CVNA - Carvana: Why I Am Staying Far Away Ahead Of Q3 Earnings

2023-10-31 16:49:16 ET

Summary

- Carvana's share price has surged by almost 500% this year, driven by better-than-expected earnings in Q2.

- The company's debt restructuring has contributed to the rise in share price, but I believe its capital structure remains unsustainable.

- The sales outlook does not look optimistic and will further complicate Carvana's path to recovery. I expect the company to report further revenue declines in the third quarter.

- When reporting third quarter earnings later this week, the company is likely to report gross profit per unit in line with expectations. However, the company remains far from profitable.

Carvana Co (CVNA) share price has skyrocketed this year and is up by almost 500% year-to-date. This drastic rise in its share price was largely due to Carvana reporting better-than-expected earnings in the second quarter. However, despite this improvement, the company remains unprofitable and has continued to see declining revenue. In my view, there is little justification for the rise in the share price and I would be hesitant to add this stock to my portfolio.

The balance sheet

The restructuring of Carvana's debt has contributed materially to the rise in the share price. At the time of announcing its second quarter results Carvana indicated that they have successfully finalized a debt restructuring deal, resulting in a reduction of the used car retailer's overall debt by over $1.2 billion. This agreement will specifically remove more than 83% of their unsecured note maturities for 2025 and 2027, as well as decrease their mandatory cash interest payments by more than $430 million annually over the next two years.

The agreement prompted a ratings upgrade from S&P Global in light of the near-term improvements in the company's liquidity position brought about by it. However, this was still accompanied by a cautionary note in terms of which S&P warned that -

While the restructuring reduces debt and improves liquidity over the next 24 months by reducing cash interest expense, we believe the company's capital structure remains unsustainable. This is due to its weak earnings profile and the substantial PIK interest, which will cause the company's debt load to increase over the next two years.

I am in agreement with this cautionary statement. In my view, the agreement has done little more than kick the can down the road rather than addressing the company's long-standing unsustainable debt load. John Engle expressed similar concerns and noted that while Carvana's debt restructuring may initially seem like a significant achievement, a closer examination suggests it's more of a temporary fix than a long-term solution.

Engle correctly points out that a closer examination of the debt restructuring reveals several worrisome aspects. Notably, the immediate positive impact on cash flow is offset by higher interest rates across all debt. Essentially, Carvana has managed to postpone cash expenditures and extend repayment deadlines. Additionally, as part of the deal, the company will conduct a dilutive stock offering, involving the sale of $35 million worth of shares at the current market price.

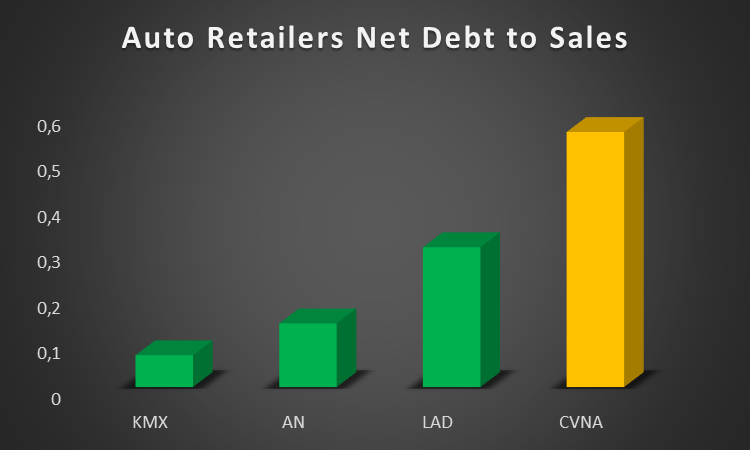

Carvana's debt levels are also much higher than that of other automotive retailers as depicted in the peer comp chart below. The company's net debt amounts to around 0.56 times expected sales for 2023 which is much higher than the second-most indebted automotive retailer, Lithia Motors ( LAD ), whose net-debt to sales ratio is around 0.307.

Auto Retailers Net Debt to Sales (Author created based on data from EquityRT)

{kind=link}

The earnings outlook

Carvana's second quarter results came in better than expected with most analysts having expected a $1.15 per share loss rather than the $0.55 loss per share reported. Revenues at $2.97 billion also came in substantially higher than the expected $2.6 billion. Nevertheless, revenue still came in around 24% lower than a year ago. In the current economic environment, I also don't expect the revenue picture to turn around in the near term.

There has been a substantial increase in defaults on auto-loans in recent months. Due to soaring inflation, a growing number of Americans are unable to meet their automotive loan obligations, reaching levels not witnessed in almost thirty years. The proportion of subprime borrowers, who are at least two months behind on their loan payments, climbed to 6.11% in September. This is an increase from the previous peak of 5.93% in January, as reported by Bloomberg citing Fitch Ratings data.

The rise in defaults has already resulted in some banks tightening underwriting criteria for automotive loans. This tightening of credit will likely contribute to a more prolonged sales slump in the used vehicles segment which will make it even more challenging for Carvana to resume sales growth. In my view, these conditions are likely to persist in the next few quarters and will make it particularly difficult for Carvana to see meaningful sales growth.

This is further exacerbated by ongoing inventory challenges brought about by the pandemic. A recent article published on CNBC explained this well in noting that at the start of the COVID-19 pandemic in 2020, automakers temporarily closed factories to contain the virus, leading to subsequent supply chain disruptions, including a prolonged semiconductor chip shortage. This caused factories to halt production for extended periods over the past few years. The reduced production resulted in a scarcity of new vehicles transitioning into the used market. These supply shortages have persisted long after the reopening of most economies.

Moreover, an unusually high number of consumers are opting to purchase their leased vehicles to avoid exorbitant car prices and escalating interest rates. Used vehicle inventory has decreased substantially and has been stuck in the 2.2 - 2.3 million vehicles range compared to the pre-pandemic levels of 2.8 million available vehicles in 2019. According to Cox Automotive, it is not anticipated that the total number of used vehicle sales will return to the pre-pandemic figure of approximately 38.2 million units until at least 2026.

Given these challenges, it seems unlikely that Carvana's upcoming third quarter results would have the same positive surprises in store as the second quarter results. Nevertheless, management has provided updated guidance for the third quarter and currently expects gross-profit per unit to come in at around $5500 while revenue is expected to remain unchanged. Should Carvana be able to deliver on this guidance, the stock is likely to react positively. Nevertheless, the company remains far from profitable.

Valuation

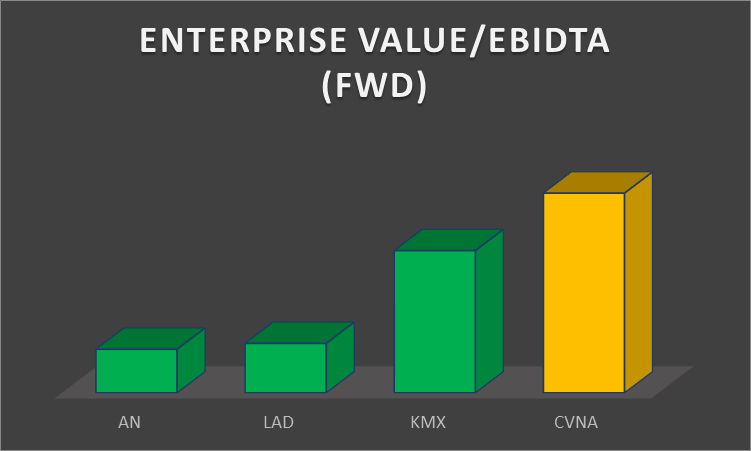

Carvana's consistent lack of profitability makes it more difficult to assign a value to the stock using traditional metrics such as the price-to-earnings ratio. In the peer comp chart below I compared Carvana's enterprise value to 2023 expected earnings before interest, taxation, depreciation and amortization (EBITDA ). On this basis Carvana is the most expensive auto retailer considered in the peer comp charts.

Enterprise value/EBITDA (FWD) (Author created based on data from EquityRT)

{kind=link}

Such higher valuation might have been justified had the company seen growth rates far outpacing that of its peers. However, this has certainly not been the case at Carvana over an extended period of time. It becomes even more difficult to justify the premium when its peers have been consistently profitable while Carvana has never been, nor is it certain if it ever will be. The uptick in gross profits per unit might signal some profitability in future but this remains much too uncertain.

Nevertheless, further improvements in EBITDA might prompt the share price to continue its rise. This is a material risk to the sell rating. However, in my view, EBITDA would need to rise by a substantial margin to justify further share price growth, particularly given the high debt levels at Carvana. Ultimately, I would view an EV to EBITDA level of around 10 to be more appropriate for Carvana given the continued high debt levels and debt servicing costs associated with the company.

Risk to the thesis

The key risk to my negative view of the company includes a positive uptick in gross-profit per unit beyond the $5500 indicated in the guidance by management. A substantial increase in this metric might well contribute to a temporary uptick in the share price even if the company remains unprofitable. Investors are likely to monitor this metric particularly closely when Carvana reports earnings later this week.

An unexpected increase in revenue could have a similar effect. However, I do not foresee this as likely given the challenging economic environment and the introduction of more stringent underwriting rules in relation to auto loans.

Conclusion

While Carvana's share price has performed exceptionally well this year it's crucial to note that the company remains unprofitable, with declining revenue persisting. Furthermore, while the debt restructuring has provided short-term relief, concerns about the long-term sustainability of Carvana's capital structure remain. In my view the debt restructuring is a temporary fix that simply kicks the can down the road rather than a lasting solution to the debt problem that has long plagued Carvana.

The ongoing inventory challenges, stemming from pandemic related supply chain disruptions and the increase in the number of consumers purchasing leased vehicles rather than trading in, further complicates Carvana's path to recovery. These challenges together with the rise in default rates and the tightening of lending criteria suggest that the used vehicles sales market might experience further slowing down. This will significantly hamper Carvana's ability to return to revenue growth.

When evaluating Carvana's valuation, it becomes evident that its lack of profitability and high debt levels warrant a cautious approach. A more conservative EV-to-EBITDA ratio of around 10, aligned more closely with companies like LAD, seems more appropriate given the current circumstances. Therefore, I currently rate Carvana as a sell. However, I would not personally short the stock given the high volatility associated with the stock price and the risk of a short-squeeze despite the weak fundamentals

For further details see:

Carvana: Why I Am Staying Far Away Ahead Of Q3 Earnings