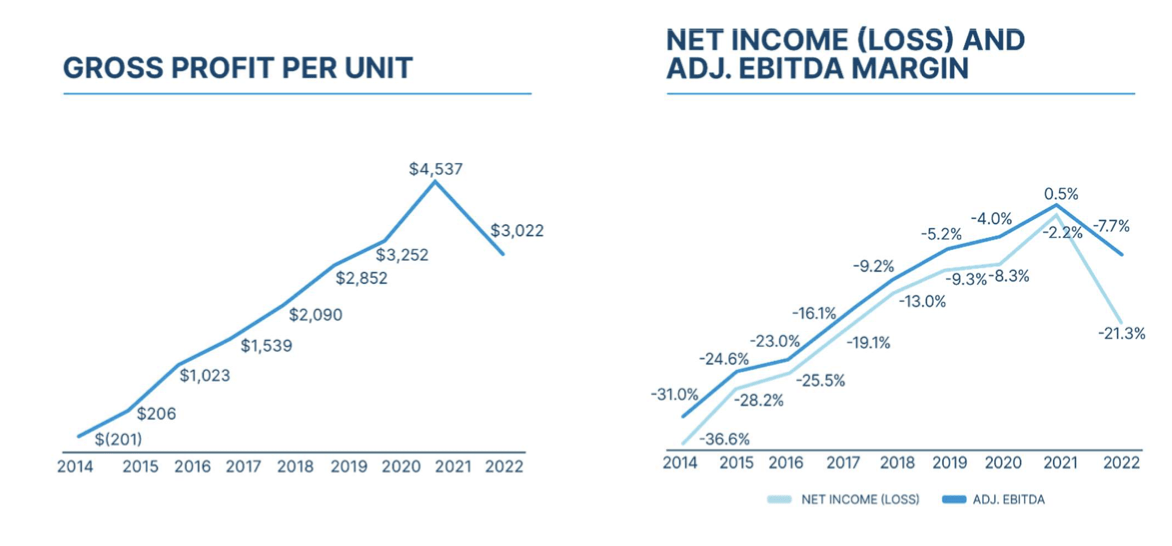

It's worth noting as well that volume deleverage and higher inventory levels (which leads to carrying costs and depreciation) have caused Carvana's gross profit per unit ((GPU)) to fall sharply to just $3,022 in 2022, a -34% y/y decline.

{kind=link}

Management's outlook for the used-car space isn't exactly bullish, either. Per CEO Ernie Garcia's remarks (key points highlighted)on the most recent Q4 earnings call :

First industry level demand. There are many data sources available to assess industry level demand, but regardless of the source demand is slow. Industry data sources estimate new sales down approximately 10% to 15%, year-over-year in the third quarter. And many of the forward-looking indicators that we use internally, including web searches and artist activity on carvana.com indicate further slowing recently . Cars are an expensive discretionary often finance purchase that inflated much more than other goods in the economy over the last couple of years, and is clearly having an impact on people's purchasing decisions [...]

Regardless, we're building our plans around assumptions that the next year is a difficult one in our industry and in the economy as a whole.

Next interest rate increases. Interest rates have risen rapidly with the two-year treasury a good benchmark for automotive loans rising 3.9% over the last year and 2.6% since 2019. In addition, credit spreads have risen about 1% in the last year. To put this in perspective for a customer utilizing financing the moves into your current yields plus credit spreads of last year are equivalent in their impacts the customer's monthly payment of about a $3,000 price increase. As a result, for customers using financing cars ended the quarter at their most unaffordable point ever, despite the fact that retail prices have dropped roughly 10% this year. As benchmark, interest rates risk spreads and market expectations for future credit performance evolve over time, we do expect those changes to impact our other GPU and sales volumes before the market fully adjusts, which is built into our expectation that other GPU will move down in the fourth quarter relative to the third."

The net of this: with no end in sight to current macro hardships, Carvana's issues don't have any near-term fixes.

The debt burden

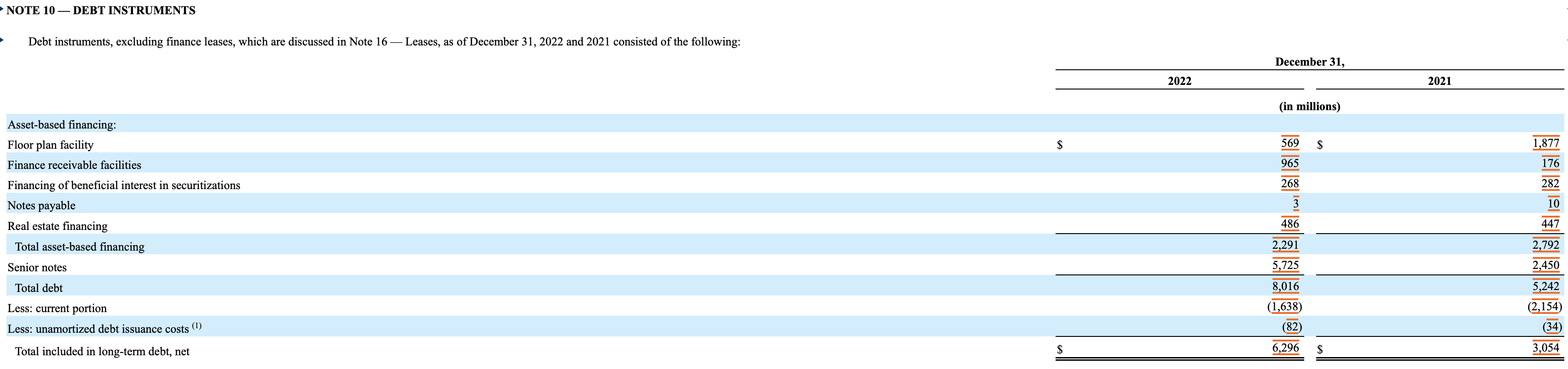

During the boom times of 2021, investors looked the other way as Carvana aggressively financed its expansion into other markets via debt. Now, the company is sitting on over $8 billion of debt, as shown in its 10-K filing:

{kind=link}

Note that the majority of Carvana's short-term debt is on floating rates, meaning Carvana is exposed to rising interest rates not only from a revenue standpoint (hurting used car sales) but also directly to the company's cost structure. And even the company's long-term debt, which it is currently attempting to restructure, doesn't come at cheap interest rates either, with the largest $3.3 billion tranche of senior notes due in 2030 carrying a whopping 10.25% interest rate.

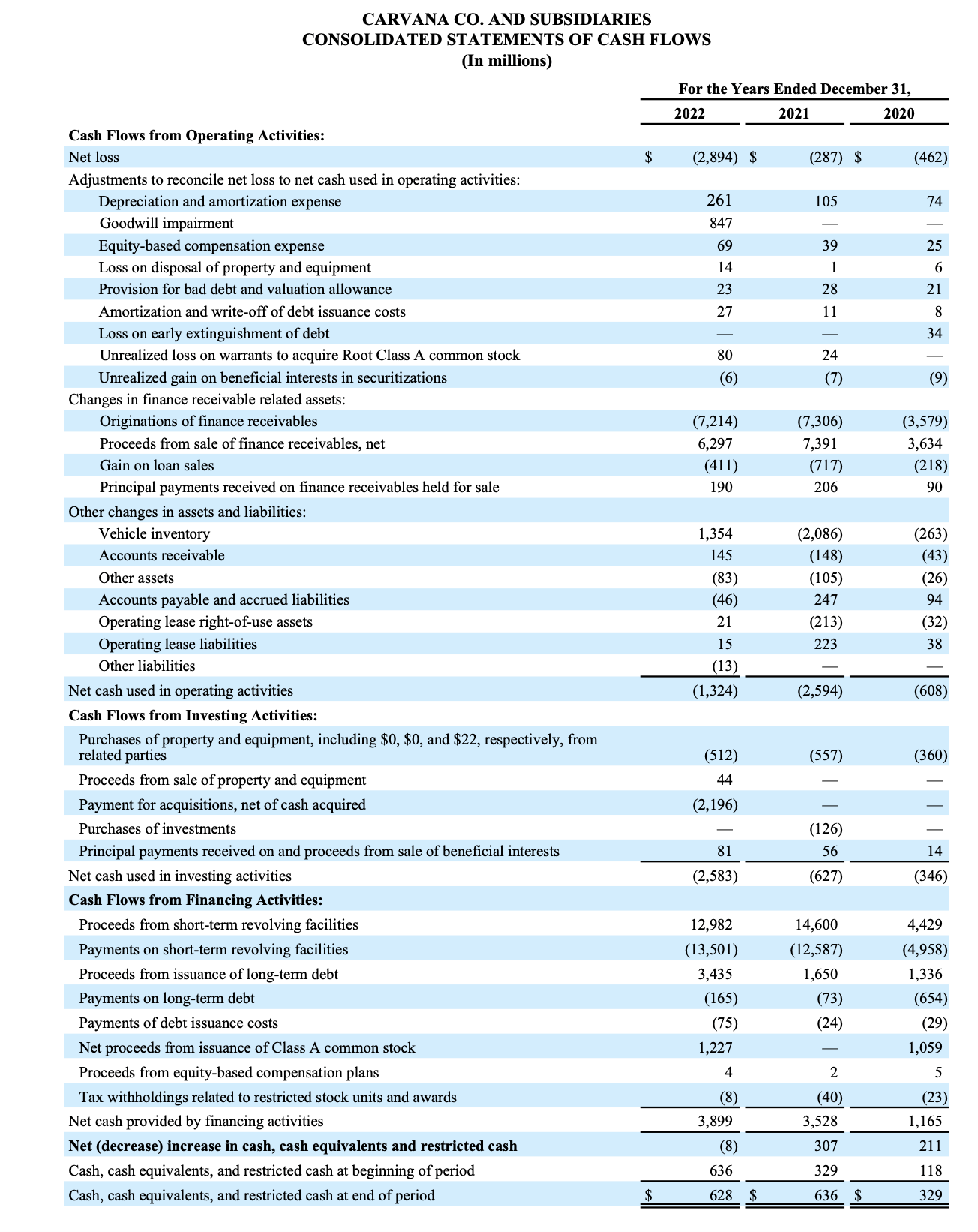

Carvana's cash burn is also quite significant. The company recorded a -$1.3 billion loss in cash from operations, and note that this is with the benefit of $1.3 billion unwinding inventory (as the company slowed down its purchases of cars amid the slowdown). This "benefit", however, can't indefinitely continue as Carvana has to maintain inventory variety in order to keep running its business.

{kind=link}

To the company's credit, it is addressing cost aggressively. It notes that from Q1 of 2022 to Q4, quarterly advertising expenses dropped 44% (though this won't do any favors toward Carvana's goal of reinvigorating unit sales). Overall, it reduced pro forma operating expenses by $140 million over that same time frame, with plans for more aggressive cuts.

The question is though: is it enough to absorb the company's $1+ billion in annual OCF losses? With only $434 million of cash left on its books, Carvana will most likely have to shoulder more debt in order to survive.

Key takeaways

The landscape is undoubtedly quite grim for Carvana: declining sales, soaring interest rates, and a crippling debt load. This is not the right stock to bet on at this moment: approach Carvana with extreme caution.

For further details see:

Carvana's Problems Don't Have A Near-Term Fix