ACMR - China Semi-Caps: A Preamble

2023-03-31 10:48:58 ET

Summary

- Chinese semi-caps are still in their infancy and at a competitive disadvantage versus their global peers.

- The Chinese government has attempted to bridge this through two consecutive Five-Year Plans.

- Despite governmental intervention, Chinese OEMs still lag behind, hindering China's chip sufficiency ambitions.

I had recently penned an article outlining the impact of the current macro and geopolitical environment, as well as the semi cycle, on the semiconductor capital equipment (semi-cap) sector. I have since received several requests to share my thoughts on the impact those factors might have on Chinese semi-cap OEMs.

Given the wide range of factors at play, I will be sharing my thoughts in two articles. This first chapter looks at Chinese semi-caps from a historical perspective and attempts to shed light on how they've come about and how they have developed over the past 15 years. My next piece will assess the opportunities that lay ahead for them in the current geopolitical environment.

The Birth of Chinese Semi-Caps

It is important to start by putting the Chinese semi-cap sector in context. Unlike their Western and North Asian peers, Chinese semi-caps are in their infancy.

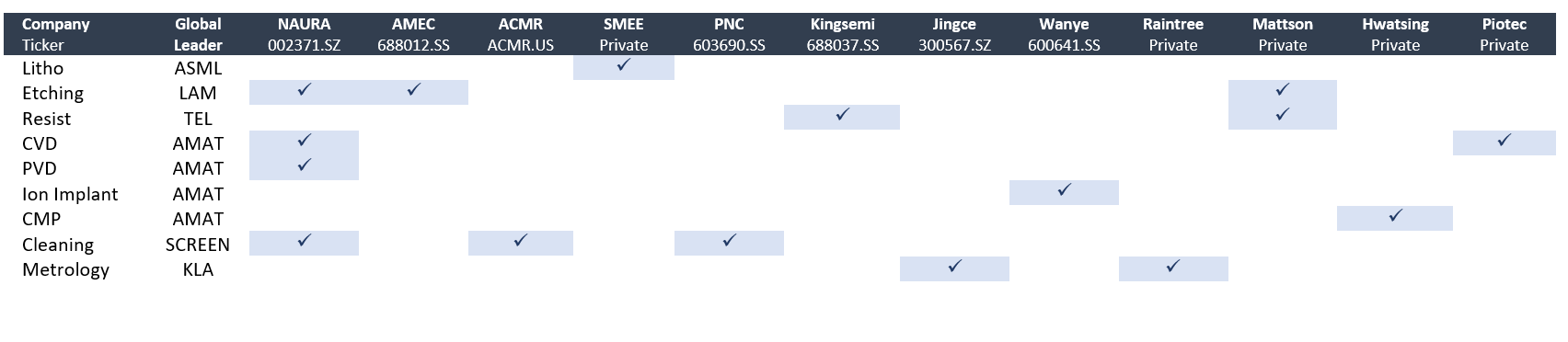

In 2006, the Chinese government launched the "02 Project," also known as the VLSI Fabrication Technology Research Program, to enhance the growth of local semi technology. The program offered grants to semi-cap applicants that conducted research on specific areas related to semiconductor manufacturing, such as dielectric etching ((AMEC)), cleaning tools (ACM Research), and chemical vapor deposition (Piotech). As each research project covered a distinct area of the semiconductor manufacturing process, there was limited overlap between local semi-cap OEMs, which instead of competing, collectively covered most equipment categories in wafer fabrication. This dynamic is illustrated in the table below.

Tool Capabilities by Chinese OEM (Annual Reports, Own Research)

{kind=link}

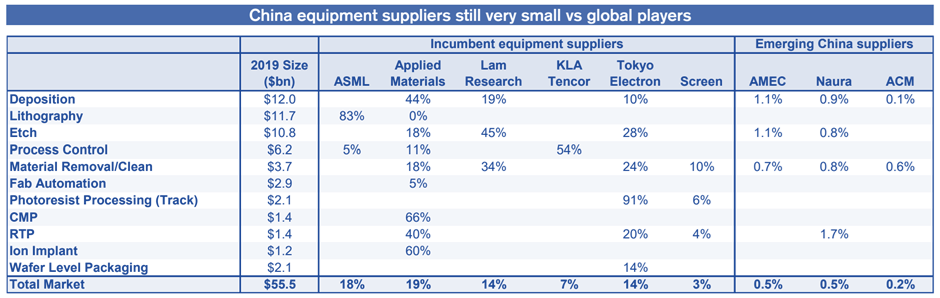

Chinese semi-caps have since made significant progress in equipment categories with lower technological barriers to entry such as furnaces and cleaning tools. NAURA's furnace equipment has secured the majority of YMTC's public equipment tenders, SK Hynix has embraced ACM Research's cleaning tools, and TSMC's 5nm fab utilizes AMEC's dielectric etcher. In spite of that, China still imports most of its WFE from global majors such Applied Materials or Lam Research. And despite the efforts of Chinese semi-caps to bridge the gap with global companies, they still are comparatively very small (see table below).

{kind=link}

Their late entry to the game and relatively small scale has led to a number of competitive disadvantages that prevent Chinese OEMs from competing at a global stage:

- They are currently far behind their global peers in technology. For example, the sole Chinese lithography machine supplier, SMEE, can only scan 90nm patterns, which are about 2 decades behind ASML's latest EUV offering. SMEE has announced that they would be able to ship 28nm and 14nm DUV machines by the end of 2022, but there are no official news of their use in China.

- Their small scale implies that Chinese OEMs lack the human and financial resources to develop technologies that would bridge the gap with global leaders. In fact, Applied Materials had a higher R&D expenditure in 2021 than the 5 largest public Chinese semi-caps' revenues combined (see below).

- They have less established relationships with both Chinese and global fabs, and therefore less opportunities to solve engineering problems and to move up the value chain.

- There isn't yet a mature ecosystem of tier-1 suppliers that can partner with Chinese semi-caps in the development of new tools. ASML worked alongside a few thousand suppliers to develop its EUV tools, effectively outsourcing capex, opex and most importantly R&D. As a matter of fact, the latest lithography machines are only technically viable because of the Zeiss mirrors, the Trumpf and Cymer power sources, the Edwards vacuum systems, etc.

It follows that in the absence of an established ecosystem and starting from a relative disadvantage, to compete domestically and perhaps one day even at the global stage, Chinese semi-caps will have to rely on external support.

Enter the CCP.

Industrial Policy at Work: Chinese State Aid to the Semi Industry

China's 13th (2015 - 2020) and 14th (2021 - 2025) Five Year plans put the spotlight on semiconductors and articulated the country's aspiration to build self-sufficiency in integrated circuits (IC). As of this writing, Chinese semiconductor production is sufficient to meet 25% of its internal demand, but China's ambition is to meet at least 70% of domestic chip consumption with locally produced content. To that end, the most recent Five Year plan specifically aims for breakthroughs in:

- IC design tools

- Cutting-edge memory technologies

- Semiconductors with wide bandgaps like silicon carbide and gallium nitride

- Equipment and materials used in the semi manufacturing process.

To achieve this, the Chinese government has employed a variety of industrial policies including setting production goals, offering subsidies and tax benefits, implementing trade and investment barriers, and incentivizing foreign companies to form joint ventures. These policies aimed to leverage China's prominent position in the global consumer electronics manufacturing industry and its potential as a semiconductor production center to encourage foreign companies to localize production, share technology, and collaborate with the Chinese government and its affiliated entities. To realize its semiconductor plan, China established a government fund, the China Integrated Circuit Investment Industry Fund ((CICIIF)), to channel approximately US$150bn in state funding to support the domestic industry, state-managed overseas acquisitions, and the acquisition of foreign semiconductor equipment. In October 2019, China announced a second semiconductor fund with a projected capitalization of US$28.9bn.

It is hard to quantify the impact of these stimulus measures on Chinese tool-makers, but we can use chipmakers as a proxy. According to Brueggel , between 2014 and 2018, Chinese chipmakers were the most heavily subsidized in the world by a very wide margin.

Estimated total government support provided to semiconductor firms, 2014-2018

State Subsidies by Chipmaker (Brueggel)

That capital, was primarily deployed in two areas:

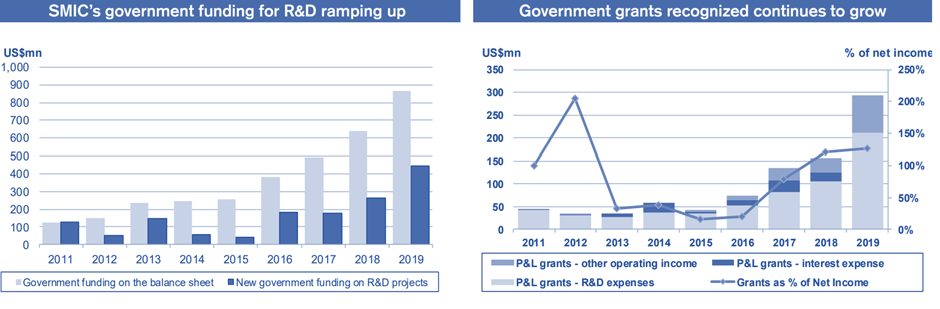

- R&D : The charts below, courtesy of Credit Suisse ((RIP)), capture the amount of money poured into SMIC, China's best known semiconductor company. According to its 2019 Annual Report, SMIC spent US$687mn in R&D, or about 22% of sales. That is a full 400 basis points above the average R&D expenditure of US chipmakers according to the SIA . Per CS, about 3/4s of that spending was financed by the Chinese government.

{kind=link}

- Capex : the chart below captures the capex expenditure of SMIC and Hua Hong as a percent of revenues. We can see somewhat of a higher base from 2015 onwards, as the 13th Five-Year Plan was rolled out, and that picks up substantially from 2019 onwards. In fact, SMIC's capex ballooned from US$1.9bn (60% of sales) in 2019 to US$5.3bn (135% of sales) in 2020, before dropping to a still high US$4.1bn (76% of revenues) in 2021. For the sake of comparison, TSMC's capex has consistently hovered in the 40 - 50% of sales region over the past years.

Credit Suisse

One can expect the same forces to be at play at major Chinese semi-caps such as NAURA, AMEC and SMEE. I.e., incentives such as tax breaks and import tariff exemptions complemented with capital injections that are eventually deployed in R&D and capex. Moreover, it is likely that those semi-caps also benefited indirectly from incentives created for chipmakers to buy locally, especially taking into account the disproportionately higher capex those chipmakers had vis-à-vis their global peers.

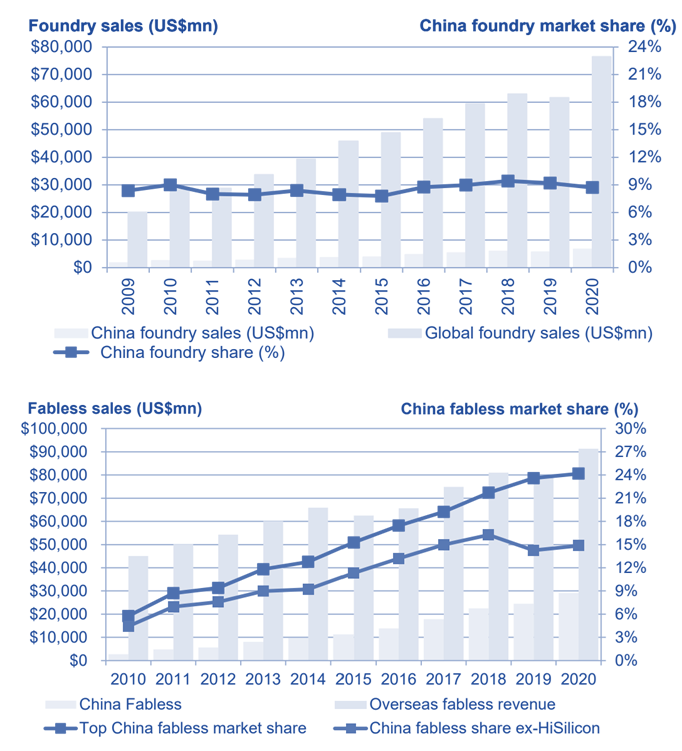

Intuitively, these policies are sound: supplant private sector capital with massive government stimuli and eventually the gap with the West, Taiwan et al will be bridged. Ex-post, however, evidence suggests that State aid was merely enough to keep the Chinese semi ecosystem at par with its global peers. The chart below illustrates how since the inception of the 13th Five-Year Plan China's share of the global foundry market has remained flat. The same was the case for fabless excluding Hi-Silicon, which is now in the U.S. entity list alongside parent Huawei.

{kind=link}

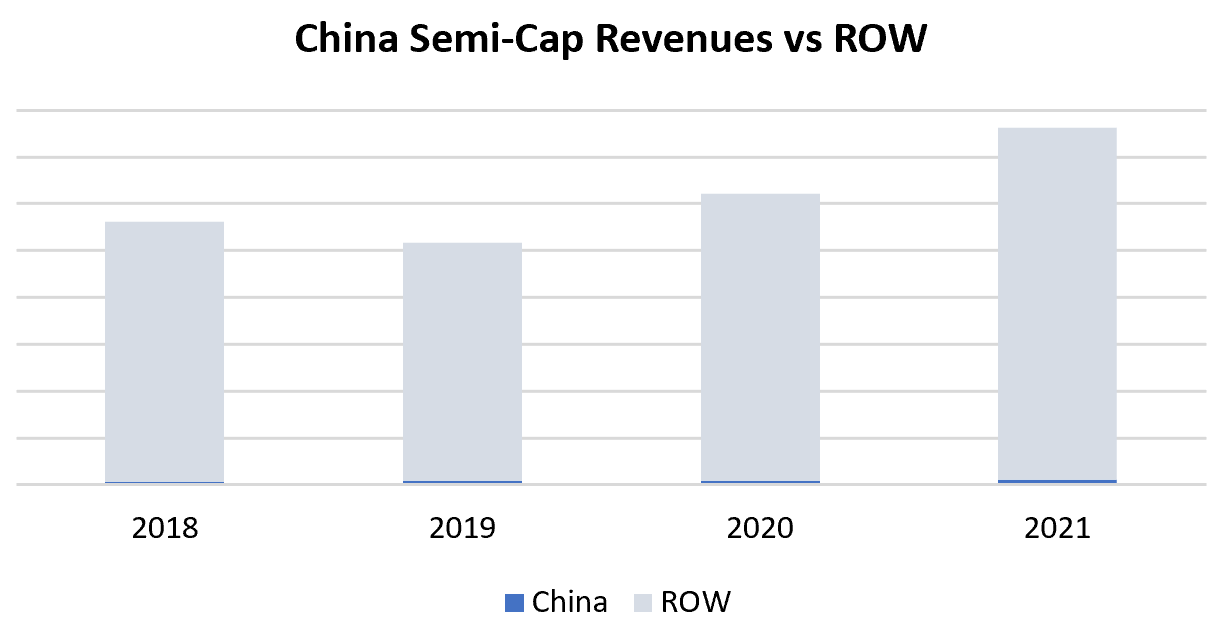

Naturally, the same occurred with semi-caps. As (barely) shown in the chart below, the share of Chinese WFE OEMs has barely budged in the 2018 to 2021 period, from an estimated 1.1% of total revenues to 1.4%.

{kind=link}

What gives?

Several factors are at play. As pointed out by Prof. Luo and Prof. Li in a recent paper published by the China Academy of Sciences the Chinese research ecosystem is still far behind the U.S. and Europe. There have also been pretty publicized issues with mismanagement and corruption at Tsinghua Unigroup. But more importantly, the limited impact of industrial policy on semi in the period leading to 2021 illustrates how idiosyncratic the semiconductor space is. Unlike the photovoltaic or automotive markets, it is nearly impossible to leapfrog leading edge semi technology or even to reverse engineer it. That would require a coordinated effort that spans across multiple extremely technically intensive verticals ranging from design, to semi-caps and materials.

It is not for nothing that several players, including Global Foundries, have decided against trying to develop leading edge nodes. Moreover, even if such a coordinated effort were to succeed, leading edge node and leading tool manufacturers would have already moved on by the time it did. In semi, it is extremely difficult to get ahead of the bell curve having started a couple of standard deviations behind the mean…

For further details see:

China Semi-Caps: A Preamble