CVNA - Carvana: Shorts Might Get Burned

2023-07-06 00:34:29 ET

Summary

- Carvana's stock has gained 183% since the last publication, despite being a favorite for short-sellers. Management has issued a positive outlook, but the company is still suffering from high debt and declining revenues.

- CVNA's financial indicators are poor, with a surge in used car sales due to stimulus checks not translating into increased earnings. Management has been criticized for poor decision-making and it has had to borrow heavily to finance business initiatives.

- I advise against short-selling Carvana due to the risk of the company improving its fundamentals and not heading for bankruptcy.

Carvana ( CVNA ) stock has been one of many short-sellers' favorites for months already. This article is an update of my earlier work on this company. When I covered CVNA, lots of my valued readers were highly eager to profit from Carvana's stock price crash. But the long-awaited crash has not happened. In fact, since my last publication, as of the time of writing, CVNA has gained a whopping 183%, whilst S&P 500 has risen by just 12%, quite a big gap. Imagine what would have happened to the short-seller selling the shares on 11 November 2022 and buying them back now. Do not get me wrong. I am not a great advocate of CVNA shares. But if you consider short-selling CVNA, think twice. Let me explain why.

Carvana stock - positive news

So, why did CVNA stock rise in value, in the first place? The company's management has recently issued a press release saying that Carvana would report a positive adjusted EBITDA of more than $50 million and total gross profit per unit above $6,000 in the second quarter of 2023. The management seemed to be optimistic about the company's outlook as it presented such a positive outlook.

However, some analysts point out that the rise in operational efficiencies was a one-off. Carvana is still suffering from high debt and declining revenues. Right now Wall Street analysts expect Carvana to report sales of $2.57 billion in 2Q 2023 and $2.63 billion in Q3 2023. These results would look much worse compared to 2022's Q2 and Q3 revenue figures of $3.88 billion and $3.39 billion, respectively.

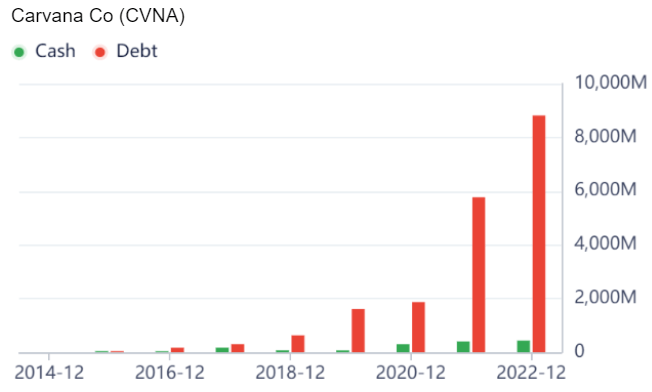

As reported at the end of 1Q 2023, Carvana's long-term debt was $6.5 billion. So, the company is quite indebted, indeed. Its operating cash flow was negative as of $66 million in Q1 2023. The company has never been profitable. But let me cover its fundamentals in some more detail.

Carvana's financial indicators

As I have briefly mentioned above, Carvana never had good financial indicators. However, the second-hand car market was boosted by generous giveaways by the government during the coronavirus crisis. In other words, in order to stimulate the economy, the US government gave out a lot of stimulus cheques to the general public, not only the unemployed. These cheques were accumulated as savings and spent on many goods, including used cars. Obviously, this made car sales soar. But in spite of that surge in revenues, Carvana's earnings have not risen.

| Year |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Sales revenue |

| 859 |

| 1955 |

| 3940 |

| 5587 |

| 12814 |

| 13604 |

| Total gross profit |

| 68 |

| 197 |

| 506 |

| 794 |

| 1929 |

| 1250 |

| Net loss |

| -164 |

| -255 |

| -365 |

| -462 |

| -287 |

| -1587 |

Source: Seeking Alpha

Author

This past performance was all due to the management's poor decision-making. As I mentioned above, there was a surge in demand for used vehicles. But Carvana neither had enough cars to meet its clients' demand nor the facilities and employees to process the cars it had available. In order to solve the problem, the management took the decision to buy ADESA and a large number of cars amid very high car prices. But after that, the demand growth started to slow down amid increasing interest rates and recessionary fears. Needless to say that Carvana was forced to borrow heavily to finance these business initiatives. In fact, it has systematically borrowed money to pay for its losses and growth initiatives. Only acquiring ADESA's U.S. physical auction business from KAR Global cost Carvana $2.2 billion earlier this year .

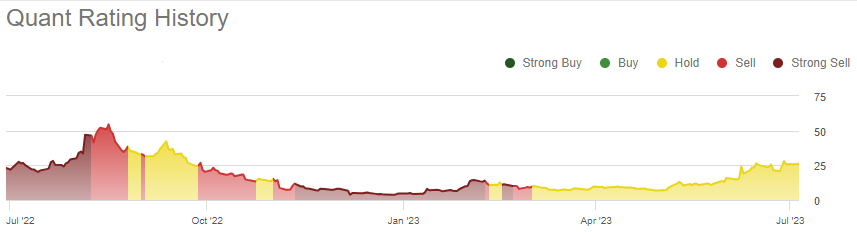

Seeking Alpha's system assigned the company with a quant rating of "Hold", quite a neutral recommendation, I would say. According to the quant factor grade, CVNA's valuation is quite poor. But its profitability is even worse. However, the company's sales are growing and its EPS were revised to the upside.

{kind=link}

But as can be seen from the graph above, CVNA's quant rating has improved thanks to its sales growth and also the positive momentum for the stock.

With all that being said, let me present a few excerpts, clearly showing Carvana's fundamental indicators.

GuruFocus

Just a quick look at Carvana's "financial strength" indicators would allow you to see how indebted and unprofitable the company is.

GuruFocus

The only bright spot is Carvana's positive gross profit. The rest, including its operating profit, is negative.

{kind=link}

The cash-to-debt position of Carvana is really poor. True, the current and the quick ratios are all tolerable but otherwise Carvana's debt is mounting, whilst its cash levels are not rising substantially.

Risks to the short-sellers

With all that being said, I urge you not to risk short-selling Carvana. To start with, Carvana reported improving gross profit per unit ((GPU)). It is not likely this improvement will be sustainable as the management expects. However, there is still a risk the company would somewhat improve its fundamentals. Not to mention the company is not headed for imminent bankruptcy in the near future. So, the likelihood its stock value would fall down to zero is also quite limited. Any good piece of news can potentially make Carvana's stock soar. This clearly happened after the GPU announcement was made at the beginning of June. At the start of this year, Carvana's 2022 full-year results were published. These were not brilliant, indeed. The gross profit declined, whilst the net loss soared. But a small rise in the company's sales made many investors show some optimism. Then, as you will see in the valuation section of this article, CVNA's current stock price of about $25-$26 is substantially below the all-time of about $360 per share recorded in 2021. So, it seems there are very limited gains to be made, whilst some CVNA optimists might make the stock price soar should anything positive be announced about the company.

Moreover, earlier on I wrote about GameStop ( GME ) and other meme shares. There was an irrational rally in early 2021 fueled by Redditors who decided to artificially increase the prices for the most heavily shorted stocks. GameStop was one of them although there were no positive changes to GameStop's fundamentals. But short-sellers who had good reasons to short-sell GME recorded huge losses. The point I am making is that short-selling is highly risky because the potential gains are limited, whilst the potential losses are unlimited. There are other general risks many short-sellers face, including the possibility of a margin call and a sudden change in fees. But the main risk in my opinion is that Carvana's management might once again surprise the market with a positive announcement. So, CVNA's short-sellers might end up recording substantial losses the way they did at the end of 2022 - the first half of 2023.

Risks to the bulls

The risks to the bulls are obvious, in my view. The company is not profitable. It is heavily indebted, whilst the used car market is not in its best shape . In fact, since the interest rates are rising, the demand for second-hand cars is falling. So, as a result, car sellers are forced to reduce their prices. If Carvana was in good financial shape, this downturn could be temporary for its business. In other words, it could be used as an opportunity to invest in CVNA stock. However, this is not the case, unfortunately. A recession is likely to come and the demand for used cars might fall even further. Moreover, it might get even harder to service Carvana's debt, which is high, indeed.

Valuations

In spite of the fact CVNA is off its 2021 high, Carvana's stock is still not good value for money.

Carvana is not profitable. It is also cash-flow-negative. So, I cannot use the P/E and P/FCF ratios. But as you can see from the excerpt below, its P/S ratio is substantially less than 1, which is good on its own. But I would not say it is a value play. Not at all.

GuruFocus

Let us just have a look at its price-to-book (P/B) ratio. It is reasonable but only adequate for a company that is profitable and has a moderate debt load. This is not the case for Carvana, unfortunately. But the stock is still not particularly expensive compared to its 2021 highs. At the same time, it is not good value for money either.

Conclusion

I am not a great optimist when it comes to Carvana's stock. There have not recently been any sound improvements in its fundamentals. The future does not seem to hold too much in store for the company. That is why it does not look very good value for money either. At the same time, its stock has already fallen substantially from its all-time highs. And there are not many gains to be made here. Moreover, it does not seem to be heading into imminent bankruptcy in the near future. That is why I am saying that short-sellers might get burned, especially given the fact we had a meme stock mania before.

For further details see:

Carvana: Shorts Might Get Burned