LEU - Centrus Energy: Continue Owning For Near-Term Upside But Beware Of Longer-Term Risks

2023-05-23 07:43:22 ET

Summary

- The World is in desperate need of HALEU (High Affinity Low Enriched Uranium) in order to deploy new nuclear reactors and meet 2050 climate goals.

- Centrus Energy is perceived to be the front-runner in HALEU production, and the consensus view is that Centrus will take the lion's share of what could be a $5+billion market.

- The Consensus view: DOE is providing significant incentives to accelerate domestic HALEU production. The Reality: Incentives are not fully funded and are designed to create an oversupplied market.

- Survivors in the HALEU market will need to be a low-cost producer. Centrus is unlikely to be this. In this report we analyze the competitive landscape (Urenco, ASPI, SILXF).

- I am long Centrus, because near-term news flow will likely drive share price higher. But in enrichment I prefer ASPI and in Uranium supply chain I prefer UUUU.

Editor's note: Seeking Alpha is proud to welcome Opes Sapiens as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Summary and Conclusion

I am long Centrus Energy (LEU) and I see the stock working in the near term. The perception is that this stock is the most leveraged play on HALEU and Uranium enrichment and news flow on both topics will continue to be positive and likely drive the share price higher. With the optics of a low valuation combined with positive news flow, it is easy to become bullish on the stock. It is likely that additional sell side coverage on a stock that is set to solve one of the world's greatest environmental problems will provide an additional strong tail wind. The case to be long is easy and difficult to argue against this. Being long will likely be the correct call for the next 12-24 months.

But having read many bullish reports on the stock (both on Seeking Alpha, other stock commentary websites as well as sell-side research), it is becoming increasingly obvious that most market commentators do not appreciate the risks associated with this company and this stock. The stock is likely to continue to work in the near term, as uranium news flow and HALEU news flow is likely to be supportive. But longer term, there are substantial risks relating to both its current cash generating business and the company's primary growth driver HALEU. It is highly likely that these risks are not fully understood by investors. With total liabilities standing at 37x last 12 months operating cash flow, this stock could easily be a zero, if the risks I highlight in this report turn out to be correct.

Centrus Energy is one of the World's largest suppliers of nuclear fuels and generated revenues of $294 million and gross profit of $118 million in 2022. Market commentators appear bullish on Centrus for two primary reasons:

- The company is perceived to be in pole position in the race to produce HALEU in the USA.

- The company's valuation appears low and the company has a strategic position in the supply chain for nuclear fuel into the USA

As I describe in this report, there will likely be far more competition for HALEU production than the market currently perceives. The DOE incentives are likely to rapidly create an oversupplied market and many other potential enrichers may have a significantly lower cost position relative to Centrus. For investors wanting to gain exposure to the enrichment industry, I believe ASP Isotopes has considerably greater upside (perhaps trading <3x 2024 free cash flow).

There is no doubt that Centrus is a valid play on the Uranium cycle and most commentators remain correctly positive on the supply/ demand dynamics of uranium. I am also extremely bullish on Uranium and believe we will see prices >$100 in 2024 and possibly >$300 in 2026+. For investors that want exposure to the Uranium cycle, I see Energy Fuels (UUUU) as a far less risky opportunity with equal gearing to the upside drivers also enjoyed by Centrus Energy. For complete disclosure, I own all three stocks (LEU, ASPI and UUUU).

The consensus view is that valuation is cheap (and at 8.7x P/E) it is difficult to deny. However, either government-imposed sanctions or self-imposed sanctions by Centrus' customers could cause bankruptcy almost overnight and the company's total liabilities, standing at $780 million is 37 times last 12 months operating cash flow and 59 times the average annual operating cash flow generated over the last seven years. I provide a detailed valuation analysis at the end of this report.

NB. In this report I refer to two technical terms and I will define these before we go any further:

SWU: Separative Work Unit - This is the measure of how much separation is done during an enrichment process and is basically a function of the concentrations of the feedstock, the enriched output and the depleted tails. It is typically proportional to the amount of energy required and mass produced. UxC provide SWU prices on their website which are measured in $/SWU and energy companies contract with enrichers to enrich uranium and they are charged an amount depending on how many SWU the energy company requires (which is obviously a function of how much uranium they want and how much enrichment they require).

HALEU: High Affinity Low Enriched Uranium - This is uranium that has been enriched in the U235 isotope to between 5% and 19.75%. Typical uranium used in a nuclear reactor is referred to as LEU (Low Enriched Uranium) and is enriched up to 5%.

HALEU first - this market is likely to quickly become oversupplied (read - High-cost producers will be priced out of the market)

The bull case for HALEU is well known so I will not spend time reviewing it here. In short, most new SMRs ( Small Modular Reactors ) will require HALEU and there is currently no western producer of HALEU. Per NEI (Nuclear Energy Institute) estimates, up to 2,924 metric tons of HALEU may be required by 2035 (see NEI letter to Secretary Granolm, Secretary of Energy, Department of Energy , in Dec 2021) versus total available HALEU production today of zero. Even if NEI is wrong by 75%, the supply demand imbalance is difficult to debate.

The consensus opinion on Centrus is that the company is set to make outsized profits on the production of HALEU. The company has received the only Category II license from the NRC (Nuclear Regulatory Commission) to produce HALEU in the USA and is set to produce kilogram quantities in 2023/24 . The company has received considerable financial support from DOE over the past 3-4 years, without which this company would have failed to even leave the starting blocks. The near-term supply/demand imbalance cannot be debated however, longer term, it would appear that DOE is trying to incentive an oversupplied market, whereby enrichers fail to generate economic returns and the highest cost producers rapidly go out of business. Centrus is undeniably in the lead currently, but there are multiple competitors that are also preparing to enter this market and not a single market commentator or sell side analyst has discussed these companies, all of which could become stiff competition for Centrus.

The DOE $700 million IRA incentive which will encourage domestic HALEU production is neither fully funded nor going to allow supersized profits for any HALEU producer

If anything, the incentive is likely to encourage an oversupplied market in years to come and result in significant losses for any high-cost enricher. It is difficult to see how Centrus can be a low-cost producer given they are on the start line with no enrichment capability and a track record of losing money without government assistance.

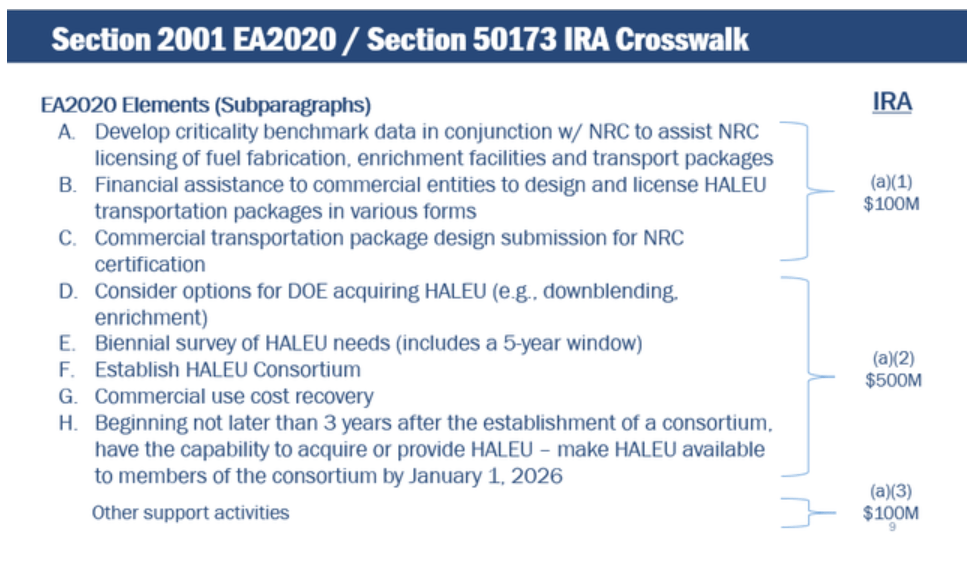

Below is a slide shown by DOE at the recent HALEU workshop which I attended at the NEI headquarters in October 2022 (I think I was probably the only investor in attendance and the slides are available on the internet). The $500 million incentive is the portion of the IRA money that is of interest to enrichers such as Centrus, with the additional $200 million being used to fund other activities also in the HALEU supply chain but not necessarily in enrichment. See the slide below.

{kind=link}

The focus of the $500 million is to set up a "HALEU Bank" whereby DOE buys HALEU from an enricher and sells HALEU to a customer. This concept was originally proposed in the NEI response to the RFI (request for information) issued by DOE in December 2021 and responded to in February 2022. All the responses made to the DOE RFI are available from DOE via a FOIA request and collectively they make good reading for those who quickly want to understand the issues at play in this highly regulated industry. Below is a slide used by the DOE at the NEI industry symposium in Washington in October 2022 and it shows how the $500 million will be used in the "HALEU Bank".

{kind=link}

As you will see, DOE intend to use the $500 million to enter into long term contracts with HALEU suppliers and purchase UF6, or uranium as an oxide or as a metal (all at 19.75% enrichment - bad luck X-Energy (who require 15.5% enrichment supplied as an oxide)).

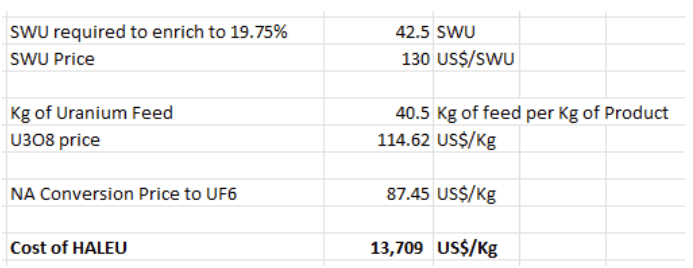

Using current SWU prices, conversion prices and uranium ore prices, the cost of a kilogram of UF6 enriched to 19.75% will be approximately $13,709/ Kg. This is shown below using current spot prices supplied weekly from UxC.

My calculations/ prices from UxC.com

{kind=link}

At current spot prices the $500 million of available funds from the IRA will buy precisely 36.5 tons of HALEU in UF6 form. In other words, any ten-year commitment from the DOE is funded for just the first 2 years. The remaining 8 years will have to be funded from appropriations and will require over an additional $3 billion (at current prices).

Readers should remember that current legislation means that DOE is not allowed to sell inventory of isotopes either at a loss or undercut other domestic commercial suppliers in the market selling an identical product (or course legislation can change). It is very difficult to see how this is going to work in practice, but investors should assume that any HALEU producer has to be able to stand up on their own two feet without the support of DOE if they are going to survive longer term. When one considers the competitive landscape (see below for a review of the competition) it is unclear if Centrus has that ability. Higher cost producers are unlikely to have a place in this market and it is difficult to see how Centrus is going to be a low-cost producer.

Also, on the slide above you will see the notes that Trevor Bluth (secondary point of contact for the symposium from DOE at Idaho Falls) used when presenting to the 100+ members of the audience. It clearly states that the HALEU must come from newly mined uranium. During the Q&A session, the presenter stated that DOE may relax that criteria but if upheld, means that importing overseas enriched LEU as a feedstock, is unlikely a path that will be permitted. If this is not relaxed, any facility Centrus constructs in USA will require 41 SWU per Kg of HALEU rather than 5.8 SWU per Kg HALEU and the Capex for such a plant is likely going to be 4-6 times as much as any plant Urenco will construct.

The Chicken and the Egg - There are many competitors waiting to enter this market

The perception is that there is a huge HALEU supply shortage. At the current time there is… but the reality is that enrichers are not building enrichment facilities without firm orders, and SMR companies are not yet in a position to place firm orders. It is a case of the chicken and the egg - what comes first. As I highlight below, there are many additional companies working to enter the HALEU industry. Some of these may have better technology than Centrus, affording them a lower position on the cost curve. Others are better capitalized, have greater experience and potentially have access to cheaper feedstock. As soon as the HALEU supply chain is unraveled the winners and the losers will be determined by a cost curve and the competitiveness of a company's technology. It is unclear at this point just how competitive Centrus will be versus other players.

Competitor Snapshot #1: Urenco

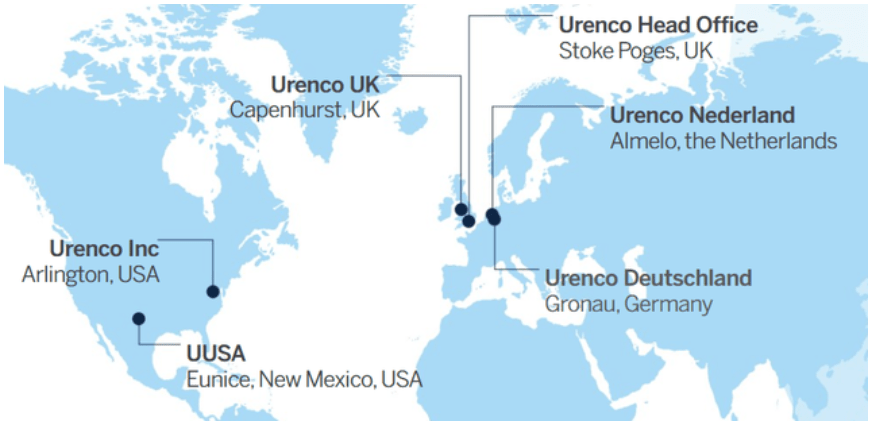

Urenco is one of the World's leading suppliers of uranium enrichment services and fuel cycle products and have been a pivotal player in the nuclear fuel supply chain for over 50 years. Per the company's annual report , Urenco generated revenues of Euro 1.7 billion in 2022 and EBITDA of Euro 825m. With Capital expenditure of just Euro 184 million, the company generated operating cash flow of Euro 1.1 billion. Urenco is owned by the Governments of the Netherlands and the United Kingdom and two German companies, E.ON and RWE. The company currently owns and operates the only commercial uranium enrichment facility in the USA (Eunice, New Mexico).

Without substantial subsidies (which currently appear unlikely) It is unlikely that Centrus will be able to beat or even match Urenco on price. Urenco currently has enrichment capacity of 18.6 million SWU (out of a global capacity of 60.6 million SWU). Approximately 4.9 million SWU of this capacity is located in the USA at Eunice (see below for map of Urenco's operations). The annual report provides an exceptional overview of the enrichment industry and makes an excellent primer for those investors wanting to learn more.

{kind=link}

It is trivial to calculate just how much additional capacity Urenco will need to add to their manufacturing plant as well as how much of Urenco's current capacity would be needed to supply feedstock to the new plant. Note that the new capacity will require a new balance of plant capable of enriching up to 19.75%.

A simplified version of the formula that calculates the work W SWU required to produce a quantity of product P of product assay X P from a quantity of feedstock F of feed assay X F whilst concurrently producing tails quantity of T of tails assay X T is given by the following equation:

{kind=link}

Basic calculation for SWU (Common literature)

Where,

common literature

The above mathematical formula can be found in many sites on the internet and text books on the subject. For those less mathematically literate Urenco provide a SWU calculator on its website .

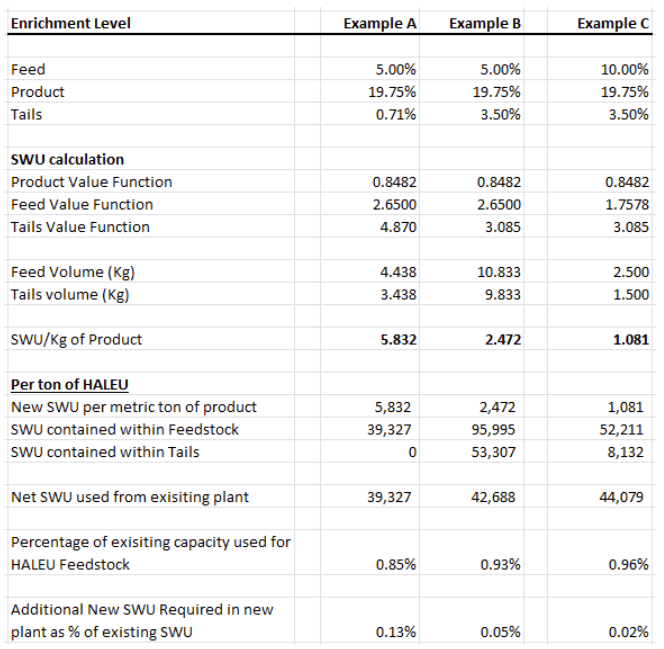

In the table below I use three examples. Example A and B assume Urenco use LEU (enriched at 5%) and use it as feedstock into the new plant which will then enrich it to HALEU. In example A the tails from the HALEU plant is stripped down to 0.71% (which now becomes the feedstock for the current plant), while in example B, the tails from the HALEU plant is stripped down to 3.5% which is now sold as LEU. In example C, Urenco uses a 10% feedstock (Urenco has approval to produce such product in New Mexico) and this is then fed into the new HALEU plant.

{kind=link}

As shown in the table above, Urenco needs to add very little additional SWU to its existing plant in order to produce HALEU.

If we assume annual demand for HALEU settles at 20 metric tons per year, additional capacity that Urenco will need to construct is less than 120,000 SWU per year equivalent to about 3% of the current plant. It is unlikely that any other company can either build this capacity as cheaply as Urenco, as quickly as Urenco or operate it with the same degree of efficiency as Urenco. When you are a mouse… it is difficult to fight against an elephant. For anyone to outcompete Urenco, they will require a very different technology that repositions them on the cost curve. Centrus may have that… but it feels unlikely.

Competitor Snapshot #2: ASP Isotopes ('ASPI')

Little is known about ASP Isotopes Inc. The company IPO'd onto NASDAQ in November and the stock has not exactly had a great run - it is down approx. 75% since its IPO. That said, this hasn't been a great market for profitless microcap stocks and this poor share price performance is despite the company achieving some positive results both in contract wins and completion of manufacturing plants. At a market cap of just $15 million this stock likely has the greatest upside of all the stocks mentioned in this report, if the company can hit milestones. The company issued a news letter to shareholders on March 13, which is interesting reading and suggests there is considerable upside.

Per the company's S1 , (which also makes good reading for those investors wanting a primer into isotope enrichment), ASP Isotopes acquired the isotope enrichment technology and the scientists from a South African company called Klydon which went through bankruptcy in 2021. The scientists came from the South African Nuclear program back in the 1980s when they successfully enriched uranium for their nuclear reactors and built 6+ nuclear warheads. The program was stopped in 1994 and the weapons dismantled.

The company is focused more on medical isotopes such as Molybdenum-100, Carbon-14 and Silicon-28 but they do state in their presentation that they are researching into the production of HALEU and that they would like to partner with another group (government or company). Very little is known about their technology but according to the World Nuclear Association:

The Aerodynamic Separation Process being developed by Klydon in South Africa employs similar stationary-wall centrifuges with UF6 injected tangentially. It is based on Helikon but pending regulatory authorization it has not yet been tested on UF6 - only light isotopes such as silicon. However, extrapolating from results there it is expected to have an enrichment factor in each unit of 1.10 (cf 1.03 in Helikon) with about 500 kWh/SWU and development of it is aiming for 1.15 enrichment factor and less than 500 kWh/SWU. Projections give an enrichment cost under $100/SWU, with this split evenly among capital, operation and energy input.

Source: Uranium enrichment

Management don't appear to deal in "fluff press releases" and their website provides little information on either the science or their manufacturing plants. Perhaps management need to employ an investor relations or public relations firm as their website looks incredibly basic and the investor slide deck could do with some work!

Management own about 50% of the company's stock and there has been insider buying also - the Chairman and CEO bought $150,000 stock in the IPO at $4/ share and another director, Duncan Moore purchased stock in multiple transactions ( one , two and three ) at higher prices than the current share price. This is considerably better insider participation than either Centrus or Silex Systems (SILXF) where there has been no insider buying. With a market cap of just $15 million and no debt, if management successfully execute on even just half their business plan this could easily be a $500m+ stock in a few years' time, just like Centrus and Silex. The stock has no sell side coverage yet and so there are no consensus forecasts but presumably as time evolves, if we see sell side coverage, the stock will benefit from this. The lack of track record, lack of trading, low liquidity and small market cap also make this stock the riskiest and hardest to forecast etc. But for those who have an appetite for risk, this could well be the place to park some of your venture capital.

It really is impossible to say more about the company's HALEU prospects given how little is known about either their science or technology at this time. I guess we will have to wait and see. I hope to meet the company at an investor conference in the near future and I may write about the company in the future.

Competitor Snapshot #3: SILEX Systems

Of all the company's mentioned in this report, Silex Systems could possibly be described as the oldest (although the other two have either been through a reorganization or similar during the past few years). Silex Systems was founded in 1987 but is still yet to generate any meaningful milestones or revenue. The stock has been trading on the OTC since 2008 and has a market cap of $550 million with cash on balance sheet of $145 million (as at 8 March 2023) and accumulated losses of $241 million (as at Dec 31, 2022). The company has a good website with plenty of information available.

The company describes itself as a technology commercialization company whose primary asset is the SILEX laser enrichment technology, originally developed at the Company's technology facility in Sydney, Australia.

Laser enrichment processes have been a focus of interest for some time but to date, all have failed to yield commercially viable results. The development of the Atomic Vapor Laser Isotope Separation (AVLIS) began in the 1970s. During the 1980's and 1990's the US Government spent over $2 billion on research and development into the technology but they appeared to have failed to produce a commercially viable plant. A similar story is true for the French, who scrapped the program in 2003 after enriching 200 kg of 2.5% enriched uranium.

Silex System's original venture into Uranium enrichment (called GLE or Global Laser Enrichment) started seventeen years ago in 2006 when they entered a partnership with GE Energy (subsequently GE Hitachi). The original plan was to construct an engineering-scale test loop, then a pilot plant and finally a fully commercial plant, in the USA. In-mid 2008 Cameco bought into the GLE project, paying $124 million for a 24% share, alongside GE (51%) and Hitachi (25%). Cameco is one of the world's leading uranium producers and nuclear fuel suppliers. In April 2016 GE and Hitachi exited GLE and then in February 2019 Silex Systems and Cameco agreed to buy out the GEH 76% share in GLE for US$ 20 million on a deferred payment basis (i.e. zero upfront). After this transaction, Cameco held 49% of GLE and Silex 51%. Cameco has an option to purchase an additional 26% of GLE from Silex.

The company has entered into an agreement with DOE it enrich depleted tails up to 0.71% enriched uranium at Paducah which it hopes to achieve by 2027/28. Assuming the company is successful with this endeavor, they will then try to enrich HALEU.

It is unclear how this will play out in the future; however, laser enrichment of isotopes should not be dismissed. Russia currently uses lasers to enrich atoms such as Nickel 64 and Ytterbium 176 (which sell at >$20,000 per gram - see isoflex). In addition, South Africa had considerable success with enriching isotopes with lasers during the 1980s when they built 6 nuclear warheads which involved uranium enriched to >85% and lithium-6 enriched to >95% (lithium-6 was used as a detonator for the warhead). However, it remains worrying that DOE failed to find AVLIS commercially viable having spent over $2bn on the project.

Management at Silex appear average (if I am being polite) - they have failed to really generate any meaningful results during the last seventeen years and if they have failed at every stage during the last seventeen, it is unclear why they will be able to achieve much in the next seven. Also, the fact that GE bailed out on this project and the US Government bailed out on other laser projects suggests that this is nontrivial science or there are other hurdles that cannot be determined by an outsider.

In addition to enriching Uranium, the company is hoping to enrich silicon-28 and ytterbium-176. The company hopes to have commercial quantities of enriched silicon-28 (up to 5 kgs per annum) during 2023 and then up to 10 kgs per annum by 2024. The company recently added Yb-176 into its menu however Mo-100 was on the menu for multiple years previously but was recently removed to allow room for Yb-176.

Not all HALEU is equal

Uranium has three isotopes that are of interest to companies involved in the nuclear supply chain: U-234, U-235 and U-238 . It would appear that most investors focus on the U-235 isotope and pay little attention to the U-234 isotope, after all, the U-234 isotope is found at an abundance of just 0.005% in natural uranium (55 parts per million). The half-life of U-234 is 245,500 years compared to 704,000,000 years for U-235 and 4,468,000,000 years for U-238. The abundance of U-234 to U-235 to U-238 is approximately inversely proportional to their half-lives.

However, when one enriches U-235, one also unintentionally enriches U-234. U-234 is an unwanted isotope of Uranium for both enrichers and nuclear power plants for numerous reasons.

Uranium-234 nuclei decay by alpha emission to thorium-230. As one increases the abundance of U-234, the amount of alpha decay also increases and this makes the storage or U-234 more challenging. The shorter half-life of U-234 relative to U-235 and U-238 means that alpha particles (helium) produced are higher. It is highly likely the some of the modern materials used to construct centrifuges are unlikely to be able to withstand the alpha emission at higher levels of U-234. Russia has not experienced this issue because their centrifuges are constructed from steel and were designed to enrich weapons grade uranium. But enrichers with modern equipment, building their centrifuges out of carbon fiber are likely to have problems as carbon fiber is unlikely to be able to tolerate this level of alpha emission. Companies employing non-traditional routes of enrichment such as ASP Isotopes and Silex Systems (SILXF), may be less likely to suffer from this issue.

Uranium-234 is also a neutron absorber . The fission of one atom of Uranium-235 releases 202.5 MeV . During this reaction, one neutron collides with a U-235 atom splitting it into numerous other atoms and releasing a substantial number of additional neutrons. These neutrons then go onto collide with other U-235 atoms and so the chain reaction continues releasing more and more energy. During a controlled fission (such as that in a nuclear reactor), the rate of this reaction is controlled. The addition of U-234 makes the control of this fission reaction more challenging. There was an interesting paper published by the IAEA here ( TECDOC-1529). It is quite possible that HALEU with lower levels of U-234 will trade at a premium to HALEU that contains higher levels of U-234 and it is likely that HALEU produced by Centrus will contain higher levels of U-234 because the centrifuge equation, which determines the efficiency of a centrifuge, implies that the enrichment of U-234 will be to forth order versus U-238.

Another interesting point here is that 2-3 years ago, the base case assumption was that DOE will down blend weapons grade Uranium to fulfill HALEU requirements. SMR reactors have a limit on U-234 abundance of 0.05% and it isn't possible to achieve this upper limit on abundance when weapons grade uranium is down blended. Basic mathematics instructs us that on the way up, the enrichment of U-234 is of the fourth order but on the way down (via down blending) it is of the first order. DOE were broadly silent on this technical issue and market commentators conveniently blamed national security reasons and the recent geopolitical upsets as the reason for the U turn on down blending, but basic math suggests that the down blending of weapons grade uranium was never a viable route. But this also suggests that U-234 enrichment is a real problem.

Additional well understood and well appreciated non-HALEU risks to Centrus

Currently, Centrus does not have any commercial enrichment capability of its own currently. Its entire uranium sales (in the form of Low Enriched Uranium- LEU) are produced by TENEX (Russia) and Orano (France) (see the company's 10-K for more details ). Centrus Energy purchases the uranium feed and then purchases SWU (Separative Work Units) from both companies and then resells the enriched uranium to customers in the USA. This business model is associated with many risks, most of which are likely already appreciated by investors and commentators.

Potential for further sanctions against Russia.

Centrus currently obtains a significant (read, the majority) of its SWU (Separative Work Units) from Rosatom (Rosatom State Nuclear Energy Corporation). Following the invasion of Ukraine in Feb 2022, there are currently sanctions imposing trade restrictions with Russia for most products, goods and services. One exception is stable isotopes and essential fuels such as enriched Uranium. It is not unrealistic to think that the USA might place sanctions on the importation of additional Russian goods, products and services including Uranium and other stable isotopes. Many senators and congresspeople are proposing and advocating for such sanctions ( which I view as ridiculous and extremely bad for the American people but I am an investor, not a politician). The company states that if sanctions were imposed on the availability of SWU from Rosatom, it would have a material impact on the company's operating results. It is unclear how much of Centrus' SWU comes from Russia but it is likely >90%.

Potential for self-imposed sanctions by Centrus' customers.

A little-known fact is that no NEW contracts have been signed by US customers with Russia since the Ukraine invasion in February 2022 ( Source: Nuclear Energy Institute ). EXISTING contracts have been honored but no NEW contracts have been entered into. As existing contracts roll off, it will be interesting to see if Centrus' customers renew them or look for an alternative source of enriched uranium that is not derived from Russia. It is not unreasonable to think that Russian SWU may end up trading at a discount to non-Russian SWU.

Historically, the Company has only really survived through Government Support.

This company failed to generate any free cash flow until recent years when a cyclical upswing in SWU prices occurred and the company received considerable inflows of capital from the DOE (Department of Energy). It is worth noting that the CEO, Daniel Poneman, has had a long career in politics having previously served as the Deputy Secretary of Energy at DOE, the Acting Secretary of Energy and in various roles in Defense Policy, Arms Control and Non-proliferation and Export Controls. With what is likely a full rolodex it is likely that most poles are well greased and this support will likely continue. However, it is worth pointing out that incentives through the IRA (Inflation Reduction Act) are likely to involve (unfunded) long term supply contracts rather upfront cash payments or cost sharing programs to assist with construction costs. Also, it is worth pointing out that historically, companies that have only survived through government aid and government support have not made good investments.

Valuation Summary

Centrus Energy trades on a 2022 P/E multiple of 8.7x and a 2023 P/E multiple of 10.4x, based on consensus estimates. The stock trades on an operating free cash flow yield of approximately 5%. If one views this stock as a commodities producer, the stock is not cheap on a free cash flow yield. For a company that is essentially a reseller of Russian and French LEU into the USA, without any production facilities of its own, this current valuation feels more than fair. For there to be considerable upside to the stock, one needs to believe in HALEU.

With HALEU news flow likely to remain positive for the foreseeable future (at least the next 12-24 months) it is very likely that Centrus' share price will start to price in some of this upside during this period, which clearly makes this stock a Buy for an investor with a 12-24 month time horizon.

Additionally, the company has total debt of $169.8 million and total liabilities of $779.6 million which are both large numbers, when one considers the cash flow generating capacity of the current business. In addition, it is likely that significant capex is required if the company is to enrich its own isotopes and produce HALEU.

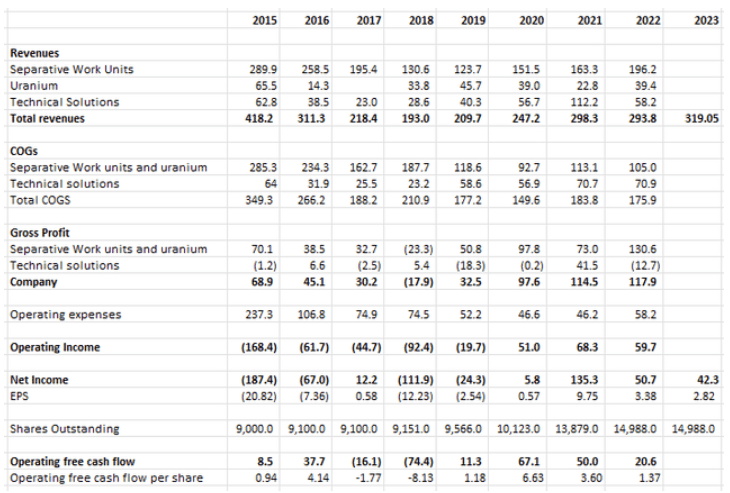

Below is a basic historic financial model for Centrus from the last 8 years and includes consensus estimates for 2023. It is clear that this has been a poor cash generating business over the past 8 years. During recent years, the situation has improved, and earnings should remain elevated while SWU prices remain at their current levels ($130/ SWU). Obviously, if the geopolitical

{kind=link}

What could HALEU be worth?

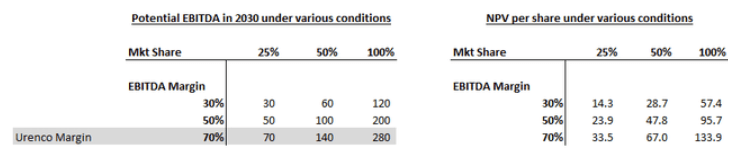

Based on a $13,700/Kg HALEU, the HALEU market could easily $1.6 billion annually by 2030 and $5.3 billion annually by 2035, per estimates by the Nuclear Energy Institute. Many of the future plants included in the NEI estimate at projections for future plants that may or may not be built. Many market commentators suggest that the actual demand may be closer to 25% of the NEI figure. So, assuming a 75% discount to these estimates and that the 2030 figure is closer to $400m. The table below shows just how much EBITA this may create in 2030 at various market shares and EBITDA margin. Applying a 15x multiple and discounting this figure back 6 years provides the potential NPV per share from HALEU. It is very obvious that this is a huge opportunity for Centrus. Assuming Centrus are able to achieve a 50% ENITDA margin on HALEU (Urenco achieve c. 70%) and Centrus is able to capture a 50% market share (with Urenco taking the other 50%), HALEU could be worth as much as $48/ share.

{kind=link}

Conclusion

As I highlight in this report, there are considerable risks associated with a long-term investment in Centrus. The market correctly appreciates that HALEU could be very valuable to Centrus and that Centrus is currently in the lead, in terms of development in terms of HALEU supply. However, few investors have likely appreciated just how competitive this market may become and it is likely that high-cost producers will quickly become loss making. It is difficult to see how Centrus can ever be a low-cost producer and with an exceptionally leveraged balance sheet, there are significant longer-term risks.

I hope you find this report useful. Good luck investing!!

For further details see:

Centrus Energy: Continue Owning For Near-Term Upside But Beware Of Longer-Term Risks