CA - Chartwell Retirement Residences: Recovery In Its Operation Is A Positive Sign

2023-12-23 01:10:30 ET

Summary

- Chartwell Retirement Residences has seen significant improvement in its operations in 2023 after struggling during the pandemic.

- The company's occupancy rate has been steadily increasing and is expected to continue to improve.

- A significant portion of Chartwell's debts will mature before the end of 2024, which may put pressure on its share price in the near-term.

Investment Thesis

We last covered Chartwell Retirement Residences ( OTC:CWSRF ) ( CSH.UN:CA ) in March 2019. At that time, we pointed out about the oversupply issue in the industry. This oversupply issue worsened during the pandemic and caused Chartwell’s operation to dwindle. The good news is that after a few years of struggle, we are finally seeing signs of recovery as Chartwell’s operation has improved considerably in 2023. However, its share price is still under pressure as a significant portion of its debts still needs to be refinanced before the end of 2024. While interest expense may be higher after refinancing, improvement in its operation should be able to cover the interest expense. In addition, any surprise moves by Bank of Canada to lower the rate will provide positive catalyst to Chartwell’s share price. Therefore, we think this is a good time to start buying shares of Chartwell and average down on any price weaknesses.

YCharts

Earnings and Growth Analysis

Q3 2023 highlights

Chartwell’s operation continued to rebound in Q3 2023. The company saw its adjusted same property net operating income increased from C$50.7 million in Q3 2022 to C$60.7 million in Q3 2023. This represented a growth rate of 19.7%. Its weighted average occupancy rated increased by 300 basis points to 81.4% in Q3 2023. Its funds from operation increased considerably from C$0.13 per unit in Q3 2022 to C$0.16 per unit in Q3 2023. This improvement was primarily due to better occupancy rate, rental growth, and a decline of agency costs. In fact, management indicated that the agency cost has declined by 30% year over year and is expected to trend lower to pre-pandemic level.

| (C$000s, except occupancy rates and FFO/unit) |

| Q3 2023 |

| Q3 2022 |

| Change (%) |

| Adjusted Same Property NOI |

| 60,701 |

| 50,729 |

| +19.7% |

| Adjusted NOI |

| 75,297 |

| 65,115 |

| +15.6% |

| Weighted average occupancy rate (same property portfolio) |

| 81.4% |

| 78.4% |

| +300bps |

| FFO per unit |

| C$0.16 |

| C$0.13 |

| +23.1% |

Source: Created by author

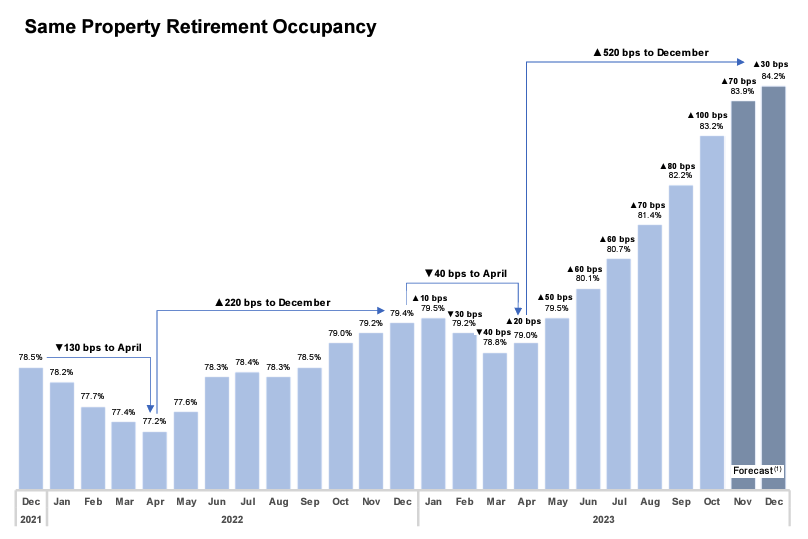

Improving occupancy rate

One of the primary drivers to Chartwell’s improving Q3 2023 was the rising occupancy rate. As can be seen from the chart below, its occupancy rate has improved from the low of 77.2% reached in April 2022 to 83.2% in October 2023. Management is expecting this occupancy rate to further improve to 84.2% towards the end of the year.

{kind=link}

Chartwell was also able to apply rental rate increase to help offset inflation. Management expects that total rental and service rate growth in 2023 to be between 3.5%~5%. As can be seen from the chart below, growth rate varies depending on the locations of its retirement residences.

Company Report

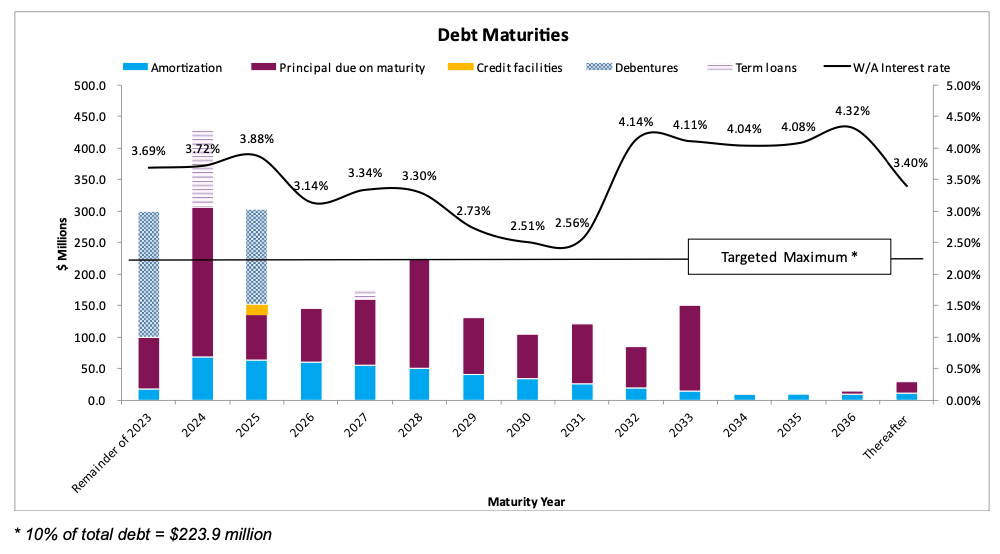

Nearly 1/3 of its debts will mature before the end of 2024

While Chartwell’s operation appears to be improving with growth in both occupancy rate and adjusted NOI, about 32.7% of its debts will mature in Q4 2023 and 2024. These debts have a weighted average interest rate of about 3.7%. Given the current elevated rate environment, refinancing these debts may result in higher interest rate. This may put some pressure on its share price in the near-term. Another 13.5% of its debts will mature in 2025. However, we are not as concerned about debts maturing in 2025 as most economists believe inflationary pressure will subside considerably beyond 2024. This means that interest rate will likely also come down considerably. Therefore, re-financing debts that will mature in 2025 should not materially increase the interest costs.

{kind=link}

Supply and demand trend remains positive

While the market may continue to be concerned about Chartwell’s debt re-financing in the near-term, we noted that its long-term outlook remains positive. Not only the company’s operation has improved considerably after the pandemic, supply and demand dynamic is also improving. On the demand side, as can be seen from the chart below, the number of Canadians aged 75 and over is expected to grow from 3.1 million in 2022 to 6.3 million in 2042. Therefore, there is tremendous demand for retirement residences.

{kind=link}

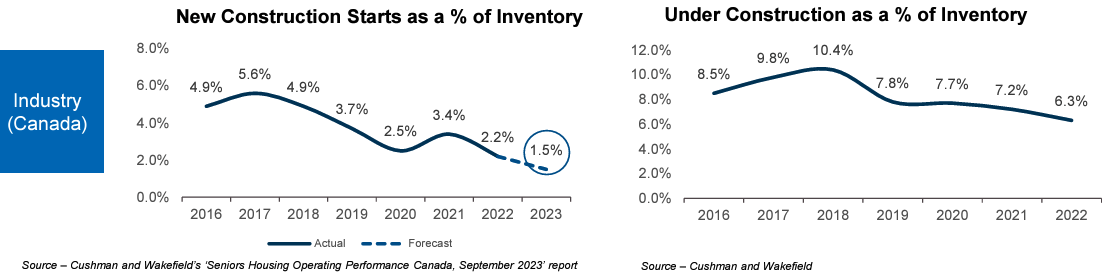

On the supply side, new construction starts as a percentage of inventory has been in a declining trend since the peak reached in 2017. As the left chart below shows, construction starts as a percentage of inventory has declined from the peak of 5.6% in 2017 to only 2.2% in 2022 and is expected to fall further to 1.5% in 2023. In addition, under construction as a percentage of inventory has also declined from 10.4% in 2018 to only 6.3% in 2022. Therefore, supply and demand dynamic remains quite favorable for Chartwell in the next few years.

{kind=link}

Valuation and Dividend Analysis

Chartwell currently pays a monthly dividend of C$0.051 per unit. This is equivalent to a dividend yield of about 5.3%. Prior to the pandemic, Chartwell has increased its dividend for five consecutive years. However, the pandemic disrupted its operation and the company has not been able to raise its dividend since 2020. We do not think Chartwell will raise its dividend in the near-term as its payout ratio is still quite high.

Company Report

Chartwell has generated FFO of C$0.39 per unit in the first 9 months of 2023. We expect Chartwell to generate C$0.17 per unit in the last quarter of 2023. Therefore, Chartwell will generate C$0.56 per unit in 2023. The company currently trades at a price to FFO ratio of 20.5x. While this is high, we expect FFO per unit to rise to C$0.70 per share thanks to a combination of improving occupancy rate, higher rental rate, and lower agency cost. This means that Chartwell is only trading at a price to 2024 FFO of 16.4x. In the past, Chartwell has typically trade in the range of 16x ~ 20x. Therefore, its price to 2024 FFO ratio is towards the low end of its valuation range.

Investor Takeaway

As discussed in our article, we are seeing signs of recovery in Chartwell’s operation. The only near-term headwind to its share price is debt refinancing. However, this headwind will likely not last long, as Canada’s central bank may soon lower the rate in 2024 and beyond thanks to subsiding inflationary pressure. Therefore, investors may wish to start accumulating shares now and buy more on any share price weaknesses.

Additional Disclosure : This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

For further details see:

Chartwell Retirement Residences: Recovery In Its Operation Is A Positive Sign