CVNA - Carvana: Turnaround Sounds Enticing But Don't Bite

2023-05-18 10:24:31 ET

Summary

- Carvana managed to dramatically reduce its operating costs to forecast a positive adjusted EBITDA in the following quarter.

- However, this may not be enough for the company due to Carvana's extremely high debt and its burdens.

- Macroeconomic concerns coming from high interest rates could also work as a headwind.

Introduction

Throughout 2022 as used car demand and prices fell from pandemic highs, Carvana's (CVNA) stock saw a massive decline. The bloated levels of inventory bought during times of pricey used cars were a burden for the company as the used car prices started to drop. Also, the company's focus on growth over profitability did not bode well in quickly changing macroeconomic conditions. As such, the company was in a dire situation throughout most of 2022 and into 2023. However, after the company's 2023Q1 earnings report, some investors started to point out that the worst could be over as the company's turnaround seemed possible. Results, both top and bottom-line, were better than expected with an expectation of a positive adjusted EBITDA in the following quarter. The company dramatically reduced operating costs while working down inventory to successfully bring up the gross profit per unit to a historical high. Yet, I would like to ask a question. Is this enough? I believe that even this impressive progress does not warrant a buy rating as there are too many risks involved with the company. Carvana's operating costs are still too high, despite the improvement, likely leading to the company continuing to report negative net income throughout 2023, and most importantly, the company's debt load is extremely burdening. Although there may be some positive tailwinds from recovering used car prices, I believe it is too early and too risky to start investing in Carvana; thus, Carvana is a sell.

Progress

Progress has certainly been made by the company during 2023Q1 . Carvana dramatically reduced costs including SG&A, marketing, and logistics costs. SG&A expense declined from $727 million in 2022Q1 to $472 million in 2023Q1, which is about a 35% decline. Marketing expenses dropped to $56 million from $155 million a year ago. Finally, logistics expenses dropped to $35 million from $56 million in the previous year. Through these successful cost-cutting measures, the company reported an adjusted EBITDA margin of negative 0.9%, a significant improvement from a negative 10.3% margin in the previous quarter. Further, beyond cost cutting, the company also made progress in right-sizing inventory increasing the GPU, gross profit per unit, to a record high of $4796. Finally, continuing the progress and moving forward, the company forecasted an above $5000 GPU with a positive adjusted EBITDA.

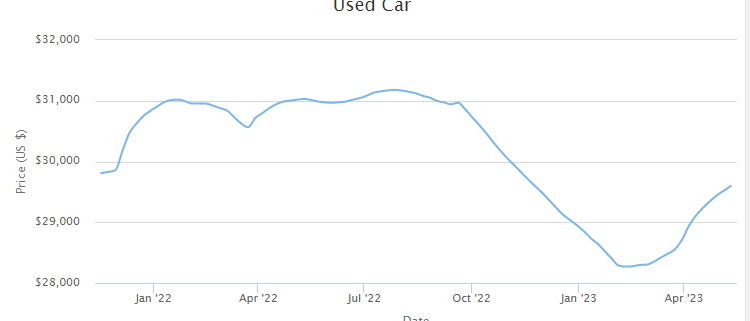

On top of the company's own efforts, a market tailwind has been forming in recent months. After a used car price decline throughout 2022, used car prices have been increasing again in the past months. According to the CPI data from the US Bureau of Labor Statistics , used car prices jumped 4.4% month-over-month in April after seeing multi-months of sequential price declines. And, CarGurus' (CARG) used car index also supports this data. As the chart below shows, the used car prices tracked by CarGurus show that the price has been seeing a consistent increase throughout most of 2023. As such, Carvana's results were likely aided by the macroeconomic tailwind, and with the pricing trend seeing no signs of reversing, Carvana may continue to enjoy a favorable tailwind trend.

{kind=link}

Is It Enough?

The progress Carvana reported during 2023Q1 is amazing. However, I believe it is too early to conclude that the company's turnaround efforts will be successful due to the company's debt load and potential impending macroeconomic concerns.

Carvana's debt load is extremely burdening. The company had a long-term debt of about $6.5 billion with cash and restricted cash of about $694 million. As such, in 2023Q1, the company had an interest expense of $159 million, which is about 46.6% of the gross profit. Further, the company's depreciation and amortization expense was $93 million during 2023Q1. Two expenses combined equaled 78.8% of the gross profit. Therefore, while achieving positive adjusted EBITDA, on the surface, seems great, because of the company's interest expenses, Carvana will continue to be deeply unprofitable.

This, in my opinion, is extremely concerning. Used car demand and prices were extremely high during the pandemic, yet the company could not turn a profit. Then, in 2023Q1, the company reached an all-time high GPU burning through the existing inventory, yet, again, the company burned through $66 million in operating activities. Thus, beyond negative financial metrics that are putting pressure on the company, I believe it is reasonable for investors to have doubts about the future potential of the company's business model until further progress has been made despite an improving outlook.

Another point of concern that I have is the growth and inventory. The company's inventory declined by about $385 million in 2023Q1 from 2022Q4 to about $1.5 billion after declining about $1.35 billion throughout 2022 . During this period of aggressive inventory management, revenue declined 25% year-over-year as retail units sold declined, and the company is continuing to expect a revenue decline in 2023Q2. For achieving minimum cash burn to paint a turnaround, this may be optimal, but eventually, in the next few quarters, the company will need to acquire cars to maintain certain levels of inventory, which could be problematic. The company has a difficult time reporting positive adjusted EBITDA burning through its existing inventory when the time comes when the company can not burn through hundreds of millions of dollars in inventory, achieving profitability could be extremely challenging, especially with the company's debt load and rising used car prices.

Finally, macroeconomic headwinds may be impending. According to the St. Louis Federal Reserve, the average financing rate of used car loans has increased steadily throughout 2022 and has reached 14.78% in 2022Q4. Although the organization did not yet update the data, many third-party companies point to a continual increase in loan rates in 2023. I believe this to be reliable as the Federal Reserve has raised the federal funds rate by 50 basis points since 2022Q4. Therefore, for buyers of a used car who is financing the purchase, it is getting more difficult, which will likely act as a headwind to Carvana for the foreseeable future.

Summary

Carvana is showing strong progress in its turnaround efforts. Both top and bottom-line results improved as operating expenses were greatly reduced. However, I believe this result was only possible as it came at the expense of burning inventories. When the time to purchase a car comes, the story may be different. Further, the company's debt load is extremely high creating a wall that may not be easy to overcome, especially as macroeconomic headwinds regarding interest rates are likely impending. Therefore, I continue to believe Carvana is a sell.

For further details see:

Carvana: Turnaround Sounds Enticing, But Don't Bite