C - Citigroup: Q4 Only A Restructuring Play Right Now

2024-01-20 01:43:50 ET

Summary

- Citigroup's fourth quarter results were disappointing due to extraordinary charges, causing a substantial drop in earnings.

- The bank's net interest income is expected to decline in 2024 as short-term interest rates are set to be slashed.

- Citigroup's ongoing restructuring efforts and poor financial performance make it a risky investment, with potential for further job cuts and expense management.

Citigroup Inc. (C) has profited, in terms of stock performance, from expectations about an ending rate hiking cycle, but the bank's fourth quarter results were anything but great. The bank recorded a number of extraordinary charges in the fourth quarter that caused Citigroup's earnings to drop substantially.

I think that Citigroup's net interest income is poised for a fall in 2024 as the central bank is going to slash short-term interest rate, which I would expect to be a headwind for Citigroup's valuation.

Taking into account that Citigroup's stock has rallied since the middle of the fourth quarter, and that Citigroup is still stuck in it restructuring, I am given Citigroup a pass.

My Rating History

Inflation and recession risks were, in April 2022, considerations for me to be skeptical about Citigroup's profit potential . Citigroup's exit from the Russian market also caused a profitability challenge.

The bank continues to be weighed down by ongoing restructuring efforts and Citigroup's fourth quarter earnings were not great. Citigroup should be expected to slash more costs moving forward to improve its profitability and remain a restructuring investment.

Substantial Profit Miss Due To Unexpected Charges

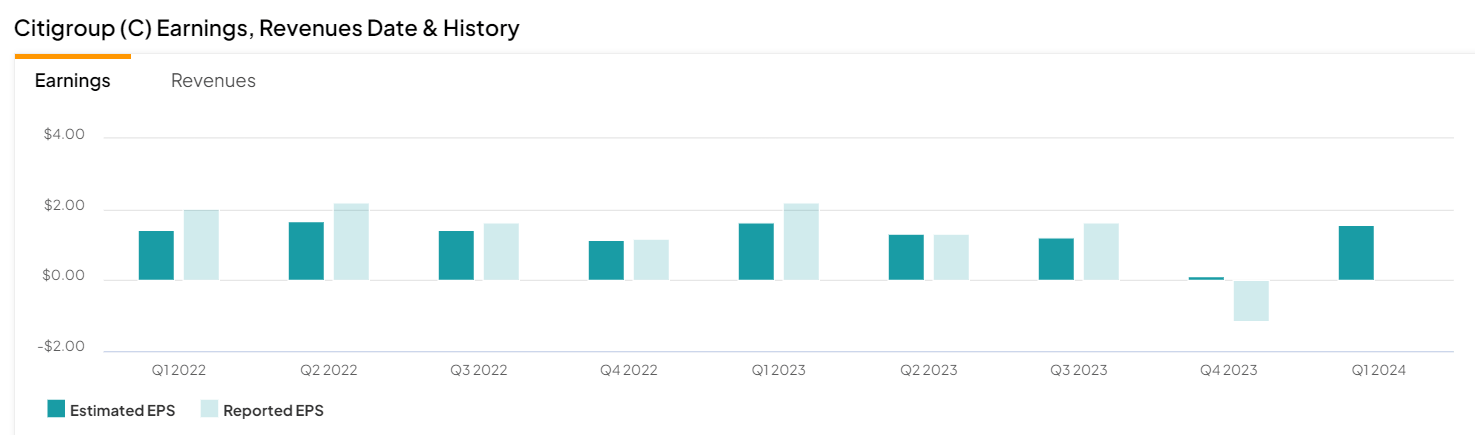

Citigroup's fourth quarter earnings may not be entirely comparable to last year's period because the bank recorded a litany of extraordinary charges that are distorting results. The bank reported a fourth quarter loss, on a per share basis, of $1.16 which compares to an estimated gain of $0.11 per share.

As I will discuss later in this article, some of Citigroup's charges related to banking crisis in 2023, causing higher FDIC contributions, as well as to problems in Argentina and to the bank's ongoing restructuring. Last week's 4Q-23 earnings were the worst in years, from an EPS beat perspective.

Estimated Earnings (Yahoo Finance)

{kind=link}

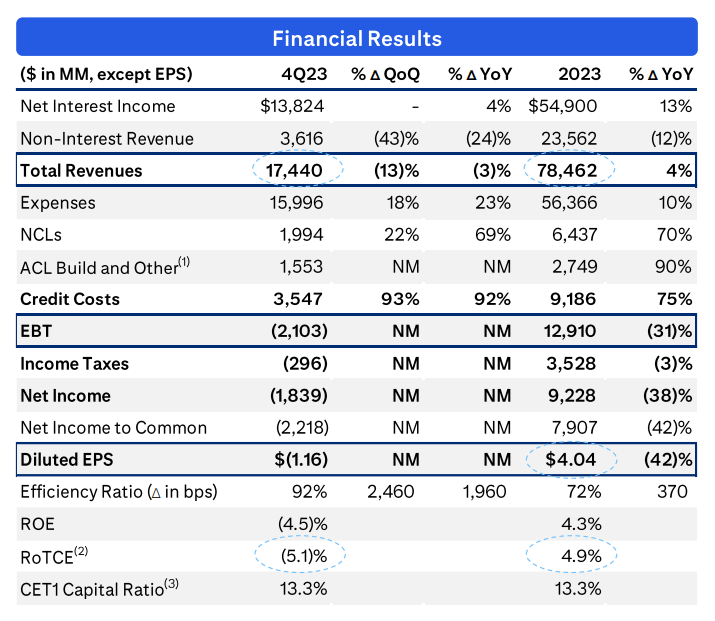

When looking at Citigroup's financials, I think it becomes clear very quickly that the bank had a rather bad fourth quarter. Citigroup's reported a loss of $1.84 billion and a per share loss of $1.16.

Though sales slid only a relatively minor 3% YoY in 4Q-23, Citigroup reported much higher expenses and higher credit costs, all of which create an underwhelming performance picture. Citigroup's return on equity was negative 4.5% and the bank's book value per share, as a consequence, declined 1% QoQ to $98.71.

{kind=link}

What Are Some Of Those Special Charges Booked Against Earnings In 4Q-23?

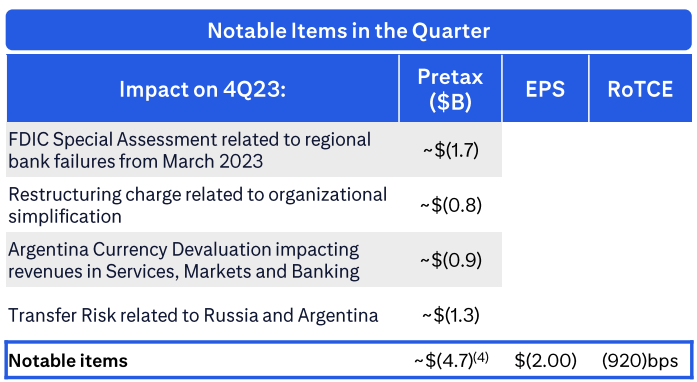

In the initial discussion of Citigroup's fourth quarter results, I pointed to the bank announcing a multitude of special charges that negatively impacted Citigroup's earnings profile, which I will now turn to.

In the fourth quarter, Citigroup recorded a charge of $1.7 billion related to the banking crisis, which requires large banks to top up the FDIC's rescue fund, an $800 million restructuring charge and a $0.9 billion Argentina currency charge.

Furthermore, Russia and Argentina-specific risks negatively affected Citigroup's fourth quarter profits to the tune of $1.3 billion.

These extraordinary charges, particularly the FDIC fee, should be one-time charges and should not pressure profits in the coming quarters, unless, of course, we would have to deal with a new financial crisis.

Notable Items In The Quarter (Citigroup)

{kind=link}

Net Interest Income

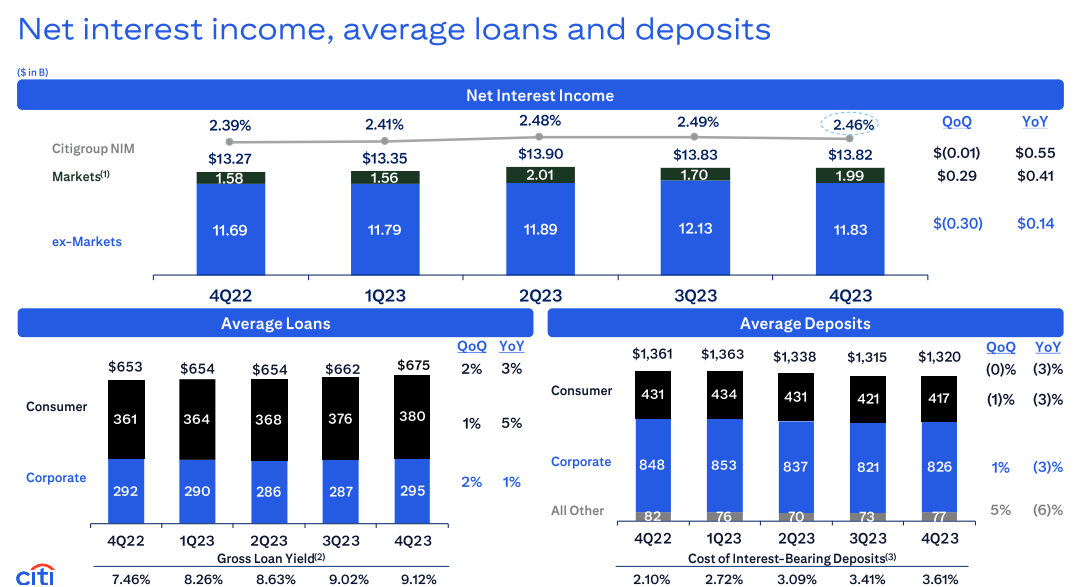

The trend in net interest income is negative which is a reflection of the central bank's slowly changing interest rate policy. The market is pricing in a decline in key interest rates in 2024 which unfortunately also reflects a headwind for Citigroup's net interest margin.

Citigroup's net interest margin came out at 2.46% in 4Q-23 compared to a margin of 2.49% in 3Q-23. Investors should expect Citigroup's net interest margin to decline in a falling-rate environment, which might create yet another headache for Citigroup.

Net Interest Income, Average Loans And Deposits (Citigroup)

{kind=link}

Citigroup would obviously profit from higher interest, a scenario possible under an inflation flare-up situation. Based on Citigroup's 10-Q report , the bank would profit from a 100 basis point instantaneous increase in interest rates to the tune of $1.30 billion (over a twelve months period) in terms of net interest income. An interest rate move to the downside would have the opposite effect on Citigroup's net interest income.

{kind=link}

Citigroup Is A Restructuring Investment And The Valuation Multiple Reflects This

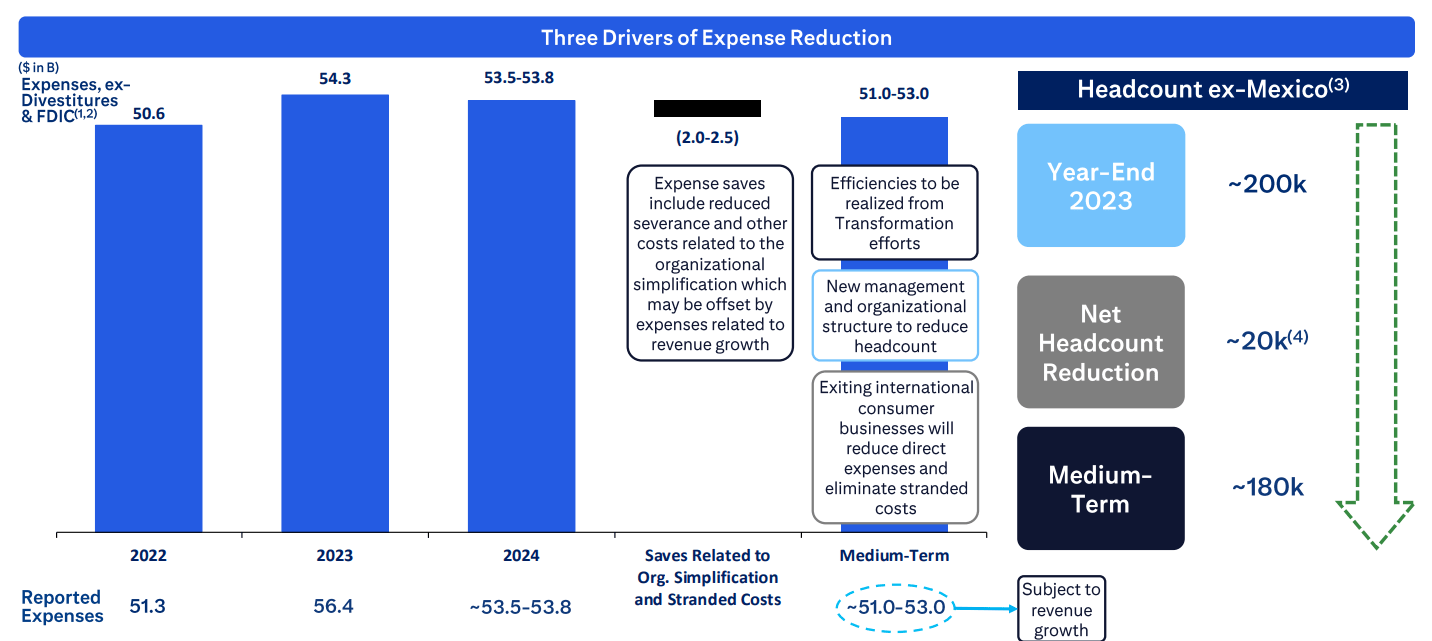

Citigroup's large extraordinary items that were booked against the bank's 4Q-23 earnings, totaling $4.7 billion, show that the Citigroup is, and will probably remain, a restructuring investment in 2024.

Citigroup anticipates at least $700 million and possibly up to $1.0 billion in severance and restructuring expenses in 2024 which would yield an expense target range of $53.5-53.8 billion this year. This implies, on a YoY basis, a decline in expenses of about 5%.

Citigroup said that it will cut its workforce by 10% in an obvious attempt to lower operating expenses and return the bank to a higher baseline of profitability.

Drivers Of Expense Reduction (Citigroup)

{kind=link}

Citigroup's restructuring status is reflected in the bank's valuation and other banks, like Bank of America Corp. ( BAC ) have pulled ahead. Citigroup is presently selling for a big book value discount of 47% whereas Bank of America is priced at just a 2% discount to book value.

The fact that Citigroup needs to keep cutting jobs in order to boost profitability is something that I think will weigh on the bank's outlook moving forward.

Obviously, the market is much more in favor of Bank of America and since Citigroup is still in the grip of its restructuring program, I think that Bank of America is the way better investment right now.

Some Risks That Need To Be Considered

Banks have cyclical profit profiles, at their core, so Citigroup, with or without a restructuring backdrop, is a risky investment.

Short-term interest rates are poised to drop in 2024 which would remove a catalyst for net interest income growth from Citigroup. However, on the flip side, if the central bank were to decide that key interest rates fall more slowly than expected, then Citigroup would have an opportunity to profit from a higher-for-longer rate period.

A successful restructuring and lower operating expenses might be reasons why investors change their attitudes towards Citigroup and why the stock might become a Buy.

Moving forward, my best guess is that Citigroup will continue to announce job cuts and focus on expense management to grow bank profitability.

My Conclusion

I don't think that Citigroup presently makes a strong value proposition for investors.

Though the banking crisis in 2023 was obviously not Citigroup's fault and the bank actually did reasonably well during this time, the negative 4Q-23 ROE, a litany of charges affecting the profit profile and the fact that short-term interest rates should be anticipated to weigh on Citigroup's net interest margin moving forward are reasons, in my view, to remain skeptical.

Citigroup announced major workforce cuts last week which continues to suggest that Citigroup may remain in a multi-year restructuring loop. I don't see any compelling reason to consider Citigroup at this point and therefore think that a stock classification of Sell is prudent.

For further details see:

Citigroup: Q4, Only A Restructuring Play Right Now