LEU - Centrus Energy Growth Enriched By Domestic HALEU Deal

Summary

- The first domestic enriching capacity contract was granted to Centrus Energy Corp. since U.S. capacity fell to 0 in 2013.

- There is significant money in next-generation nuclear technology utilizing HALEU fuels. Centrus Energy Corp. has first-mover advantage, being granted $150 million from the DoE for commercialization.

- Centrus expects a 40% growth in nuclear energy by 2050 without climate incentive policies. 105% with those policies included.

- Every U.S. reactor imports 100% of its fuel, including 30% from Russia. Estimated 15 million SWU gap if Russia is cut off from uranium exports.

This article uses the Separative Work Unit ((SWU)) to measure uranium enrichment. Usually, this ratio is a maximum of 5% for LEU standard fuel (low-enriched uranium) and 20% for HALEU (High-Assay Low-Enriched Uranium) fuel.

For example, separating 100kg of raw uranium into 10kg of standard fuel takes approximately 62 SWUs. It is the nuclear equivalent of a BTU (British Thermal Unit).

Investment Thesis

Centrus Energy Corp. ( LEU ) is a diversified global uranium enrichment and nuclear technical services firm. Traditionally, Centrus contracts out the enrichment of nuclear material before assembling fuel. However, the DoE has granted approximately $150 million to construct the first commercial enrichment facility in the US since capacity dropped to 0 in 2013.

Centrus was approved to provide HALEU fuel on a commercial basis. HALEU fuel is more energy dense than traditional enriched fuel and required for SMRs (Small Modular Reactors).

Provided Centrus can deliver on its obligation of 20kg of HALEU fuel by the end of FY23 to the Department of Energy, there is significant commercialization potential. Every U.S. reactor imports 100% of its fuel, including 30% from Russia. With the war in Ukraine dragging on and experimental SMRs showing promise, there should be significant growth in domestic demand for enriched uranium.

We believe that Centrus is a long-term play. It has first-mover advantage for commercialization in the next generation of nuclear fuel and domestic capacity of current standard fuels.

Estimated Fair Value

EFV (Estimated Fair Value) = E24 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E24 EPS X P/E = $3.30 X 19.0 = $62.70

Estimating forward earnings power of Centrus is difficult, given the fluctuations in pricing for standard fuel enrichment. We have used our guesstimate for E2024. If they are successful, earnings power could surge above $10.00 per share at the end of the decade. We have assumed a 19 P/E for this growth stock. Commercializing HALEU fuel should cause P/E expansion as the growth path will be well-illuminated.

| Centrus Energy |

| E2023 |

| E2024 |

| E2025 |

| Price-to-Sales |

| 2.5 |

| 2.2 |

| 2.0 |

| Price-to-Earnings |

| 19.6 |

| 14.8 |

| 12.3 |

Market Conditions

Nuclear energy is green, with nearly no greenhouse gas emissions, a small waste footprint, and a very energy-dense fuel. Eating a banana will give you a higher radiation dose than living next to a nuclear power plant — despite its scary reputation. Nuclear fills critical energy needs for baseload power on a large scale, as the intermittent nature of solar and wind solutions makes them unreliable. There is also the issue of excessive land usage.

{kind=link}

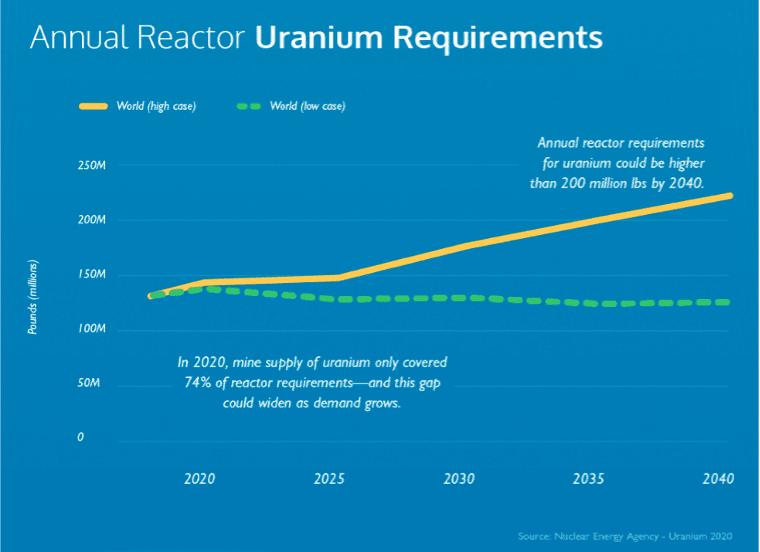

In 2020, uranium production only covered 74% of reactor requirements. Centrus expects 40% growth in uranium demand by 2050, even without climate incentive policies, and 105% with those policies included. There are 440 active nuclear reactors globally, with 60 new reactors under construction. This is 10% of global generation capacity, just short of 2653 TWh (Terawatt hours).

The Russian invasion of Ukraine presented a new domestic opportunity. Russian uranium accounts for 38% of global uranium output . Between 1985 and 2015, uranium enrichment capacity has fallen from 27.3 million SWUs to 0. Meanwhile, Russia has taken a leadership position, increasing production from 3 million to 26.6 million SWUs over the same period.

U.S. Demand in 2021 was filled 100% by imports of enriched material with 28% originating from Russia. Global demand will face a 15 million SWU/yr gap in nuclear fuel because of sanctions on Russia. This is the equivalent of the entire annual consumption of the United States.

Nonproliferation treaties dictate that foreign enrichment technology cannot be used in projects critical to national security. These include Military microreactors, nuclear arms, and Naval reactors. Within the 10 year horizon, the United States may need to modernize its nuclear arsenal with Putin’s pull from the START treaty .

Research and Construction

The DoE (Department of Energy) approved for Centrus to build a refinery for HALEU fuel. Traditionally, this fuel was used exclusively for research reactors by the government in the ARDP program (Advanced Reactor Demonstration Program).

The DoE’s original plan was to ramp up U.S. enrichment capacity again in 2024 once the ARDP program began to show commercial success. Advanced reactor manufacturers under the ARDP program traditionally sought enriched fuel from Russia. TENEX/Rostam is the only company in the world currently able to produce HALEU on a large scale and is a Russian state-owned enterprise. However, as previously discussed, the Russian invasion of Ukraine significantly shook up the uranium and fuel markets. The DoE projects that there will need to be 40 metric tons of HALEU supplied by 2030. Centrus estimates that the total addressable market for HALEU fuel could be $5.3 billion per year by 2035.

LEU was given a cost-sharing grant for $30 million to construct a demonstration centrifuge facility, contingent on delivering 20kg of HALEU fuel by the end of FY23. Once this condition is met, the facility will be authorized to produce 900kg per year. The DoE will offer the second phase of the contract, on a cost-plus basis, of around $90 million. Centrus states the facility is highly scalable, with the ability to produce 6 metric tons per year within 42 months of additional funding.

An additional research project is a partnership between Clean Core Thorium Energy and Centrus , to produce sample pellets of an experimental thorium-HALEU-based fuel called ANEEL. Commercialization of ANEEL is expected to be possible in 2H24 . The fuel is primarily marketed for PHWR (Pressurized Heavy Water Reactors) reactors which are used primarily in Canada and India. The main appeal of ANEEL is its waste footprint, being lower than traditional uranium fuels by 80%.

Present Results

4Q22 saw a 41.80% year-over-year increase in revenue, primarily because of this DoE contract. It beat normalized EPS estimates and came in at $1.42 per share. We expect this number to decrease slightly until HALEU reactors come online and the fuel is more heavily commercialized in FY24. Centrus will assume $30 million in construction costs related to HALEU centrifuge construction.

Current fuel generation demand is an addressable market of $1.4 billion domestically and $1.3 billion internationally. Centrus stock saw a 16% 3-year-CAGR in revenue , generating $235.6 million in revenue from standard fuel sales. This is a $50 million or 23% increase over FY21 for the segment.

The traditional fuels order book is $1 billion in renewing orders through 2030. In FY22, $270 million in new fuel orders was added to the order book. The increase in revenue is primarily due to higher average prices over the year, and pricing actions to account for an offset in volume.

The technical services segment saw a $10.5 million decrease in revenue. This was because of the reduction in experimental work on HALEU reactors.

Risk

One of the primary risks facing Centrus is its ongoing contract with the Russian-state-owned Rostam. Centrus has a supply contract with TENEX, the exporter of Rostam – Russia’s state nuclear power company. This contract was intended to last until 2028. Neither enriched fuel nor raw uranium is on the US’s sanction list with Russia. However, there is a renewed effort in Congress to prohibit importation.

Standard fuel enriching is a complex process that varies wildly with pricing. Inputs are very dependent on tariffs, uranium costs, and energy costs. Across the entire firm, the gross margin 5-year average is 27.8%. In 2015 the gross margin of the firm was 16.5%. In 2018 it was -9.3%, and the trailing 12 months is 40.1%. There is not a robust futures market for enriched uranium fuel, and Centrus assumes losses during market slumps.

The bulk of the DoE contract money is contingent on the delivery of 20kg of HALEU fuel. Should Centrus be unable to deliver on this obligation, it could lose out on the $90 million supply contract, and the DoE may look elsewhere.

Conclusion

We believe that Centrus Energy Corp. is a long-term play. It offers a higher risk but a higher reward. Provided the current ARDP experimental reactor program yields results that can be commercialized, HALEU fuel could become a significant portion of the green energy push.

For further details see:

Centrus Energy Growth Enriched By Domestic HALEU Deal