CA - CGX Energy: A Fly On The Wall In The Data Room

2023-07-19 07:00:00 ET

Summary

- In this article, we bring readers up to date on the CGX Energy/Frontera Energy Corentyne prospect, offshore Guyana.

- Christine Guerrero, AKA "SheDrills" sits down with us to unpack recent technical data released by the company and offers some interpretations. It should be a tech-fiend investors delight.

- We will also discuss ways to play what looks like a huge discovery, with multi-billion dollar payouts in the offing.

- Positions in either Frontera or CGX come with above average risk, and only very risk tolerant investors should consider it. We are long CGX and would buy more at a lower price.

Introduction

The Frontera Energy, (FECCF) and CGX Energy, (CGXEF) joint venture-JV, have two legitimate discoveries in the northern end of the Corentyne block, offshore Guyana. With the just completed, year-long campaign drilling the discovery well, Kawa#1, and the confirmation well, Wei#1, the JV have established a petroleum system inside the " Golden Lane ," set forth in the slide below. Nearly twenty Exxon Mobil, ( XOM ) discoveries inside this lane, and to a lesser extent the Apache Corp, ( APA ), and TotalEnergies, ( TTE ) discoveries offshore Suriname have made this the most productive exploration basin in the world.

CGX Corentyne block (CGX)

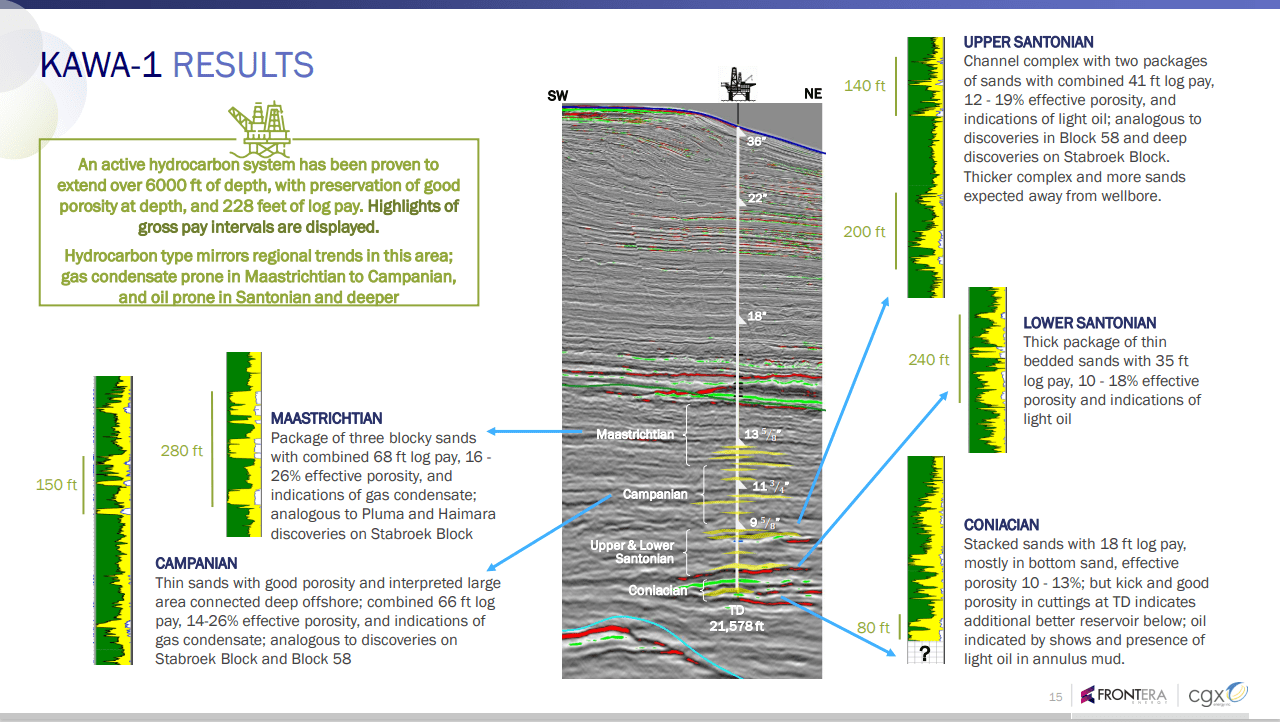

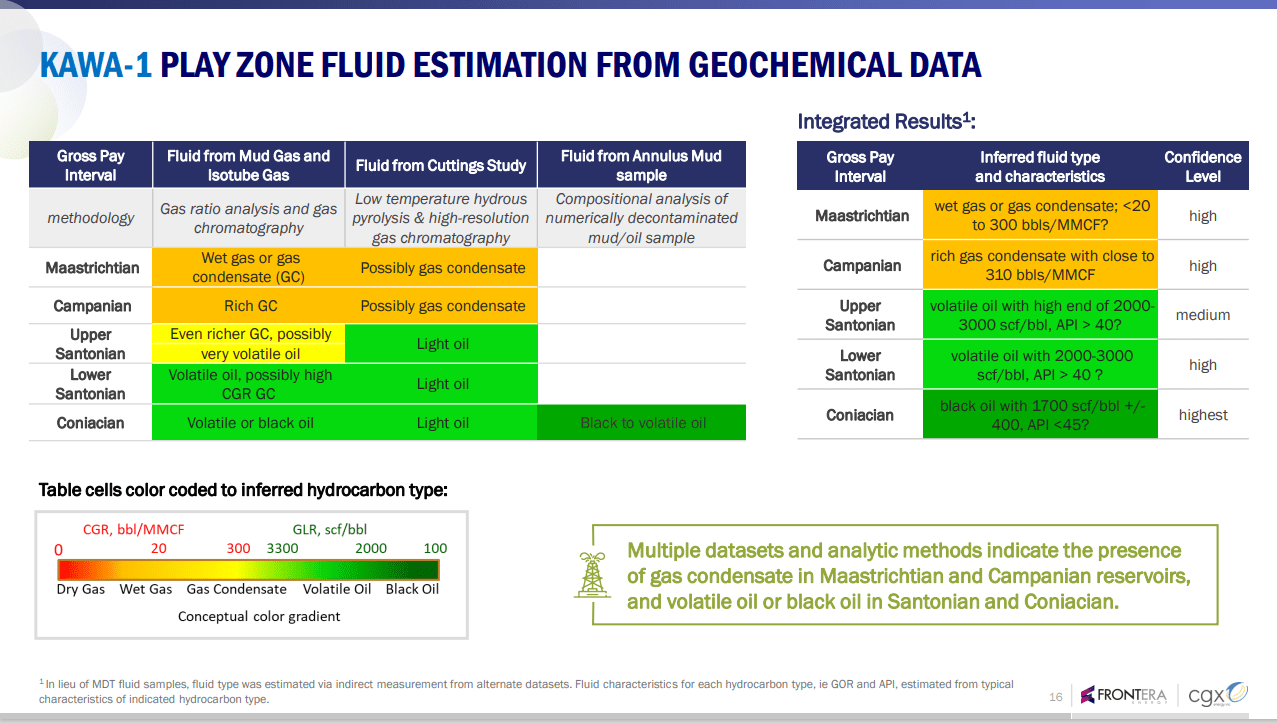

With the Press Release on the Wei, at the end of June, CGX, the operator of these two wells confirmed they had cut a combined footage of pay through the Maastrichtian, Campanian, and the Santonian stratas, of 287', with 210' being in the Santonian. All with light to medium oil shows. Logs and cores are now with an analyst lab for a complete geochemical and rock properties workup.

The world holds its collective breath for the next several months while this process unfolds.

A 30,000' overview of CGX and FECCF.

I've done several articles on CGX- the operator of this concession and link them here for your review. I've also done one on Frontera Energy, and you can find it here .

CGX Energy is the concession holder which is the reason probably they still exist. Guyana gave some very generous terms when trying to stimulate interest in these blocks years back, and new concessions will not be so generous, as noted in this summary of the current bidding round. CGX has no revenue to speak of, and has had to give up a big chunk of their percentage in the block to Frontera in exchange for a capex carry on these two wells. Drilling in deepwater isn't cheap! In addition to the development of the Corentyne block, CGX is developing a deepwater port and supply base, on the Berbice river. CGX latest filings have " Going concern " language that highlights the risk investors are taking with their shares. They also owe their JV partner Frontera $11-15 mm based on their remaining 32% of the block, for costs associated with the delays on the well. Money they don't have and are trying to raise. There is a very likely prospect of a capital raise with new shares coming to the market, which of course will dilute current shareholders. The current low price of CGX shares attenuates that risk somewhat, but not entirely. Currently there are 337.2 mm shares outstanding.

Frontera Energy has been fronting costs associated with drilling these two wells, and as of their most recent reports and filings are well capitalized. In Q-1, 2023 they show $1.3 bn in revenues, ~$800 mm in EBITDA, $500 mm in LT debt, and have $162 mm of cash on the books. Worth noting is the decline in their cash balance from a year ago, from $257 mm to the present $162 mm. As I said, drilling in DW isn't cheap. That's the easy stuff with Frontera. It gets a little murky when you peak under the covers.

Catalyst Capital a large Private Equity-PE, firm based in Toronto, Canada, holds 40.8% of Frontera, and the Managing Director of Catalyst, Gabriel de Alba is the Chairman of the Frontera Board. Got all that? It gets better. Catalyst is looking to offload Frontera , as of Q-2 of this year (although the linked article suggests this desire goes back a ways.) Now since Frontera owns 76% of CGX we might see a reason why CGX would avoid a cap raise. And a reason why Frontera simply can't let CGX go bankrupt. The value in CGX lies in the Petroleum Prospecting License-PPL it holds, the value of which could come into question were CGX to fail.

Summing all of this up. As I've noted in past articles, whatever happens with Frontera or CGX, one thing is clear. They are at a standstill and need a Big Daddy. Stay tuned for more info here.

An interview with "SheDrills," aka Christine Guerrero

Christine is an experienced drilling engineer and economic advisor with about 20 years of experience. She listed a few of her stops along the way in our conversation. Schlumberger and Precision Drilling as a LWD Engineer, Chevron as a Senior Drilling Engineer and Decision Analyst, Hess as an Exploration Planning Advisor, and then to her own company. Christine has just the right experience to give us an inside look at the Corentyne prospect and what may lie next for Frontera and CGX Energy.

Fluidsdoc- Thanks Christine for taking some time today. I was interested in speaking to you because you've got the knowledge to back up your opinions. So let's start with your assessment of the Corentyne prospect itself and why should Exxon, Total, Hess, Apache or others be interested in becoming the "Big Daddy" here?

Christine - As you know, the Corentyne license extends into the Golden Lane, all you have to do is fly over that location and see where all the discoveries are from Stabroek leading into block 58. And it's obvious there is this "String of Pearls" that is called the Golden Lane and Northern Corentyne extends into that Golden Lane. It’s just common sense that there is going to be oil in that region. And even though that block looks small compared to the Stabroek and the Block 58 in Suriname, it's still the equivalent of ~150 Gulf of Mexico blocks. This is a substantial acreage position with many prospects yet to be drilled.

Fluidsdoc- what about the prospectivity, or size of the potential resource we are considering here?

Christine -So basically when it comes to the resource size, the only thing that we have to rely on right now is the McDaniels Resource Report that was published in early 2021. 32 exploration prospects were identified, and eight of those prospects were larger than 2,500 acres each. Some of them are significantly bigger, more than 10,000 acres each. Kawa was estimated on some of their earlier slides to be one of those prospects bigger than 10,000 acres. Those are huge prospects if the thickness is there, that is going to hold hundreds of millions, if not even a billion barrel discovery. That's why I've been so bullish. I don't even have to talk about the entire Corentyne block. I mean, I can completely ignore the tail and just focus on the Northern Corentyne prospect area where they've had two successes. Both are within tie-back distance of existing discoveries. You know Stand Alone development breakeven cost might be $30 or $40 per barrel to put an FPSO in the field, whereas a tie back to an existing FPSO nearby might break-even at only $15 or $20/bbl. I see these fields as being advantaged exploitation plays for Exxon and Total given their fields nearby.

Fluidsdoc- It seems like a no-brainer and with your background, you could easily be working at Exxon, Hess or Shell on an asset evaluation team. Give us a "fly-on-wall" insight into what must be going on in the companies I named.

Christine - I worked for Chevron in Exploration Strategy and Planning as an economic advisor. I was trained in all their competencies, where I would look at exploration plays and I would run full scope Economics on prospects. And with Hess I was a senior exploration advisor doing strategy, planning and portfolio management work. My main focus there was the Gulf of Mexico, but I would also look outside of the Gulf of Mexico and analyze competitors to figure out who would be a good strategic partner for blocks we might want to buy into.

Fluidsdoc- so there must be people with exactly that sort of background in a half dozen companies we've been talking about right now. What are they thinking?

Christine- I've been buying into CGX Energy and Frontera Energy since before Kawa and every time they've released results, I've usually bought more. I even went down to the Frontera Energy Investor meeting last year and after I left, I bought more. They haven't produced any results yet that have changed my conviction on this acreage, everything they've released has been positive. So people in the companies you mentioned have got to be working up resource and development scenarios for their companies regarding these opportunities. They are surrounded by discoveries and are within tieback distance to several of them .

Fluidsdoc - yeah, that's my thinking as well. This is low hanging fruit for someone. Let's talk about the Santonian as that was their original objective in the Corentyne. They didn't get enough data on Kawa, but finally made it down on Wei. Then they couldn't get their backup MDT tool to function properly. And, you know, I guess that's kind of a frontier area where service companies don't have enough tools or whatever?

Christine - This also comes down to the market conditions, so a little bit more of my background before I was a Chevron drilling engineer. I was a Schlumberger logging engineer in the Gulf of Mexico. I started out running tools and it was a similar period to where we are now, when there had been under investment in the industry. Things are starting to ramp up now following under investment occurring within the OFS companies as well. What I'm saying is, Schlumberger is more than likely short on tools. They had sent at least two MDT tools for that job to the rig and then one of them got stuck to the point that they had to Sidetrack and then when the second one failed Schlumberger likely said, okay, we can get you another one but it's going to be two weeks. I mean, they were likely in a situation where they were waiting for another tool to come off a rig before they could send it over to CGX and Frontera’s rig. You know about open hole conditions; you’ve been a fluid’s engineer. You know what a well looks like after two weeks of open hole with no circulating. All they would have done was go down there and get stuck again.

Fluidsdoc - it would be a mess down there for sure. Unless they goosed up the yield point, all the barite would have settled out, and the ECD on mud that thick might frac the reservoir when they began to drill out. They made the right call to stop the pain in my book. What are your thoughts about the Santonian reservoir?

Christine - We don't have any detailed data released from Wei yet so I’m leveraging information from Kawa-1. They presented a technical presentation with detailed reservoir properties last summer, and there's the potential in Wei for the results to be comparable or look much better. We will have to compare when they release the results following log and core evaluation.

{kind=link}

{kind=link}

Kawa was drilled on the flank of their Santonian prospect. The sand formations would have been getting thin and ratty there. If they were to drill an appraisal well in the heart of the Santonian prospects, the formation properties might look better. Which I think will happen at some point in time, after a major farm-in, in the hopes of finding cleaner sands, better permeability and much better porosity.

This area has always reminded me of the first field that I ever worked in, South Pass-78, in the Gulf of Mexico. If you're familiar with the Gulf of Mexico, you know, that was for a long time the sweet spot of the Gulf of Mexico shelf. It is right at the mouth of the Mississippi River, where all those sands were flowing out and depositing. That field was a freaking Cash Cow for Chevron.

When I first started looking at the Corentyne block at the mouth of the Berbice River, I thought, could this be like South Pass-78? Now I'm not a geologist, but if you look at the depositional environment and everything else, it seems like a similar situation, and I believe the oil is there.

I also believe that because the wells are drilled on the slope, they're much more technically challenging. I mention that because people have been ragged on CGX and Frontera for their well cost and how long it's taking them etc. What they're not looking at is the fact that even though the water is shallower, the formations are not so they're having to drill much more dirt. They don't have the benefit of added water depth that Exxon has and so that's made those wells a little bit more challenging.

These exploration wells are just vertical wells because they're trying to get as much data as possible but in a development situation they would be drilling these directionally, and perforating those formations perpendicular and not at some angle that's probably making it hard to even stay straight.

Fluidsdoc - Great explanation. So are we expecting light oil from the Santonian, as with the Maastrichtian and the Campanian? Is that likely? You know, they sent the cores off and they've got the logs, you know, the only thing they don't have is an oil sample.

Christine - So the original hole that was drilled when that MDT got stuck, it was at the top of this Santonian when that happened. They saw something there as you don't normally stop in the middle of drilling a hole section and run an MDT because it is the tool that's most likely to get stuck. And sure enough, they stuck the damn thing but they got the digital data that should have told them it's light oil, but they just don't have the physical sample to prove it, until they do the core and the cuttings analysis from the sidetrack.

Fluidsdoc - they have had some bad luck, but I thought their Drilling Supt, Kevin Lacy added a lot of experience to the team. You know, that was something that impressed me about CGX the guy they got to run the operation. There is an ex-Chevron pro with lots of lots of experience.

Christine - In deepwater, your company man better have more than 20 years of experience. Let's just be real, you do not want somebody out there on an exploration well, who isn't at the absolute top of their game. I've known Kevin for a long time as he’s on the Petroleum Engineering advisory board for The University of Tulsa. We went to the same University. I ran into him while I was working for Precision Drilling, at an alumni event. He got me an interview with Chevron and the next thing you know, I'm going to work in their technology department in the rock mechanics team as a drilling SME.

Fluidsdoc - Best way to get a job. Why do you think they were having so much trouble drilling the Santonian?

Christine - I think it was probably wellbore ballooning . They have a lot of open hole there and in these types of drilling environments, there was probably a lot of give and take from the reservoir. It's like the same drilling conditions as in a lot of the Gulf of Mexico wells. With wellbore ballooning, it's drinking mud and then it's giving it back, minutes or hours later, and you never know the timing so you're constantly stopping and closely monitoring your mud. Proceeding with caution and waiting to ensure your well is not getting out of control. I think that's it. I think that they were cautiously drilling because they had a lot of open hole and the entire time potentially fighting ballooning. So again, that's just my guess. Until they disclose something publicly, we don't know 100% for sure. But for me, that's what makes sense.

Fluidsdoc -It seems like something could have been able to anticipate and have a plan for, you know, Well Bore strengthening-Stress Cage, or something to seal that off. Moving on, have you put a pencil to the volumes we might be thinking about here?

Christine - If we assume that that 76 feet announced in the Kawa Santonian extends for the 10,000 acres that they've shown and if I apply the rock properties that they gave in their technical presentation, I think deterministically, we could be looking at over 200 million barrels. Which is equivalent to what's been occurring in Stabroek but those are mostly Campanian discoveries. I also think that it's going to be more than that because I think they'll appraise it and they'll find that it's thicker as you get toward the heart of the reservoir. But for the intents and purposes of this interview, I can defend 200 million barrels. And that's recoverable, and those are oil barrels. I'm not even including added equivalent barrels from the solution gas.

For Wei’s 77 feet of net pay in the Campanian, applying the Kawa Campanian rock properties from the May 9th 2022 technical webinar and also using the 10,000 acres, I calculated deterministically over 275 million barrels of recoverable oil.

Finally, I looked at the Santonian with 210 feet of pay, that was announced. I'm assuming that's net pay and also using the rock assumptions from the technical webinar and 10,000 acres. I got close to 600 million barrels of recoverable oil.

So when we add those three sections, we're looking at over a billion barrels of recoverable oil and that 1 billion barrels is, I think, a good number where you can start to apply dollars per barrel for deal valuation. Anywhere between $2 and $6 per barrel, because we can benchmark deals over the years where we see that's been done. For example, Total for Block 58 farmed into Apache's Maka Prospect prior to the end of the well and they paid about two dollars a barrel. So that should be the floor in my opinion for Corentyne.

Fluidsdoc - can we put that in NPV?

Christine - Sure. I did build some cash flow models. You can easily defend putting an FPSO on Corentyne for developing these three reservoirs as a hub development. There is also a high confidence prospect that is centrally located between Kawa and Wei, which might bring in another 200+ million barrels. So if we were to review the economic assumptions and the field development plan for Liza, then apply that to the contract terms for Corentyne, based on eighty dollars per barrel and assume that we are, five years out from first oil you could say that this is worth well over four billion dollars to the contractor Net Present Value with the borrowing rate of 10%.

So all these different ways that I look to value that block keeps telling me that it's worth anywhere between two billion dollars and six billion dollars for the contractor group today. The market just doesn't believe it yet.

Fluidsdoc - So then the question becomes, who might be sitting in the deal room with a calculator humming?

Christine - You have Exxon on to the Northwest, Total to the West and Northeast and then, Chevron and Shell to the Southeast…somebody's going to nibble.

Fluidsdoc - I think you have the Chinese in there as well...

Christine -Yeah the Chinese and it's also recently been announced that Petrobras is going to be bidding on blocks in the current licensing round. And why bid in the licensing round and not farm-in to Corentyne? The bid round acreage is higher risk acreage when someone can farm into the Golden Lane and then also get access to a deep-water port that's on the Berbice river through CGX Energy and Frontera Energy. The Berbice river runs all the way up to landlocked Brazil. If I was at Petrobras, I would be like let's just go buy CGX Energy and Frontera Energy. Let’s just take them out. These small companies are no big deal for them. Not to mention it's strategic for Brazil because they could again, with the port location and with these fields located there, run a natural gas pipeline to the port and then run power lines into Brazil. Where they desperately need power because that land-locked region is remote. And then also start also exporting trees and crops and all kinds of stuff out of Brazil through an economically advantaged zone because Guyana has their doors wide open for trade. They are ready to do business.

Fluidsdoc - let's talk ways to play this. Both Frontera and CGX carry some risk. Frontera with a potential sale and CGX with lack of cash to take care of every day expenses. What are your thoughts?

Christine - Fronteras is definitely the safer bet. But there's pros and cons to each side. Mainly Frontera Energy has cash flow and CGX does not yet. In my opinion, the reason that CGX is trading where it is today is that everyone knows that there was a well cost overrun and CGX has no revenue to pay for it. So, until they let the investment community know how they're paying for that overage, they're going to trade sideways at best.

Your takeaway

Christine and I agree. It is near-certain a big IOC player or State Owned Enterprise-SOE, will step forward in the near future. There is provably light oil present in commercial quantities in each of the three sand packages they have tested. The fact they didn't get the MDT down in the Santonian limits the testing somewhat, but they got cores-which presumably they preserved and can confirm oil quality from the rock. The wells are within tie-back distance to at least a couple of the Exxon Mobil, ( XOM ) hubs going in Stabroek. They could also be serviced from an FPSO, which Christine thinks is economic now, and would be supported by further drilling in the block. As she said, "somebody is going to bite." My guess this could happen before much longer, and certainly in the next couple of months. They've got bills to pay.

Frontera Energy is the safest play but faces an uncertain future in the market. CGX is the way I've played it thus far with a small position, and I would buy more if the price declined from the current $1.00. The price of CGX is purely speculative as they have no revenue and their key asset is the Corentyne PPL. The rumor mill has been pretty quiet recently as the industry awaits a press release detailing the core and log analysis. I don't really expect much news for a couple of months. This work takes a little time to accomplish, so I think we will hear something around the end of the quarter. For reference the Press Release on the KAWA#1 was issued about 4-months after the discovery was announced. That would put us in late September, or early October.

For further details see:

CGX Energy: A Fly On The Wall In The Data Room