C - Citigroup: Asymmetric Risk-Reward Opportunity

2023-11-26 05:24:11 ET

Summary

- Citigroup's target of 11% to 12% return on tangible equity in the medium term is doubted by analysts and investors.

- If Citigroup achieves its target, the share price could reach 1.1x to 1.2x tangible book value.

- Citigroup's tangible book value is expected to reach around $100 by the end of 2025, with a conservative valuation of $80 per share.

Most analysts and investors absolutely do not believe Citigroup ( C ) will meet its target of 11% to 12% return on tangible equity ("ROTE") in the medium term (defined as 2025 and 2026). This is plainly obvious by looking at the share price that currently trading at ~0.5x tangible book value. This essentially means that almost everyone in the market is positioned on one side of the boat....hence the opportunity for investors.

From a valuation perspective, if Citi is able to achieve its target, this should translate to a share price of 1.1x to 1.2x tangible book value, assuming the cost of equity is at the generally accepted long-term average for large banks at ~10%.

By the end of 2025, I expect Citigroup's tangible book value to reach ~$100. It is currently at $86.90 and has grown 8% over the last 12 months. I expect it to conservatively grow by 7% annually and higher if large buybacks return.

If Citi is able to meet its targets of 11% to 12% ROTE, then the share price should be valued at $110 to $120 or 2.6-2.7x current share price.

Do I believe Citi will meet its targets of 11% to 12% ROTE?

I think it is a possibility but not my base case. My base case is that Citi will deliver ~10% ROTE by the end of 2025 and therefore I would attribute it a conservative valuation of ~0.8x TBV or $80 share price.

This is almost double the current share price but where it gets much more interesting is using call options or LEAPs to supercharge the potential returns.

The 3 Core Deliverables to Make the Math Work

To make the math work, Citi needs to deliver on the following:

- Revenues

- Costs

- Capital

On the revenue side, Citi guided in the Investor Day for ~4-5% growth year on year. Year-to-date in 2023 , it delivered 6% growth (ex divestitures) which is obviously a positive and above medium-term targets. The areas of strength included Services that are benefiting from increased market share as well as rate tailwinds. Personal banking is also delivering revenue growth as Card balances increase. The area of weakness is Banking revenues due to high interest rates, and the capital markets activities have been subdued. Wealth Management also under-performed expected long-term growth rates of high single-digit/low teens and only managed to squeeze out 2% revenue growth year-to-date. However, this is the function of Citi's business model, different businesses are expected to operate better depending on macro conditions. All in all, it is not unreasonable for Citi to sustainably deliver 4% to 5% CAGR growth growing forward.

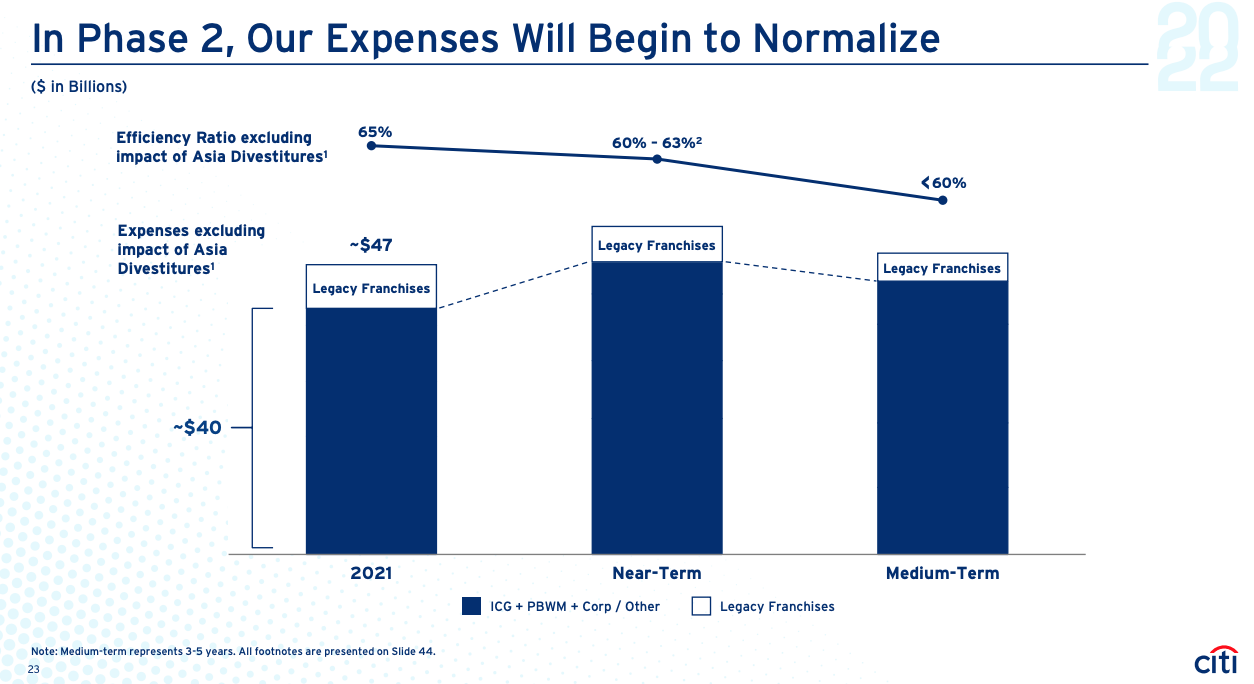

On the cost side, Citi projected the following in the 2022 Investor Day :

{kind=link}

Citi Investor Day 2022

The near-term can be seen as approximately 2023 or thereabouts. Citi is expected to print ~$54 billion of expenses in 2023, however, there are also large repositioning charges (>$1 billion). It is also guiding for bending the cost curve in the second half of 2024 and beyond. For the math to work on its return targets, Citi has to print somewhere around $51 billion in 2025/2026. If you back out of repositioning charges, then Citi is already in the $52-$53 billion range.

I have very little doubt, that Citi will deliver the cost cuts required and the recent cost actions announced are a very credible proof point along the way. If anything, should revenue disappoint, I'd expect Citi to press even harder on the cost and efficiency actions.

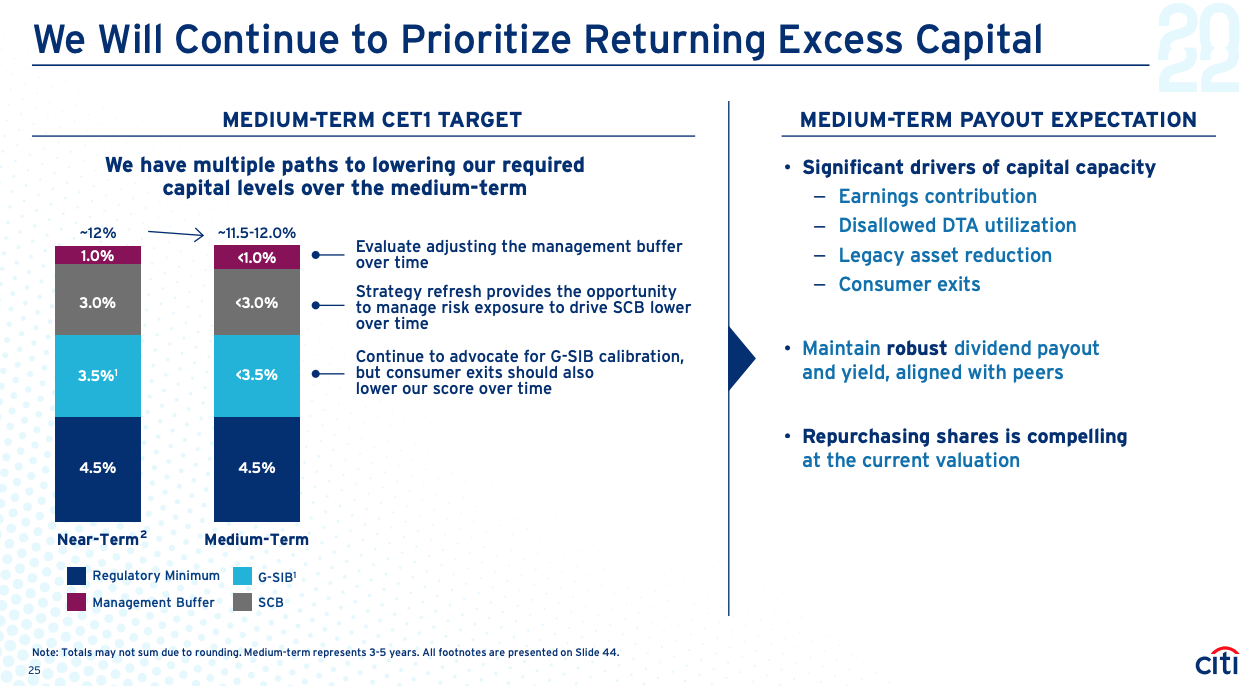

The capital question is somewhat more nuanced and the trajectory so far has not gone the way Citi expected it to as per the investors' day presentation:

{kind=link}

Citi Investor Day

Citi planned for its capital ratios over time to reduce to a target of 11.5% to 12%. Currently, its target has gone up to 13.3% predominantly due to an unwelcome outcome from the Fed's Stress Tests (otherwise known as the 2023 CCAR). Other headwinds include the final rules for Basel III. Citi projected the unmitigated outcomes of end-game regulatory reform to be in the range of 15% to 20% of additional capital. Post-mitigation and lobbying, a reasonable expectation would be in the range of 5% to 10%.

The tailwinds for capital are also strong and have not quite played out. Citi's disposals of the Global Consumer Bank and shifting of profit mix to Services and Wealth Management should certainly operate to reduce its capital surcharges (SCB and G-SIB scores). It should also benefit from a lower management buffer as well as utilization of the deferred tax asset currently disallowed. All in all, my base case is for a target CET1 ratio between 12% to 12.5% which is slightly higher than management has guided for previously.

Final Thoughts

To deliver its returns target, Citi has to triangulate its revenue, costs, and capital outcomes. So far, Citi is broadly on track despite the challenging macro environment. Almost no one in the Street believes Citi will deliver these returns. Whilst I think it is possible Jane Fraser will ultimately deliver, my base case is a much more conservative one (10% ROTCE and trading at 0.8x TBV). I think there is a reasonable probability Citi will deliver that. The risk/return is asymmetric in my view (the downside is limited), and for more aggressive investors an options strategy can be seen as especially attractive.

For further details see:

Citigroup: Asymmetric Risk-Reward Opportunity