C - CCD: This Convertible Fund May Be Worth Considering

2023-10-17 14:24:56 ET

Summary

- The Calamos Dynamic Convertible and Income Fund offers a 12.92% current yield, making it attractive for income-focused investors.

- The CCD closed-end fund's performance has been disappointing, with a decline of 15.33% since early January and a much larger price decline since the start of 2022.

- The fund invests in a combination of convertible securities and high-yield bonds, with a focus on total return through capital appreciation and income.

- The fund's poor performance was largely caused by the premium narrowing, as the stock price has substantially underperformed the portfolio over the past six months.

- The fund managed to cover its distribution in the most recent fiscal period and it is trading at the best price in a long time.

The Calamos Dynamic Convertible and Income Fund ( CCD ) is a closed-end fund, or CEF, that income-focused investors can purchase to achieve their goals without the need to sacrifice the potential upside of an equity portfolio. The fund’s 12.92% current yield stands as evidence of its capabilities in the income space, although as I have pointed out in the past there may be some concern among market participants that the current distribution is not sustainable. After all, for most of the 21st century, any asset with a yield above 10% was viewed with suspicion as such a yield was typically a sign that the market expected a near-term distribution cut. This rule is less true now that interest rates and yields are at the highest levels that we have seen since early 2001, but it is still something that we should investigate before purchasing this fund. As such, this article will endeavor to pay special attention to the fund’s finances.

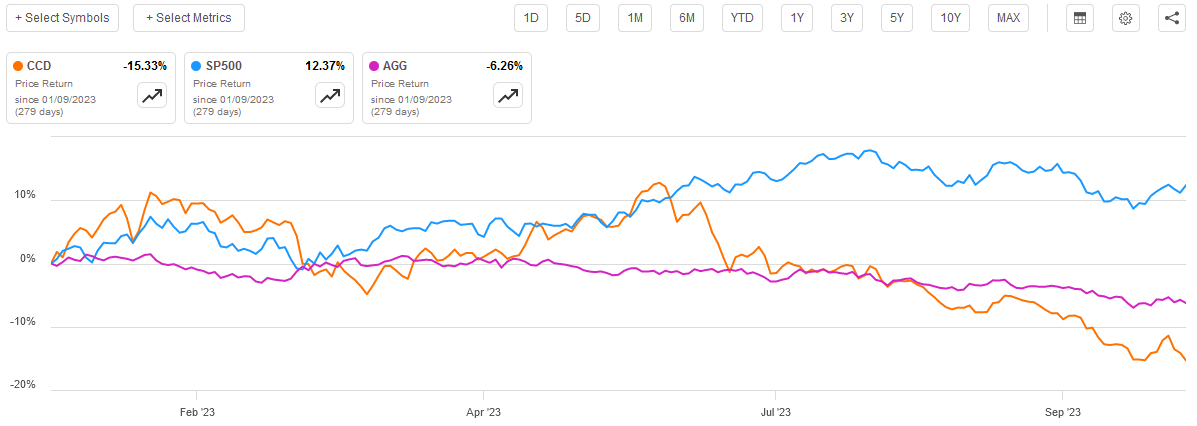

As regular readers may recall, we last discussed this fund in early January. Its performance since that time has unfortunately not been particularly impressive. As we can see here, the fund’s share price has declined by 15.33% since the date that the previous article was published. This is worse than either the S&P 500 Index ( SP500 ) or the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

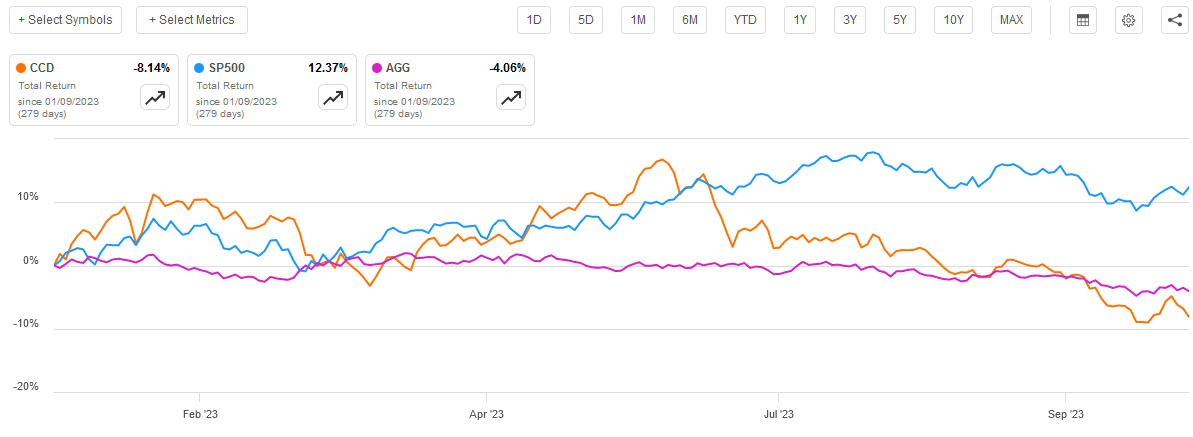

However, it is important to keep in mind that this fund has a substantially higher yield than either of the other two assets that are shown in this chart. While the distribution is sometimes overlooked by investors in favor of price performance, it does constitute an important factor in evaluating the performance of an asset. After all, the payments that you receive from a stock, or a fund can offset some of the price declines. In this case, the distributions do manage to improve the fund’s performance substantially, but investors in this fund still fared worse than investors in either of the indices:

{kind=link}

This is disappointing and certainly reduces the appeal of the fund considerably, even for those who are merely seeking to earn a high level of income. However, there might still be some reasons to consider it so let us investigate further.

About The Fund

According to the fund’s website , the Calamos Dynamic Convertible and Income Fund has the primary objective of providing its investors with a very high level of total return. That is not particularly surprising considering the description of the fund’s strategy that the website also provides:

The Fund invests in convertibles and high-yield fixed-income securities with the aim of generating total return through a combination of capital appreciation and income. To help generate income and achieve a more favorable risk/reward profile, the investment team can also sell options.

As we can see, the fund is investing in a combination of convertible securities and high-yield bonds, which are colloquially called “junk bonds.” It is much more weighted towards convertible securities, however, as 79.38% of the fund’s assets are invested in these securities:

CEF Connect

This is why the fund’s emphasis on total return makes a lot of sense. Convertible securities by themselves are income vehicles. After all, for the most part, these are just preferred stocks or bonds that happen to have the ability to be converted into common stock of the issuing company. This conversion feature is what turns these securities from simply pure income vehicles into total return ones, as that feature can provide the opportunity for enormous capital gains. After all, as I pointed out in a recent article , convertible securities are usually issued by start-up or distressed companies that cannot obtain affordable interest rates on standard debt due to cash flow problems.

I should not have to explain to anyone reading this that investing in distressed companies or start-ups can be incredibly rewarding if you pick the right company. Investing in convertible securities is generally a safer way to get these profits than investing directly in the common stock of the issuing company though since they are still fixed-income securities that sit higher in the capital stack than common equity, and they provide a reasonable level of income while waiting for the company’s story to play out.

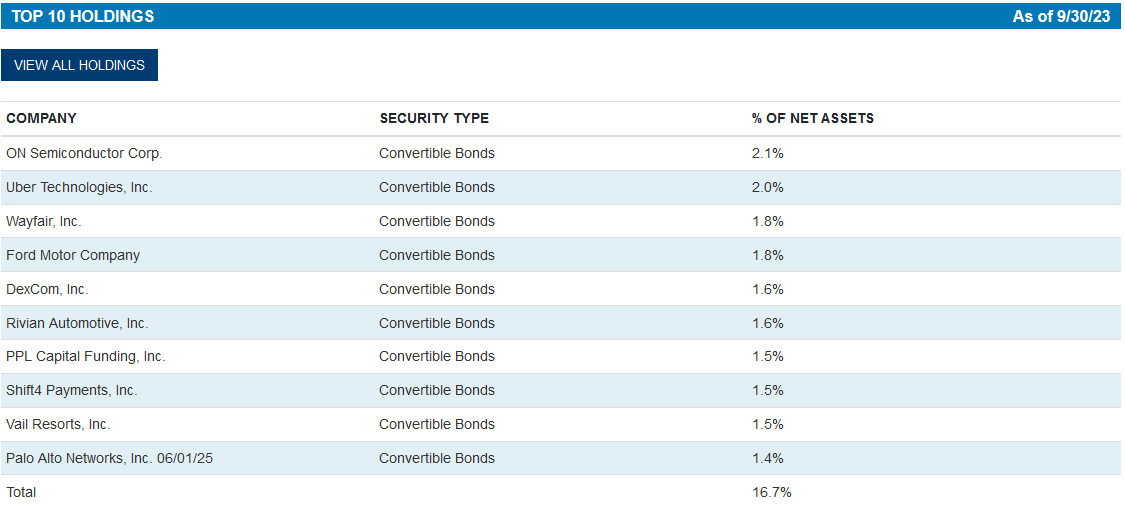

As might be expected, many of the largest positions in the fund are companies that have either had some financial problems in the past or are fairly young companies. Here they are:

{kind=link}

With the exception of Ford ( F ), many of these companies were founded within the past twenty years or so. This confirms the statement about start-ups, as we do not know exactly when each of these bonds was issued. While the semi-annual report does state the maturity date, it does not specify when each was first issued into the market.

The Uber Technologies ( UBER ) bond, for example, matures on December 15, 2025. Uber Technologies was founded in 2009, even though it did not conduct its initial public offering until 2018. Thus, this might be a ten-year bond, but it was probably issued during the pandemic considering that the coupon rate on it is actually 0.000%. Uber has always struggled with cash flow, at least until very recently, but things were especially bad for the company during the pandemic (its operating cash flow in 2020 was negative $2.745 billion) due to people not wanting to travel and generally preferring to stay at home. The company almost certainly could not have issued a zero-interest-rate bond without some sort of equity kicker at that time, even with the Federal Reserve keeping interest rates incredibly low. Thus, my guess is that this is a five-year convertible bond. The semi-annual report does confirm that this is a convertible bond, but it does not specify when exactly it was issued.

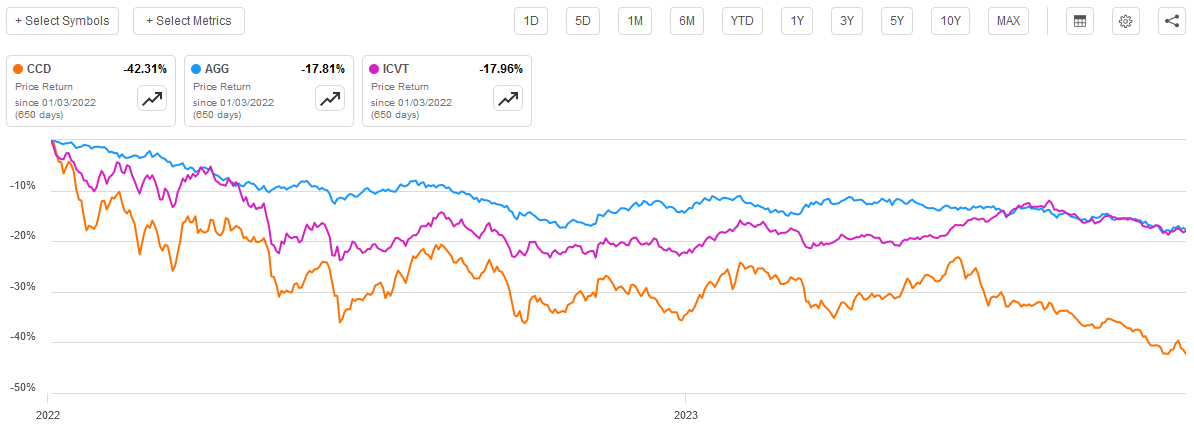

The fact that the majority of the fund’s holdings are fixed-income securities means that it has a great deal of exposure to interest rates. After all, bond prices correlate inversely to interest rates. We certainly see this interest rate exposure since the start of 2022, as the fund’s shares are down a whopping 42.31% since that time. This is far worse than either the Bloomberg U.S. Aggregate Bond Index or the Bloomberg U.S. Convertible Cash Pay >$250MM Index ( ICVT ):

{kind=link}

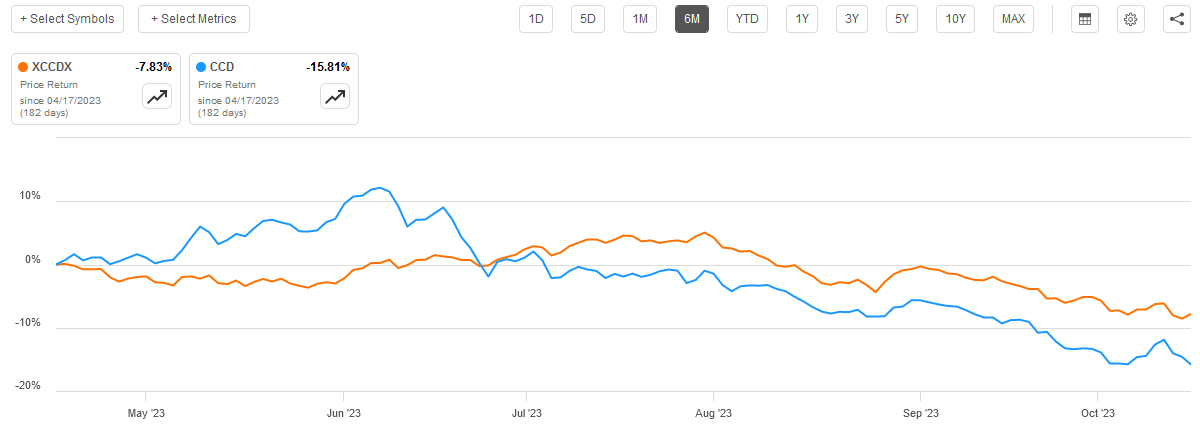

One of the reasons for this underperformance is undoubtedly the fact that the fund employs leverage. We can see this quite clearly in the fact that the fund tends to decline more than the convertible bond index does during any downturn. However, we can see that this fund has been declining since early June, but the index has not. Indeed, that actually accounts for a decent proportion of the overall decline in the fund’s shares that we see in the period. One big reason for this is that the difference between the fund’s share price and its net asset value has been narrowing. As we can see here, the fund’s share price was trading at an enormous premium to net asset value back in June, but its share price has since declined far more than the fund’s net asset value. In fact, the shares are now trading at a discount:

{kind=link}

Over the past six months, the fund’s net asset value has only declined by 7.83% but its shares are down a whopping 15.81%. That alone explains quite a bit of the disappointing performance that the fund has delivered recently. This is not a fault with the fund’s management, as the portfolio is actually holding up reasonably well considering the current market environment. The market simply became unwilling to hold this fund at a premium to net asset value. The Calamos Dynamic Convertible and Income Fund is hardly alone here, as several other closed-end funds have also experienced narrowing premiums over the past few months. I have pointed this out in a few recent articles.

The big question right now is where interest rates go from here. That is a difficult question to answer, but it is more likely that interest rates will go up, especially in the near term, rather than decline. Earlier today, the Commerce Department reported that retail sales soared 0.7% month-over-month in September, far surpassing economists’ expectations. This is despite the fact that Citibank ( C ) and Barclays ( BCS ) both reported that credit card transactions were down in September. This data is almost certainly going to increase the likelihood of the Federal Reserve implementing yet another rate hike as the central bank is trying to slow down the economy, but this data indicates that so far it remains too strong.

I will admit that I have my doubts about the quality of this data, as there has been a trend lately for the government to initially report very strong economic data that is then quietly revised down a few months later after everyone has forgotten about it. However, the important thing in terms of interest rates is how the Federal Reserve will react to the data and, while it is uncertain whether or not this alone will be enough to justify a rate hike, it is certainly not what anyone hoping for a pivot wanted to see.

Leverage

As mentioned earlier in this article, the Calamos Dynamic Convertible and Income Fund employs leverage as a means of boosting the effective yield and total return of its portfolio. I explained how this works in my previous article on this fund:

In short, the fund is borrowing money and then using the borrowed money to purchase convertible bonds. As long as the yield of the purchased securities is higher than the interest rate that the fund has to pay on the borrowings, this strategy works pretty well to boost the overall yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are substantially lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since this would expose us to too much risk. I do not usually like to see a fund’s leverage above a third as a percentage of its assets for this reason.

As of the time of writing, the Calamos Dynamic Convertible and Income Fund has leveraged assets comprising 38.61% of its portfolio. This is relatively in line with the leverage ratio that the fund had back at the start of the year, but it is still higher than we really want to see. The fact that this fund invests primarily in debt instruments helps somewhat, as the fund’s holdings will generally be less volatile than common stocks, but I would still feel more comfortable if it were to reduce its leverage. That is particularly true right now as it appears that interest rates are likely to trend up, which would increase the fund’s leverage as the value of its assets declines.

Distribution Analysis

Earlier in this article, I mentioned that the primary objective of the Calamos Dynamic Convertible and Income Fund is to provide its investors with a very high level of total return. However, in order to accomplish this, the fund invests in convertible bonds, along with a few junk bonds. These securities primarily deliver their investment returns through direct payments made to their owners. The fund collects all of the payments that it receives from the securities that it purchases using its net assets, then it borrows money and purchases even more securities to boost the effective yield of its portfolio. The fund also may be able to profit from the conversion of some of its bonds into common stock and then sell the common stock. Ultimately, it pays out all of the money that it collects from these activities to its shareholders, net of its own expenses. We might expect that this would allow the fund to boast a very high yield.

This is certainly the case, as the Calamos Dynamic Convertible and Income Fund pays a monthly distribution of $0.1950 per share ($2.34 per share annually), which gives it a 12.92% yield at the current price. The fund has been remarkably consistent with respect to its distribution over the years, as it has never cut its payout:

{kind=link}

This distribution history seems likely to appeal to those investors who are seeking to earn a steady and consistent level of income from their portfolios. For example, this payout regime might be appealing if you want money coming in every month to use to pay your bills, make your car payment, or cover some other regular expense. However, closed-end funds are highly dependent on the performance of their portfolios to get the money needed to make their distributions, and as we all know investment returns are not particularly consistent. Thus, we should examine the fund’s finances in order to ensure that it is not depleting its investment principal, as that is unsustainable over extended periods.

Fortunately, we have a relatively recent document that we can consult for the purpose of our financial analysis. As of the time of writing, the fund’s most recent financial report is the semi-annual report that corresponds to the six-month period that ended on April 30, 2023. This document was linked to earlier in this article. This is a much more recent document than the one that we had available to us the last time that we discussed this fund, which is nice.

As everyone reading this is likely aware, the market delivered a reasonably strong performance during the first half of 2023 as traders became very optimistic that the Federal Reserve would quickly pivot on its monetary policy and began bidding up the price of many assets, such as long-term bonds. In addition, we saw a bubble form in artificial intelligence, which caused several technology stocks to surge in price. The fund might have had an opportunity to take advantage of this and sell some appreciated assets to earn some capital gains. This is much better than the depressed market that we experienced in 2022.

During the six-month period, the Calamos Dynamic Convertible and Income Fund received $6,514,488 in interest and $2,402,532 in dividends from the assets in its portfolio. However, some of this interest was considered amortization of principal and is thus not considered to be income for tax purposes. As such, the fund only reported a total investment income of $5,279,479 during the period.

This was, unfortunately, not enough to cover the fund’s expenses and it reported a net investment loss of $5,909,852 during the period. Obviously, that is not nearly enough to cover any distributions, but the fund still paid out $30,759,769 to its shareholders during the period. At first glance, this is concerning because the fund did not have anywhere close to enough income to cover its distribution.

Fortunately, this fund does have other methods through which it can obtain the money that it needs to cover its distribution. For example, capital gains could be a big source of income for this fund in certain markets considering the conversion feature possessed by many of the securities in its portfolio. Capital gains are not considered to be investment income for tax purposes, but they still obviously represent money coming into the fund. The fund did have some success in this task, as it reported net realized gains of $45,095,440 during the period, which was partially offset by $32,942,643 net unrealized losses.

Overall, the fund’s net assets declined by $16,588,424 during the period. That is concerning, but the fund’s net realized gains were actually enough to completely cover the net investment loss and the distribution with money left over. Thus, the distribution was fully covered during the period.

While the fund’s net assets did decline overall, that was due to net unrealized losses. These can be erased when the market turns and starts driving asset prices upward again. It is only really a problem when we see the fund start realizing significant losses, and that was not the case here. Overall, its finances were okay during the period. We will want to examine the fund’s performance again when the full-year report comes out in a few months, as the market has weakened considerably, and the fund’s management may not be having as much success securing capital gains during the second half of its fiscal year as in the first half.

Valuation

As of October 16, 2023 (the most recent date for which data is currently available), the Calamos Dynamic Convertible and Income Fund has a net asset value of $18.12 per share but the shares currently trade for $18.17 each. This gives the fund a premium of 0.3% at the current price. This is a bit higher than the 0.05% discount that the shares have traded at over the past month, and admittedly I do not like to purchase any fund at a premium. However, this one has traded at pretty close to net asset value for a few months now compared to the enormous premium that it had earlier in the year.

For the most part, when you buy it, you are going to be doing so at a premium or discount that is so small that it hardly matters. The current price is basically about the most attractive that we have seen all year so now is as good a time as any to buy shares.

Conclusion

In conclusion, the Calamos Dynamic Convertible and Income Fund is better than it looks on the surface. The fund’s recent poor performance is simply caused by the fund’s share price falling back into line with its net asset value. The portfolio as a whole has not done that poorly considering that most of the assets in it are nominally fixed-income securities. The fact that it did manage to cover its 12.92% yield during the first half of its fiscal year is quite impressive and the current price is as good as we have seen all year.

The only real problem here is that the possibility of further rises in interest rates could drag on the fund’s performance, but that is a problem for anything that is not a pure floating-rate debt fund. Overall, this one might be worth considering right now.

For further details see:

CCD: This Convertible Fund May Be Worth Considering