C - Citigroup: After A Monstrous Surge It's Time To Play Defensive (Downgrade)

2024-01-13 11:28:49 ET

Summary

- Citigroup stock has recovered nearly 45% from its October 2023 low, normalizing its earnings multiple with its 10Y average.

- As a result, C's surging optimism reversed its gloomy pessimism in just three months, outperforming its financial sector peers.

- The bank plans to reduce 20K positions and achieve significant expense savings, leading to a lowered expense forecast range.

- With its net interest income growth likely to have peaked in 2023, the market will likely focus on its ability to cut expenses moving ahead.

- While C remains materially undervalued, I assessed that the entry levels are less attractive than my previous update in October. I argue why investors should remain cautious now.

The valuation bifurcation in Citigroup ( C ) shares has finally reached peak pessimism as C recovered nearly 45% through its January 2024 highs from its late October 2023 bottom. As a result, it has also normalized C's forward adjusted earnings multiple of 10x with its 10Y average of 9.5x. Therefore, I believe it's apt for me to provide an update from my previous Strong Buy rating, given C's surge over the past three months.

Long-term Citigroup holders should be aware of its significant underperformance, as it delivered a 10Y total return of 2%. Despite that, I believe investors have understood the importance of assessing investor psychology and its role in determining highly attractive risk/reward profiles, leading to significant market outperformance. C's relative outperformance against its financial sector ( XLF ) peers corroborates my assessment, even though Citigroup delivered a " disappointing " fourth-quarter or FQ4 release.

In other words, notwithstanding its tepid release, C's outperformance suggests the market is looking forward to an improved outlook in the medium term relative to its previously highly attractive valuation. The bank posted its Q4 release on Friday, as CEO Jane Fraser highlighted that " the fourth quarter results were notably disappointing." Fraser underscored that Citigroup believes 2023 was a "foundation year," setting the stage for its medium-term (FY26) RoTCE target of between 11% and 12%. As a result, Citigroup remains a work in progress, suggesting investors must continue to expect "significant structural and strategic changes within Citigroup.

Therefore, I'm not surprised that the bank likely needed to make a headline-grabbing announcement to demonstrate its commitment to investors about its desire to transform. Observant investors should have noted Citigroup's decision to shed 20K positions (ex-Mexico), aiming to achieve "over $2B to $2.5B in run-rate savings." Management presented that its ongoing organization restructuring is expected to attain "over $1 billion in run-rate savings from the net elimination of approximately 5,000 roles, mainly in management" at the end of the first quarter.

Accordingly, management anticipates a lowered expense forecast range of between $53.5B and $53.8B, slightly below its previous estimate of $54.3B. However, the 20K job cuts are expected to reduce its expense outlook markedly post-2024. As a result, management expects its long-term expense outlook to fall to $52B at the midpoint of its forecast range.

I believe C's sharp re-rating and outperformance over the last three months suggests that the market is optimistic about Fraser's strategic pivot. Even though the bank remains a work in progress, its valuation is still reasonable. Seeking Alpha Quant assigned Citigroup stock a "B+" valuation grade, relatively less attractive than its "A" grade three months ago. Despite that, management highlighted that C continues to trade well below its tangible book value per share or BVPS of $86.19. As a result, management is confident that its attractive valuation is conducive for the bank to continue to return capital to investors in 2024, "including modest buybacks in Q1 2024."

As C's valuation normalized in line with its 10Y average, I believe the next step forward could be more challenging. The market will likely be less tolerant over execution misses, as Citigroup's net interest income or NII has likely peaked. Management is confident it could achieve a 2024 revenue outlook of between $80B and $81B. In other words, the bank doesn't anticipate a significant impact from lower interest rates.

Citigroup highlighted that its guidance had contemplated an "assumption of three to six Federal Reserve rate cuts in their NII forecast." Based on the Fed's recent commentary , I assessed Citi's assumption as reasonable, as inflation rates remain relatively high and not expected to fall more steeply than anticipated. As a result, that should provide more clarity over Citigroup's topline assumption. With that in mind, it should bolster the bank's decision to up the ante in lowering its expenses, improving its ability to move toward its medium-term RoTCE guidance.

{kind=link}

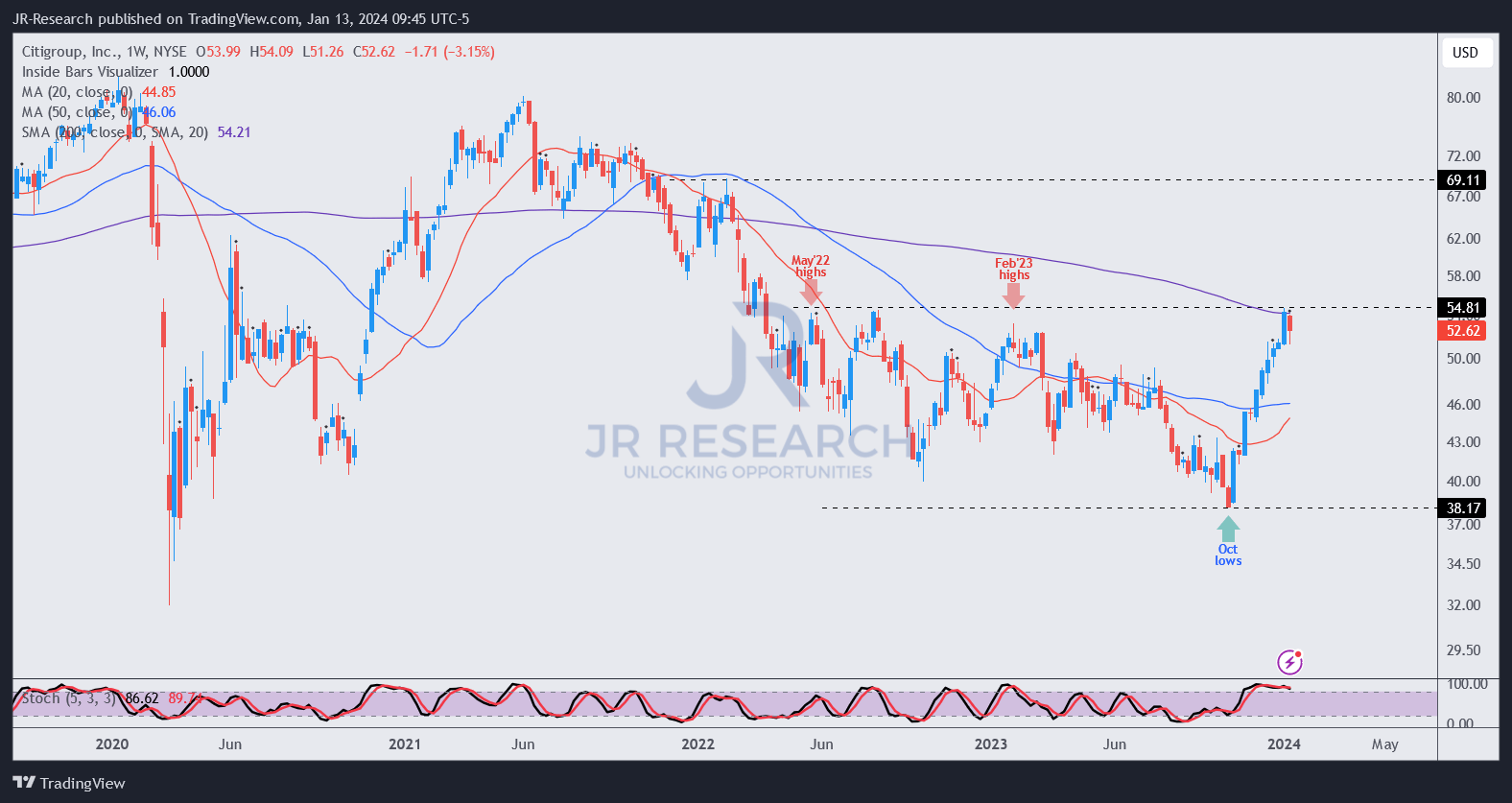

As seen above, C's price action indicates a momentum surge that re-tested the $55 resistance level, which has been in play since May 2022. While I assessed that C's valuation remains relatively attractive, Citigroup must still prove its ability to navigate the NII headwinds this year. Furthermore, the market will not likely re-rate C much higher in the near term unless it assesses Fraser and her team are expected to make significant progress in meeting its 11.5% medium-term RoTCE outlook at the midpoint. In other words, I expect C to remain materially undervalued relative to its tangible BVPS for now.

Investors who missed partaking in buying C's significant dips over the past year are encouraged to allow a welcomed profit-taking or distribution phase, allowing the market to digest its recent surge before adding.

Rating: Downgraded to Hold.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

Citigroup: After A Monstrous Surge, It's Time To Play Defensive (Downgrade)