LEU - Centrus Energy: Positioning As A Cornerstone Of The U.S.' Energy Security

Summary

- Centrus Energy provides nuclear fuel and technical solutions for US and foreign customers.

- The company could be the solution to the dependence of Russian nuclear fuel imports.

- Centrus Energy is the first and only licensed US company to produce HALEU.

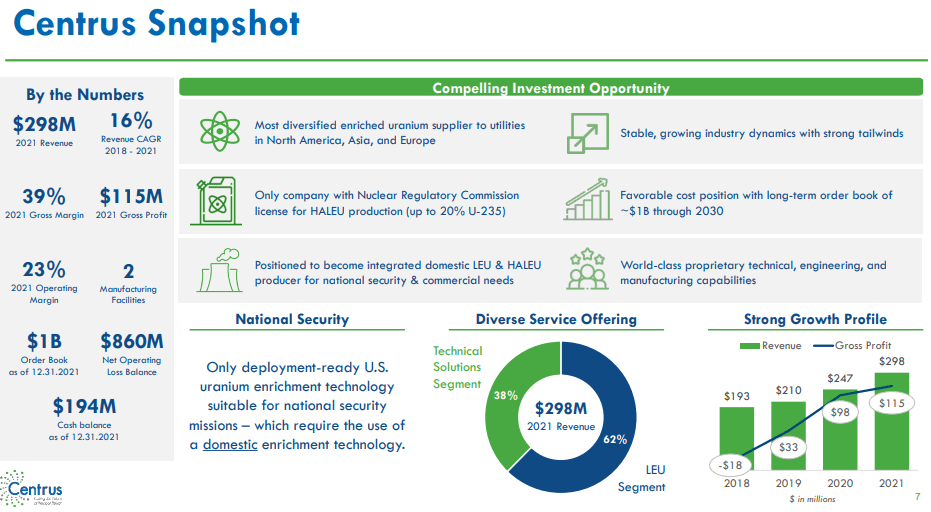

- The massive order book of US$1B+ and the nature of its clients should make the company resilient to economic turmoil.

- Valuing the company at EV/EBITDA multiple of 8.52 indicates 77.5% upside to the current share price.

The past few years highlighted the importance of supply chain security. In light of its energy dependence from Russia, Europe saw its gas and electricity prices go through the roof and only because of the mild winter has been able to avoid a catastrophe. At the same time, US nuclear power plants are dependent for part of their fuel needs to Russia. The US government is trying to solve that dependence by working with the industry for securing the supply. Here comes Centrus Energy ( LEU ). It's the first and only US entity licensed for the production of high-assay, low-enriched uranium (HALEU), which is expected to be demonstrated in 2023. In the meantime, the existing low-enriched uranium ((LEU)) and technical solutions businesses of the company have been demonstrating strong performance. In terms of fair value, I think that even the existing business of the company implies serious upside to the current share price.

Company overview

{kind=link}

Registered in the US, Centrus Energy provides services to the nuclear industry in the US and abroad. It has two main segments - low enriched uranium ((LEU)) and technical solutions. The first segment is contributing to a larger part of revenue and involves supplying utilities in the US, Europe and Asia with nuclear fuel for their power plants. The majority of sales involve the enrichment component of LEU - SWU (separative work units). It's important to note, that Centrus is not producing the LEU itself currently, although is capable of doing so, but is instead purchasing SWU from Orano and TENEX under long-term contracts and then reselling it to its clients.

Recent performance

{kind=link}

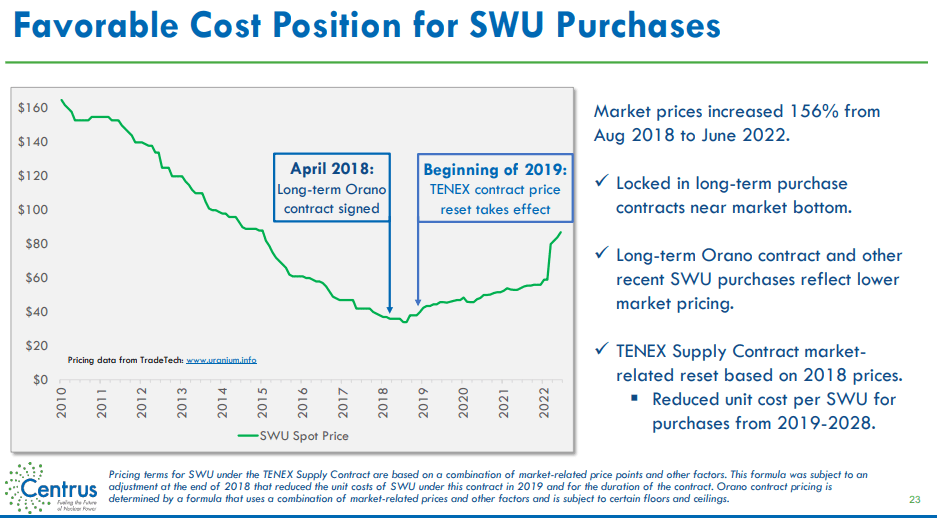

Centrus is in a very good position, having entered into long-term supply contracts with Orano and TENEX when SWU prices were at their lowest. While no information regarding the exact pricing mechanism of the contracts was provided, it's known that there's a market element, but also "other factors" as well as floors and ceilings. However, I think it's safe to assume that the pricing mechanism gives Centrus a very favourable cost structure in light of the recent SWU price surge, as demonstrated by the soaring EBITDA margin.

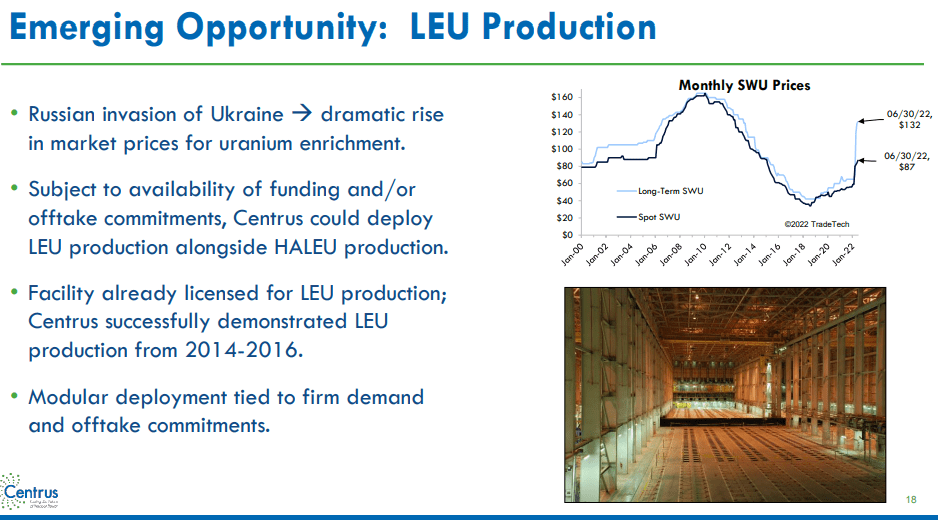

In light of the European energy crisis, more and more western countries and Japan are warming up to the idea of nuclear energy. In the US, financing has been granted for extending the life of nuclear power plants, which were previously considered for a future shutdown. Combined with the desire of western utilities to diversify away from Russian nuclear fuel, this could provide Centrus with the possible opportunity to restart its own LEU production, given sufficient demand.

{kind=link}

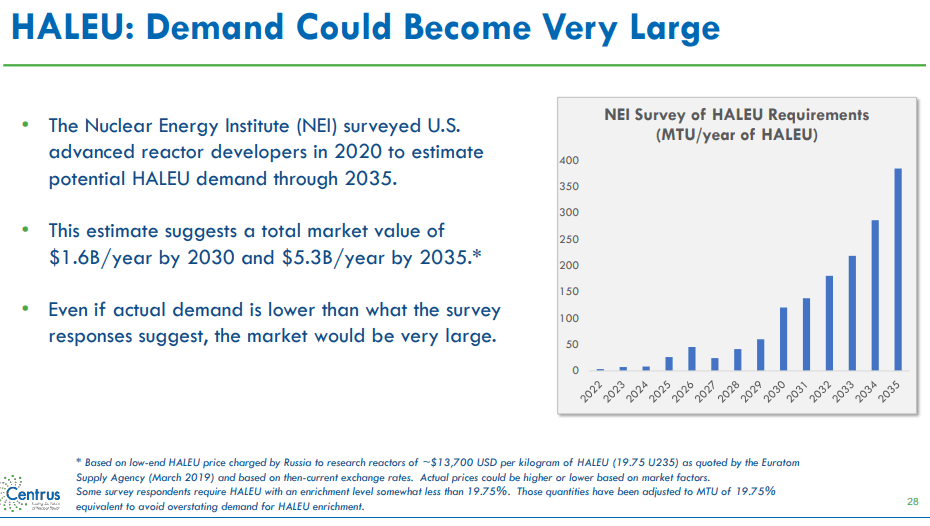

The HALEU opportunity

The potential deployment of many small modular nuclear reactors (SMRs) is expected to create strong demand for high-assay, low-enriched uranium. In order to secure a domestic source of supply, the US Department of Energy has signed a contract with Centrus, worth up to US$150M. The agreement has a cost-sharing element, where the DOE will bear US$30M of costs (50% of the estimated total) for the completion and putting into operation of HALEU cascade and produce 20 kg of HALEU by the end of 2023. In the DOE's announcement, the US secretary of energy noted :

Reducing our reliance on adversarial nations for HALEU fuel and building up our domestic supply chain will allow the U.S. to grow our advanced reactor fleet and provide Americans with more clean, affordable power.

{kind=link}

Valuation discussion

Centrus has a very niche business, which is subject to various licenses for obvious reasons, as well as technological know-how. This makes the sector that Centrus operates in with very high barriers of entry, possibly allowing for the elevated margins to persist in light of the changing geopolitical environment. In addition, the US$1B+ order book and the inelastic demand for nuclear fuel should make the company resilient to a possible recession.

At the same time, there are no publicly traded peers of Centrus. However, the nature of the majority of the company's business - getting LEU from producers to consumers, resembles the nature of the oil & gas midstream segment. According to Damodaran's database, the EV/EBITDA of the Oil/Gas Distribution industry is 11.36. To that, I apply a 25% discount to reflect the lack of dividend payments and higher volatility of margins.

{kind=link}

| Oil&gas midstream EV/EBITDA |

| 11.36 |

| Discount |

| 25% |

| Implied EV/EBITDA |

| 8.52 |

| Centrus Energy TTM EBITDA (US) |

| 126 |

| Implied EV (US) |

| 1 073 |

| Net debt (US) |

| 16 |

| Implied equity value (US) |

| 1 056 |

| Number of shares |

| 14.6 |

| Fair value (US$) |

| 72.24 |

| Current price (US$) |

| 40.69 |

| Upside |

| 77.5% |

*Author's own assumptions

The resulting fair value estimate for Centrus Energy is US$72.24, which implies 77.5% upside.

Risks

TENEX supply risk

Obviously, although nuclear fuel is not subject to the US sanctions against Russia, the geopolitical tensions put that contract at risk. In the event of the supply of nuclear fuel falling under sanctions, I think it's unlikely that Orano contract will be able to compensate the Russian quantities of SWU. In that event, hypothetically Centrus may have to restart its own LEU production, but it's unclear at what cost and timing that could happen. However, the US$121.9M worth of net uranium position in inventories as of Q3'22 may be an indication of something along those lines.

Margin contraction risk

As the exact terms of the Orano and TENEX supply contracts are not available, it's unclear how fast and to what extent the market price increase of SWU will be shifted to Centrus. This has the potential to squeeze the currently impressive margins of the company.

Operational risk

I consider the HALEU opportunity as a potential game changer for Centrus Energy. The successful demonstration of the production process could be a powerful upside trigger. On the other hand, if management doesn't deliver on this opportunity, the stock may plummet.

Conclusion

Centrus Energy is aiming to position as a cornerstone of US' energy security by offering a domestic source of supply for much-needed nuclear fuel. The HALEU production opportunity may make the company a primary supplier for nuclear fuel of future generations of nuclear power plants. At the same time, the current LEU brokerage business demonstrates elevated margins, due to long-term supply contracts with LEU producers at the right time of the SWU price cycle. Valuing the company at 8.52 EV/EBITDA implies a fair value per share of US$72.24 or 77.5% upside to the current price.

For further details see:

Centrus Energy: Positioning As A Cornerstone Of The U.S.' Energy Security