CA - Cenovus Energy: Buy This Year's Oil Sands Laggard

2023-04-14 13:31:13 ET

Summary

- Cenovus Energy Inc. is one of the highest-quality E&Ps in the Canadian oil patch.

- But its shares have underperformed peers.

- Given the company’s torque to higher oil prices, we believe the underperformance offers an attractive buying opportunity in Cenovus Energy Inc.

We believe the oil market is in a long-term structural supply deficit that will keep prices elevated in order to tamp down demand and incentivize additional production. The IEA's April Oil Market Report , which was published today, offers additional support for our view. It noted that March OECD inventories drew strongly and that the IEA's own forecasted oil supply deficit is set to accelerate throughout the year.

One of our favorite stocks for playing higher oil prices is Cenovus Energy Inc. ( CVE ). We believe the company's cash flow generation potential and management's pledge to return 100% of free cash flow to shareholders can cause the stock to double from its current price of $17.50.

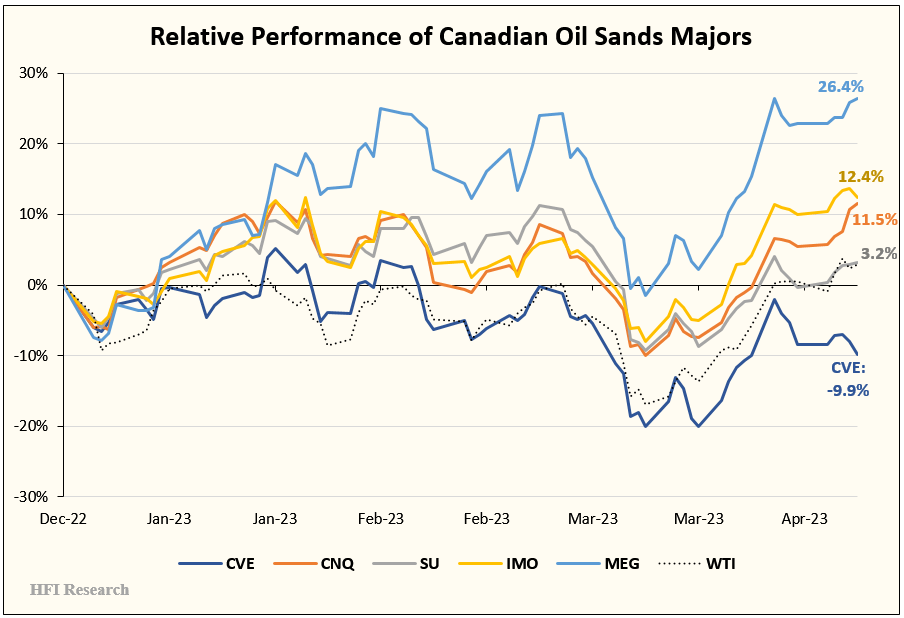

Interestingly, CVE has underperformed its peers by a large margin since the beginning of the year. MEG Energy ( MEGEF ), Canadian Natural Resources ( CNQ ), Imperial Oil ( IMO ), and Suncor ( SU ) have either kept pace with or have significantly outperformed WTI's flat year-to-date performance. Only CVE has failed to keep pace with WTI.

{kind=link}

CVE's underperformance has been a head-scratcher to us. The company's assets, return on capital, and management are among the best in the Canadian oil patch, while its long-term investment prospects have not changed during the entire stretch of underperformance. All this implies that CVE's appreciation prospects relative to its peers have increased since the beginning of the year.

What's Not to Like?

If there's a blemish on the Cenovus Energy Inc. story, it's that the company missed its guidance for increasing the amount of capital returned to shareholders. About a year ago, management had guided to higher dividends and share repurchases once CVE's net debt balance was reduced to $4 billion. At the time, management expected the debt target to be hit by the end of 2022. Unfortunately, CVE missed the target by $300 million, ending the year with $4.3 billion of net debt. Declining oil prices, lower-than-expected production volumes, and various cash payments during the second half of the year were behind the miss.

Shareholders were further frustrated when, on CVE's fourth-quarter 2022 earnings conference call on February 16, management pushed its guidance for increased return of capital to the end of the third quarter of 2023. A $1.2 billion cash tax payment and a $300 million payment toward the acquisition of 50% of the Toledo Refinery-both of which are scheduled for the first quarter-were the culprits behind the delay. The company will also be boosting capital expenditures in 2023, which will reduce the amount of cash flow available to pay down debt.

Clearly, the guidance miss was a disappointment, but not one that should sour shareholders on management or CVE's cash-generating potential at higher oil prices. At $90 per barrel WTI and $2.50 per Mcf natural gas, which we expect in the second half of the year, we estimate the company can generate around $7.5 billion of free cash flow on an annualized basis. This assumes 2% year-over-year oil production growth, a slight decline in natural gas production, a $15 per barrel WCS differential, and a boost in refinery throughput due to the Superior Refinery startup, lower turnaround activity, increased runs at the Wood Refinery, and the Toledo Refinery acquisition. If we also assume that the company reduces its share count by 3.5%, $7.5 billion of annualized free cash flow in 2023 equates to $3.87 per share. This should allow the company to achieve management's $4 billion net debt target by the end of the third quarter, consistent with current guidance. We expect significant increases in dividends and repurchases to commence in the fourth quarter.

In 2024, we estimate that CVE can generate $11 billion at $100 per barrel WTI and $2.50 per Mcf natural gas. Assuming the share count is reduced by another 5%, CVE would generate $5.97 of free cash flow per share. At that level of free cash flow, CVE shares would have to trade up to $40 to generate a 15% free cash flow yield. Given our expectation for oil prices to be sustained above $90 and our belief that a 15% free cash flow yield is generous for E&P with a three-decade reserve life, we believe CVE shares could double from today's $17.50 market price.

Conclusion

Cenovus Energy Inc. has a lot going for it, particularly with regard to its torque to higher oil prices. However, its recent stock price performance doesn't reflect its bullish prospects amid higher oil prices. Cenovus Energy Inc.'s underperformance makes little sense to us, so we view it as an attractive buying opportunity for long-term investors. Investors should consider CVE stock for exposure to higher oil prices, a growing dividend yield, stepped-up share repurchases, and inflation protection for an investment portfolio. With more than 100% appreciation potential from the current stock price, we believe investors should start buying Cenovus Energy Inc. stock now.

For further details see:

Cenovus Energy: Buy This Year's Oil Sands Laggard