CA - Choice Properties: 5.8% Yielding Growth Focused REIT

2023-10-18 10:00:00 ET

Summary

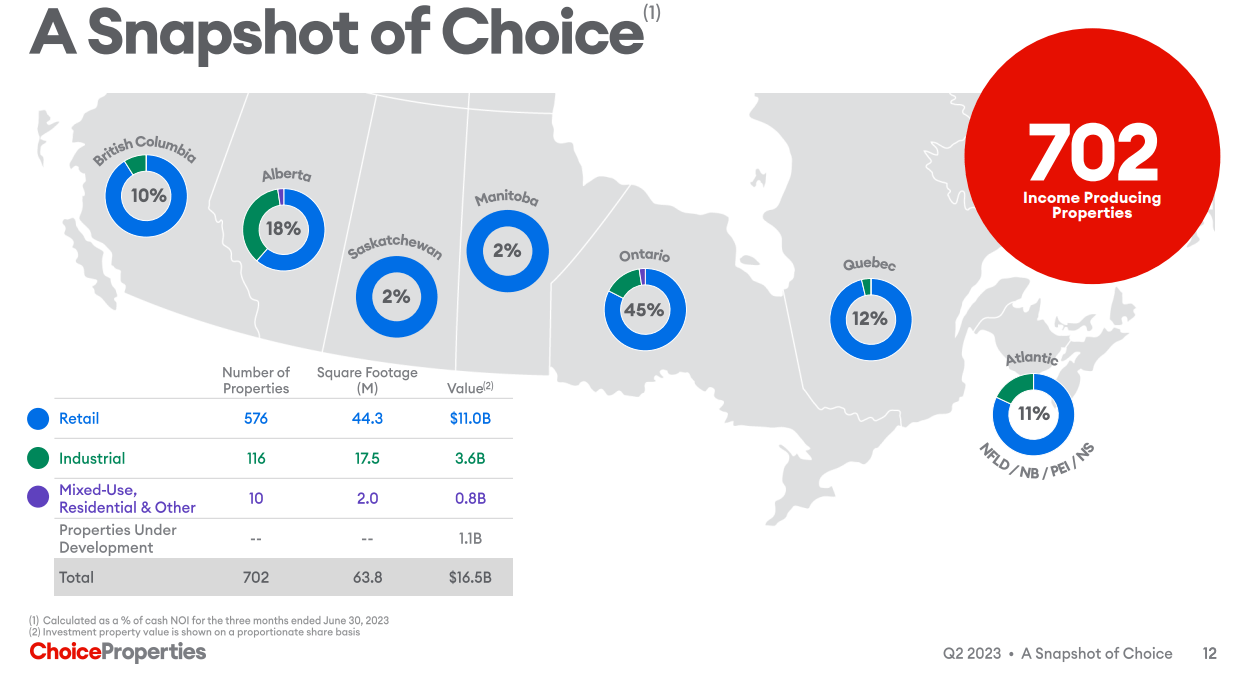

- Choice Properties REIT owns and operates 702 properties across Canada.

- The REIT's largest tenant is Loblaw Companies Limited, which contributes over 57% of its gross rental revenue.

- The REIT has been on a development tear over the last few years.

- We evaluate its prospects and provide our outlook.

All values are in CAD unless noted otherwise.

Choice Properties Real Estate Investment Trust ( PPRQF )( CHP.UN:CA ) is the owner and operator of 702 properties, spanning 63.8 million square feet of gross leasable area or GLA. The Choice portfolio is comprised primarily of retail properties, with industrial and mixed-use residential properties filling in the balance.

{kind=link}

While the properties are scattered across the country, Ontario enjoys the highest concentration, with Alberta coming in a distant second. Most of the 576 property retail portfolio is made up of grocery anchored shopping centers. That is evident in the composition of its top 5 tenants, which shows that over 57% of this REIT's gross rental revenue comes from the grocery giant, Loblaw Companies Limited ( LBLCF )(TSX: L:CA ).

Q2-2023 Fact Sheet

The 116 property industrial portfolio comprises distribution and warehouse facilities, with the count heavily skewed towards the former.

Q2-2023 Report

While many of these distribution facilities serve the needs of Loblaw, the REIT's largest tenant, they are generic enough to provide a good fit for a diverse range of businesses. The comparatively tiny, 10 property, mixed-use portfolio is located close to transit and is built on the existing retail sites, so the land is already owned by Choice. This portfolio includes a mixture of residential, retail and office buildings, giving it the "mixed-use" moniker.

The weighted average lease term of the total income producing portfolio is 5.5 years. In line with expectations from a grocery-anchor tenant, the Loblaw leases with their 5.9 year average lease term, do the heavy lifting.

{kind=link}

Of the 12% leases that were coming up for renewal at the end of Q2, close to 45% belonged to Loblaw, which based on the renewal trend for this tenant, bodes well for Choice.

{kind=link}

The overall occupancy dropped marginally from 97.8% at December 2022 to 97.4% at June 30, 2023. Most of this drop was due to Choice choosing not to renew an a lease in a multi-tenant property. Instead, subsequent to the quarter-end, the REIT leased the entire property of an existing tenant of that location.

Choice has been in a development mode over the last few years, with a focus on the industrial and mixed-use residential portion of the portfolio. The current pipeline shows another 18.2 million square feet, in various stages of progress.

{kind=link}

If one were to compare to the portfolio composition from a few years ago, say 2019, you will find that the GLA and the total number of properties (excluding those being developed at the time) is actually lower today. However, the change has come in the composition. The standalone office and residential portfolio has been slowly given way to mixed-use, transit oriented properties.

2019 Annual Report

Besides the current 18.1 million square feet of development pipeline, the REIT has its eye on an additional 70 sites, spanning 500 acres across its currently owned properties that can accommodate additional residential and mixed-use properties.

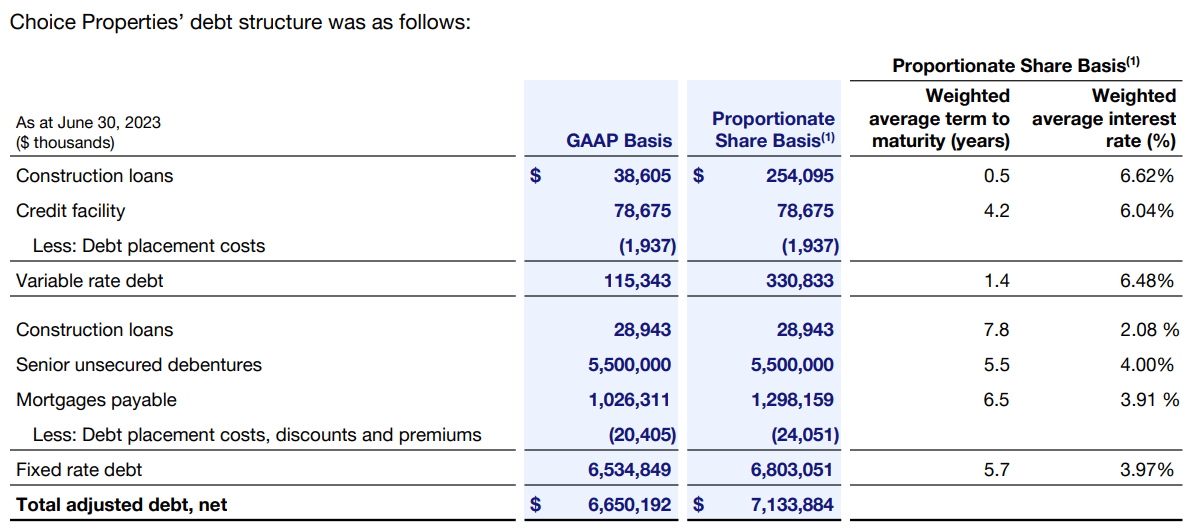

Choice is well positioned in terms of liquidity to deal with the debt that comes with development ambitions of this magnitude. At June 30, 2023, it had close to $1.47 billion in liquidity, made up of $46 million in cash and cash equivalents, along with around $1.42 billion in unused credit facility.

{kind=link}

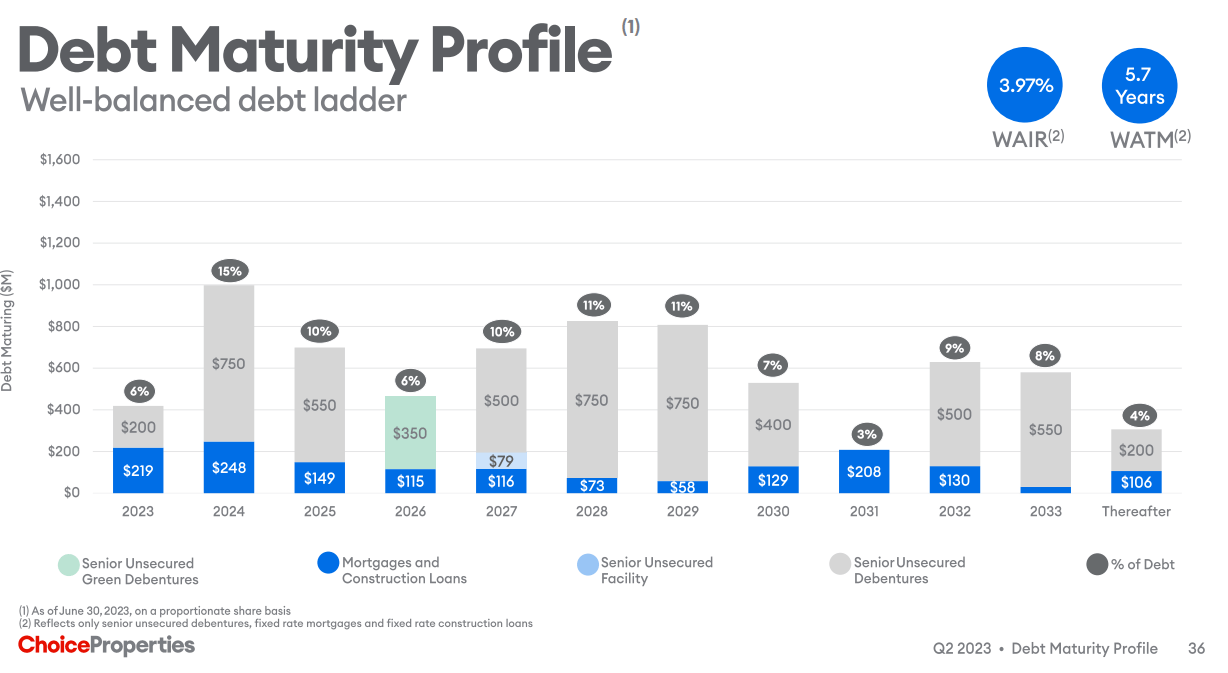

Over three fourths of its portfolio is unencumbered, adding to the liquidity cushion. All of this is more than sufficient to deal with the upcoming maturities.

{kind=link}

The weighted average term is 5.7 years, with the weighted average interest rate being 3.97%. The interest rate has increased by only 20 basis points since December 31, 2022 and 23 basis points since June 30, 2023.

{kind=link}

That is the beauty of fixing the rate on almost all of the debt, as Choice has done. Nonetheless, the fixed rate maturities in the next couple of years will keep alive the uptrend in the interest expense. Speaking of which, Choice used some of the credit facility to pay down the 4.9% yielding, $200 million in unsecured debentures subsequent to the quarter end. The interest on the unsecured credit facility is Canadian bank prime rate plus 0.20%. The prime rate at this point is 7.2%.

{kind=link}

Management mentioned that they will see how a few planned dispositions go before making a decision on replacing the credit facility borrowings with permanent financing. They intend to borrow from the unsecured market in the event they take the debt route, and they also provided some color on what they expect it to cost.

Himanshu Gupta

Alright. And Mario, do you have a sense what will be the rate if you were in the math of the unsecured debenture market? Is it like still mid 5 or is it even creeping higher than that?

Mario Barrafato

It depends on the time of day. But yes, right now, like our spreads are at 2.20 and if you are at a 3% or 5.5%, 5.6% for 10. And the thing is the yield curve is pretty flat when you go from kind of 7% as well. So 10 is a spot that would work and the pricing will be good.

Source: Q2-2023 Earnings Call Transcript

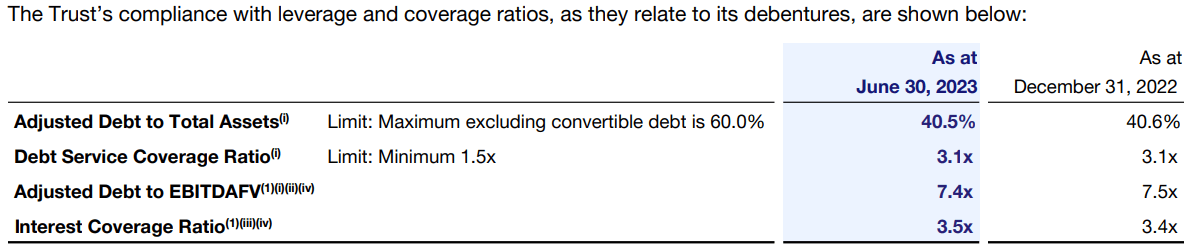

Overall, at the end of Q2, Choice had only shown improvements in its debt metrics, however minor it may be.

{kind=link}

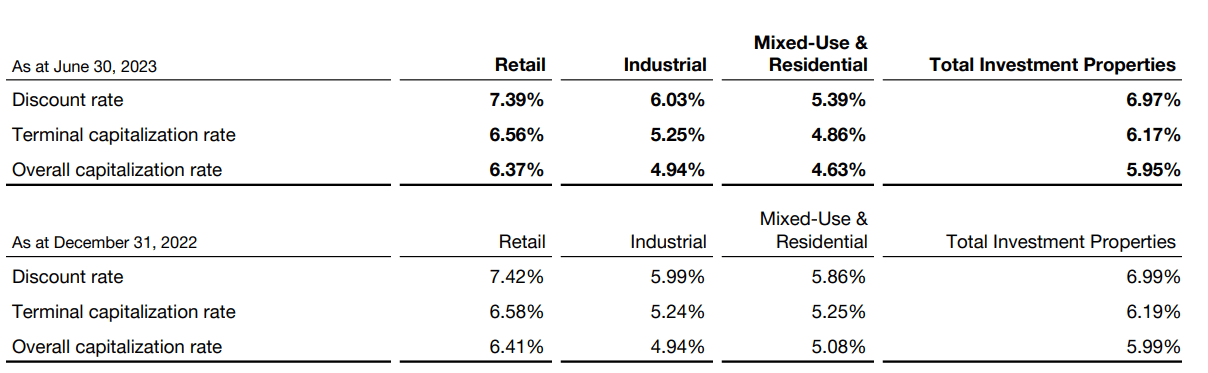

With regards to valuation, Choice showed an overall mark up (lower cap rate).

{kind=link}

This contributed, in no small part, to the 1.1% increase in the net asset value or NAV to $13.55 compared to the end of Q1-2023. This markup, as noted in the earnings call transcript , were "mostly property specific and primarily driven by industrial leasing, retail cash flow growth and transaction activity". The consensus among the 7 analyst that cover this ticker is that this number should be higher.

{kind=link}

Based on the recent mark ups, seems like the REIT is on the same page. Credit rating agencies, DBRS and S&P, also continue to provide their stamp of approval with an investment grade rating.

{kind=link}

Q2-2023 Results

Built in contractual rent escalators, higher rates on new and renewed leases in the retail and industrial segments, acquisition and development activity, and higher capital recoveries, all played a role in a 5.5% increase in year over year rental revenue.

{kind=link}

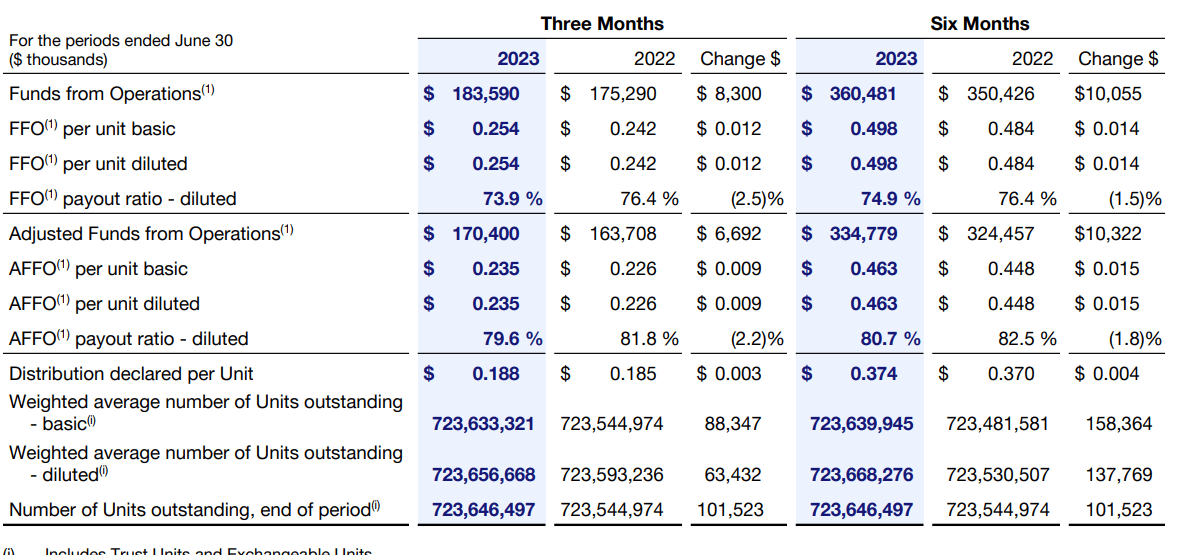

In addition, $7.4 of the $17.2 million year over year increase was from proceeds from lease termination from an inactive tenant. The building was subsequently disposed by the REIT. After accounting for the increase in interest, as well as, general and administrative expenses, the unit level funds from operations or FFO increased by 5% compared to Q2-2022.

{kind=link}

Verdict

Choice distributes 6.25 cents on a monthly basis. At the current price of $12.99, it distributes around 5.77%. This comes in at the low end of both development focused REITs on our radar, SmartCentres Real Estate Investment Trust ( CWYUF ) ( SRU.UN:CA ), that yields close to 8%, and RioCan Real Estate Investment Trust ( RIOCF ) ( REI.UN:CA ) that yields 6%. Despite the lower yield, it commands a higher multiple relative to the other two.

{kind=link}

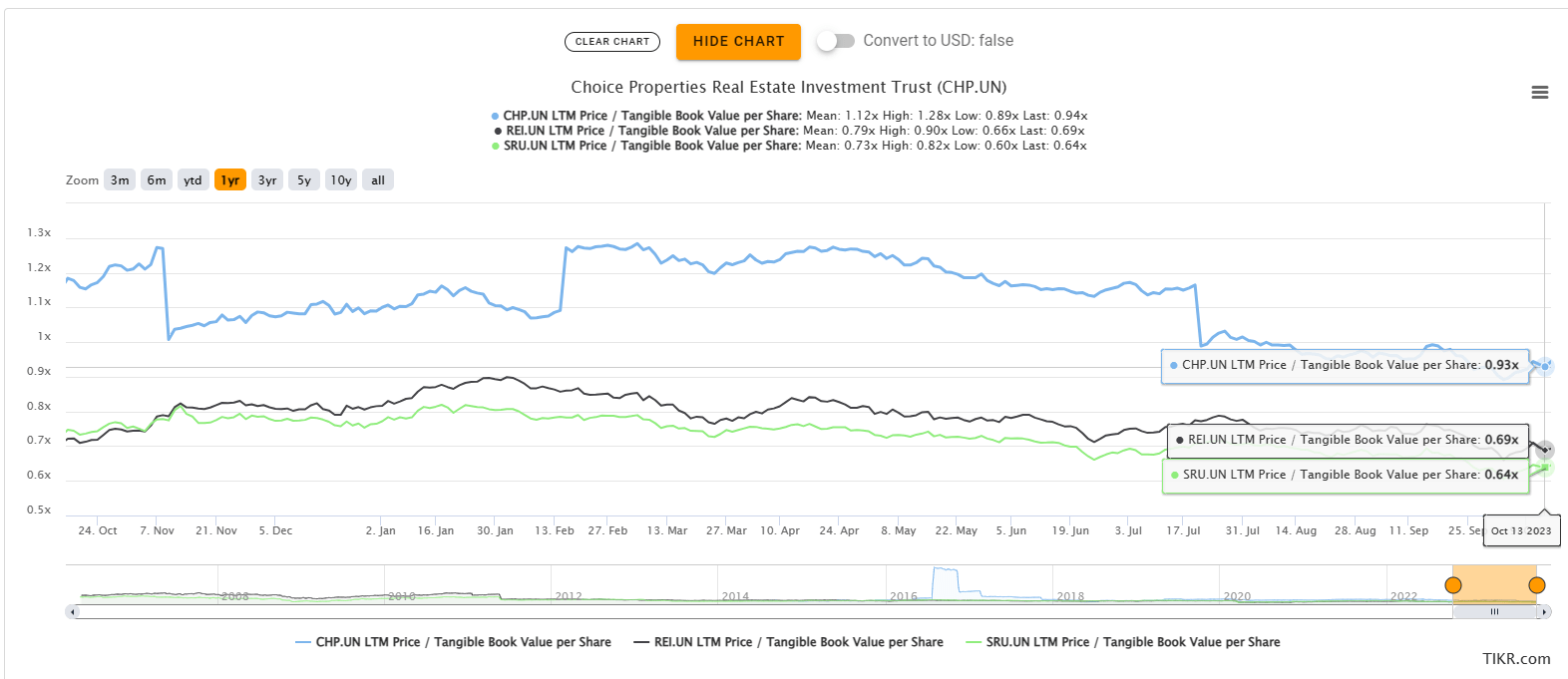

SmartCentres and RioCan can also be bought at a bigger discount to their tangible book value.

{kind=link}

Where Choice comes out ahead is in the next metric. At 7.5X Debt to EBITDA, Choice makes a far better choice than either RioCan (9.5X) and SmartCentres (10.0X). This puts it in a commanding position to weather the interest rate challenges we are seeing. Its weighted average debt maturity is also a bit better. The key debate here is whether the relative premium here discounts this. In some ways, the answer is yes. We cannot see ourselves buying Choice here because of that. That might change if it traded about 15% lower. We have some retail exposure today and we will be waiting for more multiple compression before we buy this one.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Choice Properties: 5.8% Yielding, Growth Focused REIT