CC - Chemours - There Is Upside After A Drop In Share Price

2023-04-28 22:14:30 ET

Summary

- Chemours is a company I've been covering for years. Challenges remain, but my long-term view for the business is a positive one. I maintain a position in CC.

- In this article, we'll do an update and see if the PT warrants a slight adjustment based on recent results and current global trends.

- I remain positive on Chemours. Near-term risks exist, and the current market is volatile, to say the least, but the company is competitive.

Dear readers/subscribers,

The time has come for an update on Chemours ( CC ). This is a holding of mine that for some time hasn't gone anywhere exciting, unfortunately. Since my last article, it's up - but it's not as up as much as the broader index. On the basis of this, it hasn't performed well. Because a good result is only worth considering if we actually beat index.

That Chemours has risks is nothing new - we've been through that before, and we've clarified Chemours does have risks. A chemical company with an exposure, or being a play on Titanium dioxide is bound to be a rocky or volatile play. The share price gives us an insight into how volatile it can be, given how up and down it's been going for the past 3-4 years. It's not at 5-year lows at this time, but it's nonetheless at a decent valuation.

Here is why I believe that to be the case.

Updating on Chemours - There's plenty of long-term upside here.

For the 4Q22/full-year period, the company delivered EBITDA growth. Despite challenging macro, the company delivered growth in both EBITDA as well as in EPS, which in turn led to record full-year net sales and EBITDA in both the TSS and APM segments, and was integral in over $440M of FCF.

To say that Chemours did poorly is completely wrong. CC has also gone ahead and increased shareholder returns, combining share buybacks with dividends.

2022 was a growth in both sales and income. Net sales were up almost half a billion, EPS was up 5 cents, and EBITDA was up $50M on an adjusted basis, and this is despite problematic macro, reflecting strong pricing trends.

1Q23 came out the day I wrote this article, and the results here don't change the overall thesis for the company.

Longer term, Chemours is not the most profitable company in the chemicals segment, nor is it the least indebted or soundest in terms of financials. But It's one of the most fairly-valued businesses here, by which I mean undervaluation. Also, Chemours has been buying back shares for an extensive period of time. During the past 3 years, its average share buyback ratio has been 3.2x, which is in the 97th percentile in the sector. It implies very strongly, that the company believes its own shares to be significantly undervalued.

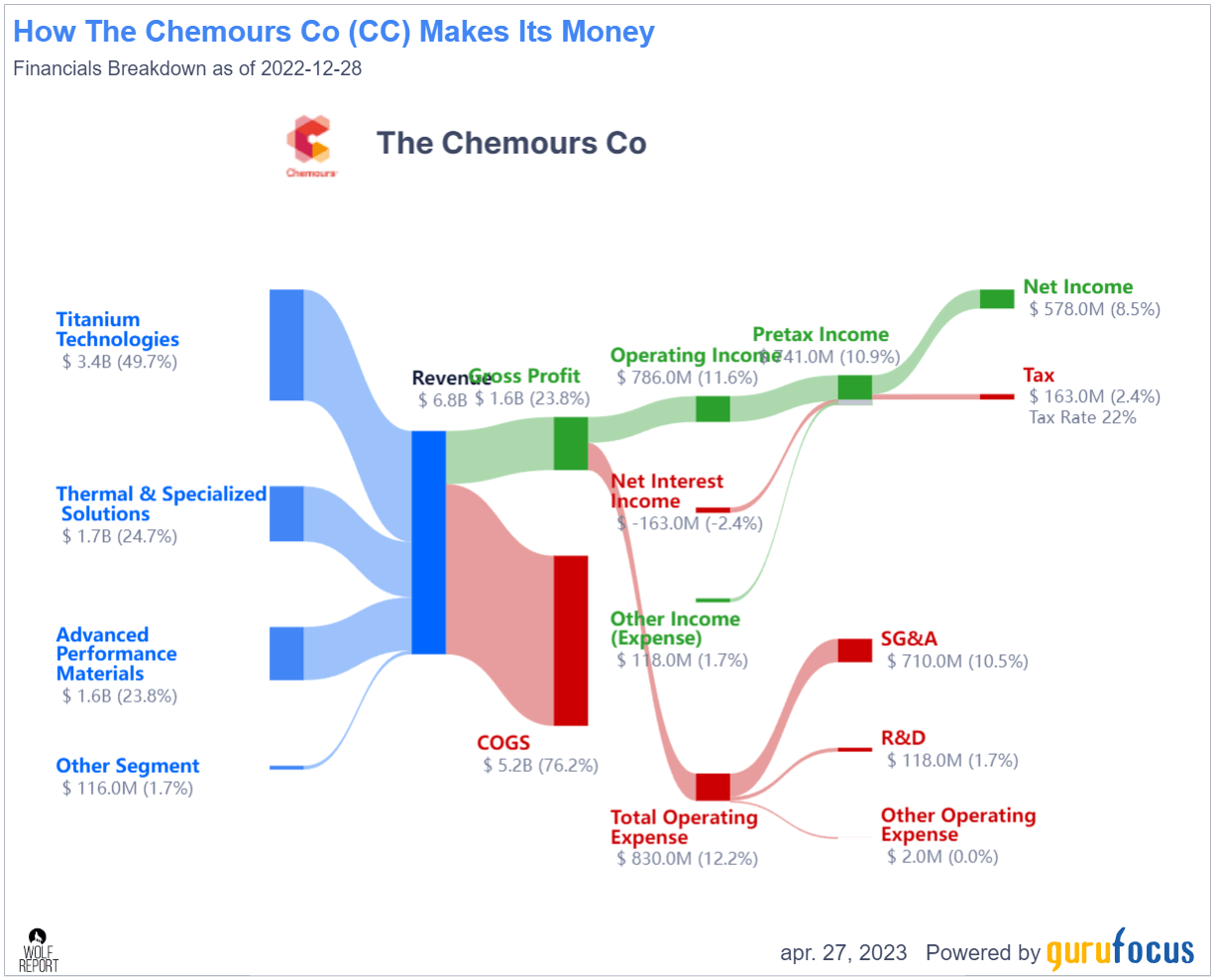

Also, the company retains basic profitability. Its ROIC is above the level of costs for capital, and the company has been growing shareholder equity year-over-year for the past two years. The company's mix remains focused on Titanium Dioxide - nearly 50% of the mix is still Titanium technologies, but other segments are growing.

Chemours Sales/net (GuruFocus)

{kind=link}

The company is also still junk-rated. It did record a slight improvement to BB, but that's it for the moment. Some of the trends we saw in 4Q, we see in 1Q as well. I'm talking about the company's push to increase prices. Negative trends also continue. Energy costs are still high, and logistics/inflation/wage costs are still influencing the company as well. There was also a weather event late last year, and weather events seem likely to continue at this point as well going into the next year.

1Q, other than what's said above, saw strong net sales and good EBITDA despite some volume problems. TSS saw record results, with APM growth drivers remaining solid and intact. The company fully confirmed its 2023E guidance for both EBITDA on an adjusted basis and FCF.

With strong net sales, what's meant is a decline of only 13% from record numbers, and GAAP EPS is down about $0.47. This is not, and shouldn't be surprising given the comps. Also, margins declined to around 20% on an adjusted EBITDA margin basis, due to volume declines and input costs.

The company still has a total liquidity of well over $1.5B.

The company's more cyclical Titanium businesses saw expected volatility in both top and bottom line results. I expect a gradual recovery of these segments, but it's largely macro-based.

The same is not true for thermal solutions, due to increased adoption of the company's Opteon products, which are driving not only sales but good through-cyclic earnings.

Chemours IR (Chemours IR)

Overall, I do not see any fundamental worries that the company will be unable to reach its 2023E goals. The reaffirming of the yearly guidance mostly confirms this. Volatility in legacy Titanium segments is held up by growing Opteon adoption and regulatory dynamics, and even in Titanium, the company expects destocking to lead to a gradual recovery in terms of demand. While raw material inflation continues to be of concern here, it's something that's expected to ease going forward.

The company's leverage still isn't bad or anything to really worry about. The company's CapEx is well in hand, and Chemours continues to generate impressive amounts of operating and free cash flow.

This leads us to the current valuation thesis for Chemours.

Chemours - valuation is appealing, an upside is possible, double-digits seem likely

The company's earnings trends continue to fluctuate pretty wildly. We saw lows of below $2/share for EPS back in 2020, only to see it go to almost $5/share in 2022. For 2023 and forward, we're expecting a slow 2023 characterized by increasing prices and similar trends, but which will then turn to impressive growth as some of the company's growth projects and other ambitions are realized.

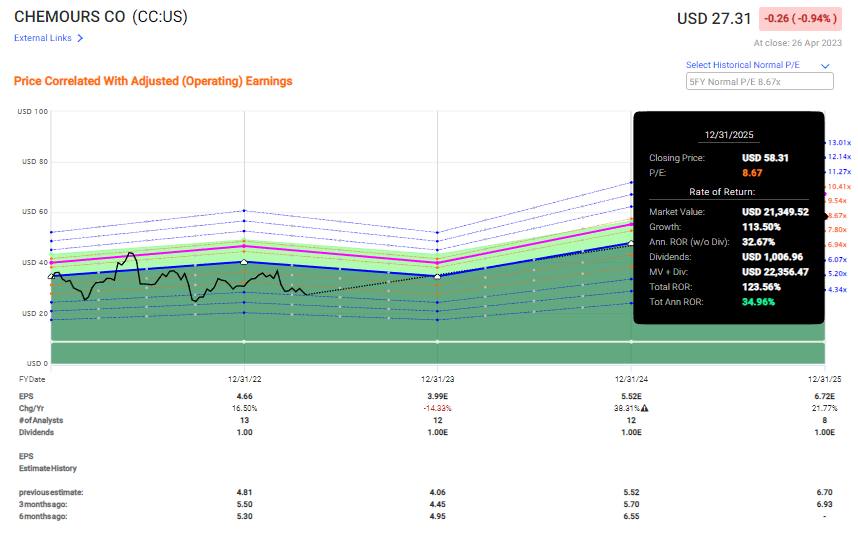

Chemours are typically cheaply traded. Its 5-year P/E is below 9. But even accounting for that, a 2025E upside based on the current set of S&P Global and FactSet forecasts comes to a double-digit annual upside, and a triple-digit 3-year RoR above 123%.

F.A.S.T graphs CC upside (F.A.S.T graphs)

{kind=link}

Even forecasting the company at lower multiples, it would take a decline to 4x for you to underperform the market - and at today's forecasts, even at 4x, you'd still get away with almost 15% RoR in 3 years. That is the definition of a bearish case or scenario here for a company like this.

Chemours really hasn't "popped" yet, reflecting its longer-term high upside. I want to point out at this time that the company is not easy to forecast accurately, so the uncertainty here is somewhat understood. However, the company has a proven track record of 50%+ not only managing estimates but beating them. In fact, the company has beaten estimates 5 years out of 7 over the past 7 years, and that is as long as the company has been around in its current iteration.

Chemours is also a very popular stock with institutional investors and billionaires. Lately, several investors like Ray Dalio, Jim Simmons, and Joel Greenblatt have been adding shares in the company. While this in itself should never be enough to cause you to buy any single company, it's nonetheless interesting to note, because they obviously would not be buying companies they thought were excessively expensive.

Chemours is cheap. This is not just me, by the way, but also analysts such as from S&P Global that follow the company. 11 analysts currently rate Chemours, and out of those, we have an average PT of around $38/share from a range starting at $27 and going up to around $52. This average PT implies an overall upside of almost 40%, and 5 analysts out of 11 are positive on the stock. Somewhat this implies that they believe there is still more downside potential in the stock at this time.

I won't argue that CC could go lower - it very well could. But I don't believe that this influences the long-term upside potential for the stock I see on a 2-3 year basis, which is in the triple digits.

Chemours has not become less qualitative in the time - the market has changed. I invest beyond these market cycles and for the long term. For that reason, I remain with my Chemours targets at this time, and this is my current thesis for Chemours.

My last PT for the company was at around $35/share. This is below the average PT from analysts, but I consider it to be conservative without failing to imply what the realistic upside here could be. The yield could be higher - good chemical companies are on sale at this time, meaning you could make better returns from others here. But Chemours is an interesting play, and a good part of a basic materials portfolio, which is why I own shares.

The main risk to CC remains a downturn in the TiO2 market. This has already happened in 2019, and it may happen again.

Aside from that, I don't see much that could go "wrong" with CC. Much of the risk and downside is baked in here, and I consider the company to be "good" - and a good overall investment.

Thesis

- The company is fundamentally appealing due to its chemical portfolio but is hounded by potential legal issues and risks - both future and historical, as well as an unappealing liability profile. This needs to be discounted for, but it's entirely possible to do so - just keep your targets below 10x P/E and a share price of $36/share.

- Improved outlooks have proven my initial bearishness to be exaggerated. I change accordingly and give the company allowance for future outperformance.

- I keep CC as a "BUY" and "Bullish" rating, with an overall price target of $35, below the current analyst average, but considered fair on a peer and risk/reward comparison. As of April 2023, i am not shifting my target here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

As things stand now, the company is still a "BUY", and it fulfills every criteria that I have except one - the quality, due to its non-IG-rating.

For further details see:

Chemours - There Is Upside After A Drop In Share Price