CVNA - Carvana: Stabilizing But Not In The Clear

2023-10-31 12:19:31 ET

Summary

- Carvana's stock has risen over 500% this year but has fallen 50% from its September peak.

- The company has made a turnaround in its bottom line, but unit sales are still falling.

- Carvana's profitability is recovering, with a significant increase in gross profit per unit, but there are transitory factors underneath this that may fade.

- With many uncertainties still on the horizon, it's best to remain on the sidelines.

Needless to say, 2023 has been a volatile year for many small and mid-cap stocks, but few more so than Carvana ( CVNA ) - the car e-commerce marketplace that took the world by storm during the pandemic. After shaving billions of dollars off its market cap earlier this year as investors balked at the company's debt concerns and falling sales, Carvana staged an unlikely turnaround: driven by its decisions to shrink inventory, reduce its own headcount, and improve profitability.

Now, year to date, the stock has risen more than 500%: though it has fallen ~50% from its September peak. It's also worth noting that Carvana remains down more than 90% from its peak pandemic highs that briefly exceeded $350.

The question now is: with all this volatility, what is the best thing to do with Carvana stock?

Earlier this year in April, I wrote a bearish opinion on Carvana when the company was dealing with the brunt of its issues. Debt was mounting, unit sales were falling, and GPU was declining. Since then, the company has made a major turnaround in its bottom line, driven by rising GPU as well as the company's decision to l ay off 8% of its workforc e, or roughly 1,500 people. In light of the company's sturdier bottom line, I'm raising my viewpoint on Carvana to neutral. It certainly also doesn't hurt that CEO Ernie Garcia purchased more than $100 million worth of stock in August, reflecting confidence in a turnaround.

But in terms of recommended actions at this juncture: I still think staying on the sidelines is the best move. Because while GPU improvements and positive adjusted EBITDA are comforting, we have to remember that Carvana is still a business that relies heavily on economies of scale. And at the moment, unit sales are still falling - which could impose deleveraging on the company if trends continue.

The bottom line here: though Carvana seems to have saved itself from the brink of disaster, its troubles are far from over. We'll need to see consistent trends of increasing unit sales before we feel comfortable going long here again.

The good news: profitability is recovering

Let's start with the more sanguine aspects of the Carvana story that have materialized since the start of the year.

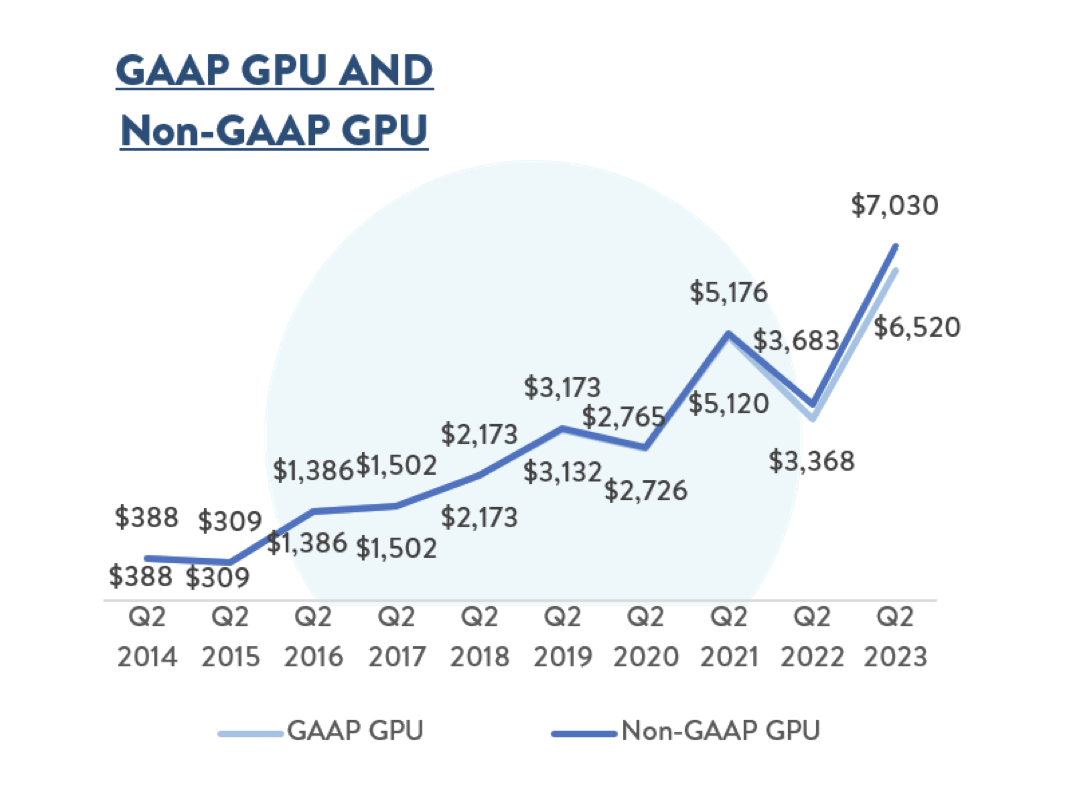

Gross profit per unit was a dire story in 2022 as used car prices dropped and Carvana's pricing power eroded. You can see that after a temporary spike in Q2 of 2021, prior-year GPU in the chart below dropped -29% y/y to $3,683.

{kind=link}

This year, however, the company has managed to notch a Q2 record GPU of $7,030, nearly doubling from the prior year. It also jumped sequentially from a $4,796 GPU in Q1.

Underneath this, the company recorded a ~$900 one-time benefit to GPU driven by two factors:

- Carvana's reduced inventory fleet means that the company took in fewer inventory write-downs, boosting GPU by a one-time $250 this quarter

- Also, the company sold more loans in Q2 in its financing portfolio than it originated, increasing GPU by ~$650 this quarter.

Excluding that noise, however, GPU still jumped markedly both y/y and sequentially. The sustained business drivers behind this include shorter shelf-lives of cars in inventory, higher dealer spreads between inventory acquisition cost and resale price, lower vehicle reconditioning costs, and higher fees charged for car shipping.

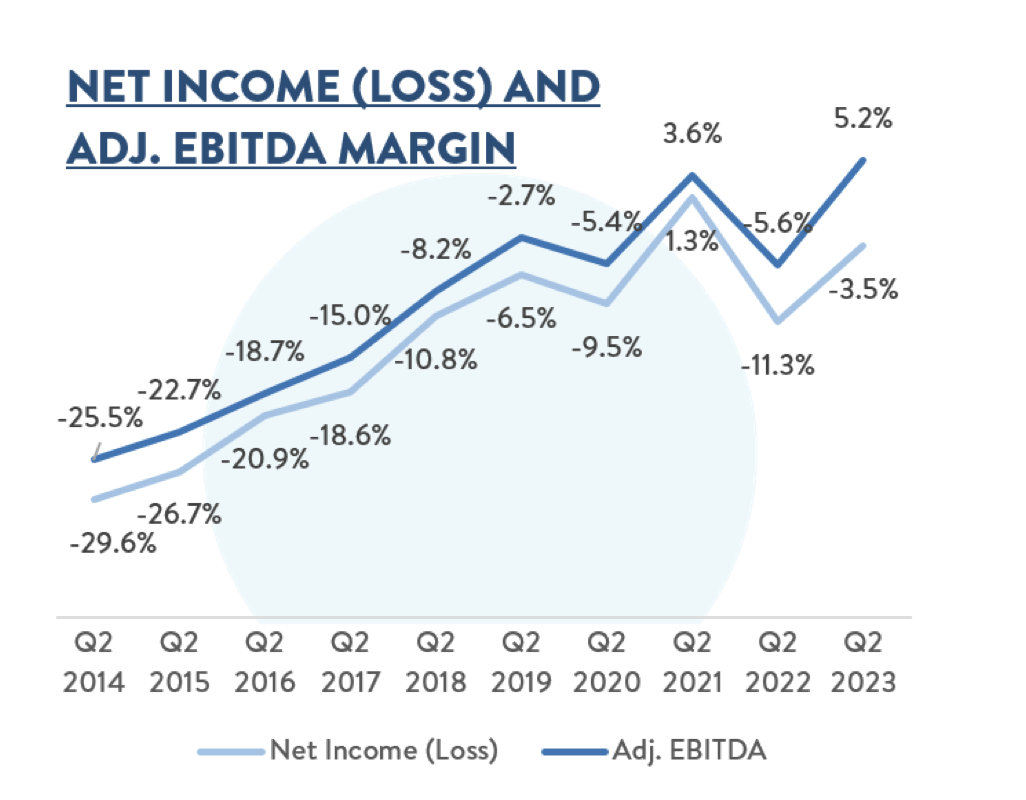

This boost in GPU, meanwhile, was compounded by Carvana's decision to lay off 8% of its headcount. The company managed to hit a record adjusted EBITDA margin of 5.2% in Q2, versus a loss margin of the same magnitude in the prior-year Q2:

Carvana Q2 adjusted EBITDA margins (Carvana Q2 shareholder letter)

{kind=link}

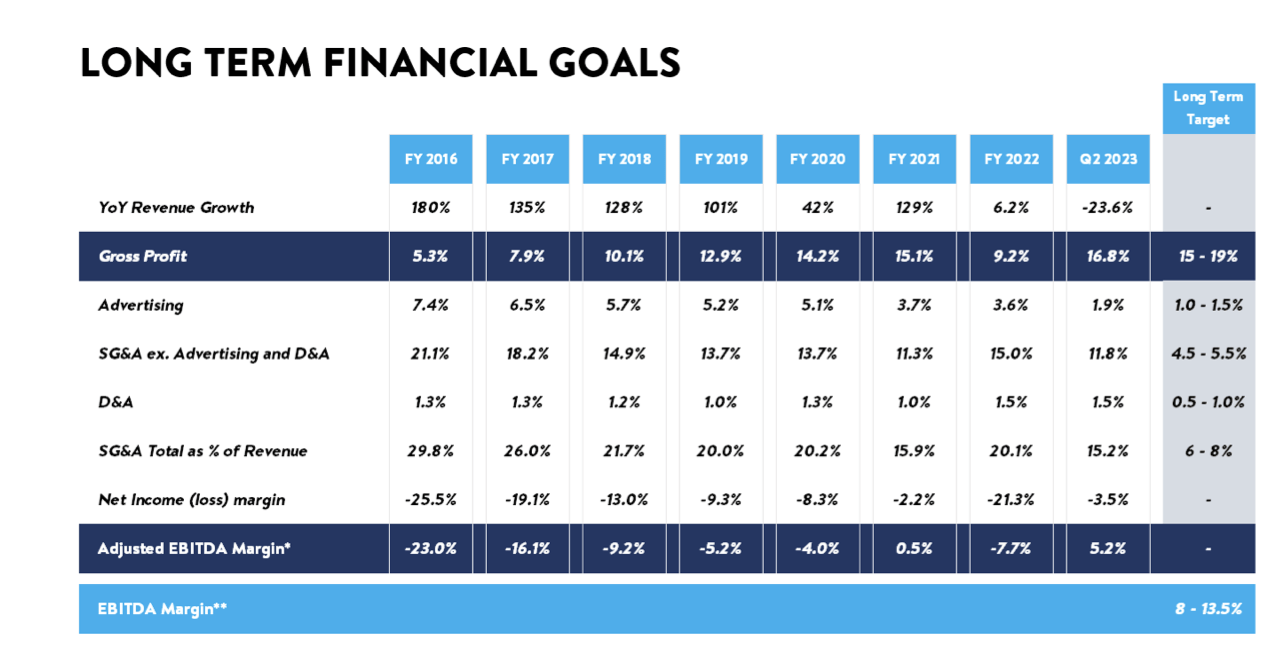

We can see as well in the chart below that Carvana has finally hit its target gross margin relative to its long-term operating model goals (with the caveat that GPU this quarter benefited by $900 or ~13% of total GPU due to one-time factors).

Carvana long-term operating model (Carvana Q2 shareholder letter)

{kind=link}

The company is also indicating that it hopes to have enough room to slice a further 6-7% of revenue off of its SG&A costs, with an aim to bring adjusted EBITDA margins to the mid-teens.

The unfortunate news: declines in unit volume sales may threaten the path to profitability

Here's where the rub kicks in, though: Carvana's path to scaling profitably relies on economies of scale. GPU benefits this quarter were driven in no small part by Carvana's inventory reductions.

Holding fewer cars means less storage and idle capital costs: but it also reduces the variety and attractiveness of Carvana's marketplace to potential buyers. Add that on top of an already weak car sales market driven by cash-strapped consumers, high financing rates, and supply chain disruptions from the recent auto union strikes, and we have a potentially disastrous formula.

{kind=link}

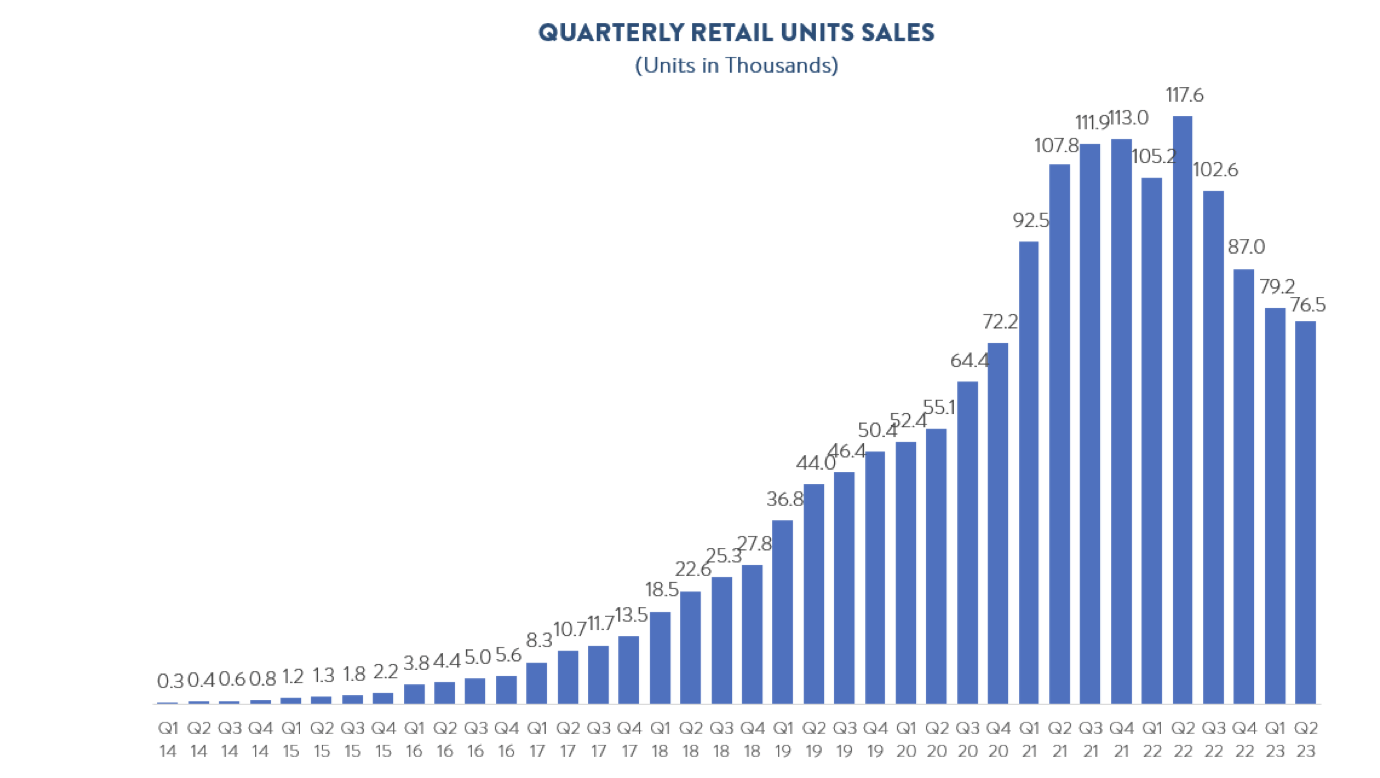

As seen in the chart above, Carvana's retail unit sales slipped -3% sequentially and -25% y/y to 76.5k units sold. Revenue, in turn, also dropped -24% y/y to $2.97 billion.

Here's CFO Mark Jenkins on the Q2 earnings call discussing the drivers behind reduced unit volumes:

In the second quarter, retail units sold totaled 76,530, a decrease of 35% year-over-year and 3% sequentially. Similar to past quarters, our decline in retail units sold, which we expected, was driven by four primary factors: reduced inventory size, reduced advertising, increased benchmark interest rates and credit spreads, and a continued focus on executing our profitability initiatives."

Now, the fact that Carvana is making nearly twice as much gross profit per vehicle certainly helps blunt this impact: but if unit sales continue their downward trajectory and the one-time benefits to GPU this quarter fade, Carvana's short stint producing adjusted EBITDA profits may dwindle.

Key takeaways

Carvana stock jumped sharply out of correction territory this year, but a lot of investor enthusiasm could be based on transitory factors (wider-than-usual dealer spreads, for example) and potentially ignore the risks that are still on the table (declining unit sales, driven in part by inventory reductions). Overall, it's too early to declare that Carvana has solved all of its problems and has a clear path to a recovery rally. Maintain caution here and stay on the sidelines.

For further details see:

Carvana: Stabilizing, But Not In The Clear