CA - Centamin: Another Solid Quarter At Sukari

2023-08-29 12:22:56 ET

Summary

- Centamin's Q2 reported increased gold production and lower costs year-over-year, leading to higher margins and free cash flow.

- Meanwhile, the company's Doropo project in Cote d'Ivoire has shown strong economics and could contribute to significant production growth post-2027.

- In this update, we'll look at the Q2 results and recent developments to see whether there's enough margin of safety to make CELTF a buy at current levels.

Just over ten weeks ago, I wrote on Centamin ( OTCPK:CELTF ), noting that given the operational momentum that would push margins higher, the stock looked like a Buy at US$1.03 or lower. Since tagging this level in early mid-August, Centamin has rallied 11% off its lows, outperforming the Gold Miners Index ( GDX ) month-to-date with the worst of its correction appearing to be complete. This immediate upside reversal from the stock's lows can be attributed to the stock finally becoming more attractive from a valuation standpoint and the company's robust Q2 financial results, highlighted by ~70% higher margins on a year-over-year basis. Just as importantly, Centamin delivered a solid updated study from Doropo with the project boasting impressive economics even at conservative gold price assumptions. In this update, we'll look at the Q2 results and recent developments and see where the stock's updated low-risk buy zone sits.

{kind=link}

Sukari Mineralization - Company Website

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

Centamin released its Q2 results last month, reporting quarterly gold production of ~114,700 ounces, a ~3% increase from the year-ago period. The Sukari Mine's (Egypt) higher output on a year-over-year basis was related to increased throughput of ~3.08 million tonnes, which more than offset the lower grades processed of 1.26 grams per tonne of gold vs. 1.36 grams per tonne in the year-ago period. However, the real outperformance was from a cost standpoint, which we'll look at in more detail later, with cash costs dropping over 11% year-over-year, bucking the trend of sector-wide cost increases. Meanwhile, the company saw progress on several fronts, with its underground paste fill plant beginning commissioning in Q2 with positive results and trial stopes being in historically mined areas as to not disrupt underground mine production in H2.

{kind=link}

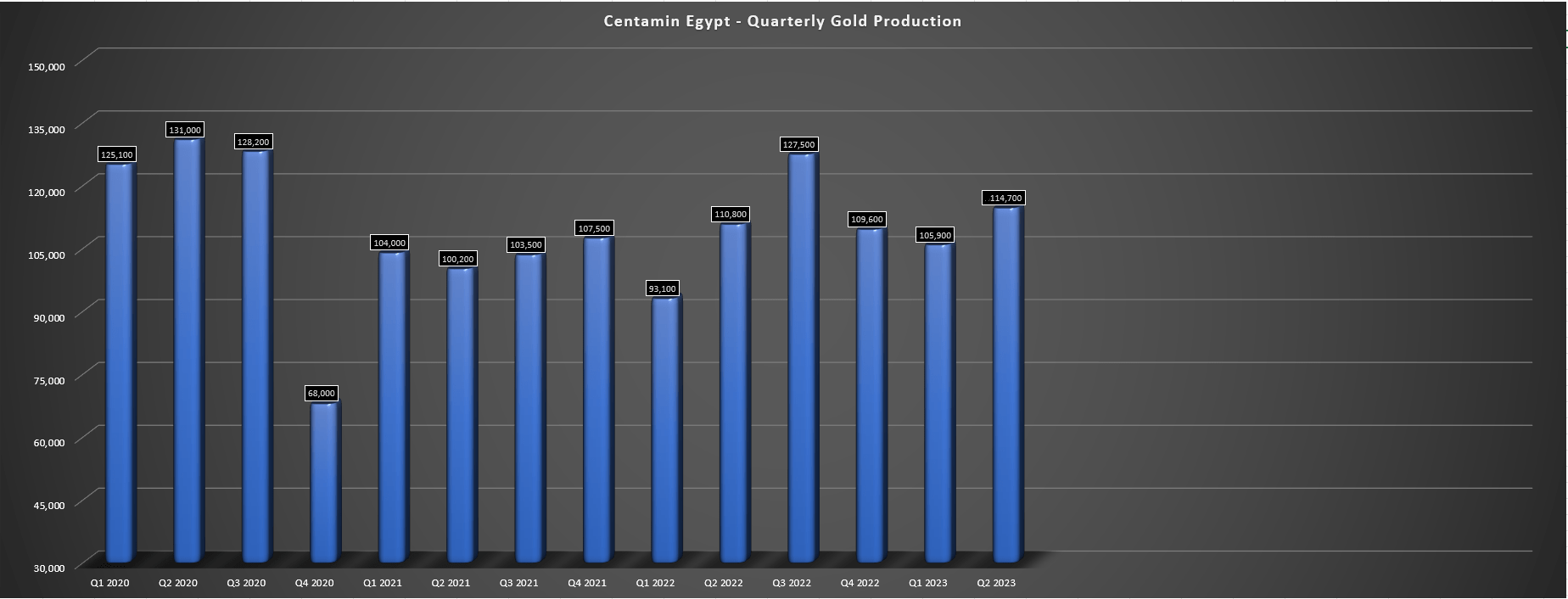

Centamin - Quarterly Gold Production - Company Filings, Author's Chart

Looking at the production results in a little more detail above, we can see that this was one of the best quarters for Sukari in years following the detection of movement in a localized area of waste material in Q4 2020 that resulted in a change to the mine plan. In fact, this was the second best quarter since Q4 2020 and this was ahead of a significant ramp up in tonnes mined underground that is expected to contribute to higher grades and production at Sukari, with a steady state of ~1.5 million tonnes per annum expected in 2025. And as the charts below highlight, Centamin is not only benefiting from lower unit costs after its shift to owner mining, but it's also seen a considerable increase in total material and ore tonnes mined, with nearly 700,000 tonnes of material mined in H1 2023, and just shy of 500,000 tonnes of ore mined from underground (Q2 2023: ~222,000 tonnes at 4.4 grams per tonne of gold).

{kind=link}

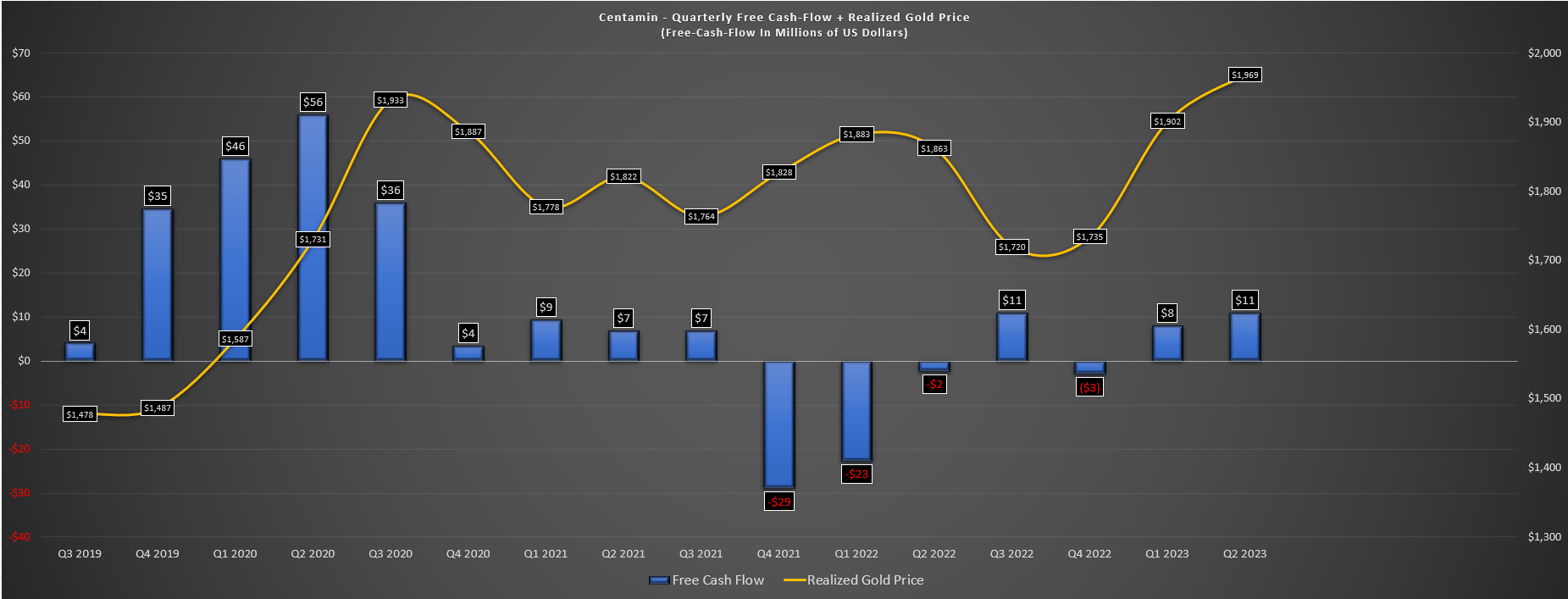

Centamin - Quarterly Free Cash Flow & Average Realized Gold Price - Company Filings, Author's Chart

Given this solid operating performance, H1 2023 production is sitting at ~221,000 ounces, tracking well to deliver towards its FY2023 guidance midpoint of 465,000 ounces. Plus, the higher realized gold price certainly provided a boost from a financial standpoint, with Centamin reporting 6% higher revenue year-over-year in Q2 ($220.4 million vs. $207.2 million), and 11% higher sales on a half-year basis vs. H1 2022 (~$425.6 million vs. ~$381.8 million). This sharp increase in revenue combined with exceptional cost control allowed Centamin to generate ~$21.9 million in free cash flow in H1 2023, up from a cash outflow of $25.0 million in the year-ago period. In addition, the company exited the quarter with ~$161 million in cash and ~$311 million in liquidity (undrawn $150 million RCF), with ample room to fund its Doropo Project when combined with cash flow generation if it green-lights the asset (assuming timely receipt of permits).

Costs & Margins

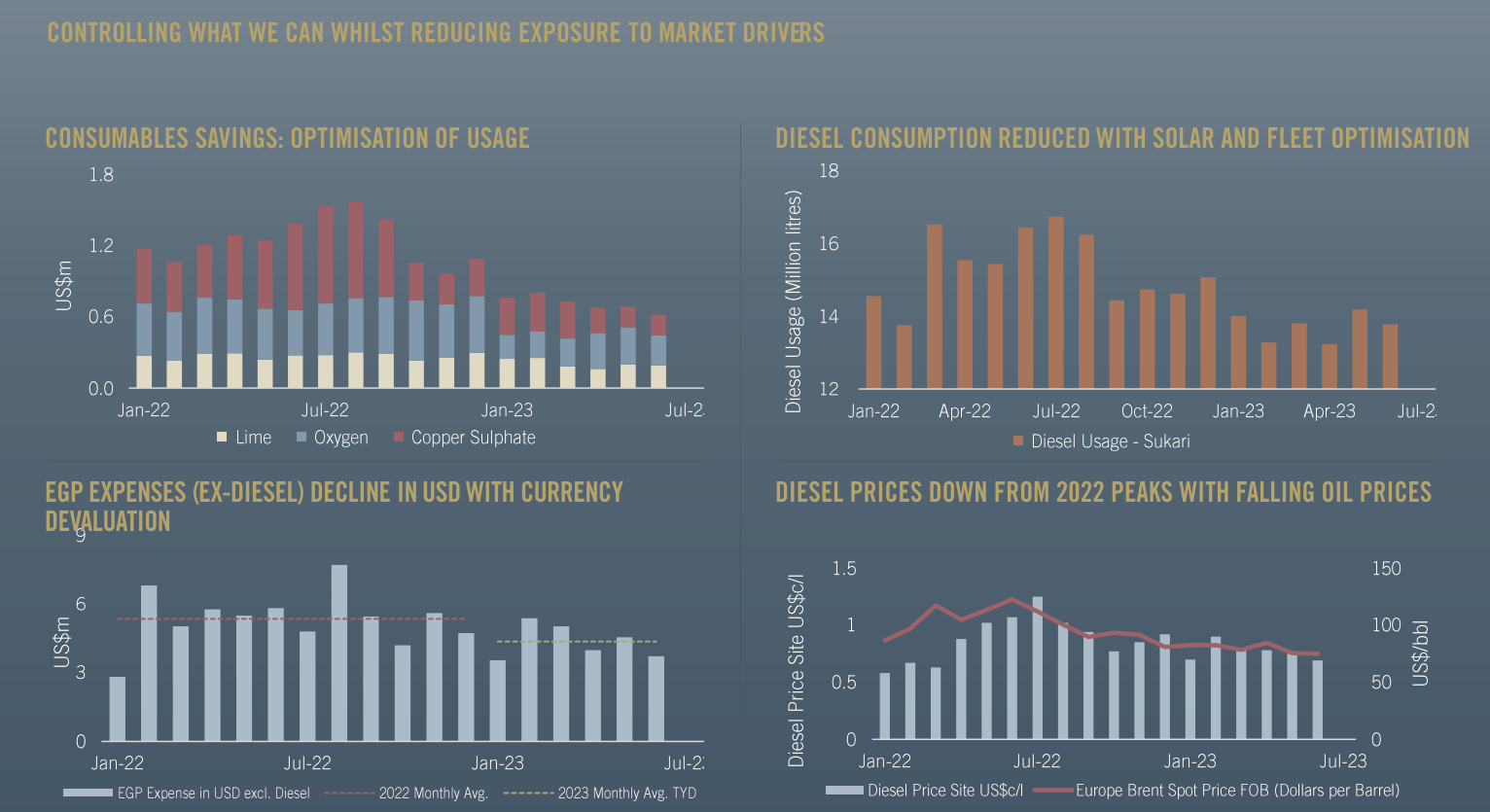

Looking at Centamin's costs and margins, the company knocked it out of the park, with Q2 cash costs of $767/oz and all-in sustaining costs [AISC] of $1,113/oz, translating to declines of ~11% and ~18% on a year-over-year basis. Not only did this buck the sector-wide trend of rising costs we've seen from most producers, but Centamin's all-in sustaining costs came in well below the industry average (Q2 estimates: $1,360/oz), benefiting from lower sustaining capital, depreciation in its local currency, and optimization work that has helped to tighten up costs at its Sukari Mine. One major win has been its newly commissioned 30MW solar plant exceeding project power expectations, with ~100,000 liters of fuel savings per day during peak sunlight hours and savings of ~$1.3 million per month on an annualized basis at current prices. These significant savings have led Centamin to look at preliminary work on an expansion to 50MW, which could be achieved for less than $30 million.

{kind=link}

Sukari Mine Cost Performance - Company Website

Looking at the chart above, we can see that displacing diesel with solar has not been the only win, with the company also reporting significant savings on consumables (lime, oxygen, copper sulphate) through optimized usage and fleet optimization. Elsewhere, the company has benefited from a decline in diesel prices which are down from peak levels. However, while this cost performance was impressive, it's important to note that the company hopes to have a grid connection for Sukari to add further low-cost power in 2024 (tender process began in Q1 2023) and a further increase in its solar plant could lead to additional savings. So, with the benefit of economies of scale underground and productivity gains (use of portals from the base of Sukari Pit), a grid connection and a further decline in diesel consumption if it expands its solar plant, the company is well on its way to trouncing its $150 million cost savings program, and enjoying even lower costs post-2025.

{kind=link}

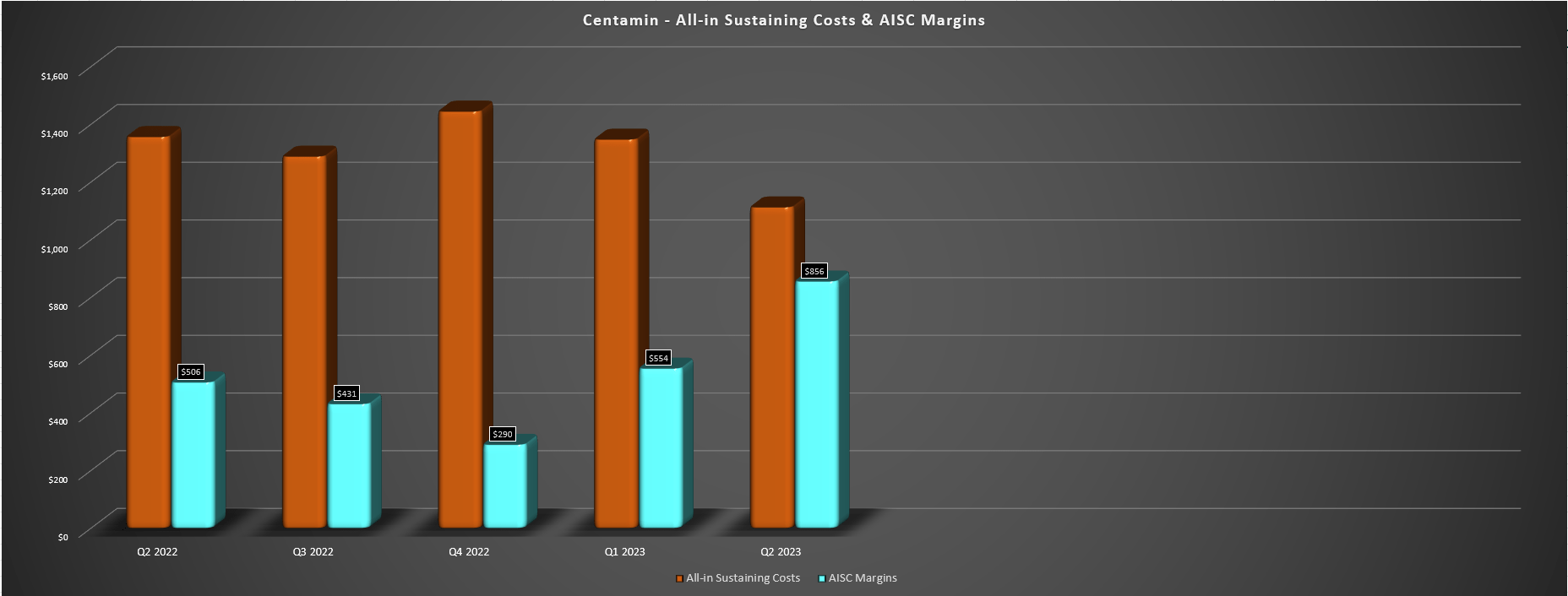

Centamin - Quarterly AISC & AISC Margins - Company Filings, Author's Chart

Finally, looking at margins, Centamin's AISC improved to $856/oz in Q2 2023, above the industry average and sitting at a multi-year high. This was helped by the record average realized gold price of $1,969/oz (beating previous record of $1,933/oz in Q3 2020), and the solid cost control in a tough environment for most producers. That said, the company will see higher capital expenditures in the second half of the year, meaning that while H1 2023 was very impressive from a cost and financial standpoint, we should see some pullback in margins and free cash flow in H2 2023.

Recent Developments

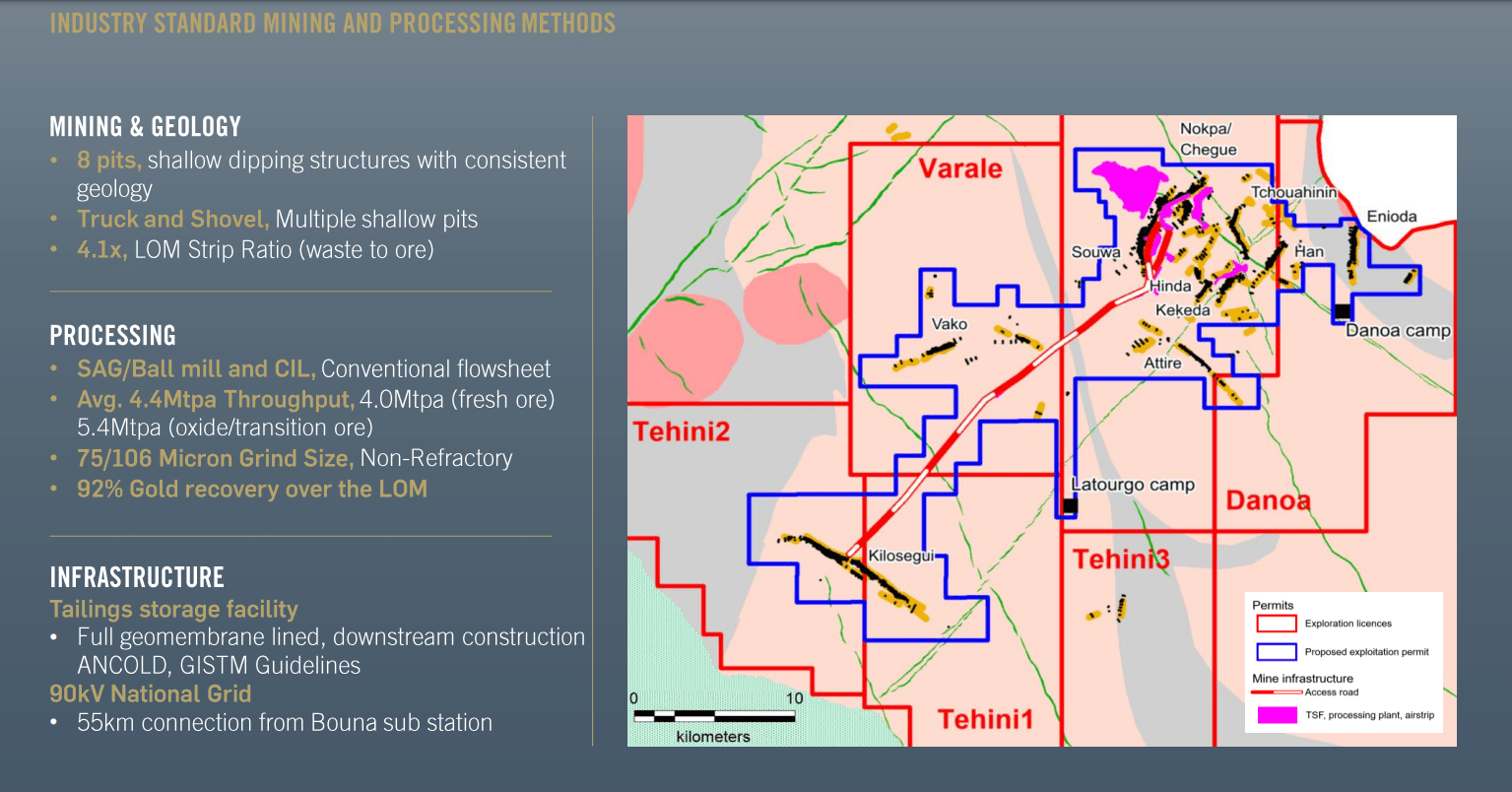

As for recent developments, the major one was the updated Pre-Feasibility Study at Doropo in Cote d'Ivoire (DFS expected in H1 2024), with this envisioning a multi-pit operation with a CIL plant, with average annual throughput of ~4.4 million tonnes per annum. Assuming 92% gold recoveries, Centamin expects annual gold production of ~210,000 ounces for the first five years (~173,000 ounces over the life of mine), with industry-leading AISC of $963/oz (first five years) and sub $1,020/oz over the mine life. Notably, upfront capex is very reasonable at $349 million and the project boasts an After-Tax NPV (6%) of $486 million at a conservative $1,800/oz gold price. So, assuming Centamin was to go ahead with the project and necessary permits were granted, Centamin's production profile could improve to 650,000+ ounces (~30% growth) at sub $1,200/oz company-wide with no need for share dilution to fund this growth (translating to meaningful production per share growth).

{kind=link}

Doropo Project - Company Website

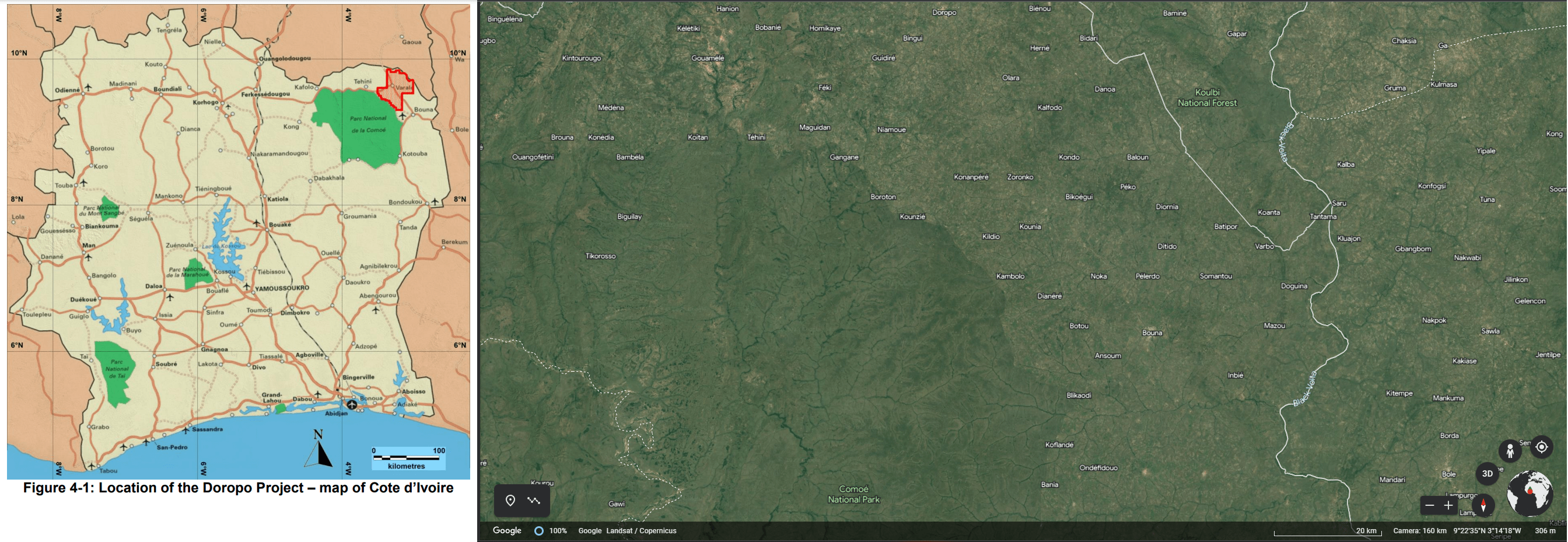

As highlighted in the map below, Doropo lies ~50 kilometers north of Bouna, and is sandwiched between the Comoe National Park on the south and the Burkina Faso border to the north. The proximity to a national park could make it a little trickier to permit relative to more remote projects, and I think a safer bet on first production is 2028 to account for a lengthier permitting process. That said, the project does benefit from being relatively simple from a technical complexity standpoint and there is the ability to focus on a smaller footprint to start due to the multi-pit design. Plus, Centamin's CEO noted that things appear to be progressing well in regards to support for the project:

"We actually met the Minister of Mines [indiscernible] a couple of weeks back. He was very supportive of the Doropo project. It is a rural relatively underdeveloped part of Cote d'Ivoire, and the government is very keen to see investment in this part of the world, infrastructure development, job creation skills and so on. And he did indicate that this was a priority project for them as well. So delighted to get that sort of in-country support for the project as well".

- Centamin Egypt, Q2 2023 Conference Call

{kind=link}

Doropo Project, Bouna & Comoe National Park - Google Earth, 2019 TR

Finally, as for the company's exploration on its three Eastern Desert Exploration [EDX] blocks in Egypt, Centamin has announced that the framework for a model mining exploitation agreement [MMEA] with the Egyptian Ministry of Petroleum & Natural Resources and the Egyptian Mineral Resources Authority [EMRA] is quite favorable. The terms include a 5% government net smelter royalty on revenue, a 22.5% corporate tax rate, and a 15% government financial net profit interest (post-tax income), as well a 0.50% community development contribution and commitments toward local employment, training and procurement. So, with this agreement in place and terms for future mining de-risked, Centamin can now ramp up exploration on its multiple targets which could increase Sukari's production profile and life of mine when it comes to regional targets and the ability to truck ore from satellite operations, a very positive development for the company.

Summary

Centamin had a solid Q2 report and while H2 2023 is likely to be softer especially if gold price weakness persists, the company is in excellent financial shape and has a bright future with a path to becoming a multi-asset producer by 2028. As for valuation, I see a fair value for Centamin of ~$1.80 billion, which assigns $300 million to exploration upside, ~$440 million to Doropo ($1,750/oz gold, 6% discount rate), and ~$900 million to Sukari, translating to a fair value of US$1.55 when including net cash. This points to 34% upside from current levels, but I am looking for a minimum 35% discount to fair value to justify starting new positions in single-asset producers. After applying this point, we arrive at an ideal buy zone of $1.01 or lower, suggesting that while Centamin offers a reasonable margin of safety, it isn't in a low-risk buy zone currently. So, with some gold producers trading within low-risk buy zones at deep discounts to fair value, I continue to see better value elsewhere.

That said, if we were to see Centamin pull back to US$1.01 or lower before year-end, I would strongly consider starting a new position in the stock.

For further details see:

Centamin: Another Solid Quarter At Sukari