CA - Centerra Gold: A Better H2 On Deck

2023-09-19 16:48:32 ET

Summary

- Centerra Gold had a tough H1, wading through a transition zone that impacted recoveries at Mount Milligan and limited production from Oksut.

- Fortunately, H2 is expected to be much better, with Oksut ramping up and better grades expected at its flagship BC asset.

- However, Centerra threw a curveball with it noting that it's looking at a potential restart of Thompson Creek, which I previously saw as non-core and likely for sale.

- In this update, we'll look at the recent results, whether the stock offers a margin of safety, and why this could make it much less relevant as a gold producer with sharply declining production at Oksut post-2024.

Just over two years ago, I wrote on Centerra Gold ( CGAU ), noting that while the company was enjoying strong free cash flow, the stock didn't fit my risk profile given that too much of its production and cash flow was coming from the Kyrgyz Republic. This suggested an elevated risk to owning the stock if we were to see any negative developments out of Kumtor (a recent Nationalist Politician, Satyr Japarov, had won an election in January 2021), and Centerra was dealt one in the worst way in 2021, with the mine being nationalized. Since the March 2021 article, Centerra has massively underperformed, down 43% vs. a 5% decline for the Gold Miners Index ( GDX ). The underperformance is not surprising when its free cash flow and production has fallen off a cliff, even if the share count has been reduced substantially (Kyrgyzaltyn shares cancelled).

Since then, Centerra has continued to maintain one of the strongest balance sheets sector-wide, but it's been a tough past year, with production at Oksut down sharply while it awaited an updated EIA (since granted), and a tough H1 at Mount Milligan because of material handling issues and lower grades and recoveries in the ore-waste transition zone. Fortunately, production is expected to improve significantly in H2 for its flagship asset (completion of mining in transition zone) and Oksut is back online, with the ramp of its crushing, stacking and ADR facility underway. In this update, we'll look at recent developments and whether the stock looks to be on the sale rack, trading ~40% off its 2022 highs.

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Production & Sales

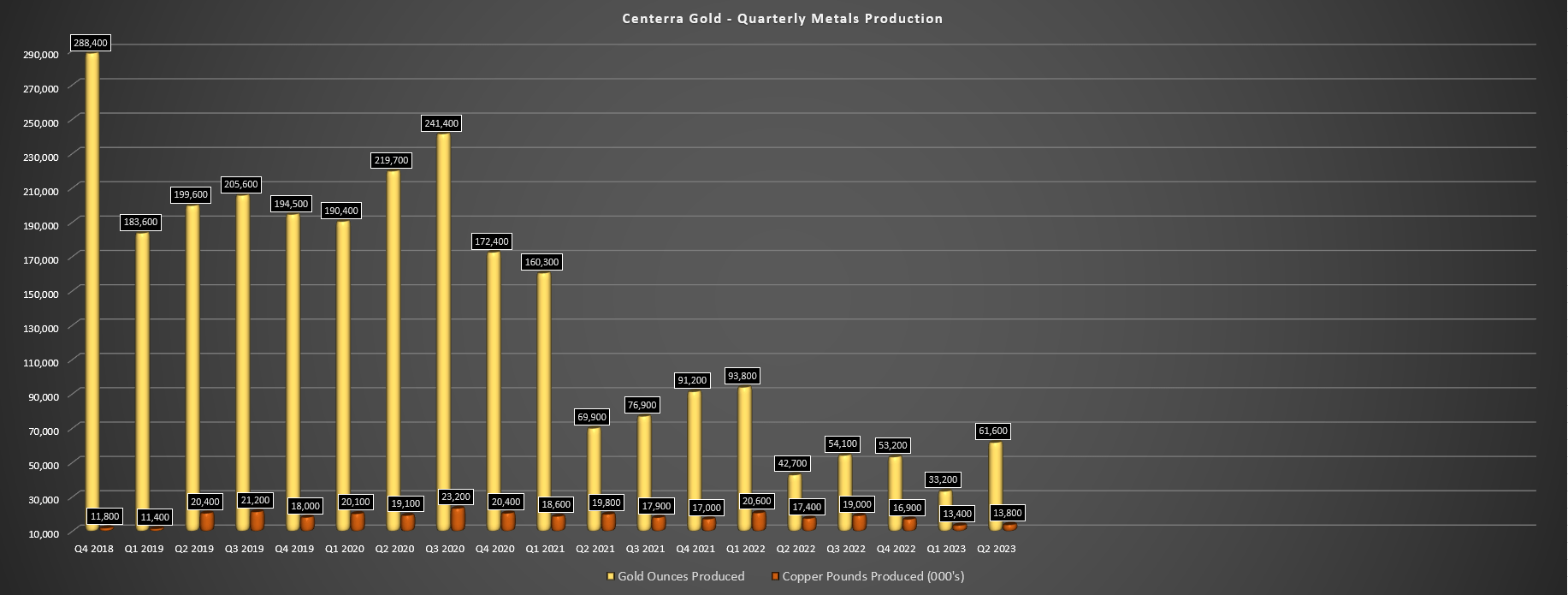

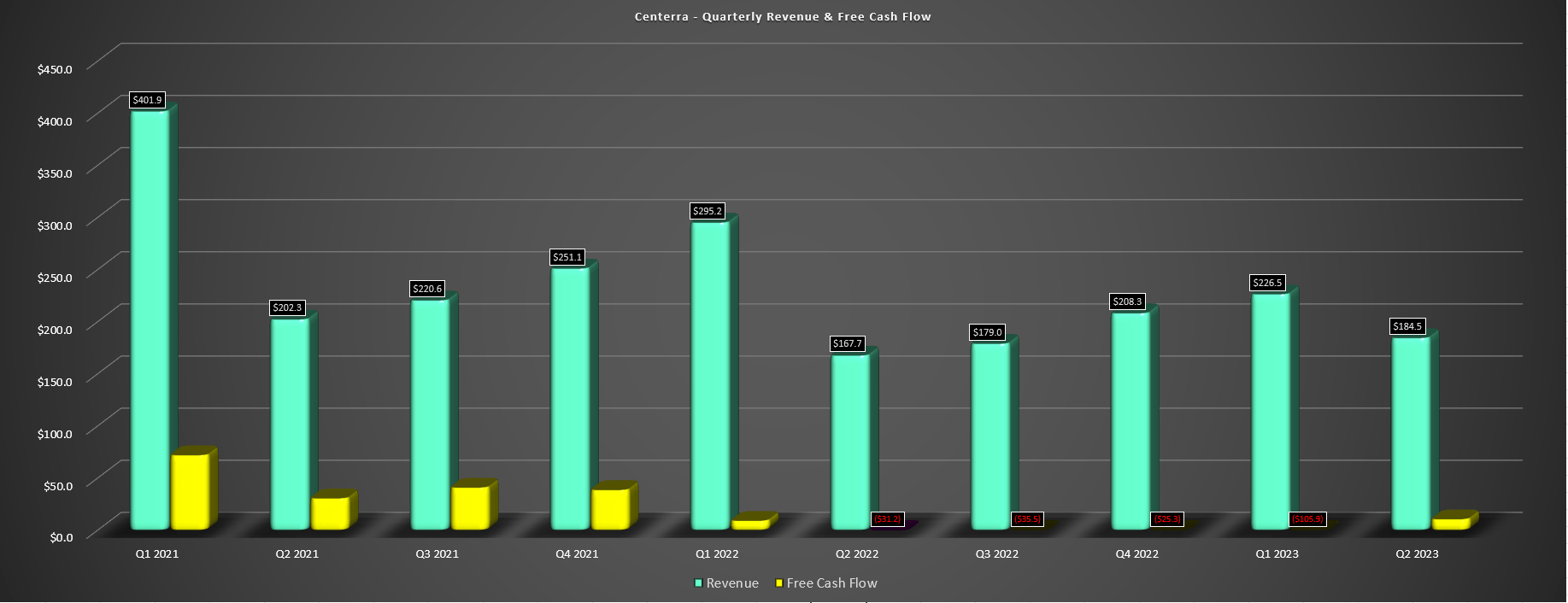

Centerra Gold had another tough quarter in Q2 2023, which may not have been clear from the headlines given that it reported 44% higher gold production. However, the company was up against easy year-over-year comparisons with no production from Oksut (gold room operations at ADR plant were suspended in March 2022), and a weaker quarter from Mount Milligan (~42,700 ounces of gold, ~17,400 million pounds of copper) due to lower gold and copper head grades. Meanwhile, revenue was up to ~$184.5 million (Q2 2022: $167.7 million), but this was because of having two assets contributing (Molybdenum Business Unit [MBU] and Mount Milligan) while Oksut production was halted. Fortunately, Centerra reported positive free cash flow in the period of $10.6 million, with Oksut contributing again, offsetting a mediocre quarter at Mount Milligan as it waded through the ore-waste transition zone that has negatively affected grades and recoveries.

Centerra Gold - Quarterly Metals Production - Company Filings, Author's Chart

{kind=link}

On a positive note, Mount Milligan's production will increase materially in H2, with the low end of guidance (160,000 ounces) at Mount Milligan implying production of 85,000+ ounces in H2 of this year. Meanwhile, Oksut will also be a much larger contributor in H2, providing a boost to free cash flow vs. the $0.4 million reported in Q2 2023 (~20,500 ounces produced in Q2 at $1,143/oz). And as noted by Centerra, crushing and stacking activities restarted in late Q2, with a balance of ~80,000 ounces in stored gold-in-carbon inventory and another 20,000 in ADR inventory. This is in addition to an additional ~200,000 in ore stockpiles and on the heap leach pad, setting this asset up for a meaningful catch-up now that the updated EIA is in hand and it can begin processing the material it's been mining. Finally, at its MBU, sales were 6% lower at ~3.0 million pounds of molybdenum, but this was offset by higher realized molybdenum prices, with revenue up 11% year-over-year ($76.1 million).

Centerra - Quarterly Revenue & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

As for the company's consolidated financial results, revenue increased to $184.5 million, free cash flow came in at $10.6 million, and the company ended the quarter with over $400 million in cash, giving it one of the strongest balance sheets sector-wide. This balance sheet flexibility prompted the company to repurchase ~1.27 million shares at US$5.76 as part of a much larger buyback program. That said, and while the strong cash balance is a positive, we can see the damage caused by not diversifying and having so much reliance on Kumtor, with revenue down over 50% from Q1 2021 levels and free cash flow down ~85%.

Costs & Margins

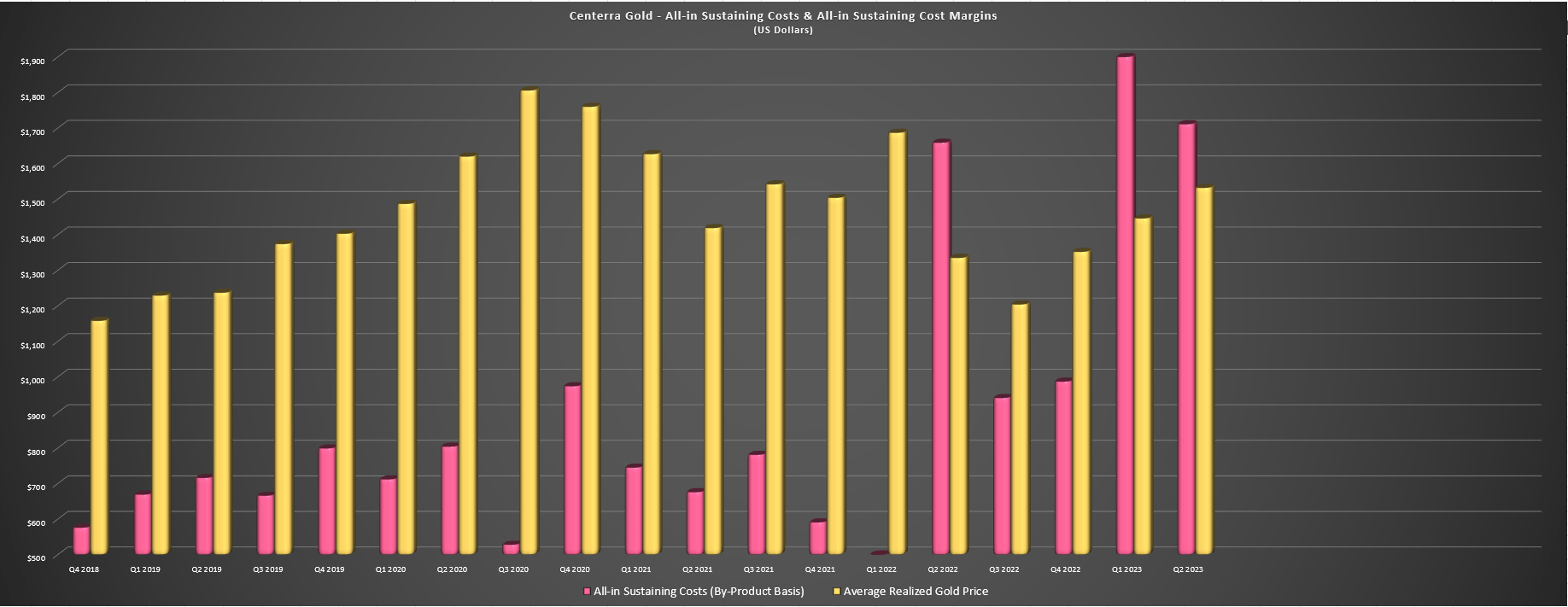

Moving over to costs and margins, Centerra reported all-in sustaining costs of $1,711/oz on a by-product basis, up from the $1,660/oz reported in the year-ago period. However, the quarter didn't benefit from the lower cost Oksut Mine with a further impact from lower production/sales at Mount Milligan. So, with a return to more normal grades and recoveries in H2 and a ramp-up in production at Oksut, we should see a significant decline in H2 consolidated AISC, which is implied by the company's FY2023 guidance of $1,000/oz to $1,050/oz despite year-to-date AISC coming in above $1,500/oz. That said, the company did note that it is seeing higher costs for maintenance and general inflation on labor and consumables. And while it benefited from lower energy prices in H1, this could be a minor drag in H2 with the rebound in oil prices.

Centerra Gold - AISC & AISC Margins - Company Filings, Author's Chart

{kind=link}

As for Centerra's margins, we've seen a dramatic increase in its margin profile despite the lower gold price, with the company no longer benefiting from a ~550,000 ounce operation with sub $750/oz AISC in Kumtor, which also improved its average realized gold price with a higher proportion of ounces not being sold into streams (Mount Milligan: 35% gold stream at $435/oz). At the same time, it hasn't helped that the company had lower production from Oksut and Mount Milligan, with its costs divided over a lower denominator. The result was that AISC margins were pinched again in Q2 2023 to [-] $179/oz, albeit a little better than the [-] $324/oz margins in Q2 2022. While these margins might appear concerning, it's important to note that they do not reflect the overall business, with Oksut barely contributing and having consistent ~$900/oz AISC margins (2024-2027), and Mount Milligan underperforming in the ore/waste transition zone and getting little help from the copper price.

Let's take a look at recent developments which are more important to the overall investment thesis:

Recent Developments

As highlighted in Centerra's recent update, it is taking a closer look at its Thompson Creek Mine in Idaho, which is one of the largest open-pit primary molybdenum mines globally that has been in care and maintenance since 2014. This mine can benefit from synergies with its Langeloth Metallurgical Facility which is operating at just one-third of capacity, and a PFS released this week suggests the potential for an 11-year mine life with average molybdenum production of 11 million pounds from Year 1 to 3, increasing to 13+ million pounds from Year 4 to 11. Even at a more conservative $20/lb moly price, this would translate to well over $200 million in revenue, with all-in sustaining costs expected to come in at $15.00 to $18.00/lb in Year 2 and 3, dropping to $12.00-$15.00/lb for the bulk of the mine life, and even lower for the mine's last three years (if restarted). The result is an After-Tax NPV (5%) of $373 million ($20/lb moly price), and an Initial Capex to NPV (5%) ratio of roughly 1:1 based on pre-production capex of $375 million.

{kind=link}

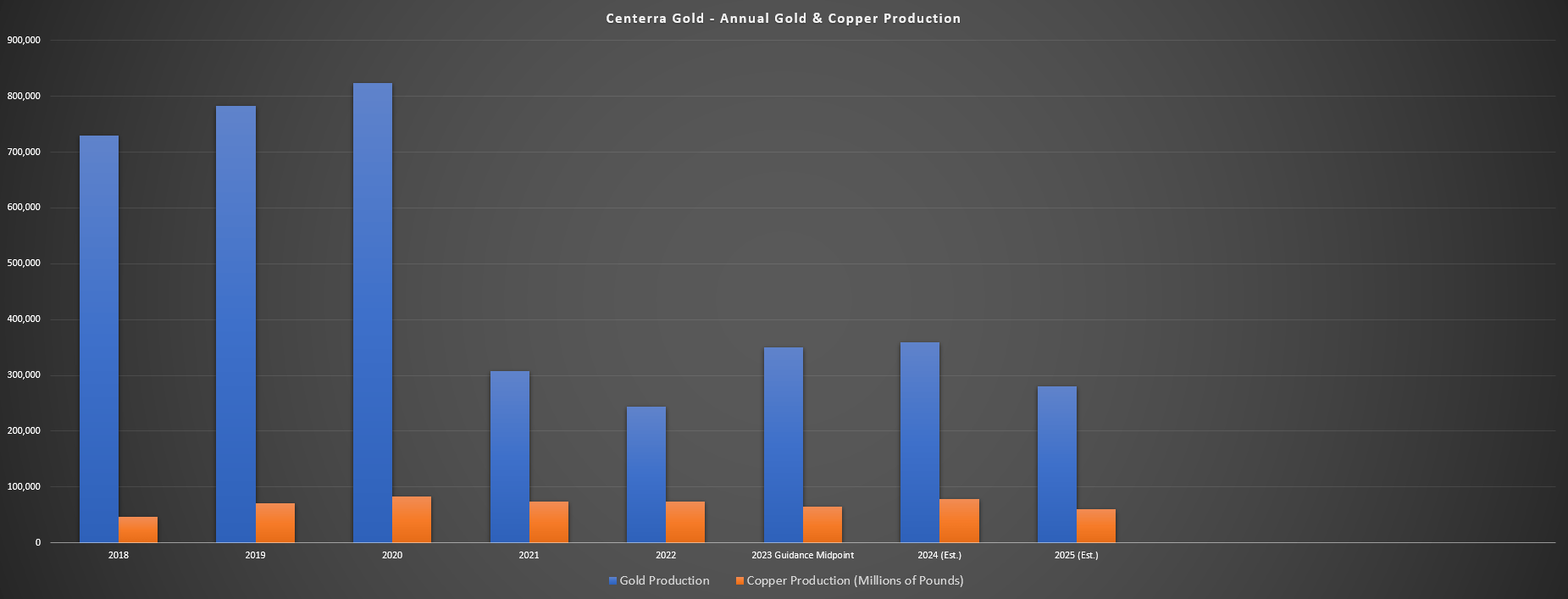

While this would be a solid contributor if restarted and it's clear there are synergies (ability to blend high-quality TC concentrate with lower-quality third party concentrates), I was previously expecting Centerra to drop the asset given its relatively high reclamation costs and package up the MBU for sale as it's been a relatively non-core asset. And as noted in the most recent Conference Call by new CEO Paul Tomory, the company intends to remain primarily a gold producer. However, if we look at the below chart and assume Thompson Creek comes online post-2025, this would certainly change the script, with gold production from Oksut and Mount Milligan combined amounting to just ~280,000 ounces in 2025 next to combined copper production of ~60 million pounds and molybdenum production upwards of 18 million pounds, with base metals making up the bulk of revenue if Thompson Creek is restarted.

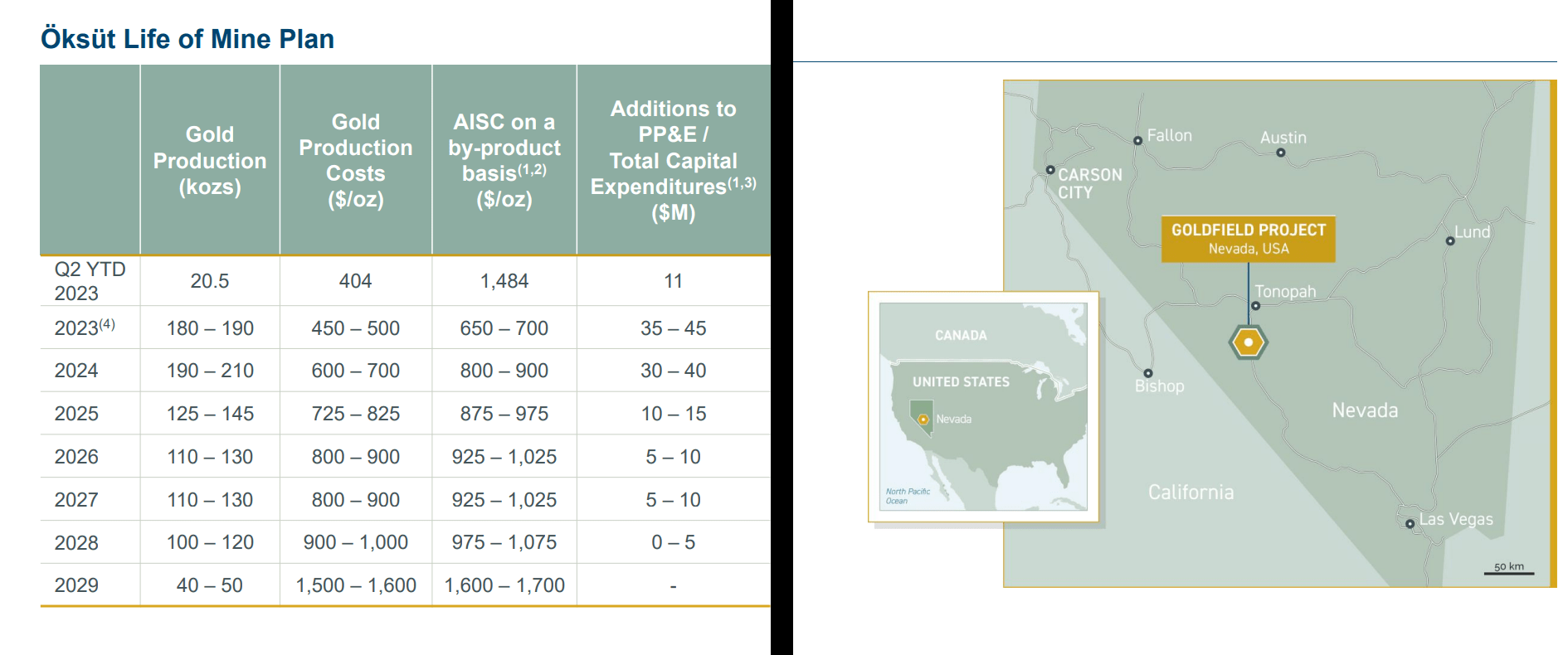

Obviously, no decision has been made yet, but the trend in gold production is clear, with a declining production profile at Mount Milligan post-2026, a sharp drop-off in gold production at Oksut post-2024, with production set to plunge from ~200,000 ounces to ~135,000 ounces in 2025 before settling at ~117,500 ounces on average from 2026 to 2028. Hence, it is getting more difficult to call Centerra a gold producer if it makes a production decision at Thompson Creek, especially with the company noting that it's taking more time on Goldfield before making a production decision. And while it's nice to see the company increasing its exploration budget at Goldfield and focusing on oxides which are much lower-capex to develop in a production scenario, I have pushed out my production estimate on Goldfield to 2028 to be conservative from 2026 previously.

Centerra Gold - Annual Gold & Copper Production - Company Filings, Author's Chart & Estimates

{kind=link}

Oksut Life of Mine Plan & Goldfield Project - Company Website

{kind=link}

Not only does this impact the company's growth profile (given that Goldfield will now simply offset Oksut, which will wind down in 2029), but it also reduces my 2026 gold production estimates which would have offset Centerra's position as somewhat of a base metal producer with just ~280,000 ounces of gold production in 2025 plus significant copper and molybdenum production (especially if it restarts Thompson Creek). And while profit is profit regardless of the metal, producers with a base metal tilt trade at lower multiples than gold producers, even if they have a substantial portion of production from Tier-1 ranked jurisdictions.

Valuation

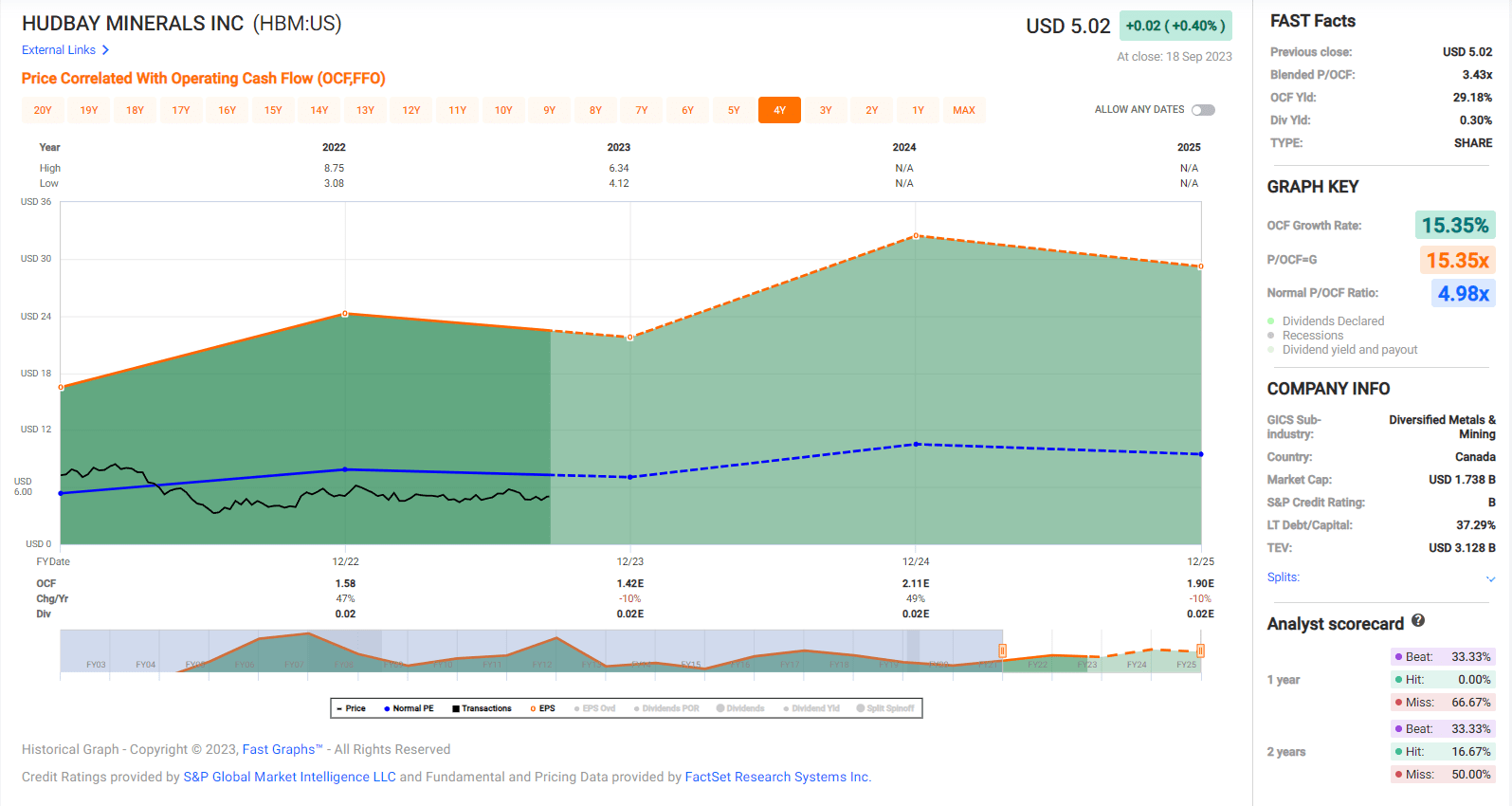

Based on ~222 million fully diluted shares and a share price of US$5.60, Centerra trades at a market cap of ~$1.24 billion and an enterprise value of ~$840 million, making Centerra one of the cheaper gold producers sector-wide. However, as noted above, small-scale copper/base metals producers tend to trade at a discount to their peer group. An example of this is New Gold ( NGD ) which consistently trades at less than 4x cash flow and Hudbay Minerals ( HBM ), a gold and copper producer in Manitoba, Peru, and British Columbia that has consistently traded below 5x cash flow the past 18 months despite also having a solid development pipeline (Copper World). Hence, with Centerra currently trading at ~4.5x FY2023 cash operating cash flow estimates (~$185 million), I don't see that much of a valuation disconnect here vs. other small-scale gold producers with a heavy base metal tilt.

Hudbay Minerals - Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

It's possible that Centerra could break this mold of lower multiples among small-scale gold/copper producers vs. its peers and the sample size is relatively small given that most smaller scale gold producers are not producing any meaningful amount of copper (and certainly not molybdenum). Still, while I see a much higher value for the stock on a sum-of-the-parts basis if it had shed its MBU and rid itself of the relatively high reclamation costs, this doesn't appear to be the direction the company is going near-term. And given this trend towards lower gold production (Goldfield pushed out, Thompson Creek in focus) and applying a more conservative cash flow multiple of 6.0x to Centerra and adding $1.80 per share in cash and $0.50 per share for Kemess (~$110 million), this translates to a fair value of US$7.50.

While this fair value estimate points to a 34% upside from current levels, I am looking for a minimum 40% discount to fair value for small-cap gold producers to justify starting new positions. In addition, I'm also looking for exceptional investment theses such as names with industry-leading growth, exceptional assets with a kicker of untapped exploration upside and ideally world-class assets. And while Oksut and Mount Milligan are solid assets, the latter is encumbered by a large stream and the former will enjoy peak production in 2024 before a sharp drop-off beginning in 2025. So, with Centerra not meeting the latter requirement (exceptional assets, considerable exploration upside or growth) and not meeting my margin of safety requirement (40% discount to estimated fair value), I see far more attractive reward/risk setups elsewhere in the sector.

Summary

Centerra's potential pivot to higher base metal production by restarting Thompson Creek may offer attractive economics, but I'm not sure that it helps from a multiple standpoint and I think an exit from the business (passing off reclamation costs) and a focus on opportunistic M&A in the gold space might have been the better move. Normally, this would not be the case, but with advanced developers and junior producers trading at their lowest multiples in years (outside of March 2020 and September 2022), this would allow Centerra to return to growth while it looks to optimize Goldfield and finally put its cash to work, all while potentially earning a multiple expansion (increased diversification, greater scale for gold business). Therefore, I'm a little surprised by the shift in focus to Thompson Creek, even if the higher molybdenum prices have certainly changed the economics here.

After applying a 40% discount to an estimated fair value of US$7.50, Centerra's ideal buy zone comes in at US$4.50 or lower to bake in an adequate margin of safety. And while there's no guarantee that the stock retreats to this level again, I prefer to get the right price or pass entirely, and especially when there are open gaps below on CGAU's chart that have a tendency to be filled ($5.20 and $4.48). In summary, while I think CGAU is reasonably valued, I don't see a clear path to a re-rating for the stock and it's tough to conclude whether this was the right move to unlock hidden value in the portfolio. Therefore, I continue to focus on what I believe to be more attractively valued names elsewhere in the sector.

For further details see:

Centerra Gold: A Better H2 On Deck