C - Citigroup: The Endless Restructuring Still Weights On The Valuation

2023-12-05 03:04:10 ET

Summary

- Citigroup is undergoing a restructuring process to reduce management layers, streamline its global footprint, and cut excess headcount.

- The effort to reduce senior headcount and cut reporting lines is causing confusion and may not lead to significant cost reductions.

- Citigroup's comparable valuation and positioning are not good enough to pick it against other competitors.

Citigroup (C) is undergoing a new restructuring process under Jane Fraser’s aim to reduce management layers, streamline the global footprint, and aggressively cut excess (senior) headcount. We already heard this kind of news in the past, and Citi has long been part of endless efforts to improve its structure while growing its business. After running a careful comparative analysis, we concluded that the current valuation is not low enough to account for uncertainties and the overall weakness of the bank. Far better opportunities are lying on the market even in similar banking stocks.

The ongoing effort: reducing, streamlining, and improving will be harder than expected

One of the key facts that investors were highlighting about Citi is the complex managerial and reporting structures that governed the bank. Given its vast global footprint, the bank clearly needs an articulated oversight, but Citi went above and beyond. Almost all of the key “head” roles across the major markets - North America, Asia, and Europe - were occupied by two people (co-heads). The other key issue was reporting lines. While it is fundamental for a large bank to keep checks and compliance of top quality, it is easy to generate recurring, redundant activities that slow down processes and increase costs.

To face these two problems, Jane Fraser decided to act in two main ways: (1) reduce senior headcount, and (2) cut reporting lines. But so far we are noticing some confusion as the news covering the ongoing efforts are highlighting. This week eFinancialCareers reported the words of a senior banker at Citi with knowledge of the matters:

This seems to have been a way of reorganizing themselves into a group that vaguely resembles what Jane wants but without anyone actually leaving, it's just chairs being moved around.

The main issue seems to be that senior people like co-heads are being removed to be placed in non-executive roles. This will do very little in terms of cost reductions and instead keep an even more confusing working environment. Also, it is unclear if second and third tiers co-head structures will be actually removed, making the efforts to reduce reporting weaker.

Also, the banker goes on to say:

In the old world, the geographical entity had all the power. Now, it's the sector teams that have priority

The other key weakness of Citigroup is its complex and vast global footprint. It is the key to any restructuring plan to simplify that. However, it seems the case that it is not happening yet. Instead, it looks like they are simply inverting the hierarchy direction of reporting instead of cutting “middlemen”.

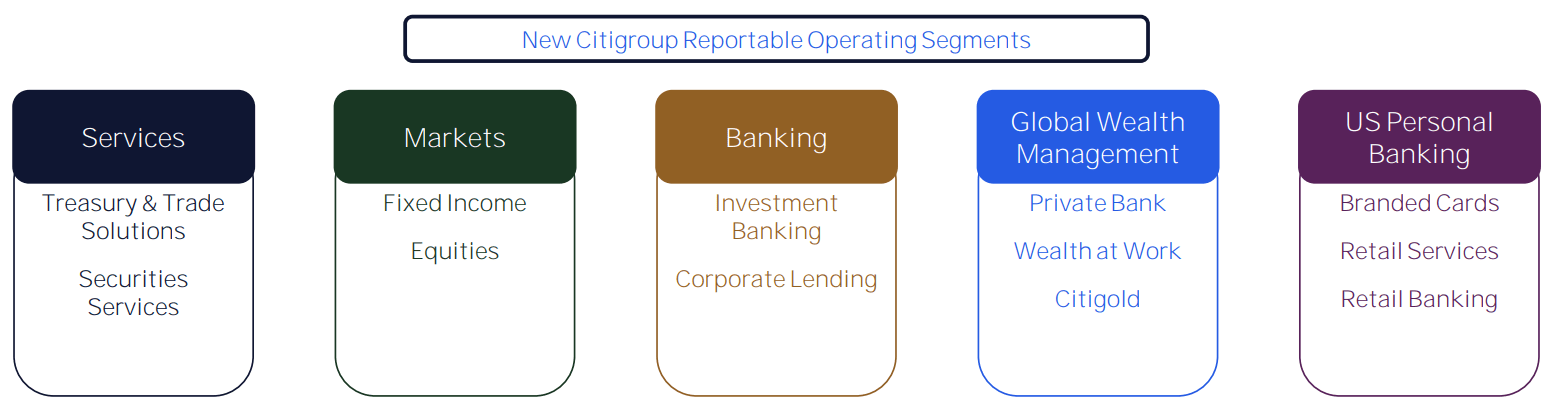

Last but not least, Citi has also announced its new reportable segments.

{kind=link}

These will be the new ones from the end of 2023, and will probably complement and then substitute the current segments. We appreciate this form, clearly much cleaner than the previous structure, and better for communicating to investors where the successes (and the losses) are coming from. Today the Institutional Clients Group is responsible for a disproportionate amount of revenues compared to the other segments, accounting for around 50% of the total.

The comparative analysis

To put these concerns in perspective we want to analyze Citi on a comparative basis. This means picking its most similar peers and running a check on important metrics. Indeed, we believe that in the case of large banking stocks, they are all more or less exposed to the same systemic and idiosyncratic drivers of results. This means that choosing the top-quality names or the ones with the best risk-reward is the best strategy. For Citi, we want to assess if the current restructuring, along with the current valuation, offers an interesting risk-adjusted yield compared to others.

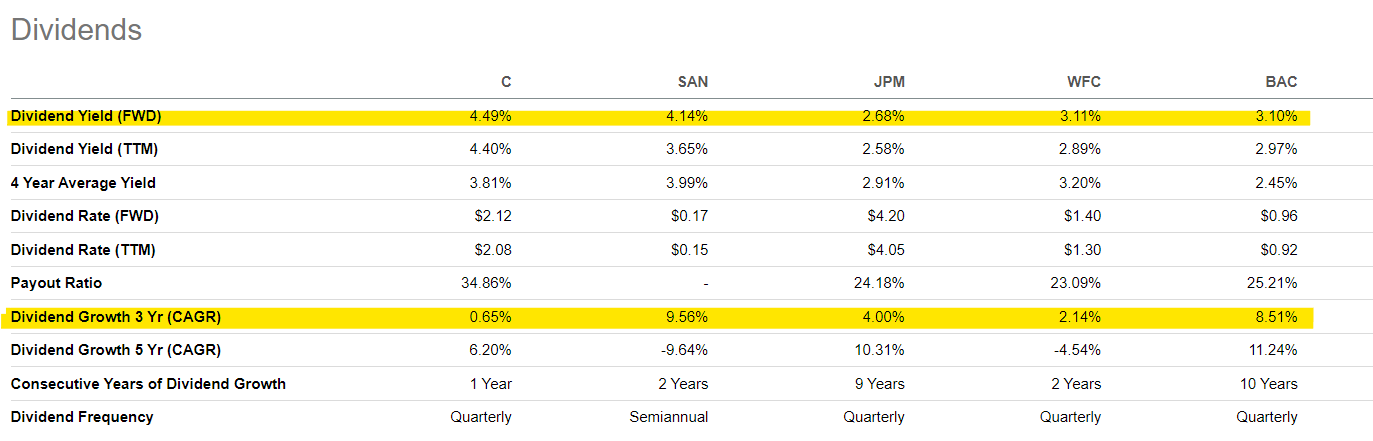

The comparables will be JPMorgan, Wells, Fargo, Bank of America, and Santander. We included the last one to include other geographical exposure other than North America as Citi is highly diversified.

{kind=link}

The first factor is dividends. Banks experienced windfall profits since mid-2022 as a result of rising rates, and now dividend yields are sitting at relatively generous levels. Citi has the highest yield among its peers, at around 4.5%. This represents around a 150-200 bps premium compared to Wells Fargo, JPM, and Bank of America. However, if we look at the ability to grow dividends over time, and thus increase its yield, we notice that Citigroup is notoriously slow and severely underperforming. In the last 3 years, BAC and JPM grew at 8% and 4% respectively, while Citi remained well below 1%. The 5 years comparison is also underperforming.

To put things in perspective, this is the difference between a 0.65% and 4% growth rate in the long run. That is, growing the current Citi’s dividend at its own rate or JPMorgan’s.

Dividend Growth Example (Author's Own Model)

While most of us certainly don’t have a time frame that extends to 2060, it is useful to see the importance of growth, even in the short and medium term.

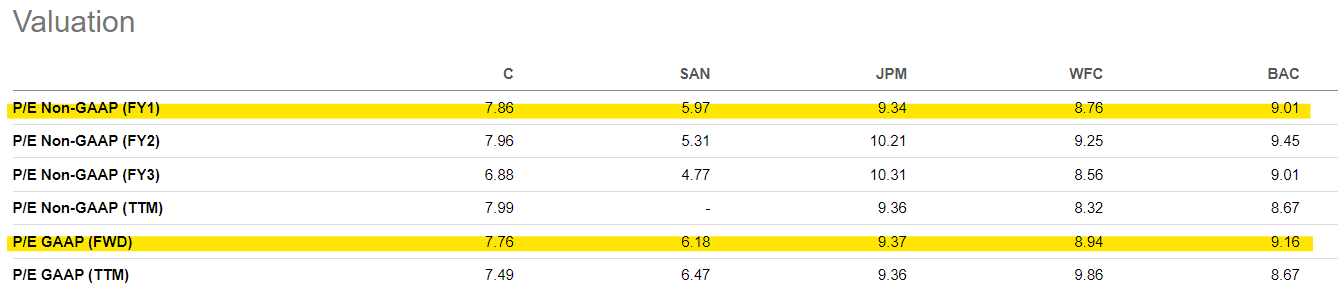

Now we focus on valuation metrics, particularly P/E.

{kind=link}

As we expected, Citi is again on the cheapest side of the spectrum. By inverting the ratio, we can extract the earnings yield. While JPM and BAC stand at 10.7% and 11% respectively, Citi is at 12.7%. Again we notice a difference below 300 bps, which means we are paid a premium of around 3% to buy a restructuring bank with a much more complex structure and a suboptimal growth rate.

What could go right: the upside scenario

While we have concerns about the ongoing restructuring, and we think the current valuation is not low enough, there is still some upside. In particular, we spot two possible strengths that may benefit Citi’s shareholders more than the other comparables. The success of the streamlining efforts could indeed trigger two main advantages: (1) margin expansion as costs are reduced with little impact on revenues, and (2) the market will re-rate Citi’s valuation multiples.

There is some sort of a double upside in case the current management is able to reach all the objectives of the current plan. This is because not only the bank will benefit from lower compensation, compliance, and administrative expenses, but the market will also praise it with higher valuations. So in that scenario, investors should expect higher returns than the other public comparables.

Conclusion

Citigroup is again undergoing a lengthy and complex process to deeply change its structure deeply and improve efficiency. We believe we have heard this story many times and it should be taken with a grain of skepticism by shareholders. At the same time, we also think other similar comparables offer better risk/reward opportunities as Citi’s valuation is still not low enough. We remain on watch waiting either for developments on the business or the valuation.

For further details see:

Citigroup: The Endless Restructuring Still Weights On The Valuation