C - Citigroup: 20000 Job Cuts Big Step Towards Richer Earnings And Investor Payouts

2024-01-14 00:44:25 ET

Summary

- Citigroup reported a worse-than-expected top line and a $1.8 billion loss, but the loss was mostly due to restructuring charges.

- The bank announced plans to cut 20,000 jobs and exit competitive and risky businesses to simplify operations and optimize resource allocation.

- Despite disappointing Q4 results, Citigroup's structural earnings power and undervalued stock offer attractive upside potential.

- According to CFO commentary, Citi may potentially achieve an 11-12% ROTE, suggesting the bank's projected earnings multiple for 2025/2026 could be as low as 5-6x.

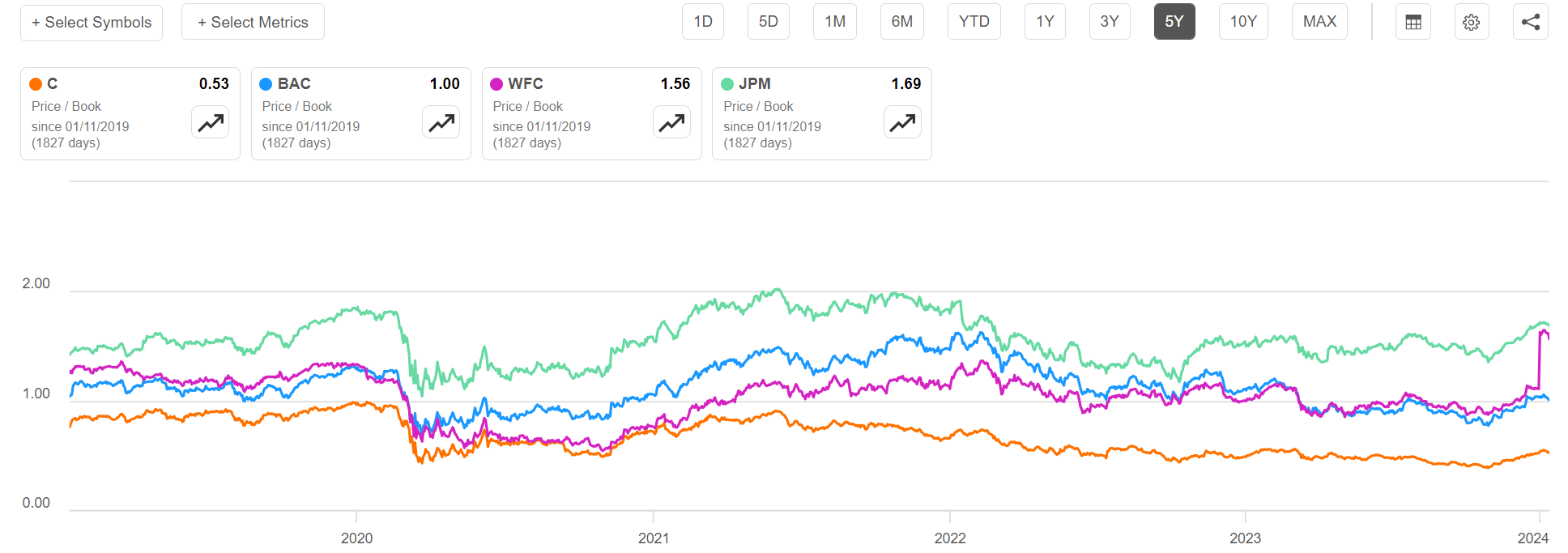

Citigroup ( C ) reported earnings for the December quarter on 12th January, and surprised investors with quite a few notable insights: On the negative, the U.S. bank reported a worse-than-expected topline and a disappointing $1.8 billion loss. On the positive, the loss was mostly driven by restructuring charges and other non-operating costs. In fact, Citi management shared ambitions to accelerate the multi-year restructuring efforts, announcing a projected 20,000 job cuts. Following the announcement, shares in Citigroup jumped by about 1%, while JPM, BAC, and WFC closed -1%, 1%, and -3%, respectively. In my opinion, this price action may be the first, tentative expectation of investors that the accelerated restructuring efforts may help to close the valuation gap with key U.S. bank peers. For reference, Citi shares are currently trading at approximately 0.5x P/B, significantly lagging the valuation of JPMorgan ( JPM ) Bank of America (BAC), and Wells Fargo ( WFC ). Notably, this relative undervaluation has persisted for many years now.

{kind=link}

Seeking Alpha

Looking into 2024 and beyond, I am bullish on Citigroup stock, as I believe shares are undervalued relative to the bank's fundamentals and cyclically adjusted earnings power. Moreover, I am optimistic about the macro backdrop as the Fed's dovish rates shift may support stabilizing net interest income on falling deposit cost pressures, as well as stimulate investment banking volume.

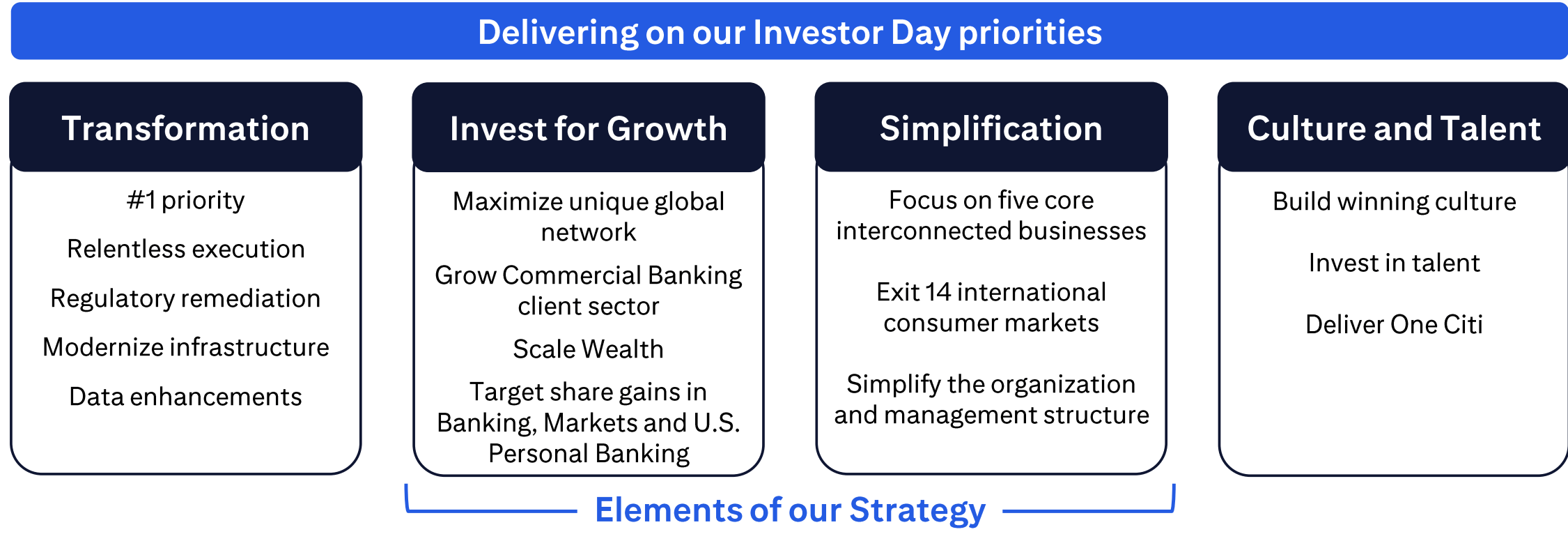

Citigroup Is Accelerating Restructuring Efforts

Citigroup is gearing up for a crucial year as it aims to reverse its underperformance compared to rivals JPMorgan Chase & Co. and Wells Fargo & Co. in 2023. CEO Fraser and CFO Mark Mason are facing mounting pressure to prove it. In that context, Citi's management team is actively working to reduce the size of the bank, simplify operations, and optimize resource allocation for growth.

{kind=link}

Citi Q4 Results

Already leading up to Q4 reporting, Citi management has announced the bank's exit in competitive and risky businesses such as municipal-bond and distressed-debt trading , following the bank's divestment of a significant portion of its international retail business -- e.g., Taiwan, as well as Russia and Argentina .

Together with Q4 results, Citigroup disclosed plans to cut about 20,000 jobs, affecting about 8% of the bank's workforce (240,000). In that context, The anticipated cuts may incur expenses of up to $1.8 billion, as stated by Citi on Friday, with potential savings reaching $2.5 billion annually by 2026 upon completion. Investors should note that applying an 8x P/E multiple to the $2.5 billion cost savings, and discounting at an 8% annual cost of capital, the equity upside to the job cuts may amount to $17 billion, or 15-20% upside to the bank's current equity valuation. On that note, the 1% trading pump following the announcement looks too timid, even accounting for an enormous, implied execution risk buffer.

In addition to the job cuts resulting from the restructuring process, the bank anticipates an additional reduction of 40,000 workers through planned exits from its consumer banking business in Mexico and other regions. If this scenario plays out as projected, Citi management has indicated that its overall workforce may decrease to as low as 180,000 by 2025 or 2026 (-60,000 delta vs. Q4 count).

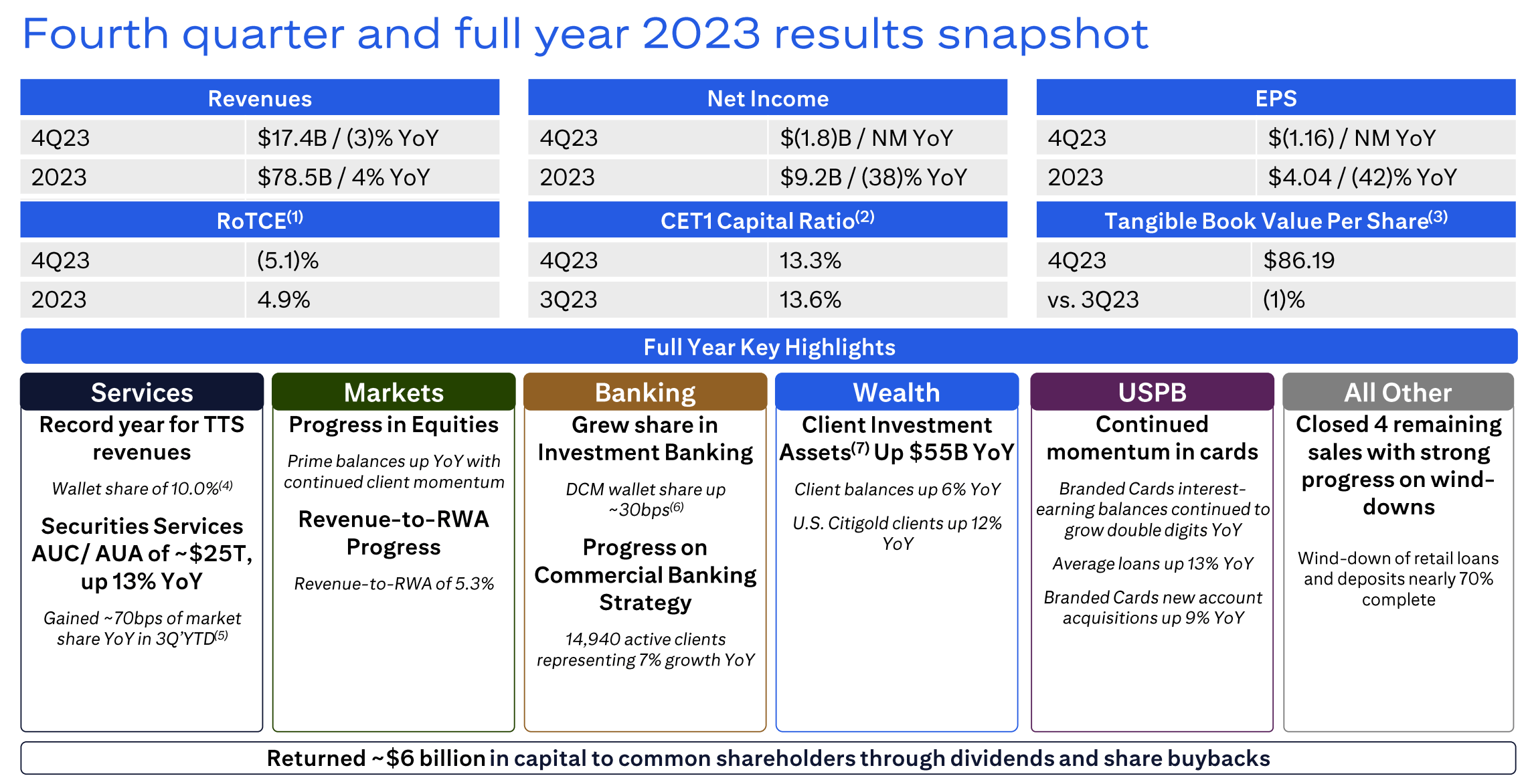

Q4 Results Were Disappointing ...

For the last quarter of 2023, Citigroup's fundamentals were overshadowed by a $1.8 billion loss. In that context, investors should note, however, that the loss was primarily influenced by $4 billion in charges and expenses. This includes $800 million linked to the restructuring efforts and significant impacts from its exposure to Russia, as well as the devaluation of Argentina's peso. Within the $4 billion in charges and expenses, there is also a notable payment of $1.7 billion as part of a "special assessment" from the Federal Deposit Insurance Corporation, aimed at recovering losses tied to regional bank failures in the previous year.

Still, even after excluding one-off charges and expenses, the bank's revenues slipped by 3% to $17.4 billion while the operating income declined by more than 20% compared to the fourth quarter of 2022. Citigroup's full-year earnings dropped by 38% from the previous year to $9.2 billion.

Challenges in Citi's Q4 performance can be mostly attributed to corporate lending experiencing a 26% drop due to decreased demand for borrowing resulting from higher interest rates. Additionally, a reduction in market volatility towards the end of the year negatively impacted the bank's traders, with revenue from the sales and trading in FICC down by 25%. Despite these challenges, there were also a few encouraging reads: Increased spending on the bank's credit cards contributed to a 12% rise in revenue in its consumer banking division, while corporate spending boosted revenue in Citi's treasury services division by 6%. Moreover, also the investment banking division performed well, up more than 20% year over year and marking its best result in over two years.

Lastly, investors will certainly appreciate that for FY 2023, Citi's payout ratio on earnings was about 73%. During the year, the bank returned close to $6 billion to investors in the form of dividends and buybacks, implying a notable 6-7% equity yield.

{kind=link}

Citi Q4 Results

... But Structural Earnings Power Is Encouraging

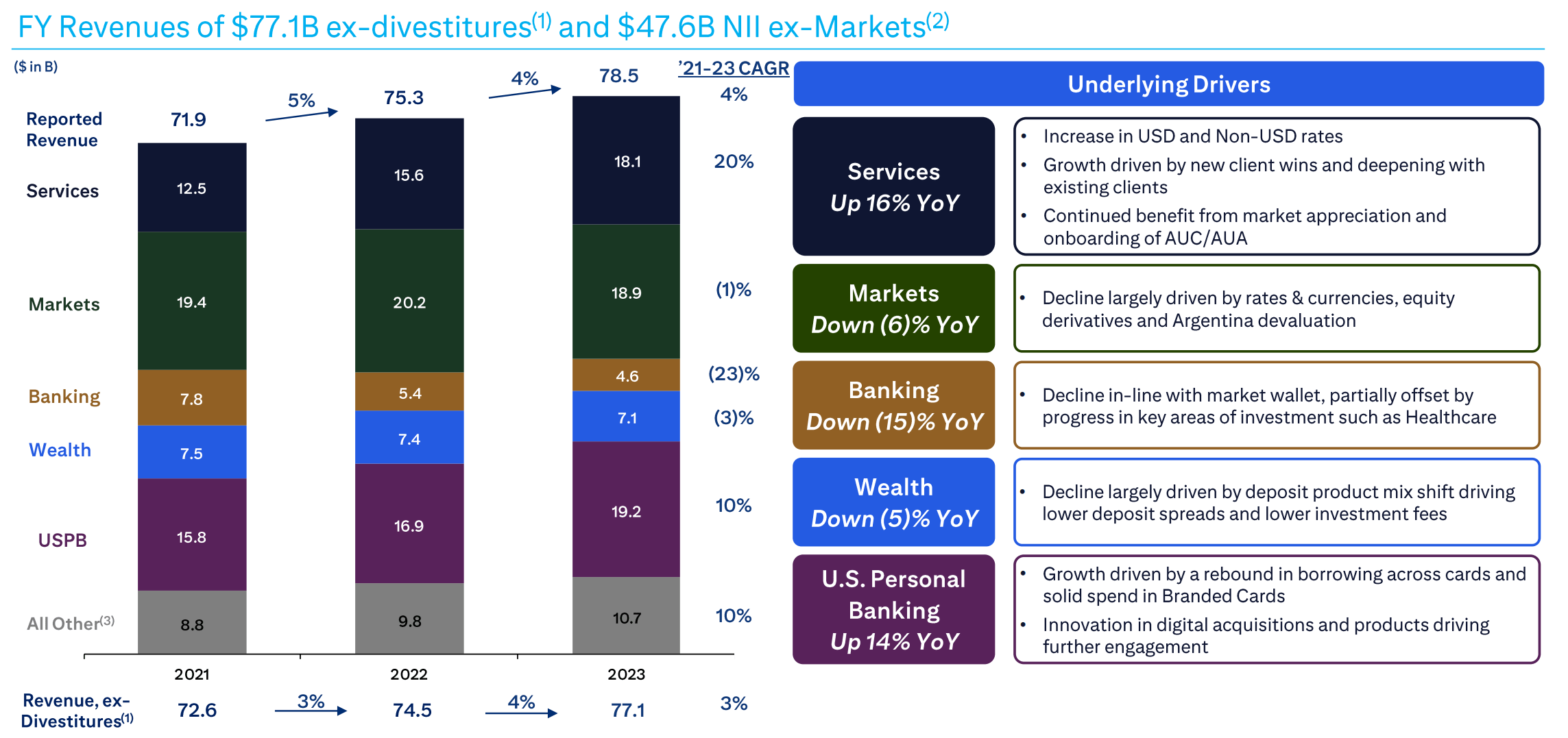

Considering all the restructuring that is going on with Citi, investors are advised to look beyond quarterly numbers and anchor their Citi stock investment assessment on the bank's structural earnings power. On that note, I point out that Citigroup's CFO, Mark Mason, recently outlined projections for a 4-5% CAGR revenue growth through 2026, targeting an annual topline of $87-92 billion. The moving variables to this target are based on a supportive growth outlook across Citi's segments: In Treasury and Trade Solutions, around half of the 18% revenue surge is independent of rates, suggesting a potential $4 billion incremental topline upside by 2026. Investment Banking anticipates growth from a depressed 2023 base, with fees potentially increasing by $1-3 billion in line with economic expansion. Wealth Management targets market share growth from 2% to potentially generate $2-3 billion in additional revenue. The remaining revenue delta for the 4-5% CAGR target may come from Markets/Trading and/or the Card division, considered feasible by the CFO.

These projections are not unreasonable, in my opinion. In fact, they broadly reflect trends seen in the past couple of years, as highlighted in the below graph.

{kind=link}

Citi Q4 Results

Meanwhile, and as a consequence of the restructuring, operating expenses are set to compress to $51-53 billion per year, below the 2023 level of $54.3 billion. If the CFO's projections are correct, Citi may potentially achieve an 11-12% ROTE.

Most notably, projecting Citi's 11-12% ROTE to 2025/ 2026, and applying the bank's 2023 payout percentage of 73%, suggests that investors who buy shares at current 0.5 P/B may potentially enjoy a 15-17% distribution yield by 2026 (dividends and buybacks), according to my modeling.

Valuation Should Offer Attractive Upside

Citigroup stock looks materially undervalued to me, currently trading at an approximate 0.5x P/BV and a 9x projected multiple on 2024 earnings. Investors should consider, however, that adjusting Citigroup's earnings multiple for restructuring and growth, the bank's projected earnings multiple for 2025/ 2026 could be as low as 5-6x (on an 11-12% projected ROTE). In my opinion, as the restructuring efforts gradually materialize, and Citi's ROTE improves, the bank's share prices should undoubtedly trend towards 0.8-0.9x P/B, suggesting that Citigroup stock may be 60-80% undervalued.

While investors wait for the fundamental thesis to play out, sentiment should be supported by growing confidence in a dovish rates shift that will likely contribute to optimism about an improved credit environment extending to supportive loan growth and manageable write-downs, in addition to an improved macro environment for investment banking activities.

I recommend Citi shares with a Buy.

For further details see:

Citigroup: 20,000 Job Cuts Big Step Towards Richer Earnings And Investor Payouts