CA - Cenovus: Three Headwinds Explain The Underperformance

2023-12-15 08:00:00 ET

Summary

- We had recommended Cenovus Energy's preferred shares for a lower-risk play on the company's credit.

- Those have outperformed the common shares by about 30% since then.

- We update our outlook on the common shares, and preferred shares and also look at the warrants.

Note: All amounts discussed are in Canadian Dollars unless specified otherwise.

In our last take on Cenovus Energy Inc. (CVE), we focused on the preferred shares and told you why they made an incredibly compelling investment. In fact, we rated the common shares of CVE as a "Buy ", but gave the Cenovus Energy Inc. CUM RED FIRST PFD Series 1 ( CVE.PR.A:CA ) a "Strong Buy" . Our logic was simply based on the heavy undervaluation of CVE.PR.A compared to almost everything else that we could find.

We see CVE as a proxy "A" rated company and hence think the preferred shares should offer a relatively low spread vs. GOC-5 yields. CVE.PR.A came with a spread of 1.73% (which we think is fair) but thanks to a price that is now 50% below par, the effective spread vs. GOC-5 is more than double to near 3.5%. This is a very high quality dividend stream (current yield 5.31%) that offers a good source of variable dividends.

Source: Preferred Shares Look Incredibly Attractive

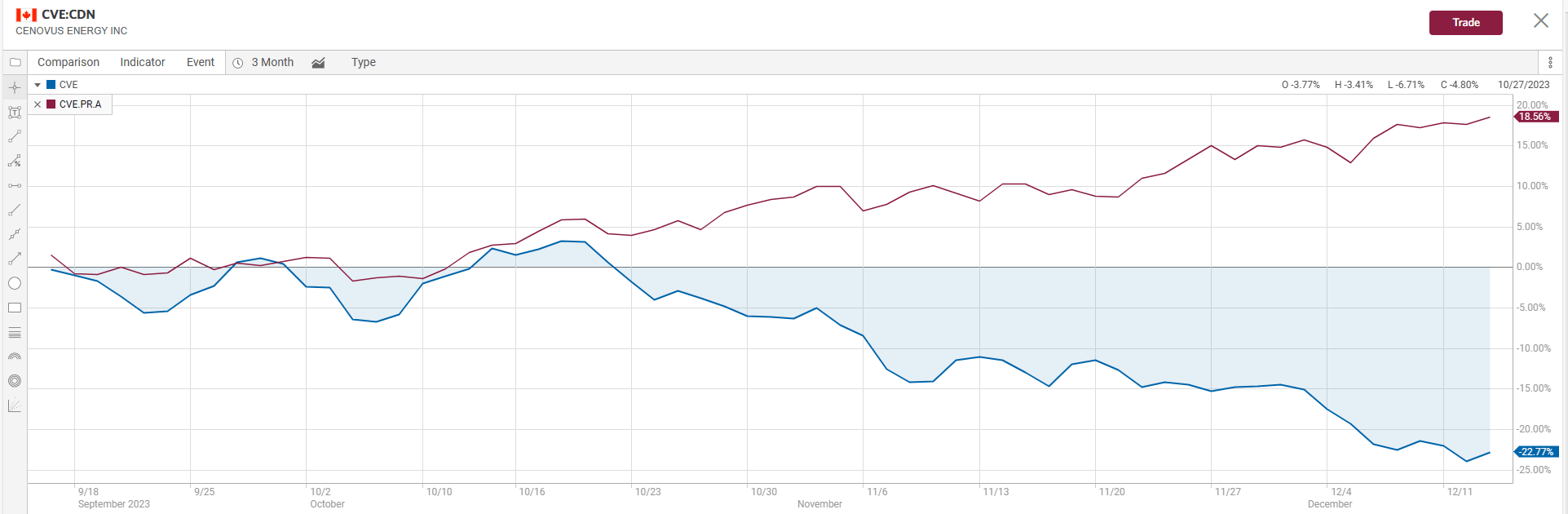

This has been a fairly unusual ride with CVE down since then and CVE.PR.A delivering some solid returns. In fact, over the last 3 months (not since our last article), the two have acted like mirror images of each other.

{kind=link}

We update our outlook for the common and preferred shares today and also weigh in on the outstanding warrants.

Why Common Shares Have Underperformed

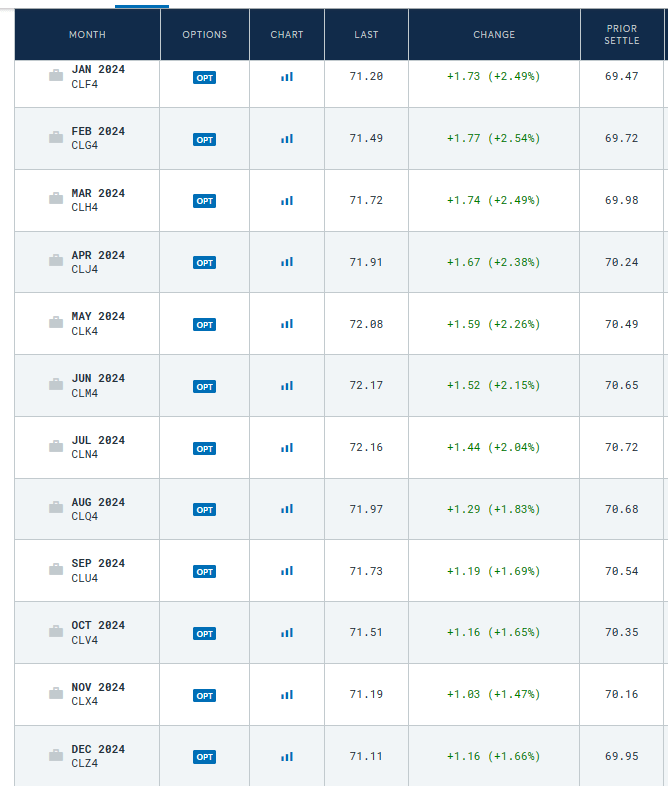

CVE has had a tough time in the back half of 2023. Investment returns tend to move a lot relative to what is priced in, and the company has had three separate punches to the face. The first was the delay in the timeline to reach the net debt target due to cash tax payments. This only delayed things by about two quarters, but in a world where everyone is focused on 1-minute charts, this can seem like an eternity. CVE is delivering cash payouts to shareholders at a fairly impressive clip, but that "100% of free cash flow payout" will have to wait. The second punch has come from oil prices, as they have really dropped since the third quarter spike. The entire 12-month forward strip averaged close to $70 yesterday. We are adding a bit on to that this morning, but there is no question that this is far below where analysts are pricing things.

{kind=link}

The average Canadian side estimate is based on West Texas Intermediate close to $80 USD/barrel. There is a pretty huge difference between $80 USD and $70 USD when it comes to free cash flow and that might not be immediately apparent. We can work this out in 4 steps.

1) All other things being equal, your revenues drop about 12.5% if oil prices are at $70 USD.

2) But since operating costs stay steady, your cash flow drops by about 20%.

3) The free cash flow, which is after capex (which again stays constant), would drop close to 35%.

4) The free cash flow after dividends, the base would drop by over 50%.

So while the company is still gushing cash, these oil price movements can have a noticeable impact on that gusher. Bulls tend to dismiss this as small and irrelevant, but 50% drops in certain metrics are hardly irrelevant.

The final aspect is the Western Canadian Select, or WCS, differential to light oil. This has been quite wide this year, and it has put additional pressure on the cash flow. This part of the pain looks past its peak, but CVE is missing estimates thanks to this headwind.

Outlook

CVE has delivered solid cash to common shareholders as of Q3-2023 via share repurchases and base dividends. The recently released budget was likely a slight disappointment, with capex coming in line with their previous guidance of $4.75 billion (midpoint) but production trailing estimates by about 1% for 2024. Valuation is compelling here for two reasons in our view. The first is that these oil prices are likely closer to the trough than at mid-cycle levels. Higher oil prices should help narrow the gap with estimates. The second is that the wide WCS differential is beginning to narrow. TMX is due to start up in Q2-2024 and line-fill will begin around February-March. The stock is cheap today and we are maintaining our buy rating. We have a $20 USD ($27 CAD) price target in one year. Risks remain that we have a severe recession that creates a $60 USD oil price. CVE remains well-positioned to deal with such a scenario, but the upside will definitely not materialize if that happens.

Outlook On CVE.PR.A

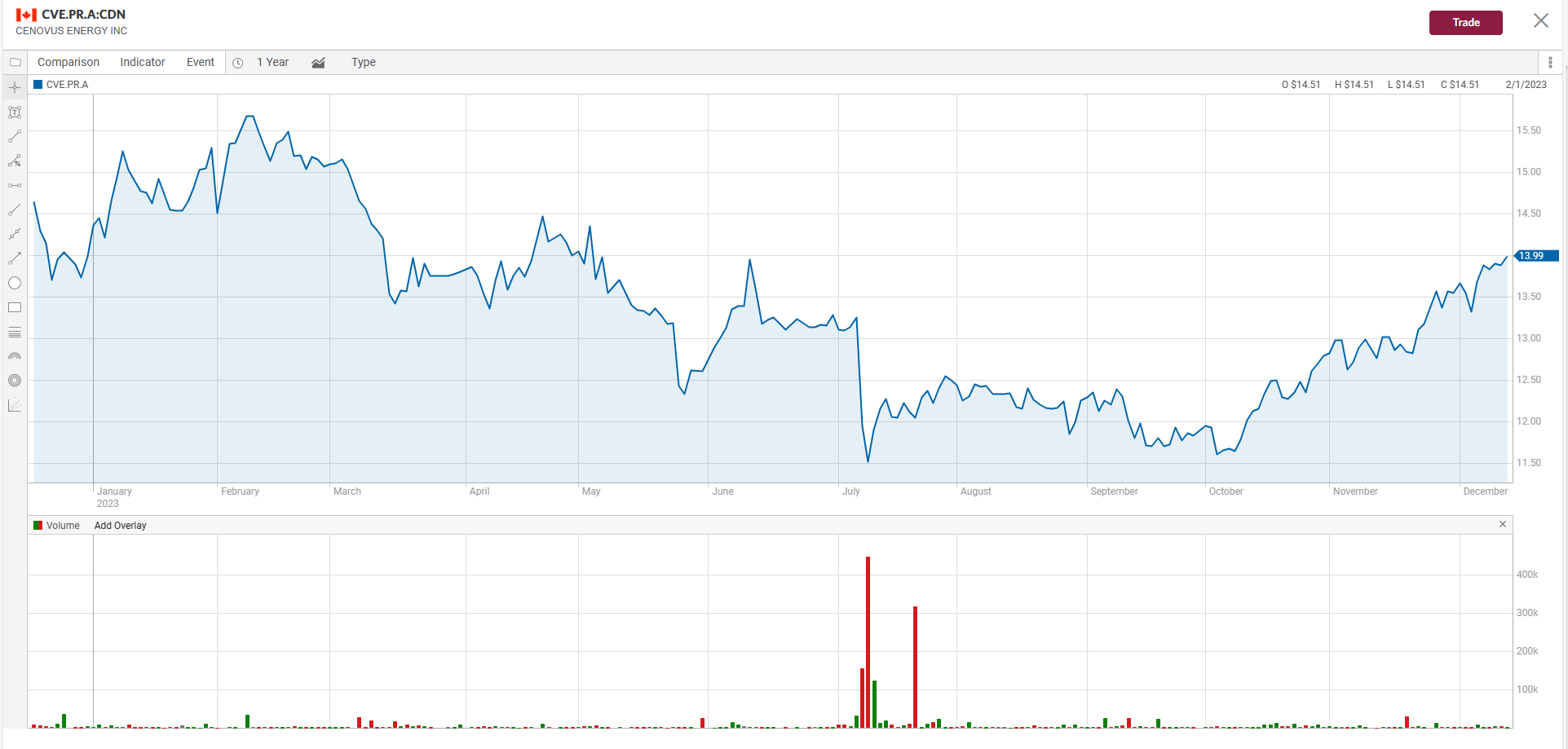

Unfortunately, the recent rally out of CVE.PR.A has gotten it close to fully valued. When we bought it in July, there was a very motivated seller who really did not seem to care what the impact to the price was. Try and see if you can find which period we are referring to in the chart below.

{kind=link}

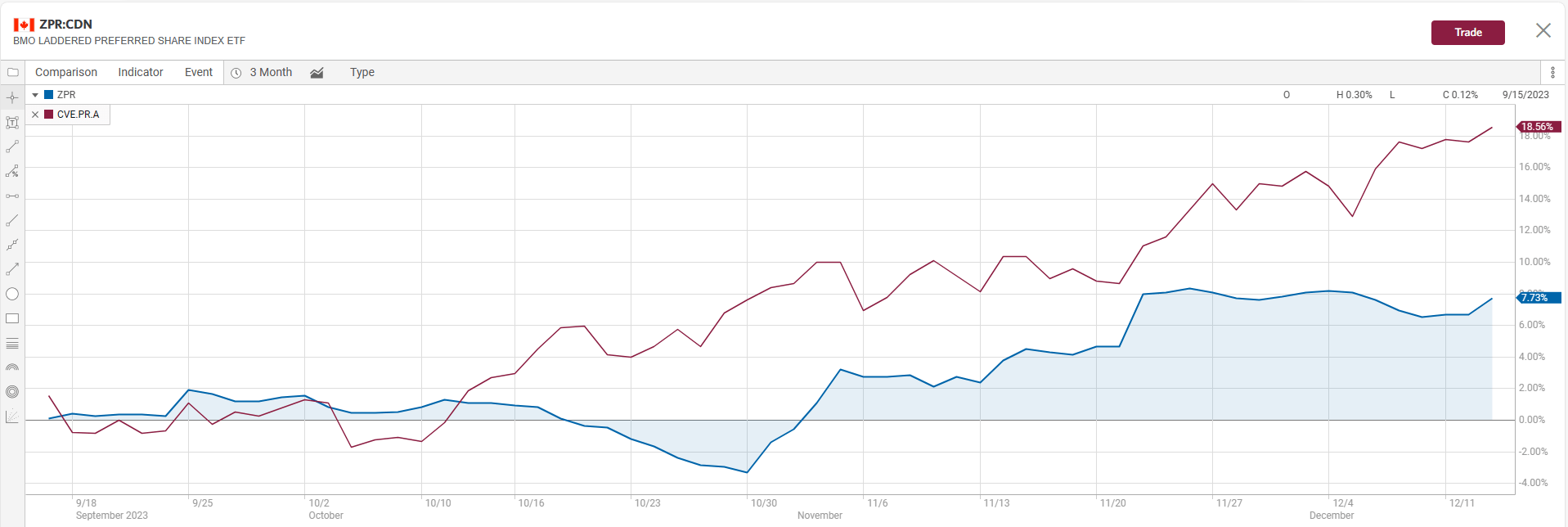

That was a great entry point and we issued an alert for our subscribers. Since then CVE.PR.A has done really well. While it has beaten the CVE common shares senselessly, it has also done far better than the BMO Laddered Preferred Share Index ETF ( ZPR:CA ).

{kind=link}

With the price at $13.98, we decided to exit. The trade delivered 20.5% total returns since our entry, at close to a 45% annualized clip. There are better opportunities in Canadian preferred space and the recent bond market volatility only improves our odds of finding fresh meat.

Cenovus Energy Inc. WT EXP 010126 ( CVE.WT:CA )

CVE's warrants were in the news in July as CVE repurchased the vast majority of these.

Cenovus Energy Inc. has reached separate agreements with each of Hutchison Whampoa Europe Investments (HWEI) and L.F. Investments (LFI) to purchase for cancellation all of the warrants held by HWEI and LFI, respectively, representing an aggregate of 45,484,672 warrants, for $711 million in the aggregate (the Warrant Repurchase Transactions). As part of Cenovus's combination with Husky Energy Inc., each Husky shareholder received 0.7845 of a Cenovus common share plus 0.0651 of a Cenovus common share purchase warrant in exchange for each Husky common share, with each whole warrant having an exercise price of $6.54 per common share, expiring January 1, 2026.

The price to be paid for each warrant pursuant to each Warrant Repurchase Transaction represents a price of $22.18 per common share, less the warrant exercise price of $6.54 per common share. The warrants will be cancelled at close, which is expected to occur later today. The company has negotiated payment terms that provide flexibility to work within its shareholder returns framework, with no expected impact to Cenovus's ability to achieve its $4.0 billion net debt target. At its discretion, Cenovus has the option to pay the aggregate warrant purchase price of $711 million for the combined Warrant Repurchase Transactions through the remainder of 2023, within each quarter's excess free funds flow, with full payment being made no later than January 5, 2024.

The 45,484,672 warrants cancelled as part of the Warrant Repurchase Transactions would, if exercised, represent approximately 2.4% of Cenovus's total common shares outstanding. This transaction represents a repurchase of 84.1% of the warrants that remain outstanding. HWEI and LFI will continue to own 316,927,051 common shares (16.7%) and 231,194,699 common shares (12.2%), respectively, of Cenovus's issued and outstanding common shares.

Source: CVE

These warrants continue to trade on TSX, but rather thinly. The average volume is just 6800 units. The strike as mentioned above is $6.54, so they are extremely deep in the money considering that CVE is trading in Canadian Dollars. From a buyer's perspective, these will add some leverage to your return profile, but they will also avoid the dividends paid on the common shares until then. These are best avoided. Warrants tend to have value when they represent out of the money strikes and have many years to expiration. In this case, these warrants started off like that but now the January 2026 expiration is relatively close. There are also standard options on CVE for January 2026, on both NYSE and TSX. So there is little appeal here for purchasing these, even if you desired leverage on CVE.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Cenovus: Three Headwinds Explain The Underperformance