CA - CGI: Charting The Future Of Digital Transformation With Superior Profitability And Greater Resilience

2023-11-03 07:52:10 ET

Summary

- CGI has a strong business model, with a global presence, substantial scale, a suite of related services, and deep expertise. It represents a compelling offering for large multinationals/Governments, and smaller ones.

- The technology industry is, and has always experienced several tailwinds that allow it to maintain strong growth decade-on-decade, with the likes of AI and Cloud being key drivers going forward.

- The company has an impressive backlog of ~2x FY22 revenue, ensuring its growth in the coming years will be strong despite the macroeconomic conditions.

- CGI performs well relative to its peers, with superior profitability and greater resilience expected in the coming year. This outperformance is enhanced by its consistency historically and competitive advantage.

- CGI’s valuation is attractive without screaming undervalued. Given its history of buybacks and financial progression, the stock is unlikely to ever be cheap.

Investment thesis

Our current investment thesis is:

- CGI is a high-quality compounder in our view. Management has shrewdly developed a globally competitive business with a diversified array of services. This has allowed it to operate above-average margins and achieve consistent growth, funding aggressive buybacks.

- Looking ahead, we see industry tailwinds and its competitive position driving a small step-up in growth, contributing to enhanced returns. We do not believe this is wholly priced in, implying an upside. Given CGI is better placed than its peers on a financial basis, we see it as a good investment at today's price.

Company description

CGI Inc. (GIB) is a leading Canadian IT and business consulting services firm, providing end-to-end IT and business process services to clients worldwide. With a focus on innovation and client satisfaction, CGI has established itself as a key player in the global technology industry.

Share price

CGI's share price performance has been good during the last decade, with over 190% returns. This lands marginally above the S&P. This is a reflection of its positive financial development and an improvement in investor sentiment about its long-term trajectory.

Financial analysis

{kind=link}

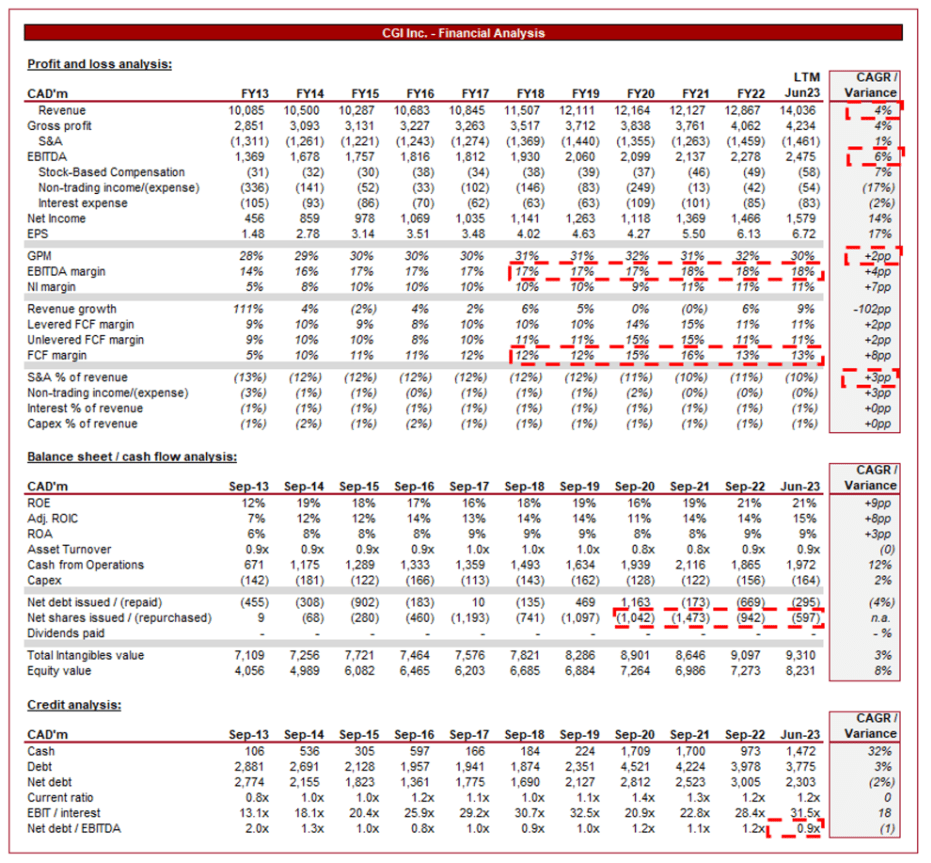

Presented above are CGI's financial results.

Revenue & Commercial Factors

CGI's revenue has grown at a CAGR of +4% during the last decade, with broadly consistent year-on-year gains. EBITDA has exceeded this, with a CAGR of +6%.

Business Model

{kind=link}

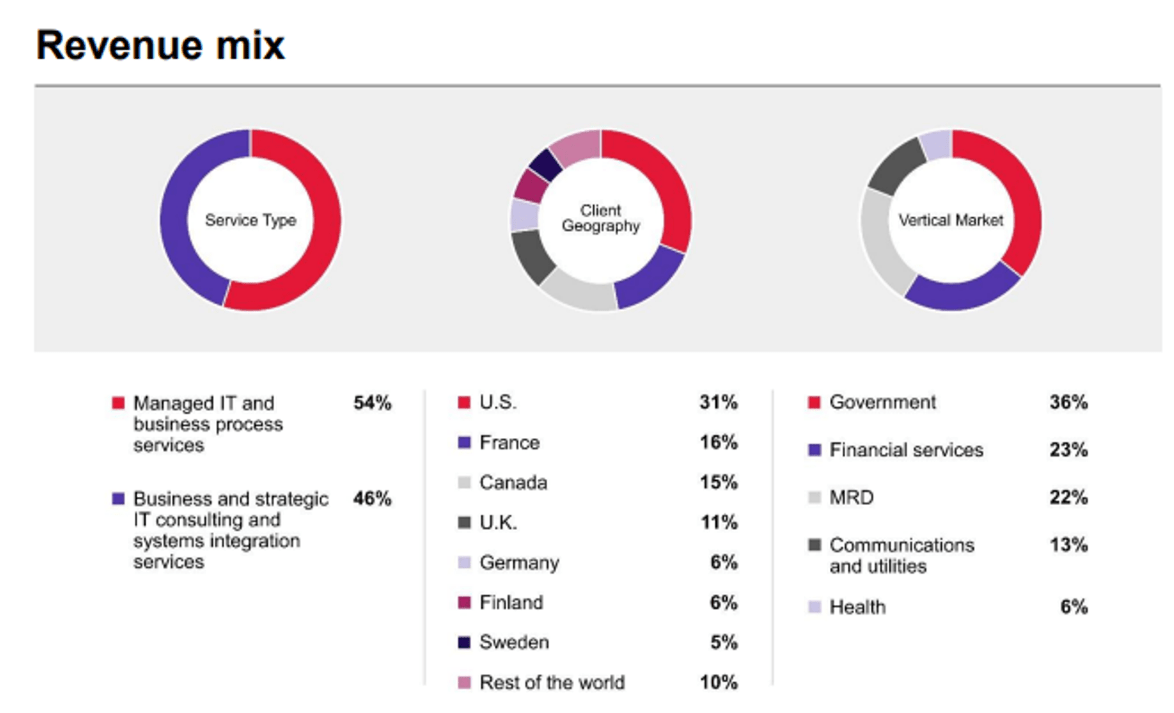

CGI provides a wide array of IT services, including software development, systems integration, IT outsourcing, and consulting. It caters to a wide variety of industries, offering tailored solutions to meet specific business needs based on historical industry-specific capabilities development. Currently, the company is heavily weighted toward Government and Financial Services, both of which are relatively less developed technologically and lend well to long-term contracts with ongoing support.

Unlike many of its smaller peers, CGI offers end-to-end IT solutions, from consulting and strategy planning to implementation and maintenance. This comprehensive approach ensures that clients can rely on CGI for the entirety of their IT requirements and the assurance that delivery is as expected. For CGI, this allows for multi-year contracts and backlog development, relieving pressures to win contracts.

In addition to consulting, Managed IT is a key service. This includes managed IT services, including IT infrastructure management, application support, and cybersecurity monitoring. These services ensure the smooth operation of clients' IT systems while enhancing security and efficiency. The upgrade process to IT infrastructure has been a key growth driver over the last two decades, with demand remaining strong due to consistent technological development and the need for ongoing support following infrastructure installation (management).

Despite its size, CGI continues to invest in R&D, allowing it to innovate and develop new capabilities to ensure it remains at the forefront of technology. Its innovative solutions not only attract new clients but also encourage existing clients to engage in additional projects. Historically, uptake of technology has been slow, in part due to prohibitive costs but we are expecting this to speed up due to technology progressively becoming more impactful in the improvements generated.

CGI operates globally, serving clients across various continents. Its international presence allows it to tap into a larger pool of potential customers, while also opening the company up to cross-border projects for multinationals.

CGI has strategically acquired companies that complement its existing services, both vertically through greater expertise and horizontally to deepen its industry exposure (>$2b spent in the last decade). M&A continues to represent a key opportunity to maintain its competitive position and further increase its attractiveness as an overall package.

Digital Consulting Industry

The technology industry is everchanging, with the following trends critical to CGI's long-term trajectory:

- Long-Term Partnerships - CGI focuses on building enduring relationships with its clients and has positioned its services suite to encourage this. This is underpinned by consistently delivering high-quality services and demonstrating reliability. With an increased desire to adopt digital technologies across industries and the requirement to do so to maintain and enhance competitiveness, we see strong demand for IT services.

- Adapting to Market Trends - CGI must stay agile and adapt quickly to market trends. Not only this but it must anticipate changes in technology and the business landscape to create/have ready solutions for early adaptors, positioning itself to offer services aligned with emerging needs and issues businesses may not know they have.

- AI - GenAI represents a significant opportunity to drive revenue growth in the coming years, as businesses seek to utilize the technology to improve back-end efficiency and better commercials. Although this is early doors, the technology certainly appears universal and powerful enough to drive value.

- Aside from AI, we consider the following two data capabilities as key growth drivers.

- Cloud Services - The cloud service revolution has been substantial, as costs have declined. In a global data-driven world, the value provided by Cloud is substantial and we believe this will mean strong demand in the coming years as businesses of all sizes seek integration.

- Data Analytics - There is an increased focus on data-driven decision-making, as businesses of all sizes and industries realize the value that can be achieved through the collection, analysis, and tracking of data.

- Market Saturation - The attractiveness of the industry has contributed to intense competition, leading to pricing pressures and potential margin erosion. Realistically, we see the primary effect being growth restriction. Key competitors include IBM ( IBM ), Big Four Accounting firms, Capgemini ( CAPMF ), Cognizant ( CTSH ), and Accenture ( ACN ).

Margins

{kind=link}

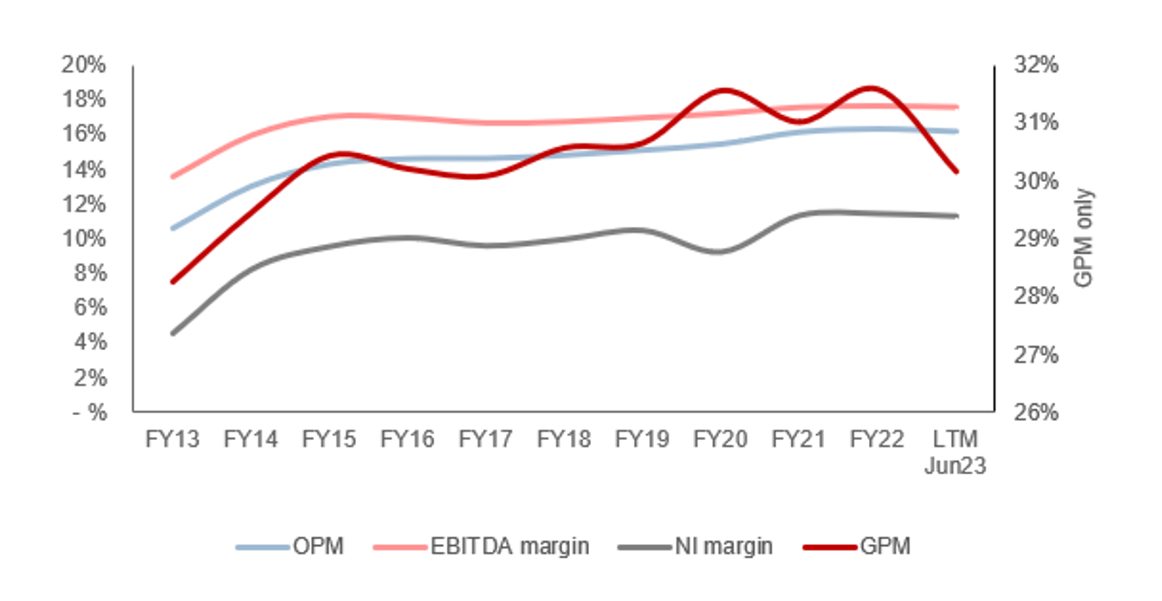

CGI's margins have broadly traded flat during the last decade, with only a step up in the post-pandemic period. This lack of improvement is not surprising given the labor-intensive nature of its services. Beyond a point (usually far smaller than its current size) x number of employees will be required to deliver y amount of additional revenue, with small variability to this level.

Looking ahead, we expect margins to remain broadly flat (very small improvements as seen historically), as the company's competitive position is not materially being challenged. The scope for improvement will come with technological innovation at some point in the future. AI could be the catalyst but this remains to be seen.

Quarterly results

CGI's recent performance has been strong, stepping up relative to prior quarters. Its top-line revenue growth was +8.0%, +11.6%, +13.7%, and +11.2% in the last four quarters. In conjunction with this, margins have continued to step up, with three successive quarters of >19.5% EBITDA-M.

This growth is a reflection of a combination of factors. Firstly, the company has benefited from FX conversion, with its constant currency growth in the most recent quarter being ~6.3%. Secondly, CGI is benefiting from acquisitions, with >$500m spent in FY22 (contributing to full-year spill-over). Finally, the company is delivering well against its objectives. This is impressive as with weaker macroeconomic conditions, the fear is that corporates will cut back spending as a means of protecting margins, as they face both inflation and weakening demand.

Key takeaways from its most recent quarter are:

- CGI attributes its resilient financial performance to its diverse portfolio of geographies, services, and industries.

- Further, margin improvement has been achieved through a combination of a focus on higher-margin services and operational discipline.

- Bookings were $4.4b, up +29% YoY, representing a book-to-bill ratio of 121.1%. CGI's current backlog stands at $25.6b, which represents ~1.99x FY22 revenue. This should ensure the company can maintain its growth if demand does fall.

- The strong bookings are driven by its managed services and IP solutions, with particular strength in the government and financial services sectors.

Balance sheet & Cash Flows

CGI's balance sheet is incredibly clean. The company is conservatively financed, with a ND/EBITDA ratio of 0.9x. This provides the business with the optionality to ladder its debt up for distributions or fund further acquisitions.

This has allowed the company to maximize its FCF returns, which similar to profitability have been impressively consistent. Management has aggressively repurchased shares to utilize this excess capital, with diluted average share count declining ~24% during the last decade.

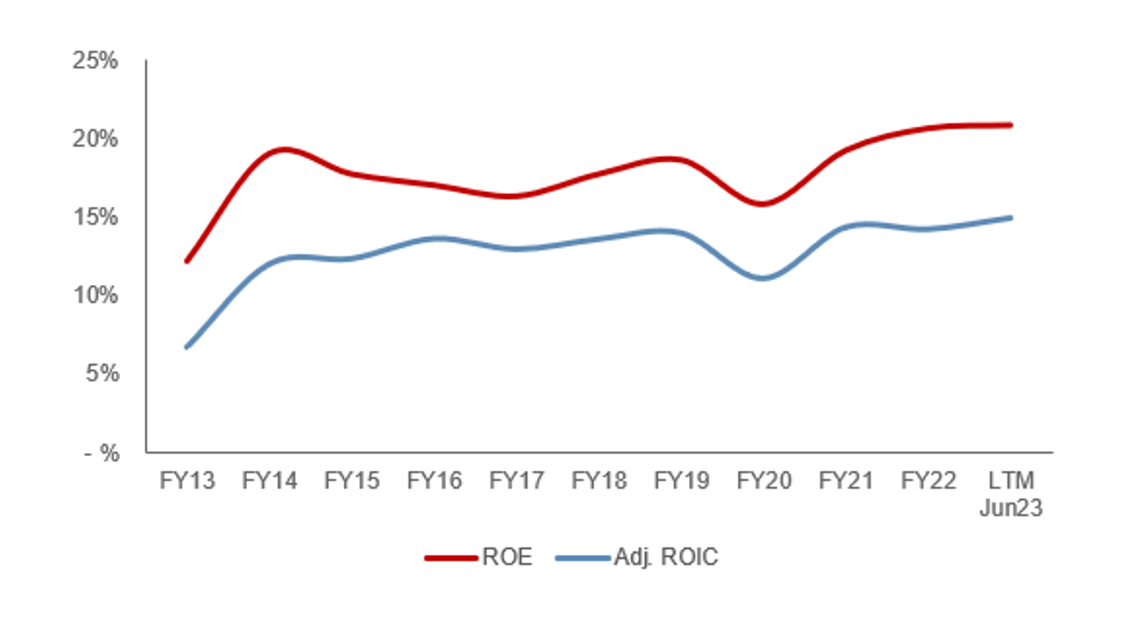

This strong consistency has allowed CGI to operate an attractive ROE, which has trended up as shares have been repurchased and profitability has nudged up (also reflecting no acquisitions have been margin and ROE dilutive, which is critical and forgotten by many management teams). This current level is highly attractive in our view and sufficient to imply a continuation of its strong returns.

{kind=link}

Outlook

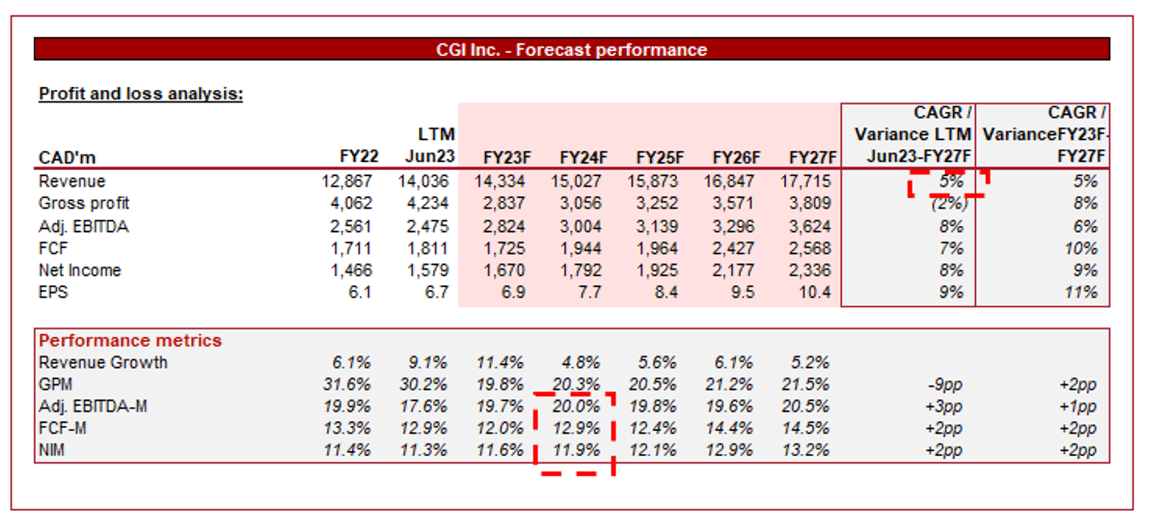

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a small sequential improvement in its growth trajectory, with a CAGR of 5% into FY27F. In conjunction with this, margins are expected to remain broadly flat.

The growth forecast appears reasonable in our view, with tailwinds contributing to an improvement in the industry's outlook. As previously discussed, margins are likely to remain flat barring significant innovation.

Industry analysis

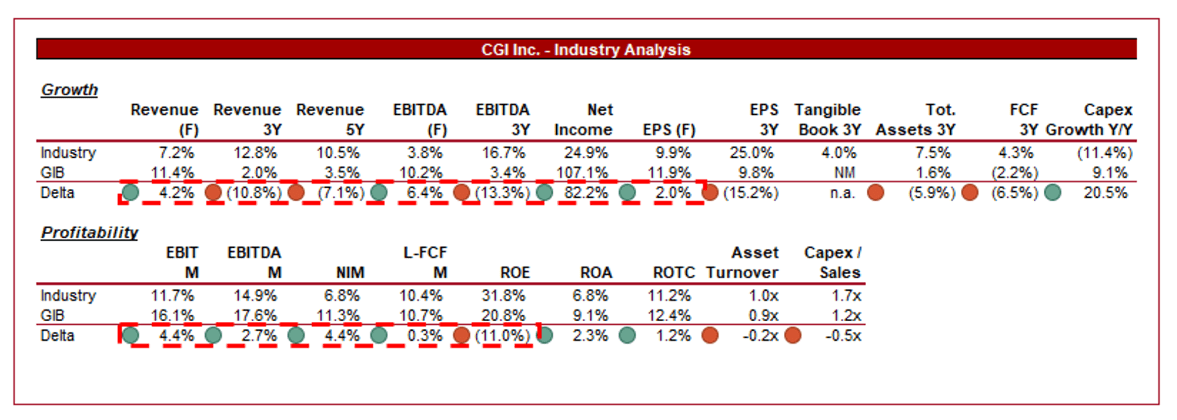

{kind=link}

Presented above is a comparison of CGI's growth and profitability to the average of its industry, as defined by Seeking Alpha (21 companies).

CGI performs exceptionally well relative to its peers. The company's key strength is its margins, with a positive delta across the majority of its metrics. The business does have a lower ROE but this is artificially deflated by the buybacks. This margin strength is a reflection of CGI's strong geographical presence and expansive service offering, allowing for a highly competitive value proposition for clients.

The company has lagged behind in growth but this is primarily a metric that is inflated by smaller growth businesses. CGI is a mature company that will struggle to achieve the absolute gains necessary. The strength of its resilience translates against peers as well, with revenue and profitability outperformance.

Valuation

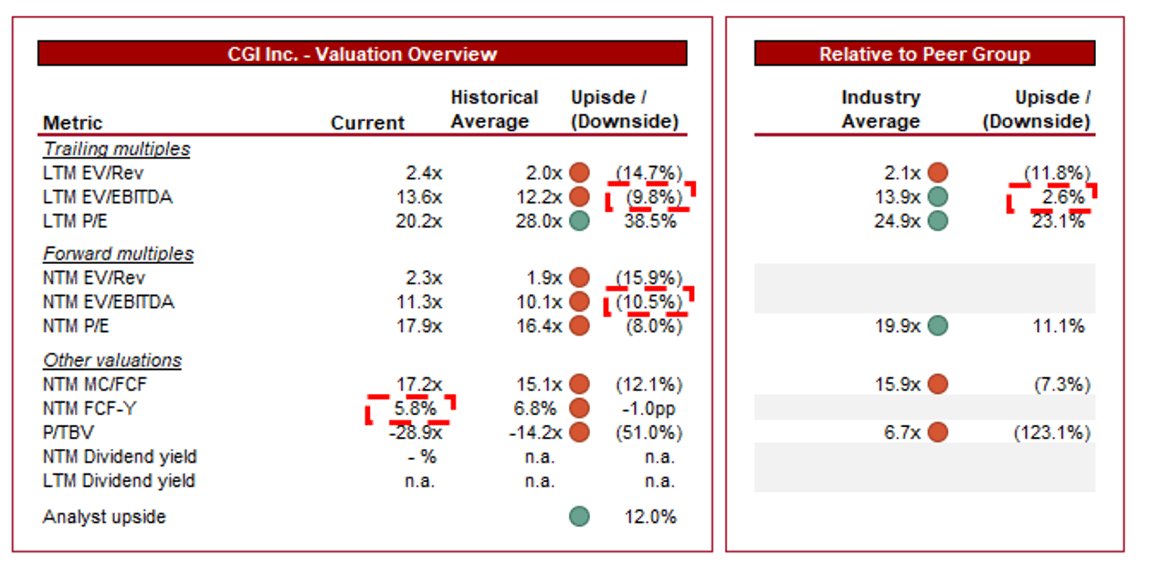

{kind=link}

CGI is currently trading at 14x LTM EBITDA and 11x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is warranted in our view, owing to the company's margin improvement, additional business model development, and improved growth outlook. At a ~10% (EBITDA) premium, we believe there is a further upside (~1% EBITDA improvement + ~2% increase in annual growth rate).

Further, CGI is trading at a small discount to its peers (~3% on an LTM EBITDA basis and ~11% on a NTM P/E basis). A discount is not justifiable in our view, owing to the company's impressive financial strength and scope for outperformance in the coming year. This implies a 3-10% upside immediately, plus a reasonable premium in our view (~10%).

Based on this, we see an upside of 10-20% at the current share price.

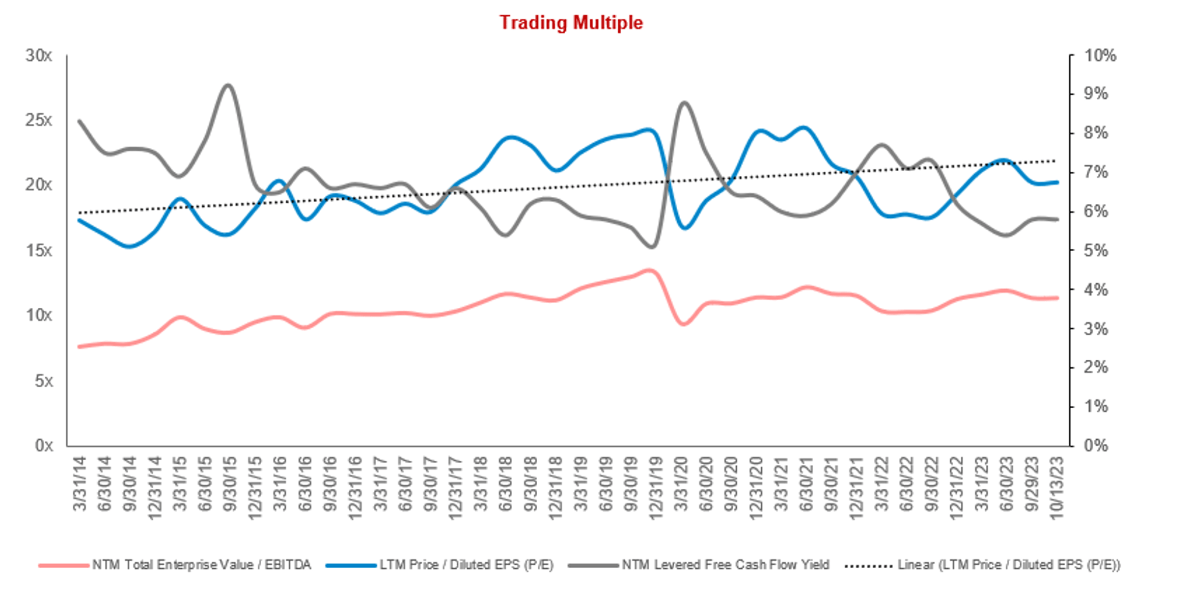

CGI's valuation has consistently trended up during the last decade, supporting investors' improving outlook of the company. With both its LTM P/E and NTM EBITDA below their respective linear trajectories, reiterating it is undervalued. The only indicator lacking in our view is the NTM FCF yield, which is highly attractive at ~6% but not in line with (ideally) below its historical average (~7%).

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Economic downturns.

- Failure to adapt to emerging technologies.

- Market share erosion due to aggressive pricing competition during these weaker market conditions.

Final thoughts

CGI is a high-quality business in our view. Its global reach, broad services suite, and deep expertise, in conjunction with its brand and scale to deliver means that it is a compelling option for businesses/governments of all sizes globally. This is a proposition that very few can match within the industry.

These characteristics are reflected in its relative performance to peers, with superior margins and respectable growth.

There are numerous tailwinds and many more that we have yet to identify that will help drive industry growth, we are not at all concerned by this. CGI's scale and M&A capabilities mean that the risks associated with failing to respond are limited, as it can spend its way out of falling behind.

With continued buybacks and a reasonable valuation, we see this stock as a buy.

For further details see:

CGI: Charting The Future Of Digital Transformation With Superior Profitability And Greater Resilience