UNH - Cigna: Attractively Valued In The Healthcare Sector

2023-08-12 04:58:32 ET

Summary

- Cigna is looking attractively valued when compared to peers and to its major competitor, United Health Group.

- A Discounted Cash Flow Analysis indicates that the company is undervalued by 30%+.

- While there are risks to the investment case of Cigna, especially due to potential regulatory changes in the US, the companies valuations offset these considerations.

The Cigna Group ( CI ) is pretty much trading flat over the last year:

This poses the question, if the company is currently attractively valued and might therefore be a good investment.

SWOT Analysis

To summarize the most important components of Cigna's business and to get a grasp of what us currently impacting the company, I conducted a small SWOT analysis for the company.

Strengths

- Diverse Product Offering : Medical, pharmaceutical, dental, supplementary insurance, health care, and other services and products relating to health are all provided by Cigna. By diversifying investments, risks are reduced.

- Strong Global Presence : Cigna has operations in more than 30 countries and jurisdictions, giving it a sizable market and enabling it to take advantage of international prospects.

- Innovative Solutions : The business has consistently made technology investments in order to offer cutting-edge healthcare services. To customize and enhance patient care, it makes use of data analytics and medical information.

- Mergers and Acquisitions : Cigna has successfully merged with and acquired several businesses throughout the years. Its 2018 acquisition of pharmaceutical benefit manager Express Scripts is notable since it greatly increased its market reach.

-

Financial Stability : Cigna can afford to finance expansions and other projects because of its strong financial foundation and revenue growth.

Weaknesses

- Complex Regulatory Environment : The health insurance industry is subject to strict restrictions, particularly in the US, which may have an impact on how businesses operate.

- High Debt : Despite being advantageous, acquisitions have resulted in debt buildup for Cigna.

- Dependence on U.S. Market : Despite having a presence all over the world, a sizable amount of Cigna's income comes from the U.S. ( ~95%+ ), making it susceptible to regional market dynamics and legislative changes.

Opportunities

- Expanding Global Healthcare Needs : Insuring one's health is becoming more and more popular worldwide. Opportunities for growth are presented by the aging populations in many industrialized nations and the rising levels of knowledge in emerging nations.

- Digitalization and Telemedicine : The COVID-19 pandemic has brought telemedicine services to even more prominence. To meet the increasing demand, Cigna might make greater investments in telehealth programs and online

- Integration with Wellness Programs : Integrating insurance with wellness and preventative care initiatives is becoming more popular. Cigna may take advantage of this to increase client loyalty and make more income..

- Collaborations and Partnerships : Working with tech firms or startups can assist Cigna in utilizing cutting-edge technology and enhancing its products.

Threats

- Intense Competition : There are several significant participants in the health insurance business, including UnitedHealth Group ( UNH ), Aetna, and Anthem. Price and profit margin pressure is a result of this.

- Regulatory Changes : Business operations can be severely impacted by changes to healthcare regulations, particularly those enacted in the US like the Affordable Care Act .

- Economic Fluctuations : Economic downturns may result in fewer individuals choosing private health insurance, which will have an impact on Cigna's income.

- Cybersecurity Threats : The danger of data breaches and cyber attacks rises as health services become more digital, which can have consequences for the law and reputation.

Valuation

Cigna is currently trading at a forward PE-ratio of 11.6. This seems pretty low considering the companies 5-year average PE of ~14. However, as can be seen below, there is a general reduction of the PE ratio visible over the last 5 years, which indicates that the average PE might be too high for today's company.

Comparing the PE Ratio to United Health Group, one of Cigna's major competitors, the company also seems to be trading at a discount.

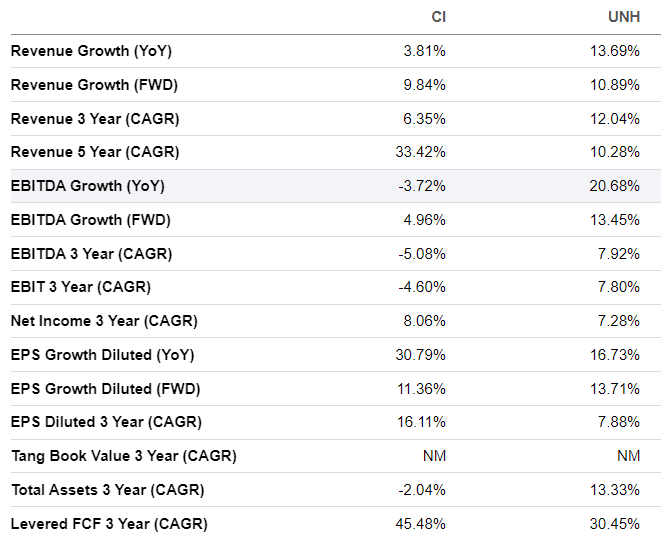

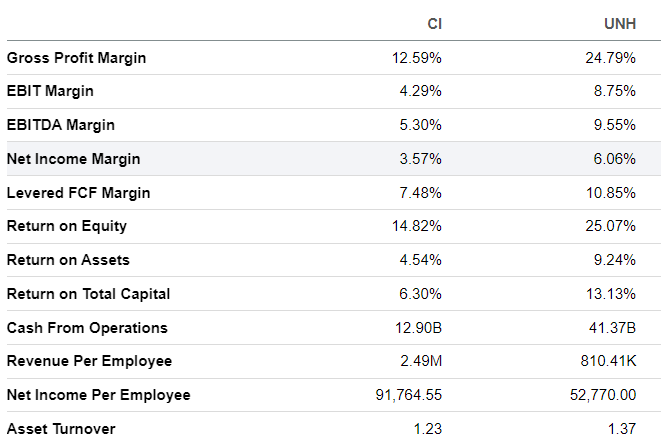

When we compare the two companies in growth and profitability, it becomes clear that UNH is the higher quality company of the two:

Growth Metrics CI vs. UNH (seekingalpha.com)

{kind=link}

Profitability Metrics CI vs. UNH (seekingalpha.com)

{kind=link}

While this gap in quality, in my opinion, justifies a premium on UNH's side, the difference in valuation between the two companies seems unreasonable.

This "mispricing" can be caused two ways:

- UNH is too expensive, which isn't the case right now, in my opinion. More on that here in my latest article on UNH.

- CI is attractively valued right now.

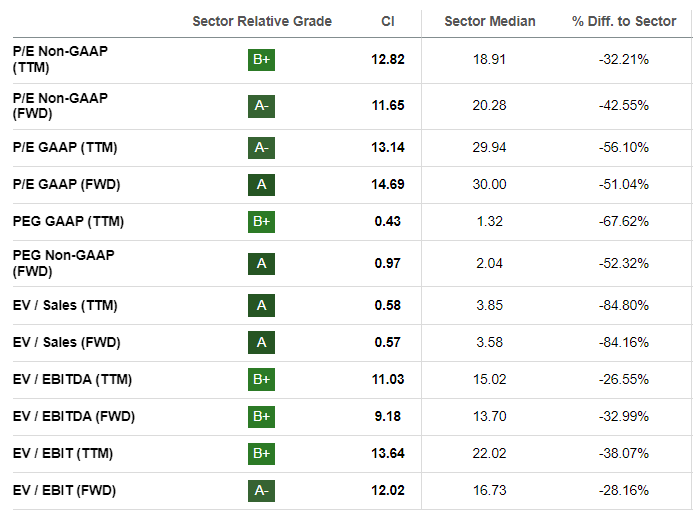

The Seeking Alpha Quant rating system is also currently rating Cigna with (mostly) very good valuation grades ranging from B+ to A.

Cigna's SA Valuation Grades (seekingalpha.com)

{kind=link}

Discounted Cash Flow Analysis

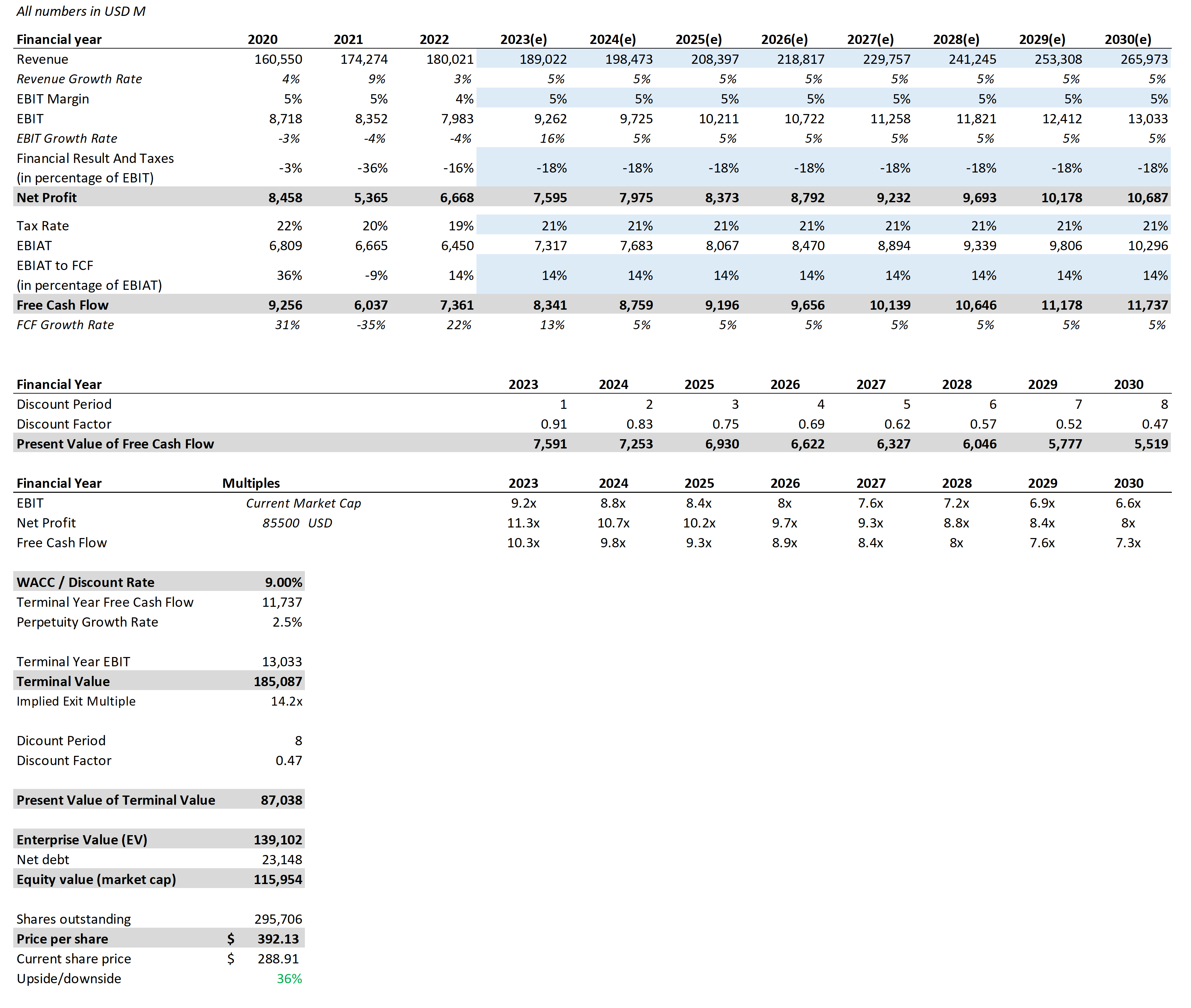

Looking at the metrics of the past and comparing the company to one major competitor and to the sector median, the company look attractively valued. Let's now take a look into the future and try to predict Cigna's future development via a Discounted Cash Flow Analysis ((DCF)). Blue cells are the assumptions I took, to evaluate the company.

- Revenue: I predicted a defensive annual revenue growth rate of 5%. This is in line with Cigna's 3-year average growth rate. For 2023 the company guided adjusted revenue of at least $190 billion, whereas I used $189 billion, which is pretty much in line.

- EBIT Margin: For the EBIT margin, I used the average of the last 3 years and anticipated that it will stay flat at 5%till 2030.

- Financial Result And Taxes: I averaged the values of the last three years and therefore used -18% to calculate the Net Profit for the years 2023 to 2030.

- Tax Rate: For the tax rate, my calculations were pretty much the same. I averaged out the last three years and then anticipated that it'll stay flat at 21% over the next years. This is also the low end of managements guidance for 2023.

- Free Cash Flow: With the metrics for 2020 to 2022, I averaged out the EBIAT to FCF ratio and assumed it'll stay flat over the next years.

- WACC: I used the current WACC of CI, which currently sits at around 9%.

- Perpetuity Growth Rate: The perpetuity growth rate assumed for the analysis is a conservative 2.5%.

Discounted Cash Flow Analysis Cigna (seekingalpha.com; thecignagroup.com)

{kind=link}

Risks to this analysis

The DCF assumes a revenue growth rate of 5% and the margins to stay flat at the average of the last three years. If one of the above-mentioned weaknesses (Complex Regulatory Environment, High Debt, Dependence on U.S. Market) or one of the threats (Intense Competition, Regulatory Changes, Economic Fluctuations, Cybersecurity Threats) comes into play, the companies fundamentals may experience a sharp decline. Especially, potential regulatory changes paired with its high dependence on the US could pose a significant risk to the companies fundamentals.

Conclusion

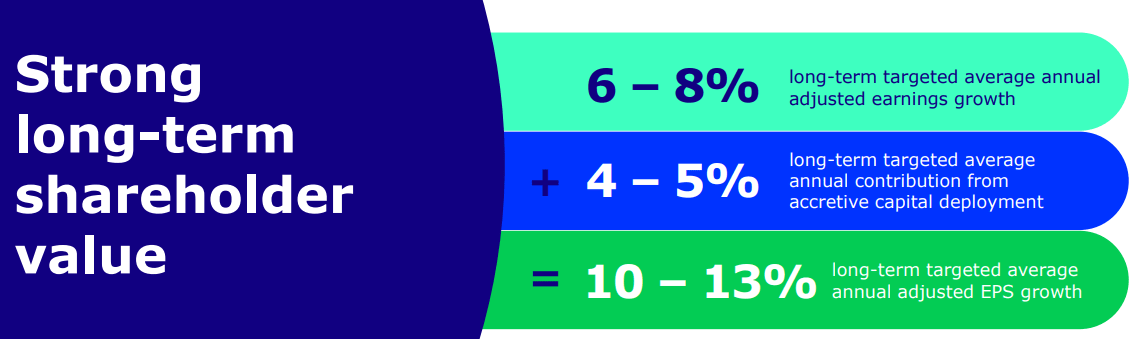

We took pretty conservative assumptions. The management itself is predicting a long term annual adjusted earnings growth between 6 to 8%, while we predicted a growth rate of 5%.

Q2 Earnings Cigna Group (thecignagroup.com)

{kind=link}

Based on our conservative Discounted Cash Flow analysis, we arrive at a price target of $392, which indicates that the company could be undervalued by ~35%.

Taking into account both valuations methods - a peer comparison and the Discounted Cash Flow Analysis - the company appears to be trading at an attractive entry point. While there are risks to consider, especially due to potential regulatory changes in Cigna's main market in the US, I still believe a position in CI is a solid investment into the Health Care Services industry right now, which is why I currently rate the company a 'Buy', with a price target of $350.

For further details see:

Cigna: Attractively Valued In The Healthcare Sector