SPY - Century Communities: Cautiously Optimistic After Navigating The Housing Recession

Summary

- Century Communities reported strong Q4 results considering an unfolding housing recession.

- The company's success makes it cautiously optimistic about the coming year despite operating at lower year-over-year levels.

- Lower costs, stronger margins, and positioning in the affordable price range give the company good odds for navigating this year.

- A looming economy-wide recession is a key wildcard.

Mid-sized home builder Century Communities, Inc. ( CCS ) reported strong Q4 and full-year 2022 earnings . The company achieved impressive results across its balance sheet, gross margins, profits, and costs. Yet with a housing recession still underway, 2023 will deliver a different year for Century Communities. Appropriately, Century Communities is cautiously optimistic as it builds out communities with slightly smaller homes made more affordable by lower input costs. The company’s guidance is the key starting point for understanding the current business.

Guidance

Going forward, Century Communities will depend heavily on key tailwinds. The company expects gross margins in Q1 2023 to be similar to the previous quarter and then increase in subsequent quarters thanks to these tailwinds.

Gross margin should improve by 400 basis points in 2023 as the company reaches a new norm in the low 20s range (in percentages). The improvement will start in Q2 of 2023 as the company sells out higher cost inventory and begins selling inventory made with cheaper materials and improved cycle times. Falling lumber prices will drive about two-thirds of cost reductions. An average 57-day improvement in cycle times (compared to 6 months ago when pricing hit its peak) will significantly reduce supply chain costs. The industry’s reduction in housing starts frees up resources. This reduction of stress in the supply chain is a positive aspect of the Federal Reserve’s rapid tightening of monetary policy. Century Communities will drive further affordability by building slightly smaller homes.

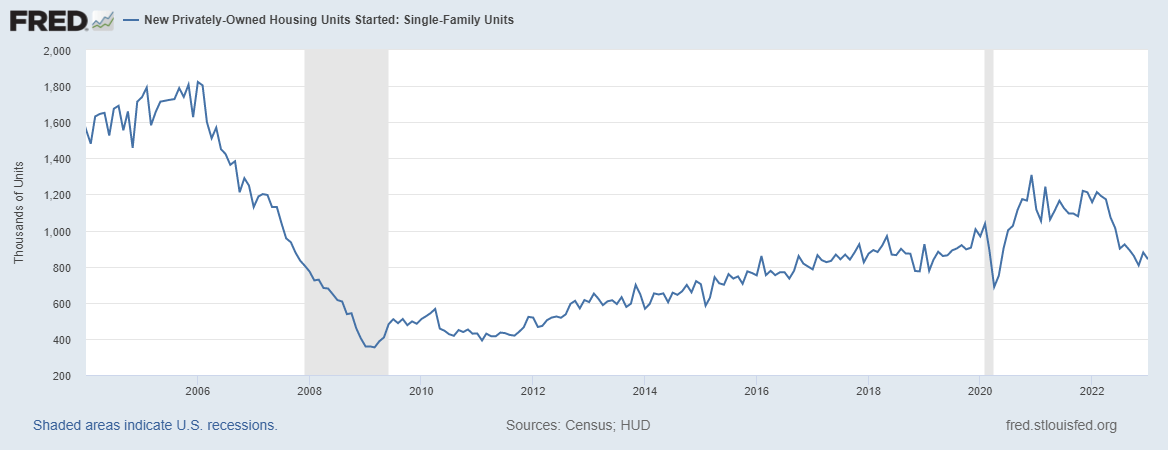

Excluding the pandemic lows, single-family housing starts are back to levels last seen during the market’s last pre-pandemic downturn. (U.S. Census Bureau and U.S. Department of Housing and Urban Development, New Privately-Owned Housing Units Started: Single-Family Units [HOUST1F], retrieved from FRED, Federal Reserve Bank of St. Louis, February 25, 2023.)

{kind=link}

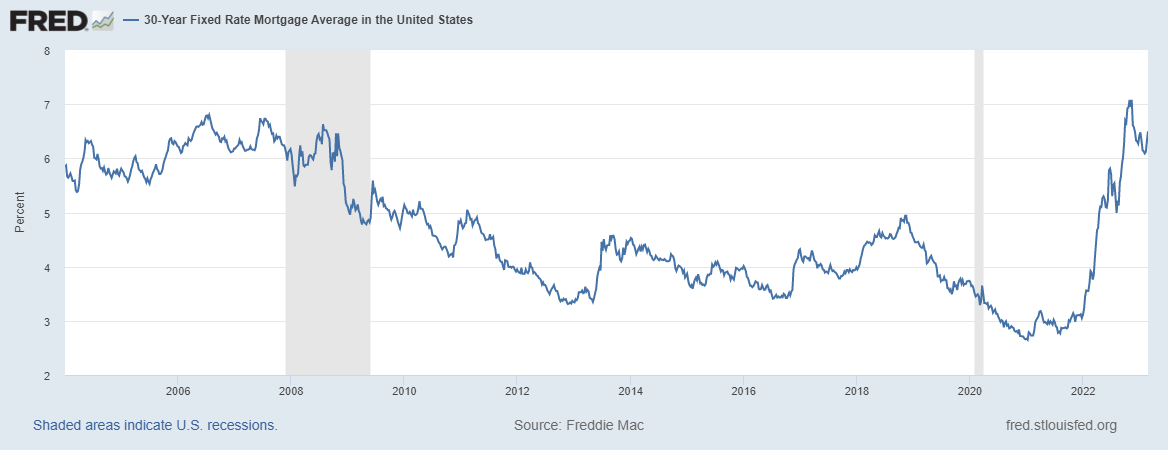

A stabilization in mortgage rates takes the pressure off the company to offer incentives to motivate sales. As mortgage rates reached a peak in Q4, CCS increased incentives to 900 basis points on closed homes. Going forward, the company expects to reduce the average level of incentives toward the historical norm of 300 basis points.

The 30-year fixed mortgage rate may have stopped going down for now but a peak may also be in place. (Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis, February 25, 2023.)

{kind=link}

For the full year 2023, Century Communities expects to deliver 7,000 to 8,000 homes. This volume is a whopping 24% to 34% below 2022’s 10,594 delivered homes, the company’s second highest level in its history. Century Communities guided to 2023 home sales revenues ranging from $2.6B to $3.1B, a substantial reduction from 2022’s record $4.4B (a 30% to 41% plunge).

The company anticipates Q1 2023 will be its lowest closing quarter of the year with growth resuming through the rest of the year. For the first and second quarters of 2023, Century Communities expects its deliveries to drop year-over-year. The company blamed delayed community openings, fewer homes started in the second half of 2022, and prioritizing sales of near-term deliveries in Q4. Deliveries will increase after Q2 2023.

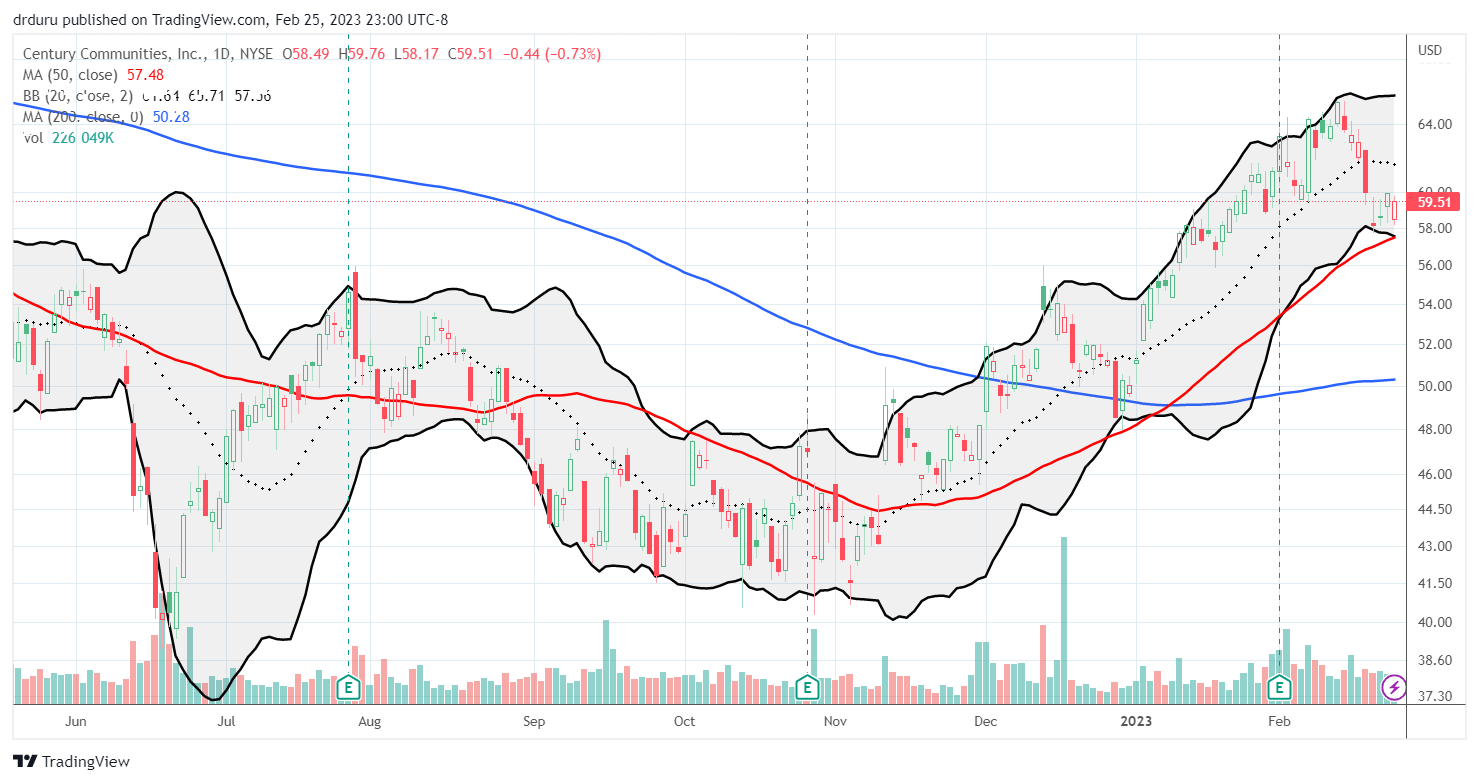

Typically, this kind of guidance can clobber a company’s stock price, especially a builder. However, investors seem satisfied with pricing in the worst of the housing recession back at the June and October lows. CCS fell 2.4% the day after reporting earnings. The stock has lost an additional 3.6% since then. CCS is still significantly out-performing the S&P 500 ( SPY ) year-to-date 19.0% versus 3.4%. CCS is also still holding an uptrend for the year. However, I think this uptrend is fragile, I do not expect it to hold if the market perceives an increase in hawkishness from the Fed and/or an economy-wide recession becomes imminent. The recent rebound in demand and sales is also providing a lift to CCS and other home builders.

CCS is clinging to an uptrend defined by its 50-day moving average (the red line above) (TradingView.com)

{kind=link}

Sales and Demand

The stock price is supported by the company’s successful navigation of the current housing recession and rapidly changing market conditions. Century Communities executed the playbook common across home builders . The company increased its cash position by concentrating its sales efforts and incentives on homes with near-term deliveries. This strategy paved the way to start homes with lower costs. The 2,903 homes delivered in Q4 was the company’s second-highest level ever. Century Communities hit its highest ever quarterly revenues with $1.2B in Q4.

Century Communities landed what it thinks is a plateau in cancellations at 37% in Q4. December cancellations fell to 28% in December and dropped more in January. Net new contracts of 1,258 dropped out of 2,008 gross contracts. The company blamed “an elevated cancellation rate, mortgage rate volatility and overall economic uncertainty keeping many potential homebuyers on the sidelines.” Sales improved from November through January. That recovery is reflected in the industry numbers: new single-family home sales have experienced a small rebound since last year’s lows.

New home sales hit a trough across lows in July and September, 2022. (U.S. Census Bureau and U.S. Department of Housing and Urban Development, New One Family Houses Sold: United States [HSN1F], retrieved from FRED, Federal Reserve Bank of St. Louis, February 24, 2023.)

Century Communities is well-positioned in this housing slowdown with approximately 81% of Q4 deliveries in homes priced below FHA (Federal Housing Administration) limits. This price range allows the company to “target the widest range of potential buyers in any given market.”

Balance Sheet

A strong balance sheet provides an element of confidence in Century Communities. The company achieved $382M in operating cash flow. This cash flow in turn helped reduce the net debt to net capital ratio to its lowest ever year-end level at 23.5%.

Century Communities “continued to step away from land deals throughout the second half of 2022 that no longer met our investment standards and that were generally higher in price than our owned lots.” The land pipeline fell by almost 27,000 lots and cut $650M in land acquisition commitments with a minimal $12M cost for abandonment.

After spending $120.6M repurchasing 2.3M shares (average share price of $52.32), Century Communities did not purchase any stock in Q4. The company still has authorization to repurchase 1.5M shares, but it did not provide guidance on any plans for drawing down on that allowance. I would be surprised if the company purchased more shares at current levels. However, this sizable authorization means that CCS should be a good buy in future sell-offs.

The Trade

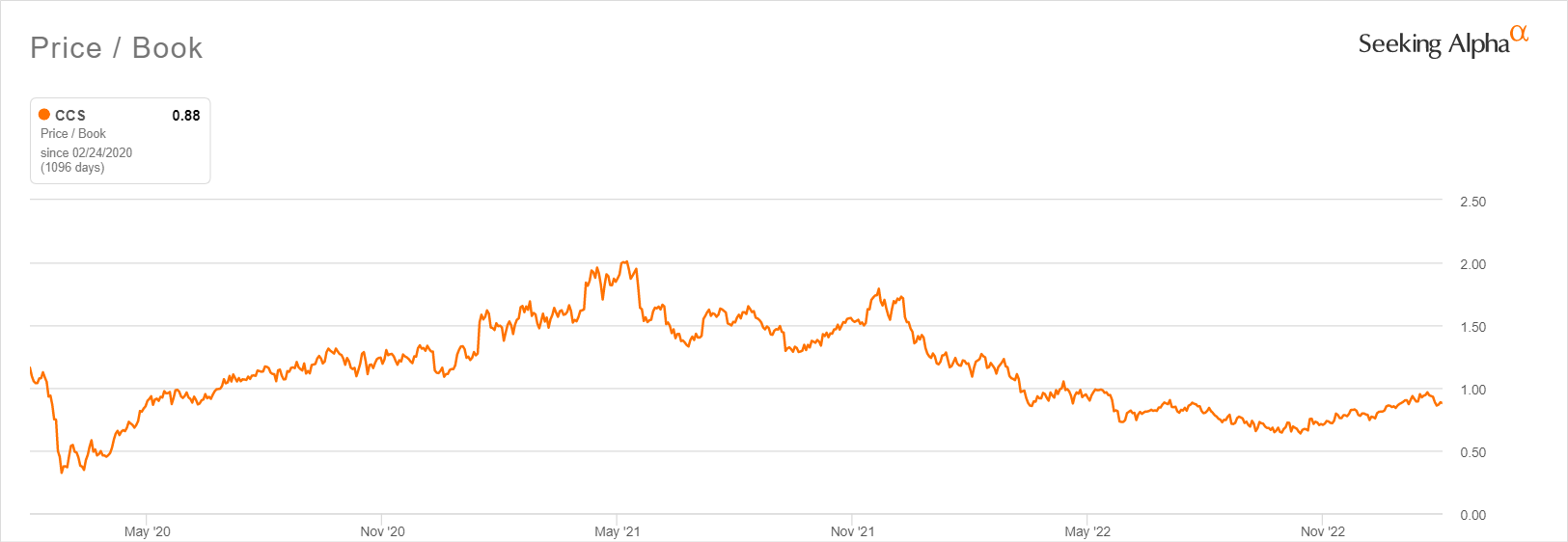

Century Communities continues to navigate industry challenges while maintaining a strong financial position. Its strategic sales decisions, cost reductions, improvements in cycle times, and strong balance sheet deliver positive indicators for the near-term future. While CCS has enjoyed sizable gains this year and since last year’s lows, the stock is still priced for a recession trading below 1.0 price/book.

CCS has traded below recession pricing of 1.0 price/book for almost a year. (Seeking Alpha)

{kind=link}

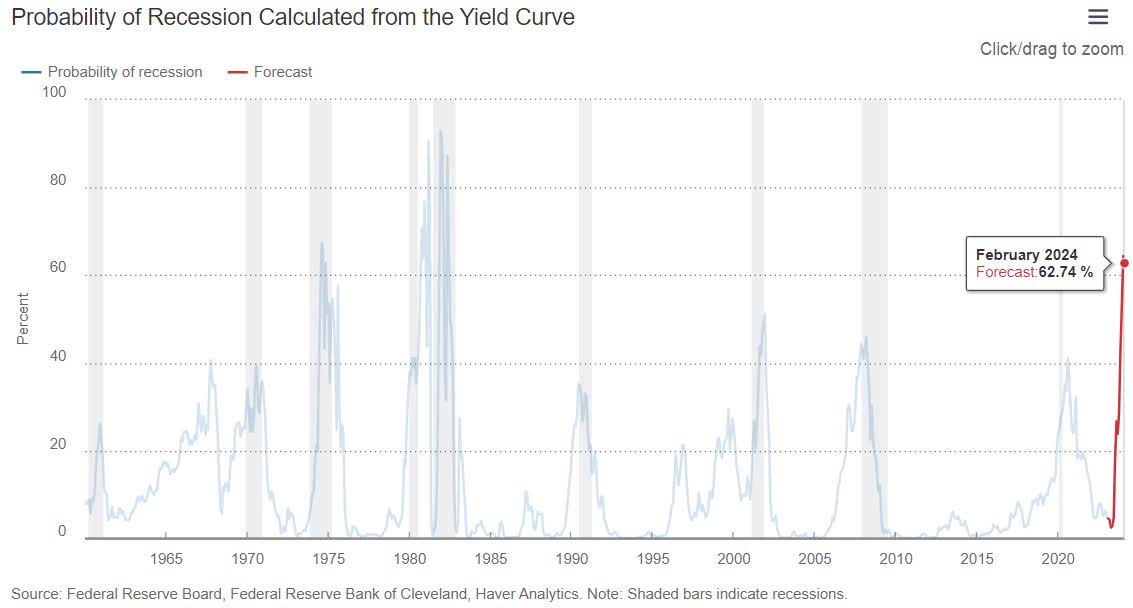

If not for the looming prospects for a recession , I would initiate a position at current levels.

The Fed estimates the odds of a recession to launch above 50% starting in December, 2023. (Federal Reserve Bank of Cleveland)

{kind=link}

Moreover, the seasonal trade on home builders will end soon (if it has not already ended). Thus, I am keeping CCS stock on my watchlist, but holding off buying for now.

Be careful out there!

For further details see:

Century Communities: Cautiously Optimistic After Navigating The Housing Recession