CPXGF - Cineplex: Why I Believe Shares Can Double From Here

2024-01-02 01:47:28 ET

Summary

- Cineplex operates movie theaters and offers a wide range of entertainment venues and activities.

- The company has experienced a slow recovery from the impact of the pandemic, but recent results show strong sales and profitability.

- The company aims to reignite theatrical exhibitions, expand its LBE concepts, and improve operational efficiencies for future growth.

- Industry outlook is looking better as the writers' strike has concluded, and several promising movies are scheduled for 2024.

- Cineplex trades at an attractive valuation and has the potential to double from here based on my estimates.

Please note all $ figures in , not , unless otherwise stated.

Investment Thesis

After a tumultuous few years during the pandemic, Cineplex ( CGX:CA ) has been on a role with another quarter of great results. With a focus towards paying down debt, Cineplex looks like it can improve its financial position. In my view, this will be supported by stronger profitability going forward, more LBE venues, and operational improvements. The outlook is looking better for the company as pent-up demand drives consumers to the theatres and the conclusion of the writers' strike brings new and exciting movies to the cinema. At a dirt cheap valuation, Cineplex shares look attractive, and I see the company's shares doubling from here.

Company Overview

Cineplex is an entertainment company that has a dominant presence in the movie theatre business in Canada. As one of the largest cinema chains, it lets movie goers experience a wide variety of viewing experiences including IMAX, VIP lounges with luxury seating, 3D screenings, and more.

But Cineplex is not just a theatre and cinema company. Over the last decade, the company has become a more diversified entertainment company offering amusement and leisure through The Rec Room and Playdium, which offer a wide range of activities and attractions (eg. arcade games, VR, food and beverage, and other entertainment) for those looking for a fun place to socialize in vibrant entertainment spaces.

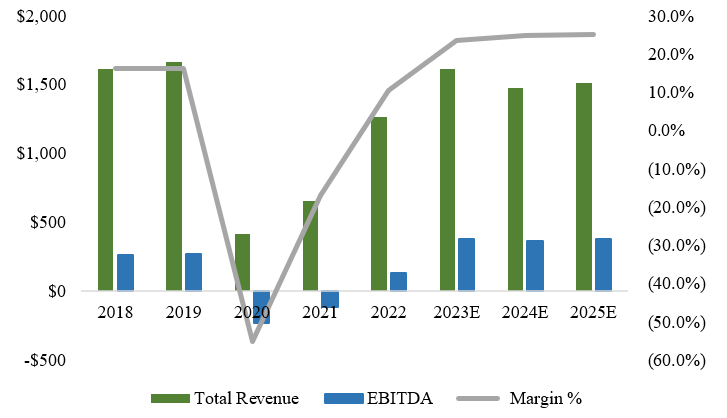

One of the big events over the last few years for Cineplex (and the movie theatre and entertainment industry in general) has been the impact of the pandemic. Since 2020, box office sales in North America have still not reached their peak in 2018. Since the trough three years ago, box office sales have begun a slow recovery.

This has also been true for annual revenues of Cineplex, with film entertainment and content being their largest segment at 75% of revenues. In 2020, sales fell 74.9% and the company went two years without making a profit. Things definitely seem to be back on track now, but the company has been burdened with a heavy debt load as a result of the damage.

Revenues and EBITDA (Author, based on data from S&P Capital IQ)

{kind=link}

Recent Results

When looking at Cineplex's most recent quarterly results , the company announced its best Q3 ever with sales of $463.6 million adjusted EBITDA of $83.1 million. While this quarter not only surpassed the Q3 of 2019 pre-pandemic, this was also a quarter with significantly better adjusted EBITDA margins at 18%. This showcases the cost cutting strategies that Cineplex has been able to implement as well as the operational improvements the company has been able to achieve since then.

Given the strong box office sales we saw this quarter (and for the year in fact), there were some great movies that came out this year that definitely helped Cineplex. 'Barbie' and 'Oppenheimer' collectively brought in $2.5 billion to the box office and movies like 'Mission: Impossible - Dead Reckoning Part One' also helped too. There's good reason to believe that this should continue in my view given the huge amount of movies scheduled to be released in 2024 and the fact that the writers' strike has now ended. With more consumers hitting the movies again, there's good reason to believe that Cineplex will likely see continued growth in the upcoming quarters.

The strong growth and sales couldn't have come at a better time for Cineplex. For the last few years, Cineplex has had a debt problem with $815 million of long-term debt on its books which has put its Net Debt to EBITDA ratio at 3.7x. Cineplex is a $532 million market cap company so clearly the debt load here makes up a big portion of its enterprise value. That said, with the two most recent quarters, the company was able to reduce its debt by $55 million as a result of strong profitability.

When it comes to debt management and the path to deleveraging, CFO Gord Nelson had this to say:

At the end of Q3 2023 we had approximately $867 million face value of debt, including $316.3 million in convertible debentures, which have a conversion price of $10.94. All our equity research analysts have a one year target price in excess of the conversion price. In the 75% to 80% attendance world, we believe that the convertible debentures would convert to equity. And as mentioned earlier, we would be within our target leverage ratio range of 2.5x to 3x and on the path to consider the reintroduction of dividend.

Based on management's comments, it seems that these convertible debentures will likely convert, so some level of dilution risk to equity holders should be factored in here. Over time, Cineplex hasn't diluted shareholders and the share count has only increased marginally from 62.8 million shares to 63.4 million over a ten-year period.

If there was a conversion, we should expect that the share count increase by 46%, given the face value amount of $316.3 million and conversion price of $10.94 ($316.3 million divided by $10.94 to get an additional 28.9 million shares added to the share count). Given that shares are trading at 9.4x next year's earnings, this risk has likely been priced into the stock already (and could act as a cap near term to the share price) but I still think it's worth mentioning here.

With respect to the remaining portion of long-term debt, the company has a credit facility with $541 million of capacity ($301 million used) at an interest rate of 6.4% maturing in November 2024. It also has notes payable of $247 million at an interest rate of 7.5% maturing in February 2026. These are pretty near term maturities for long-term debt, so it will be important for Cineplex to have capacity to extend its maturities and refinance at a favorable rate. Over time, management expects to get rid of the current covenants and restrictions and reinstate its dividend once it's able to improve its financial position.

Outlook

When it comes to the company's business strategy going forward, management wants to reignite theatrical exhibitions, prove out its location-based entertainment (LBE) concepts, and generate operational efficiencies.

For reigniting theatrical exhibitions, Cineplex wants to increase attendance in its theatres and drive traffic by growing CineClub and Scene+ programs. Scene+ already has 14 million members (almost a third of the Canadian population) and is a way for Cineplex to build loyalty with its customers. In building out its LBE concept, we've already seen 10% year over year growth in this division so building scale through new builds will be key. In my view, given that the LBE margins are nearly double than those of the film entertainment and content segment, this should also drive meaningful earnings expansion over time. On the operational efficiencies front, Cineplex also has a huge opportunity to continue to expand margins by incorporating automation into its business practices and using excess space to provide more entertainment experiences.

In terms of the broader industry dynamics and overall macro outlook, 2024 should bring a similarly strong set of films to the theatres that should translate to similar sales for Cineplex going forward. In my view, with many not having visited the theatres during the pandemic, I think there's still room for pent-up demand from consumers that should translate into a good rebound over the next few quarters. With the writer's strike concluded there shouldn't be many production delays anymore so we can likely expect a steady stream of movies hitting the theatres. Moreover, Cineplex has said that it doesn't foresee material impacts to sales going forward as a result of the strikes.

Finally, with more LBE experiences opening, I'm pretty sure we can expect to see gross margin improvement for Cineplex. While only 10% of sales right now, I expect revenues for LBE could double three or four years out, given the growth we've seen recently.

Valuation

Based on the six equity research analysts with one-year target prices on Cineplex's stock, the average price target is $12.97, with a high estimate of $14.82 and a low estimate of $11.36. From the average, this suggests potential upside of 52.4% from the current market price, indicating that analysts are bullish on the outlook of the company.

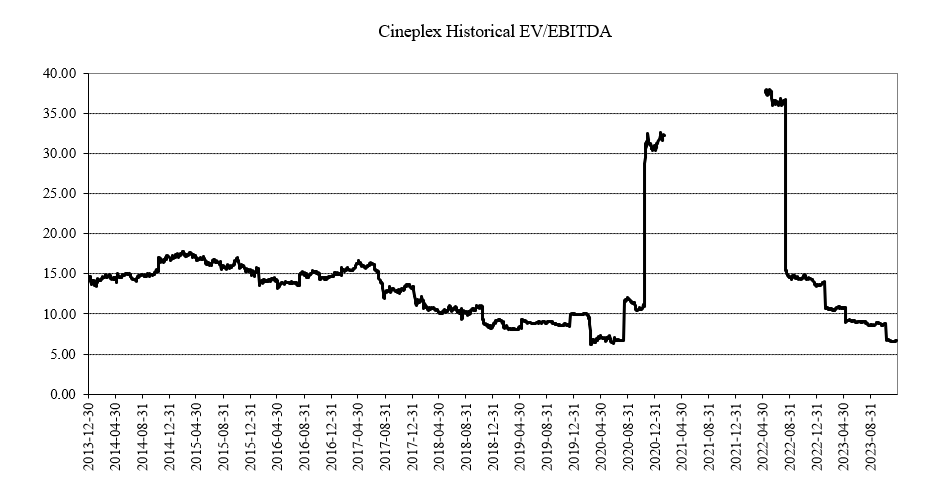

Not factoring in the conversion for debentures, based on consensus estimates for EPS, shares of Cineplex are trading at forward multiples of 6.0x EV/EBITDA for 2024 and 5.7x EV/EBITDA for 2025. Its forward P/E multiples are 9.4x next year's earnings and 5.6x 2025 earnings.

Historical EV/EBITDA (Author, based on data from S&P Capital IQ)

{kind=link}

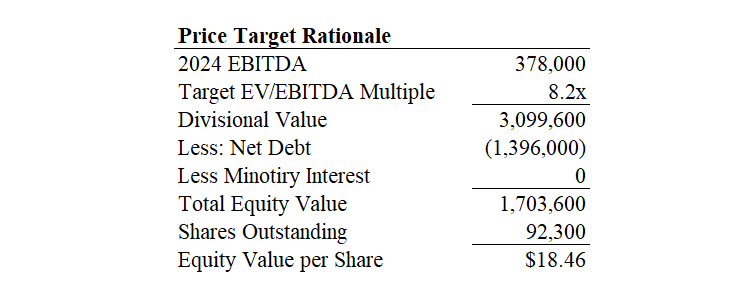

When we consider that pre-pandemic, Cineplex traded in a range between 8.2x to 17.9x EV/EBITDA, Cineplex shares look to be very cheap at 6.6x EV/EBITDA. If we take this year's EBITDA of $378 million and apply a conservative 8.2x multiple and subtract the net debt assuming conversion of the debentures, we get an equity value of $1.7 billion. Dividing by the new number of shares outstanding (46% increase from current shares outstanding due to conversion), we get an equity value per share of $18.46, implying more than a double from the current price.

Price Target Rationale (Author, based on data from S&P Capital IQ)

{kind=link}

While this may seem like high potential upside, I don't believe my estimates are unreasonable. In using the 8.2x multiple, I'm assuming the low end of what Cineplex was trading at pre-pandemic. I also believe that with the movie industry back on track with the writers' strike over and people going back to the theatres again, Cineplex deserves a higher multiple.

Conclusion

Cineplex has weathered the challenges of the pandemic well and is back on track after a couple great quarters. They company has shown its own the right track by paying down debt, building out its LBE venues, and improving its margins. Despite its debt load, this seems to be the right time to buy as the writers' strike is over, there's a promising lineup of films scheduled for release in 2024, and people seem to want to go to the movies again. So looking ahead, my outlook is optimistic. With the current valuation, Cineplex shares are just too cheap, even when we factor in dilution for the convertible debentures. Ultimately, while challenges persist, I believe the rewards outweigh the risks, and that the company's strategic initiatives, financial discipline, and overall industry recovery paint a promising picture for the foreseeable future. For these reasons, I'm a buy on shares of Cineplex today.

For further details see:

Cineplex: Why I Believe Shares Can Double From Here