CA - CF Industries: Beneficial Market Condition And Better Than Peers' Performance

2023-07-06 13:00:00 ET

Summary

- CF Industries Holdings saw a significant increase in stock price and net sales in 2022 due to high ammonia and urea prices caused by the Ukraine war disrupting fertilizer supply.

- However, nitrogen product prices decreased in the second half of 2022 and first half of 2023, leading to a 30% YoY decrease in CF's net sales in 1Q 2023.

- I expect the company's 2Q 2023 financial results to be weaker than in 1Q 2023. However, it is not the result of bad performance or bad management.

- We have to accept the new market condition. However, CF still is able to benefit from it. CF's stock price is now 40% lower than its all-time high.

- Thus, despite weaker financial results in 2023 and lower fertilizer prices, CF Industries remains a good investment option due to increased production capacity and higher demand for ammonia.

Ammonia and urea prices reached very high levels in the first and second quarters of 2022, as due to the war in Ukraine, the supply of fertilizers was disrupted in a significant way. As a result, CF Industries Holdings (CF) stock price increased from $70 in January 2022 to more than $115 in August 2022. Due to higher prices, the company's net sales increased to $11.2 billion in 2022, from $6.5 billion in 2021, up 72% YoY. However, nitrogen product prices started decreasing in the second half of 2022 and plunged in the first half of 2023 (due to lower demand for fertilizers resulting from economic headwinds and oversupply of ammonia, UAN, urea, and other nitrogen products). Thus, in the first quarter of 2023, CF's net sales decreased by 30% YoY to $2.0 billion. It is important to know that CF's higher net sales in 2022 compared with 2021, and its higher net sales in 1Q 2023 compared with 1Q 2022, were mainly due to higher realized prices, and the company's sales volume didn't change in a significant way. CF's sales volume in 2022 was 1% lower than in 2021. Also, its sales volume in 1Q 2023 was 2% lower than in 1Q 2022.

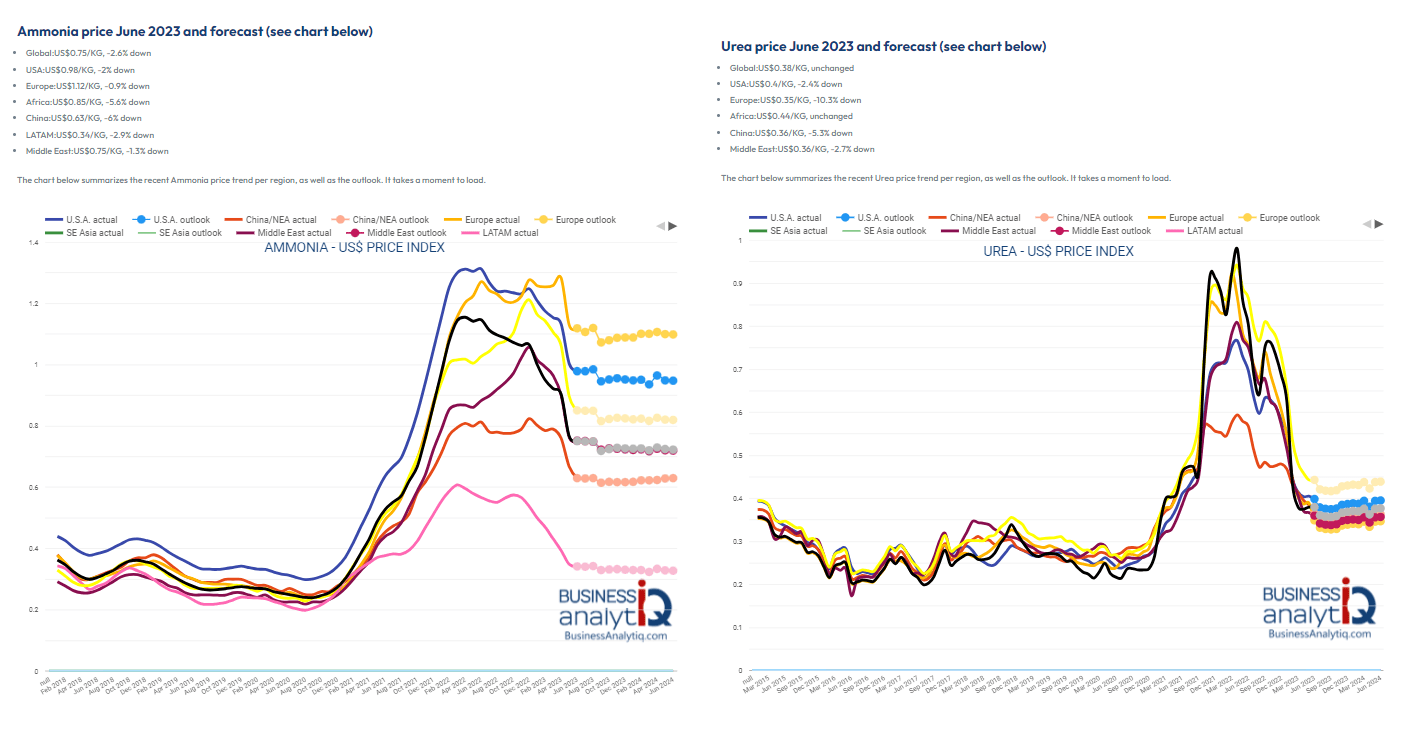

Nitrogen product prices in 2Q 2023, were considerably lower than in 2Q 2022, and also, lower than in 1Q 2023. The global ammonia price index decreased from $1.15/kg in June 2022 to $0.92/kg in March 2023 and decreased further to $0.75/kg in June 2023. Also, urea prices decreased from about $0.90/kg in June 2022 to $0.63/kg in March 2023 and decreased further to about $0.60/kg in June 2023. Furthermore, UAN32 prices decreased from about $0.72/kg in June 2022 to $0.51/kg in March 2023 and decreased further to $0.47/kg in June 2023 (see Figure 1 and Figure 2).

Overall, I estimate that CF's average selling price (the average of all segments) in 2Q 2023 can be 35% lower than in 2Q 2022, and 10% lower than in 1Q 2023. As a result, the company's net earnings attributable to common stockholders in 2Q 2023 can be 50% to 60% lower than in 2Q 2022, and 10% to 15% lower than in 1Q 2023. As a result of weaker results in 1Q 2023, and lower fertilizer prices in the second quarter of 2023 (which means lower earnings for 2Q 2023), CF stock price decreased from $85 at the end of 2022, to below $70 in July 2023.

Yes, I don't expect CF's earnings to get close to their levels in 2022 for now. However, weaker-than-2022 financial results do not mean necessarily that CF is not a good stock to buy. We have to accept that the high fertilizer prices are gone, and it would be irrational to expect them to come back. This is why CF stock is 40% lower than its all-time high in August 2022. Now, it is time to see what CF can do at the current fertilizer prices.

In the first quarter of 2023, CF signed a definitive asset purchase agreement with Incitec Pivot Limited (IPL) for IPL's ammonia production complex located in Waggaman, Louisiana, for $1.675 billion. The facility has a nameplate capacity of 880,000 tons of ammonia annually. Thus, the company's production capacity is now higher, and now, the company can benefit more from higher demand for ammonia. The United States Department of Agriculture estimates 94.1 million acres of corn planted in the United States for 2023, up 6% from last year (and also, 2% higher than the United States Department of Agriculture's previous estimation that was mentioned in CF's 1Q 2023 results). Also, the United States Department of Agriculture estimates wheat planted area for 2023 at 50 million acres, up 9% from last year. In the second half of the year, CF Industries expects higher urea imports into India and Brazil, and a higher-than-normal level of nitrogen imports into Europe (as a result of lower-than-normal ammonia operating rates in Europe). On the other hand, due to Chinese government measures to limit the exports of fertilizers, to control domestic prices, urea exports from China are expected to remain lower than the previous years. Finally, as a result of continuing geopolitical tensions in Europe, exports of ammonia from Russia are expected to remain lower than before the war (due to the closure of the ammonia pipeline from Russia to the port of Odessa in Ukraine).

However, it is important to know that now Russia and Belarus are trying to export their fertilizer products. In fact, except ammonia, the exports of other nitrogen products from Russia are at pre-war levels, as countries like the United States and Brazil have not applied sanctions on Russian fertilizer. It is important to know that currently, EU member states are also authorized to grant Russian-flagged vessels access to EU ports, as well as to grant Russian road carriers entry to the EU for the purposes of importing or transporting agricultural products, including fertilizers and wheat, that are not subject to restrictions. As a result, the kind of fertilizer price estimations that anchor their argument for higher fertilizer prices to the war in Ukraine, may not be reliable as they seem to be.

Figure 1 - Ammonia and urea prices according to businessanalytiq.com ($/kg)

{kind=link}

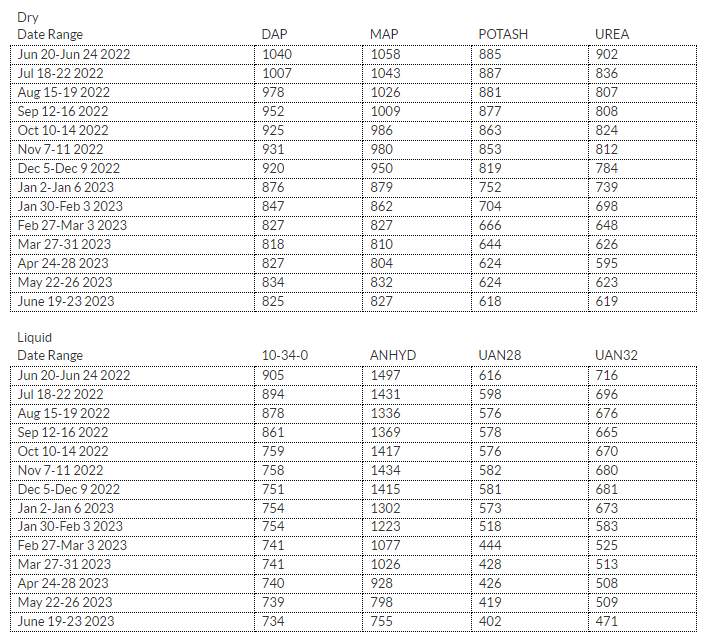

Figure 2 - Fertilizer prices according to dtnpf.com ($/ton)

{kind=link}

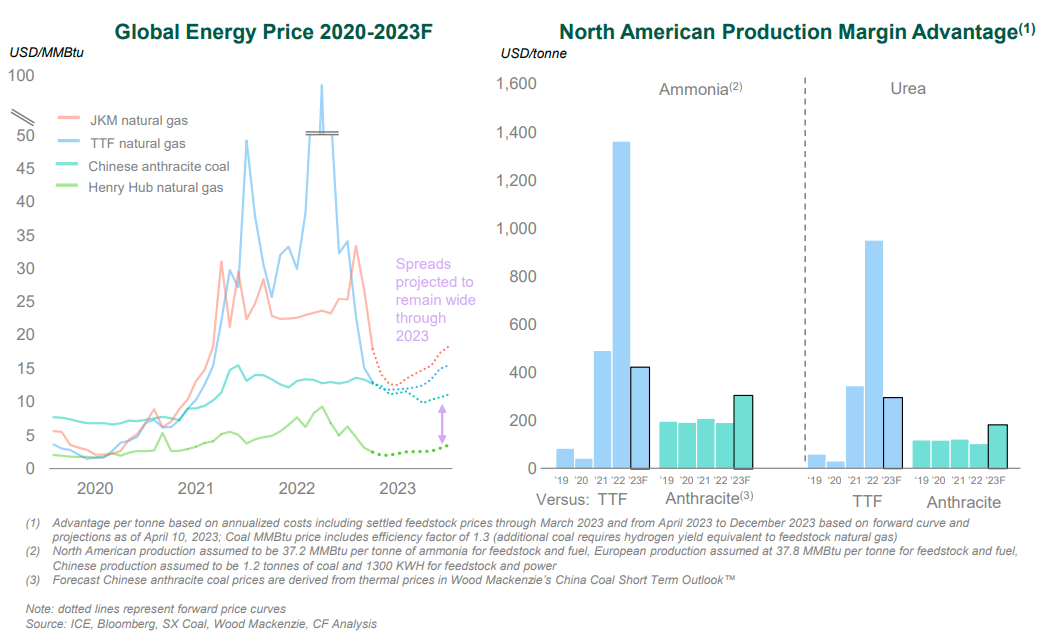

According to Figure 3 , the current energy forward spreads support North American margins advantage in 2023 compared to Europe and Asian producers. We can see that the North American ammonia and urea production margin advantages compared to Europe and Asian producers in 2022 were significantly high. In 2023, the North American ammonia and urea production margin advantages compared to European producers decreased to below 2022 and 2021 levels; however, it is still higher than in 2019 and 2020. But the North American ammonia and urea production margin advantages compared to Asian producers in 2023 are higher than the previous year, implying a great opportunity for CF's urea segment.

Figure 3 - North American production margin advantage

{kind=link}

Comparison with the peers

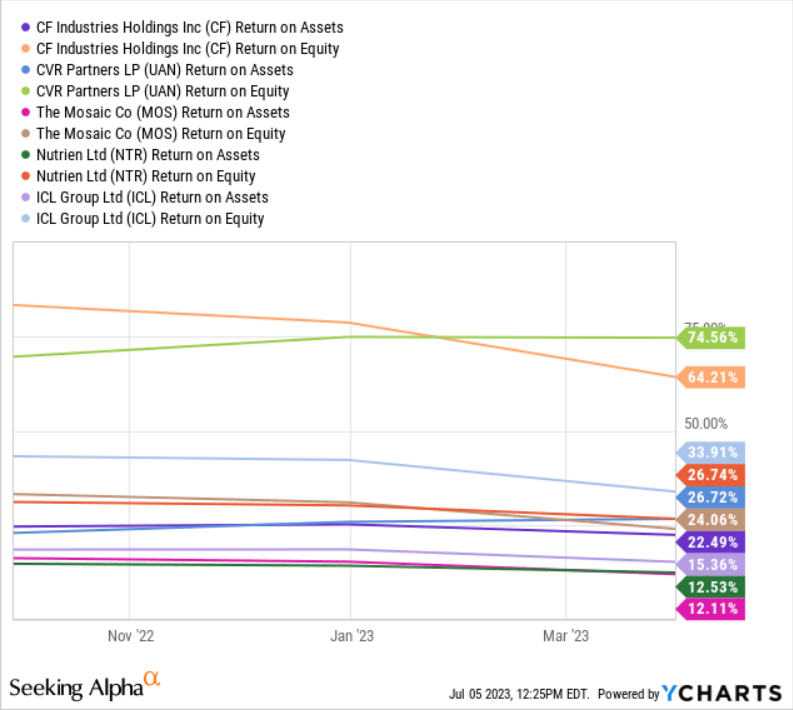

CF's return on equity ((ROE)) is significantly higher than the ROE of The Mosaic Co ( MOS ), Nutrien ( NTR ), and ICG Group ( ICL ). However, its ROE of 64.21% in 1Q 2023, is lower than CVR Partners ( UAN ) ROE of 74.56% (see Figure 4). Also, CF's return on assets ((ROA)) of 22.49% is higher than the ROA of ICL Group, Nutrien, and The Mosaic. However, the company's ROA is lower than CVR Partners. Overall, in terms of ROA and ROE, CF is in a better position compared to its peers, except CVR Partners. Be mindful that CVR Partners has a market cap of less than $1 billion, while CF has a market cap of more than $13 billion. MOS, NTR, and ICL have market caps of $12 billion, $30 billion, and $7 billion, respectively. My point is that CVR Partners' higher ROE and ROA, cannot simply mean that it is a better stock than CF, as they are significantly different in terms of size. WE can see that despite this deference in size, CF, with a market cap of $13 billion, has a close ROE to CVR partners, with a market cap of less than $1 billion.

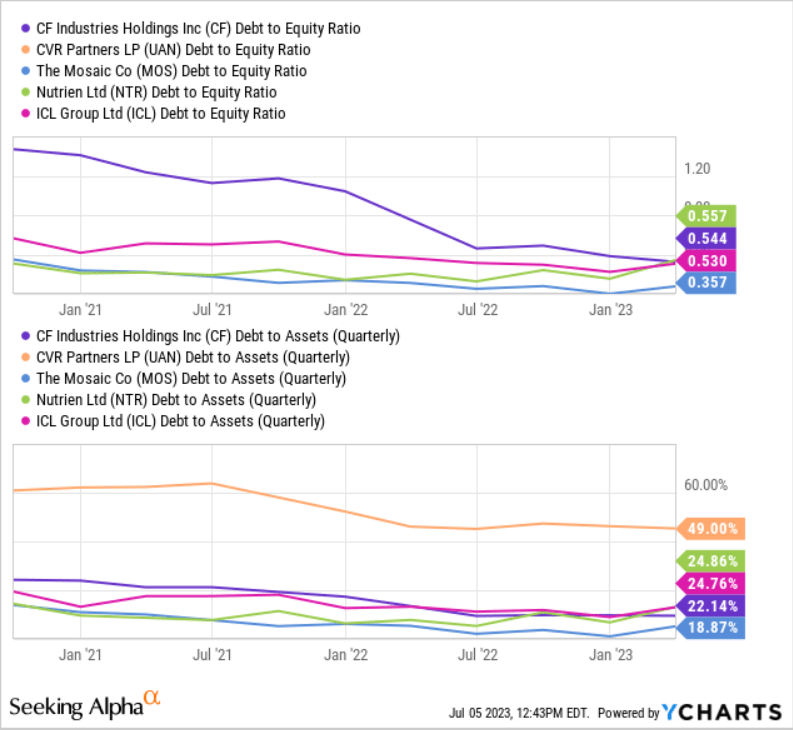

According to Figure 5, CF Industries has been able to decrease its debt-to-equity ratio and debt-to-assets ratio in the past few quarters, implying that the company paid a significant part of its debt in the past two years. We can see that CVR Partners has a debt-to-assets ratio of 49%, which is significantly higher than CF's. It implies that in terms of the debt position, CF is in a much better position. It is important to know that CF's debt-to-assets and debt-to-equity ratios are not as good as The Mosaic Co's. However, at its current pace of debt repayment, CF's debt position is expected to improve further.

Figure 4 - CF's ROE and ROA vs. peers

{kind=link}

Figure 5 - CF's debt-to-equity and debt-to-assets ratios vs. peers

{kind=link}

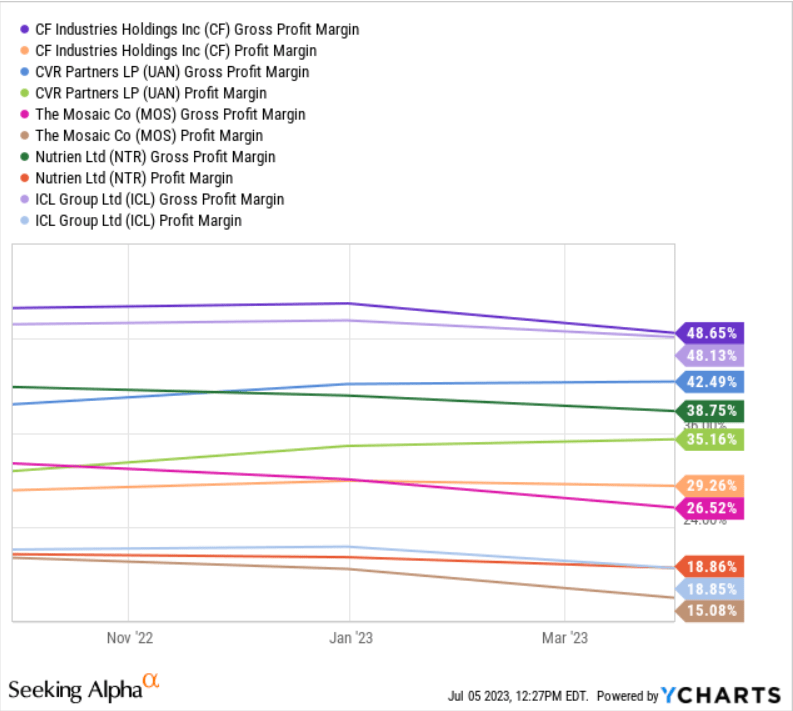

According to Figure 6, CF has a gross profit margin and a net profit margin of 48.65% and 29.26%, which are higher than all the peers, implying that CF is doing better in turning its revenues into profit. A great part of the fertilizer producer companies' expenses are linked to their natural gas costs. CF's higher gross profit margin means that the company has been able to control its costs through favorable contracts and natural gas derivatives, better than its peers.

Figure 6 - CF's profit margins vs. peers

{kind=link}

End note

Fertilizer prices dropped significantly in 1H 2023, CF's financial results in 2023 can be much weaker than in 2022. However, the stock's price is now 40% lower than its all-time high in August 2022. Fertilizer prices are not expected to jump in the following months. But, the demand for fertilizers in 2H 2023 can be higher than in 1H 2023, and CF can benefit from the still favorable market condition. Overall, at the current fertilizer prices, CF can remain profitable, and reward its shareholders. Thus, at its current stock price of about $70 per share, CF might be a good option. Furthermore, compared to its peers, in terms of ROA, ROE, debt-to-equity and debt-to-assets, and profit margins, CF is in a good position. The stock is a buy.

For further details see:

CF Industries: Beneficial Market Condition And Better Than Peers' Performance